SOLUTION

(20 min.) Fixed cost allocation.

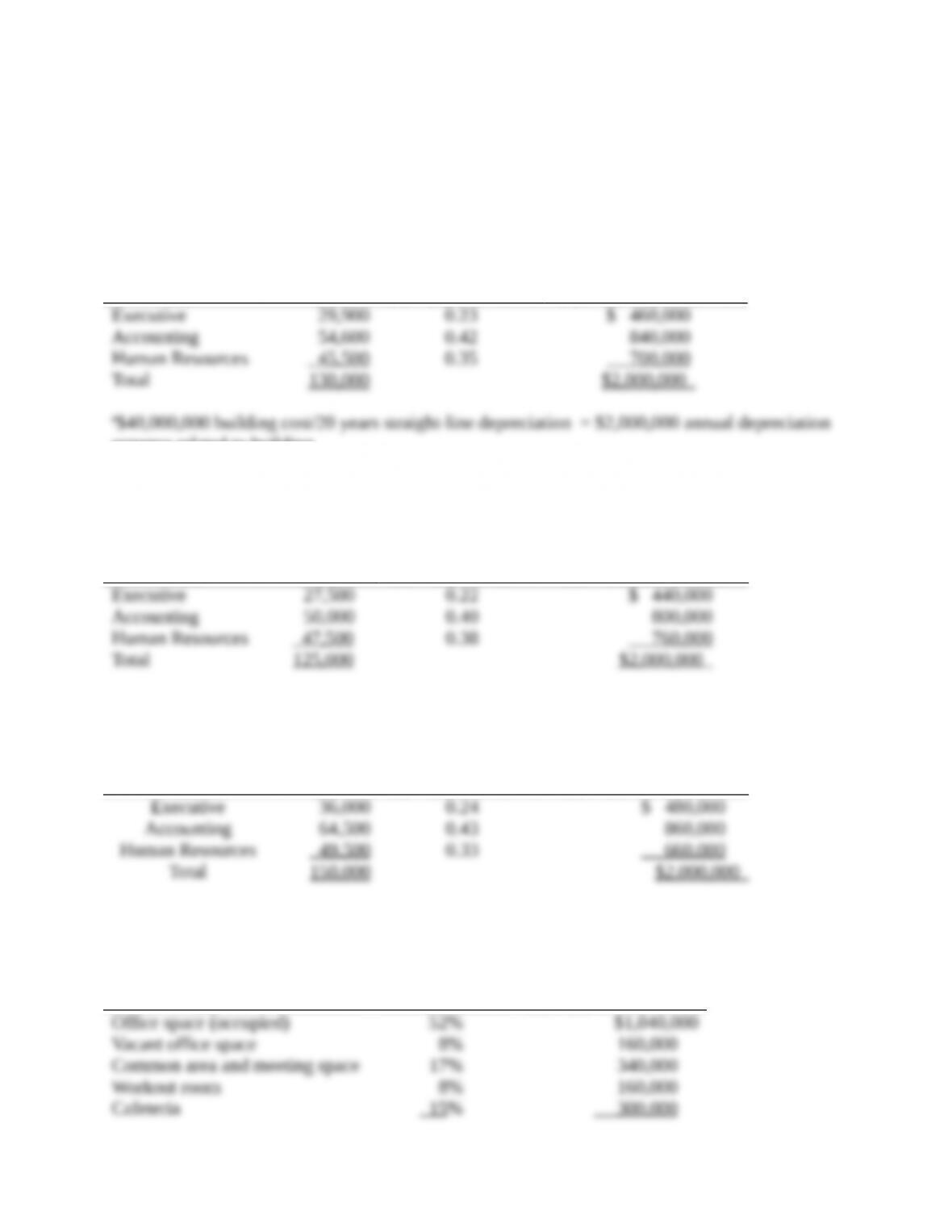

1. i) Allocation using actual usage.

Department

(1)

Actual

Usage

(2)

Percentage of

Total Usage

(3) = (2) ÷ 130,000

Allocation

(4) = (3) × $2,000,000a

expense related to building.

ii) Allocation using planned usage.

Department

(1)

Planned

Usage

(2)

Percentage of

Total Usage

(3) = (2) ÷ 125,000

Allocation

(4) = (3) × $2,000,000

iii) Allocation using practical capacity.

Department

(1)

Practical

Capacity

(2)

Percentage of

Total Usage

(3) = (2) ÷ 150,000

Allocation

(4) = (3) × $2,000,000

2.

