SOLUTION

(40 min.) Variable costing versus absorption costing.

2017 Production = Sales + Ending Inventory – Beginning Inventory

1. Absorption Costing:

Garvis Company Income Statement

For the Year Ended December 31, 2017

Cost of goods sold:

Operating costs:

a $6.00 + ($14.00 ÷ 20) = $6.00 + $0.70 = $6.70

2. Variable Costing:

Garvis Company Income Statement

For the Year Ended December 31, 2017

Variable cost of goods sold:

Variable manufacturing costs

Fixed costs:

3. The difference in operating income between the two costing methods is:

=

The absorption-costing operating income exceeds the variable costing figure by $14,000 because

of the increase of $14,000 during 2017 of the amount of fixed manufacturing costs in ending

inventory vis-a-vis beginning inventory.

4.

5. Absorption costing is more likely to lead to buildups of inventory than does variable costing.

Absorption costing enables managers to increase reported operating income by building up

inventory which reduces the amount of fixed manufacturing overhead included in the current

period’s cost of goods sold.

Ways to reduce this incentive include

9-33 Throughput Costing (continuation of 9-32)

Required:

1. Prepare an income statement under throughput costing for the year ended December 31, 2017

for Garvis Company

2. Reconcile the different between the contribution margin and throughput margin for Garvis in

2017. Then reconcile the operating income between variable costing and throughput costing

for Garvis in 2017.

3. Advocates of throughput costing say it provides managers less incentive to produce for

inventory than either variable costing or, especially, absorption costing. Do you agree? Why

or why not? Under what circumstances might you recommend that Garvis use throughput

costing?

SOLUTION

(20 min.) Throughput costing.

1. Throughput Costing:

Garvis Company Income Statement

For the Year Ended December 31, 2017

Direct material cost of goods sold:

a 1,100,000 × $4.50

b 80,000 × $4.50

c (1,100,000 × $1.50) + $840,000

d (1,080,000 × $2) + $240,000

2.

Garvis Company – Reconciliation Contribution/Throughput

Margin

Operating Income

Reasons for differences:

Variable Manufacturing Cost (other than

materials) (1,080,000 × $1.50)

$1,620,000

Lower expensing of Variable Manufacturing

Cost (other than materials) under Variable

costing: 20,000 units increase in inventory

during the year × $1.50 per unit

$ (30,000)

3 Yes, I do agree. Because fixed manufacturing costs are expensed in the period incurred under

throughput costing, there is no opportunity for managers to affect operating income by

manipulating production levels. When a significant majority of an item’s cost is direct materials,

when direct labor is really more fixed than variable (you have staff for direct labor and you don’t

9-34 Variable costing and absorption costing, the Z-Var Corporation.

(R. Marple, adapted) It is the end of 2017. Z-Var Corporation began operations in January 2016.

The company is so named because it has no variable costs (Zero VARiable). All its costs are

fixed; they do not vary with output.

Z-Var Corp. is located on the bank of a river and has its own hydroelectric plant to supply

power, light, and heat. The company manufactures a synthetic fertilizer from air and river water

and sells its product at a price that is not expected to change. It has a small staff of employees, all

paid fixed annual salaries. The output of the plant can be increased or decreased by pressing a few

buttons on a keyboard.

The following budgeted and actual data are for the operations of Z-Var. The company uses

budgeted production as the denominator level and writes off any production-volume variance to

cost of goods sold.

2016 2017a

Sales 30,000 tons 30,000 tons

Production 60,000 tons 0 tons

Selling price $ 90 per ton $ 90 per ton

Costs (all fixed):

Manufacturing $2,580,000 $2,580,000

Operating (nonmanufacturing) $ 102,000 $ 102,000

a Management adopted the policy, effective January 1, 2017, of producing only as

much product as needed to fill sales orders. During 2017, sales were the same as for

2016 and were filled entirely from inventory at the start of 2017.