Usage of Space

(1)

Percentage of

Total Building

Space

(2)

Total Annual

Building Cost

(3) = (2) × $2,000,000

15-1

a) $160,000 of Vacant Office Space cost will not be allocated to the departments but will be

absorbed by the university’s central administration.

b) Allocation of Office space (occupied) costs ($1,040,000) using actual usage.

Department

(1)

Actual

Usage

(2)

Percentage of

Total Usage

(3) = (2) ÷ 130,000

Allocation

(4) = (3) × $1,040,000

c) Allocation of all common space cost such as common area and meeting space, workout room,

and cafeteria ($340,000 + $160,000 + $300,000 = $800,000) using practical capacity.

Department

(1)

Practical

Capacity

(2)

Percentage of

Total Usage

(3) = (2) ÷ 150,000

Allocation

(4) = (3) × $800,000

Department

(1)

Allocated Cost of

Occupied Office Space

(2)

Allocated Cost of

Common Space

(3)

Total Cost Allocated to

Department

(4) = (2) + (3)

The departments would likely consider portions of the allocation method used here “fair.”

In particular, the individual departments do not pay for unused office space that is intended for

As for the allocation of occupied office space costs, it may have been more appropriate to

15-2

assignment of the cost will change year to year under the present system, depending on that

Finally, allocating the common space cost based on practical capacity is the most

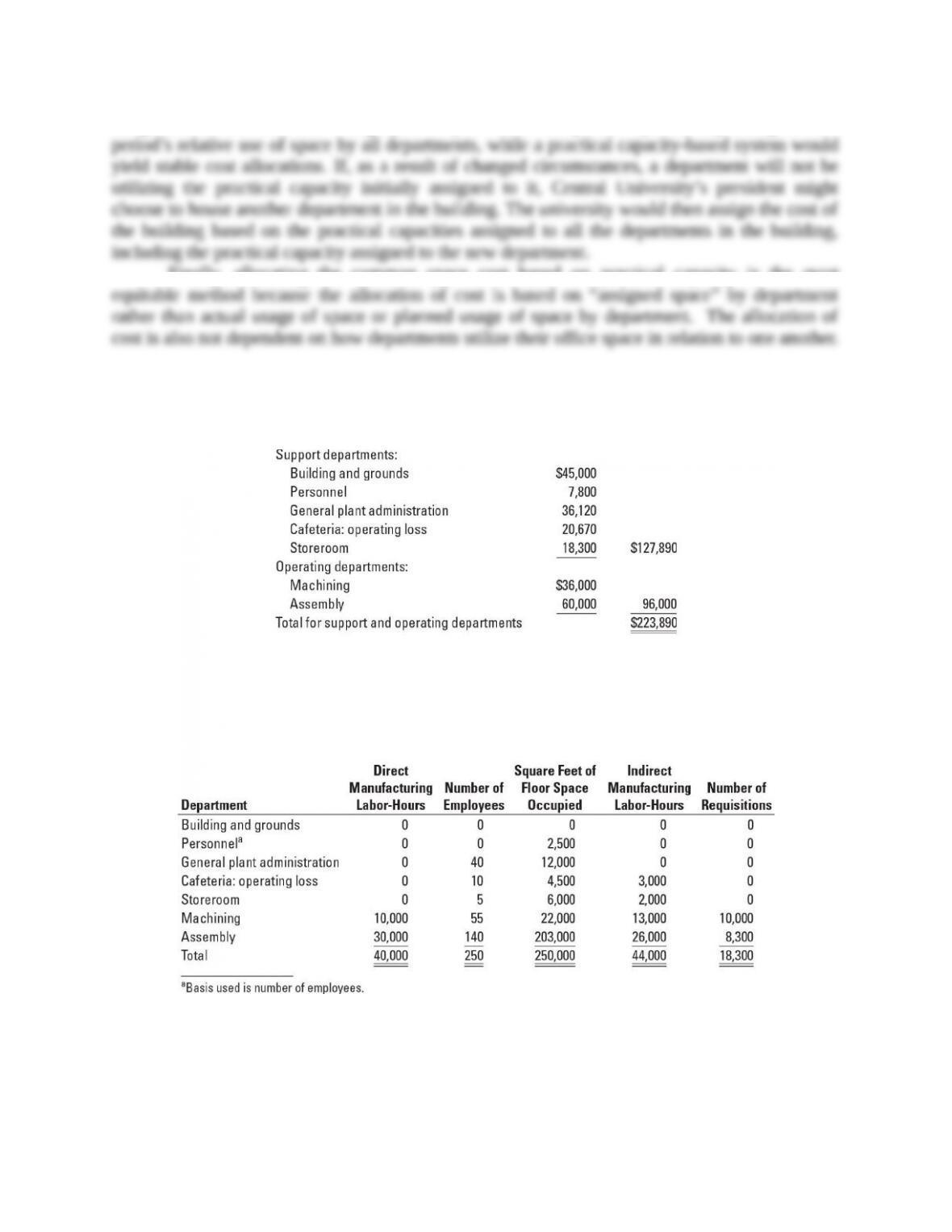

15-30 Allocating costs of support departments; step-down and direct methods. The Eastern

Summit Company has prepared department overhead budgets for budgeted-volume levels before

allocations as follows:

Management has decided that the most appropriate inventory costs are achieved by using

individual-department overhead rates. These rates are developed after support-department costs

are allocated to operating departments.

Bases for allocation are to be selected from the following:

15-3

Required:

1. Using the step-down method, allocate support-department costs. Develop overhead rates per

direct manufacturing labor-hour for machining and assembly. Allocate the costs of the

support departments in the order given in this problem. Use the allocation base for each

support department you think is most appropriate.

2. Using the direct method, rework requirement 1.

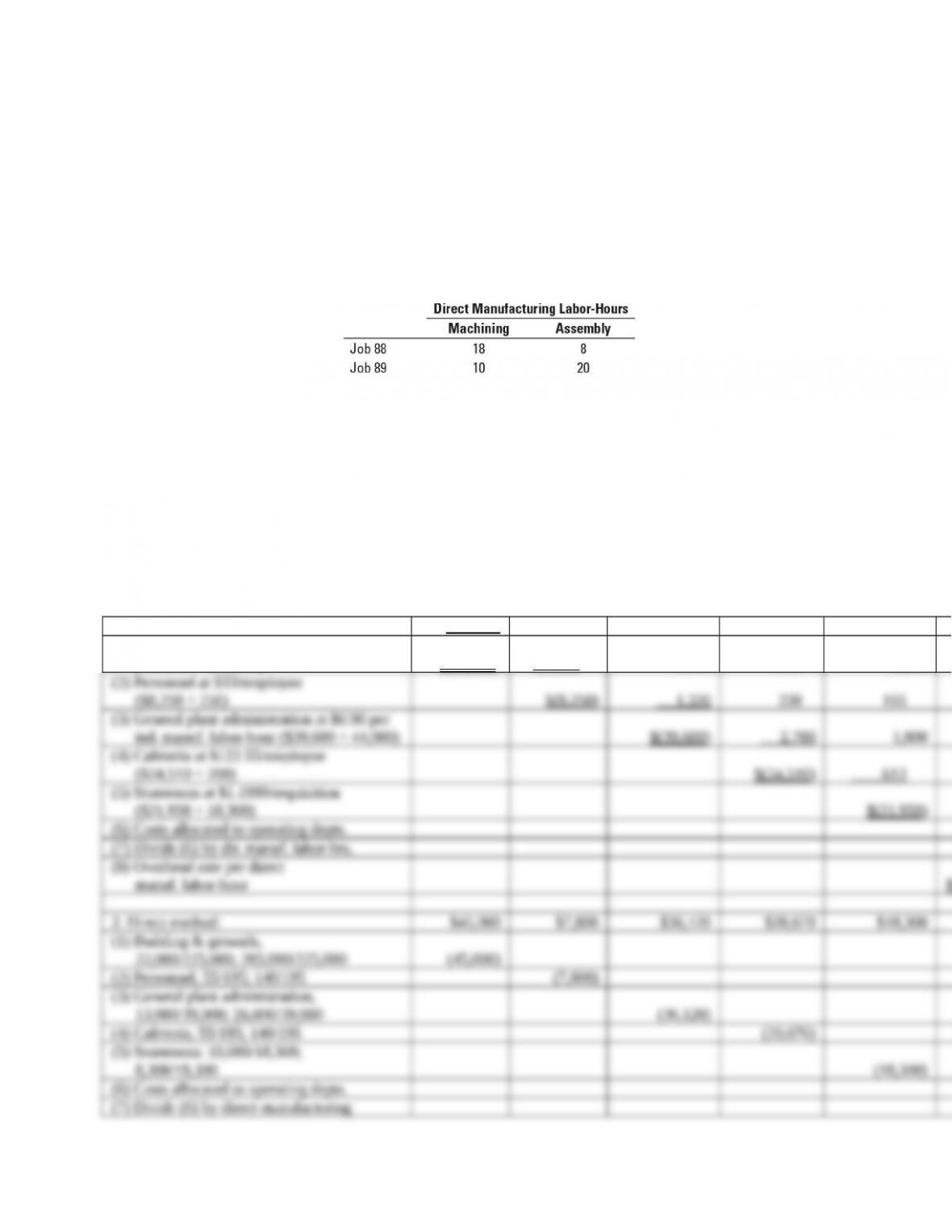

3. Based on the following information about two jobs, determine the total overhead costs for

each job by using rates developed in (a) requirement 1 and (b) requirement 2.