Required:

1. Prepare income statements with one column for 2016, one column for 2017, and one column

for the two years together using (a) variable costing and (b) absorption costing.

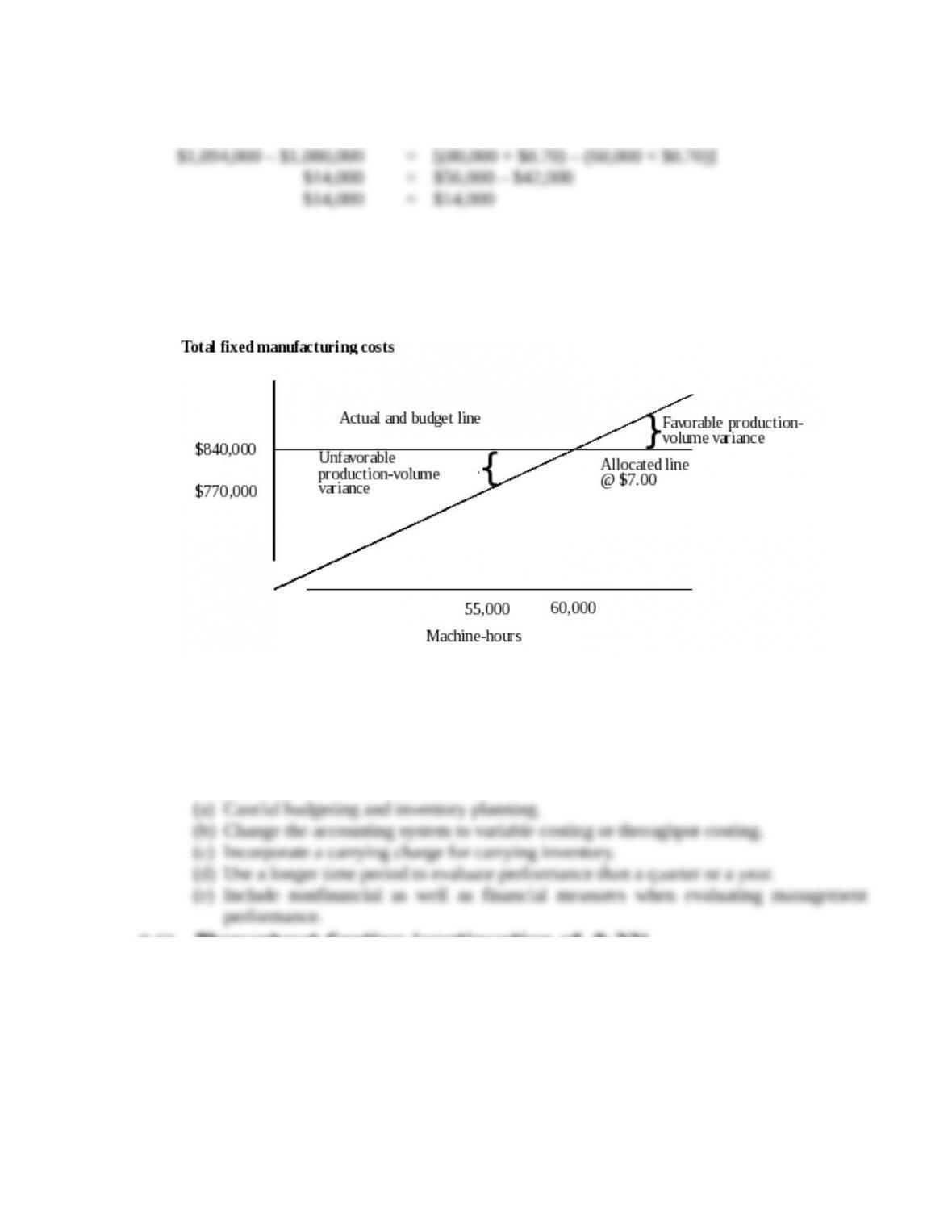

2. What is the breakeven point under (a) variable costing and (b) absorption costing?

3. What inventory costs would be carried in the balance sheet on December 31, 2016 and 2017

under each method?