4. The company evaluates the performance of the operating department managers on the basis

of how well they managed their total costs, including allocated costs. As the manager of the

Machining Department, which allocation method would you prefer from the results obtained

in requirements 1 and 2? Explain.

SOLUTION (45 min.) Allocating costs of support departments; step-down and direct

methods.

Building &

Grounds Personnel

General Plant

Admin.

Cafeteria

Operating

Loss Storeroom

1. Step-down Method: $ 45 ,000 $7,800 $ 36,120 $ 20,670 $18,300

(1) Building & grounds at $0.18/sq.ft.

($45,000 ÷ 250,000) $(45 ,000) 450 2,160 810 1,080

15-4

labor-hours

(8) Overhead rate per direct

manufacturing labor-hour $ 7.047

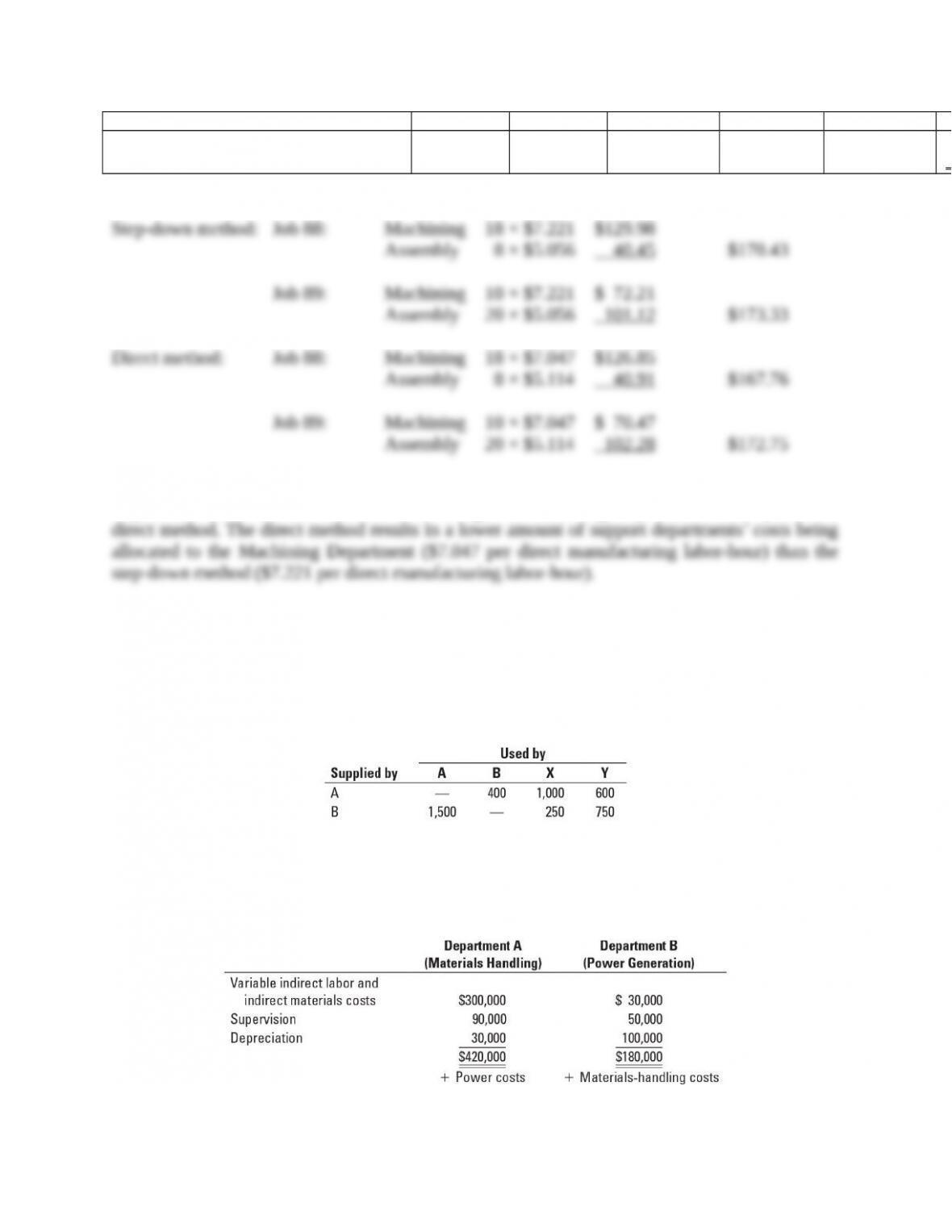

3 Comparison of Methods:

4. Compare the overhead rate, per direct manufacturing labor-hour, for the Machining

Department under the two methods. The manager of Machining Department would prefer the

15-31 Support-department cost allocations; single-department cost pools; direct,

step-down, and reciprocal methods. The Martinez Company has two products. Product 1 is

manufactured entirely in department X. Product 2 is manufactured entirely in department Y. To

produce these two products, the Martinez Company has two support departments: A (a

materials-handling department) and B (a power-generating department).

An analysis of the work done by departments A and B in a typical period follows:

The work done in department A is measured by the direct labor-hours of materials-handling time.

The work done in department B is measured by the kilowatt-hours of power. The budgeted costs

of the support departments for the coming year are as follows:

15-5

The budgeted costs of the operating departments for the coming year are $2,500,000 for

department X and $1,900,000 for department Y.

Supervision costs are salary costs. Depreciation in department B is the straight-line

depreciation of power-generation equipment in its 19th year of an estimated 25-year useful life;

it is old, but well-maintained, equipment.

Required:

1. What are the allocations of costs of support departments A and B to operating departments X

and Y using (a) the direct method, (b) the step-down method (allocate department A first), (c)

the step-down method (allocate department B first), and (d) the reciprocal method?

2. An outside company has offered to supply all the power needed by the Martinez Company

and to provide all the services of the present power department. The cost of this service will

be $80 per kilowatthour of power. Should Martinez accept? Explain.

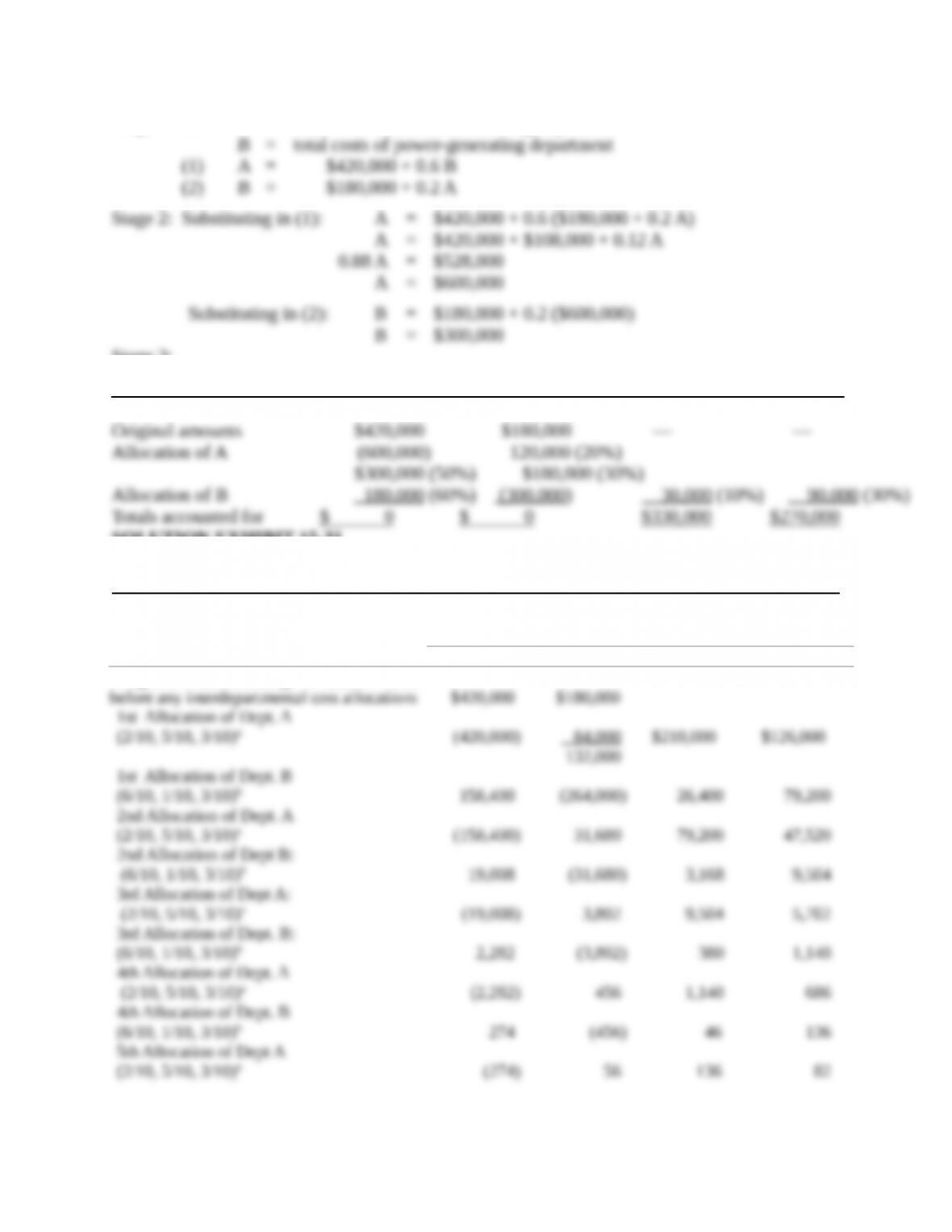

SOLUTION

(40-60 min.) Support-department cost allocations; single-department cost pools; direct,

step-down, and reciprocal methods.

All the following computations are in dollars.

1.

Direct method:

To X To Y

Step-down method, allocating A first:

A B X Y

Step-down method, allocating B first:

A B X Y

Note that these methods produce significantly different results, so the choice of method may

frequently make a difference in the budgeted department overhead rates.