4. Assume that the performance of the top manager of Z-Var is evaluated and rewarded largely

on the basis of reported operating income. Which costing method would the manager prefer?

Why?

SOLUTION

(40 min.) Variable costing and absorption costing, the Z-Var Corporation.

This problem always generates active classroom discussion.

1. The treatment of fixed manufacturing overhead in absorption costing is affected primarily

by what denominator level is selected as a base for allocating fixed manufacturing costs to units

produced. In this case, is 30,000 tons per year, 60,000 tons, or some other denominator level the

most appropriate base?

We usually place the following possibilities on the board or overhead projector and then

a. Variable-Costing Income Statement:

2016 2017 Together

Revenues (and contribution margin) $2,700,000 $2,700,000 $5,400,000

Fixed costs:

Manufacturing costs $2,580,00

0

Operating costs

2,682,000 2,682,000 5,364,000

b. Absorption-Costing Income Statement:

The ambiguity about the 30,000- or 60,000-unit denominator level is intentional. IF YOU WISH,

THE AMBIGUITY MAY BE AVOIDED BY GIVING THE STUDENTS A SPECIFIC

DENOMINATOR LEVEL IN ADVANCE.

Alternative 1. Use 60,000 units as a denominator; fixed manufacturing overhead per unit is

$2,580,000 60,000 = $43.

2016 2017 Together

Cost of goods sold

(60,000 × $43; 0 × $43)

Deduct ending inventory

(30,000 × $43; 0 × $43)

(1,290,000)

— —

Adjustment for production-volume varianceb 0 2 ,580,000

U

2 ,580,000 U

Alternative 2. Use 30,000 units as a denominator; fixed manufacturing overhead per unit is

$2,580,000 30,000 = $86.

2016 2017 Together

Cost of goods sold

(60,000 × $86; 0 × $86)

Deduct ending inventory

(30,000 × $86; 0 × $86)

(2,580,000)

— —

Adjustment for production-volume varianceb (2 ,580,000) F 2 ,580,000

U

0

a Inventory carried forward from 2016 and sold in 2017

Note that operating income under variable costing follows sales and is not affected by

inventory changes.

2.

costing

ableunder vari

pointBreakeven

=

per tonmargin on Contributi

costs Fixed

=

$2,682,000

$90

Most students will say that the breakeven point is 29,800 tons per year under both

absorption costing and variable costing. The logical question to ask a student who answers

29,800 tons for variable costing is: “What operating income do you show for 2016 under

absorption costing?” If a student answers $1,308,000 (alternative 1 above), or $2,598,000

Given that sales are expected to be 30,000 tons, let us solve for the production level that will

provide a breakeven level of zero operating income. Using the formula in the chapter, sales of

Let P = Production level

=

( )

Total Fixed Target Fixed Manuf. Breakeven Units

Cost OI Cost Rate Sales in Units Produced

Contribution Margin Per Unit

é ù

+ + ´ –

ê ú

ë û

Proof:

Gross margin, 2,171 × ($90 – $43) $102,037

Production-volume variance $ 0

We find it helpful to put the following comparisons on the board:

Variable costing breakeven = f(sales)

Absorption costing breakeven = f(sales and production)

3. Absorption costing inventory cost: Either $1,290,000 or $2,580,000 at the end of 2016

depending on the chosen denominator level, and zero at the end of 2017.