Reciprocal method:

15-6

Stage 1: Let A = total costs of materials-handling department

Stage 3:

A B X Y

SOLUTION EXHIBIT 15-31

Reciprocal Method of Allocating Support Department Costs for Martinez Company Using

Repeated Iterations.

Support Departments Operating Departments

AB X Y

Budgeted manufacturing overhead costs

15-7

Total accounts allocated and reallocated (the numbers in parentheses in first two columns)

Dept A; Materials Handling: $420,000 + $158,400 + $19,008 + $2,282 + $274 + $34 + $4 = $600,000

Dept B; Power Generation: $264,000 + $31,680 + $3,802 + $456 + $56 + $6 = $300,000

Comparison of methods:

Method of Allocation X Y

2. It appears that the cost of power is $72 per kilowatt-hour ($180,000 ÷ 2,500 Kwh) plus the

material handling costs. But Martinez should make the decision after considering the effects of

the interdependencies and the fixed costs. Note that the power needs would be less (students

frequently miss this) if they were purchased from the outside:

Outside

Power Units

Needed Needed

In contrast, the total costs that would be saved by not producing the power inside would depend

on the effects of the decision on various costs:

15-8

Avoidable Costs of

2,500 Units of Power

Produced Inside

Variable indirect labor and indirect material costs

Supervision in power department

Materials handling, 20% of $300,000*

Probable minimum cost savings

Possible additional savings:

a. Can any supervision in materials handling be saved

because of overseeing less volume?

Minimum savings is probably zero; the maximum is

probably 20% of $90,000 or $18,000.

b. Is any depreciation a truly variable, wear-and-tear type of

cost?

Total savings by not producing 2,500 units of power

$ 30,000

50,000

60 ,000

$140,000

?

?

________

$140 ,000

+ ?

* Materials handling costs are higher because the power department uses 20% of materials handling. Therefore,

materials-handling costs will decrease by 20%.

In the short run (at least until a capital investment in equipment is necessary), the data

suggest continuing to produce internally because the costs eliminated would probably be less

than the comparable purchase costs.

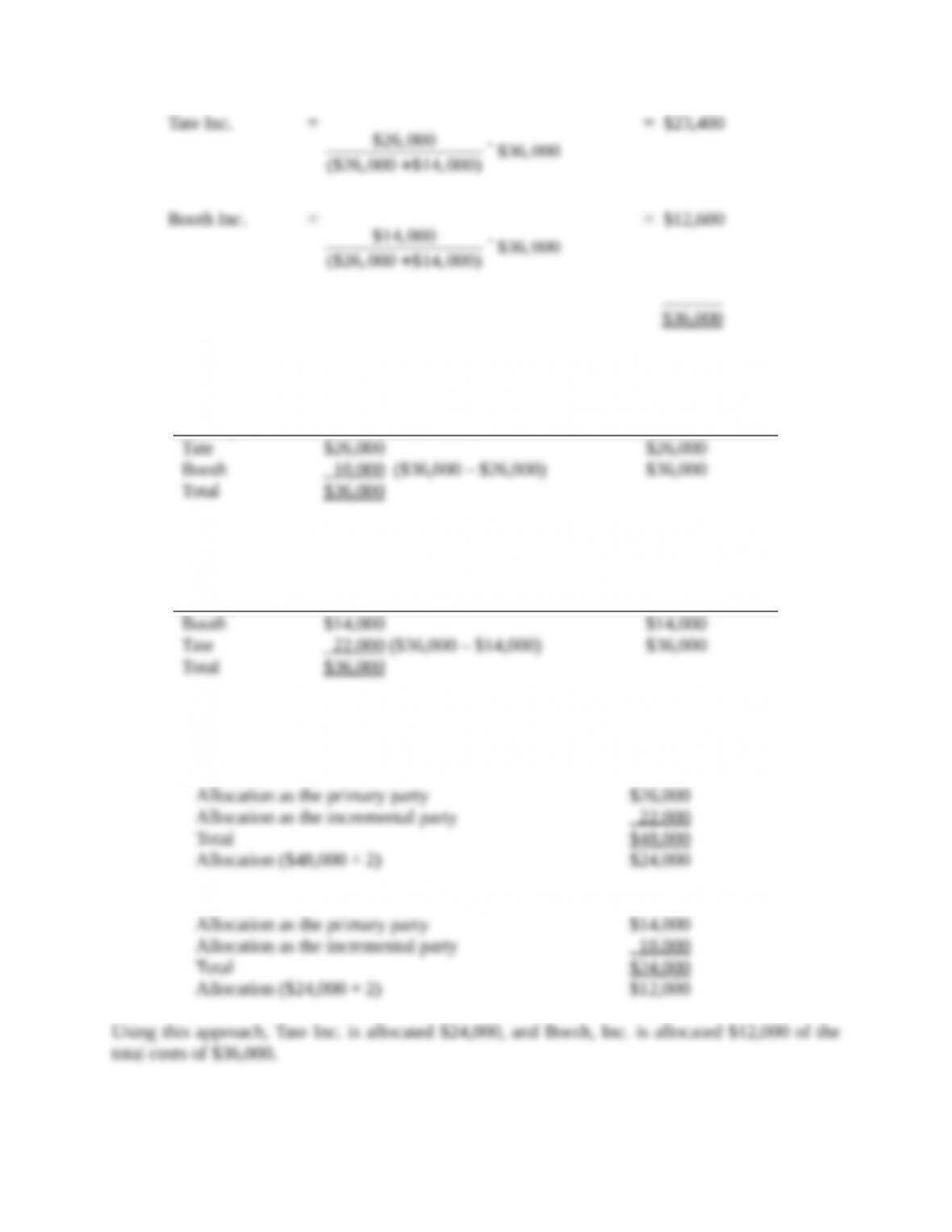

15-32 Common costs. Tate Inc. and Booth Inc. are two small manufacturing companies that are

considering leasing a cutting machine together. If Tate rents the machine on its own, it will cost

$26,000. If Booth rents the machine alone, it will cost $14,000. If they rent the machine together,

the cost will decrease to $36,000.

Required:

1. Calculate Tate’s and Booth’s respective share of fees under the stand-alone cost-allocation

method.

2. Calculate Tate’s and Booth’s respective share of fees using the incremental cost-allocation

method assuming (a) Tate is the primary party and (b) Booth is the primary party.

3. Calculate Tate’s and Booth’s respective share of fees using the Shapley value method.

4. Which method would you recommend Tate and Booth use to share the fees?

SOLUTION

(25 min.) Common costs.

1. Stand-alone cost-allocation method.

15-9

2. With Tate Inc. as the primary party:

Party Costs Allocated

Cumulative Costs

Allocated

With Booth Inc. as the primary party:

Party Costs Allocated

Cumulative Costs

Allocated

3. To use the Shapley value method, consider each party as first the primary party and then

the incremental party. Compute the average of the two to determine the allocation.