4. Operating income is affected by both production and sales under absorption costing.

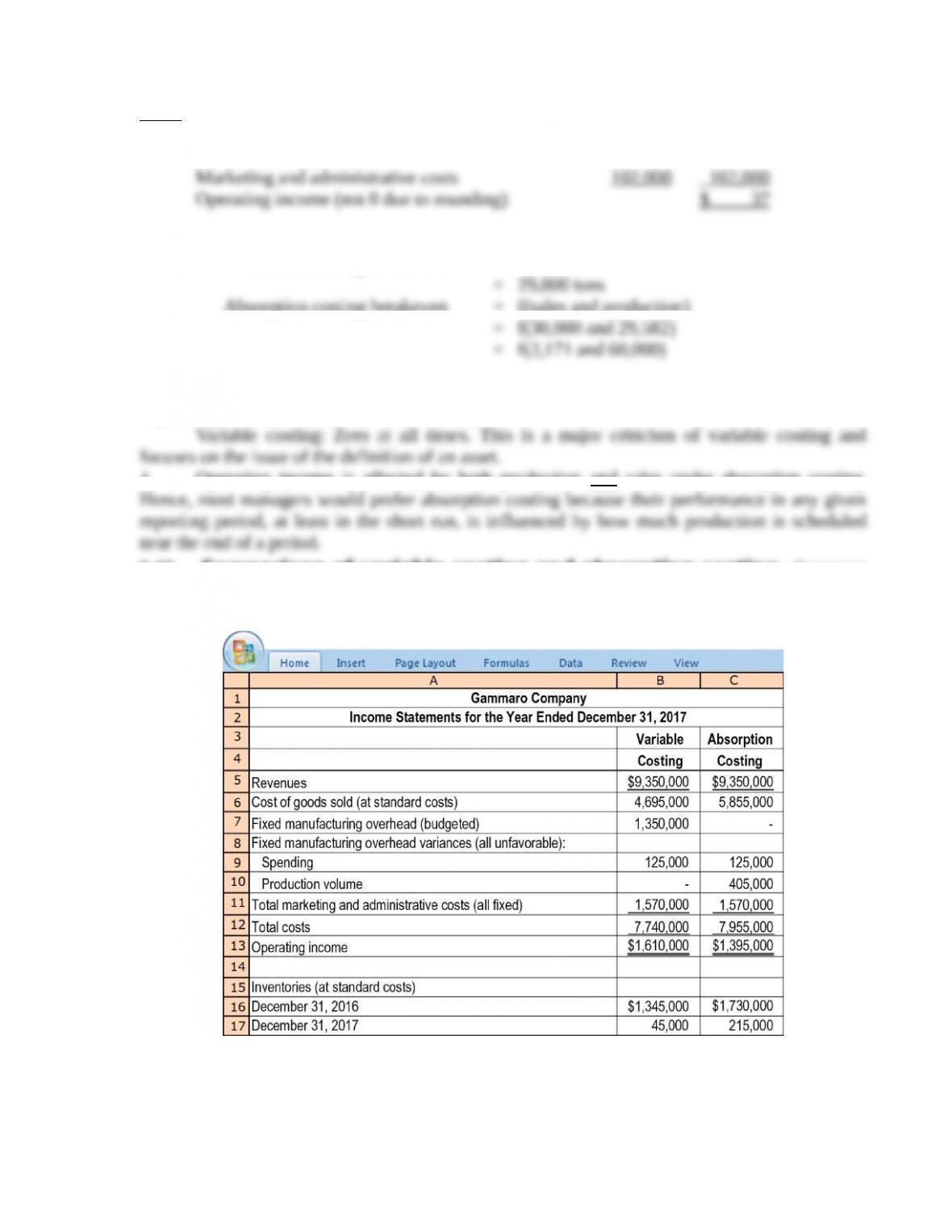

9-35 Comparison of variable costing and absorption costing. Gammaro

Company uses standard costing. Tim Sweeney, the new president of Gammaro Company, is

presented with the following data for 2017:

Required:

1. At what percentage of denominator level was the plant operating during 2017?

2. How much fixed manufacturing overhead was included in the 2016 and the 2017 ending

inventory under absorption costing?

3. Reconcile and explain the difference in 2017 operating incomes under variable and

absorption costing.

4. Tim Sweeney is concerned: He notes that despite an increase in sales over 2016, 2017

operating income has actually declined under absorption costing. Explain how this occurred.