Tate Inc.:

Booth Inc.:

15-10

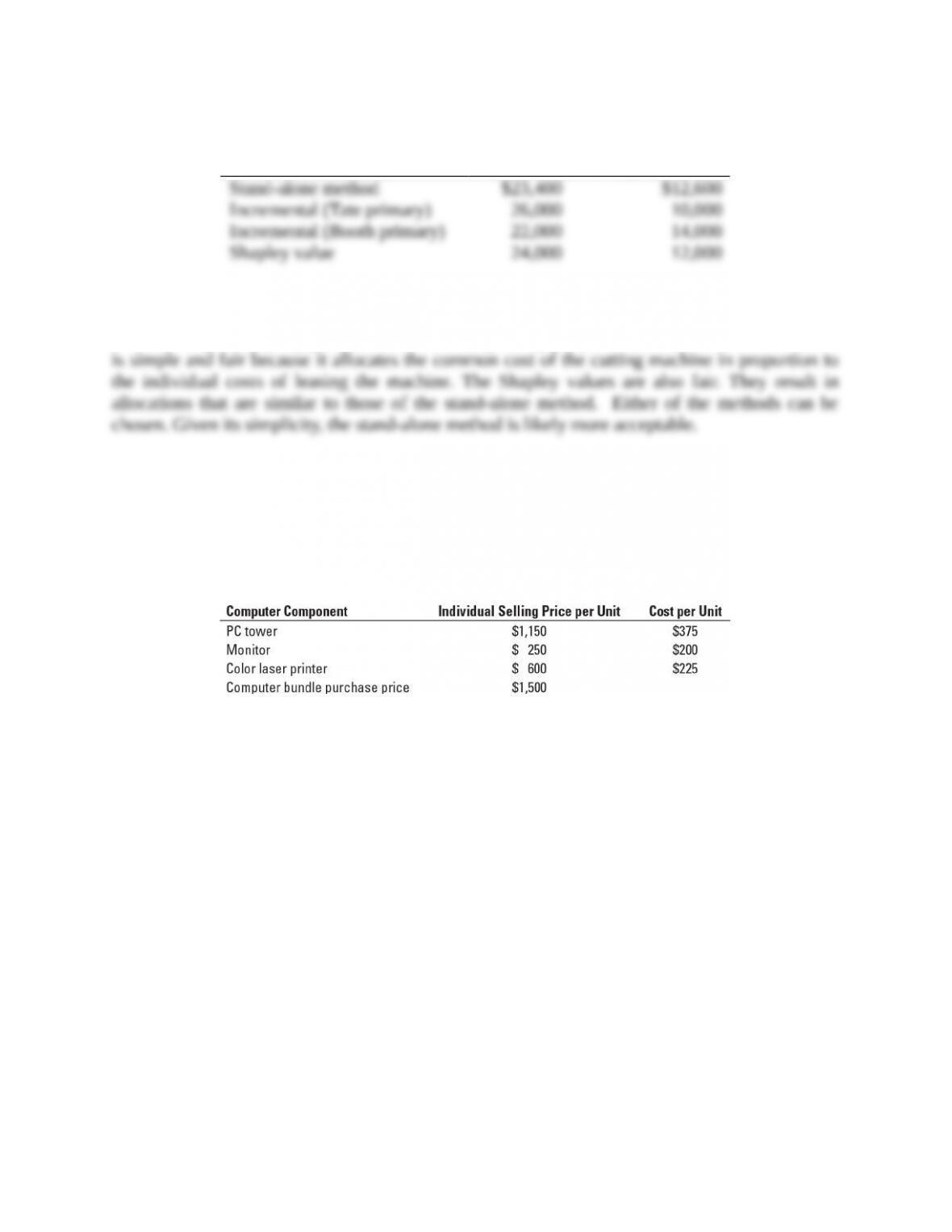

4. The results of the four cost-allocation methods are shown below.

Tate Inc. Booth Inc.

The allocations are very sensitive to the method used. With the incremental cost-allocation

method, Tate Inc. and Booth Inc. would probably have disputes over who is the primary party

because the primary party gets allocated all of the primary party’s costs. The stand-alone method

15-33 Stand-alone revenue allocation. Magic Systems, Inc., sells computer hardware to end

consumers. The CX30 is sold as a “bundle,” which includes three hardware products: a personal

computer (PC) tower, a 26-inch monitor, and a color laser printer. Each of these products is

made in a separate manufacturing division of Magic Systems and can be purchased individually

as well as in a bundle. Magic Systems sells roughly equal quantities of the three products. The

individual selling prices and per unit costs are as follows:

Required:

1. Allocate the revenue from the computer bundle purchase to each of the hardware products

using the stand-alone method based on the individual selling price per unit.

2. Allocate the revenue from the computer bundle purchase to each of the hardware products

using the stand-alone method based on cost per unit.

3. Allocate the revenue from the computer bundle purchase to each of the hardware products

using the stand-alone method based on physical units (that is, the number of individual units

of product sold per bundle).

4. Which basis of allocation makes the most sense in this situation? Explain your answer.

15-11