SOLUTIO

(10 min.) Journal entries (continuation of 17-36).

1. Work in Process––Assembly Department 4,635,000

Accounts Payable 4,635,000

Work in Process––Assembly Department

17-38 FIFO method (continuation of 17-36).

Required:

1. Do Problem 17-36 using the FIFO method of process costing. Explain any difference

between the cost per equivalent unit in the assembly department under the weighted-average

method and the FIFO method.

2. Should Hoffman’s managers choose the weighted-average method or the FIFO method?

Explain briefly.

SOLUTION

(20 min.) FIFO method (continuation of 17-36).

1. The equivalent units of work done in the Assembly Department in October 2017 for

direct materials and conversion costs are shown in Solution Exhibit 17-38A.

SOLUTION EXHIBIT 17-38A

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

FIFO Method of Process Costing,

Assembly Department of Hoffman Company for October 2017.

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Completed and transferred out during current

period:

From beginning work in process§

4,000 (100% 100%); 4,000 (100%

45%) 4,000 0 2,200

§Degree of completion in this department: direct materials, 100%; conversion costs, 45%.

†26,000 physical units completed and transferred out minus 4,000 physical units completed and transferred out from

beginning work-in-process inventory.

*Degree of completion in this department: direct materials, 100%; conversion costs, 65%

The cost per equivalent unit of work done in the Assembly Department in October 2017 for

direct materials and conversion costs is calculated in Solution Exhibit 17-38B. This exhibit also

summarizes the total Assembly Department costs for October 2017, and assigns these costs to

units completed (and transferred out) and units in ending work in process under the FIFO

method.

Solution EXHIBIT 17-38B

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and

Assign Costs to the Units Completed and Units in Ending Work-in-Process Inventory;

FIFO Method of Process Costing, Assembly Department of Hoffman Company for

October 2017.

Total

Production

Costs

Direct

Materials

(Step 3) Work in process, beginning (given) $1,489,650 $1,248,000

Costs added in current period (given) 7 ,210,125 4 ,635 ,000

Total costs to account for $ 8 ,699,775 $5 ,750,000

*Equivalent units used to complete beginning work in process from Solution Exhibit 17-38A, Step 2.

†Equivalent units started and completed from Solution Exhibit 17-38A, Step 2.

#Equivalent units in ending work in process from Solution Exhibit 17-38A, Step 2.

2. The cost per equivalent unit of beginning inventory and of work done in the current

period differ:

Beginning

Inventory

Work Done in

Current Period

Direct materials

$312.00 ($1,248,000 4,000 equiv. units)

$206.00

Direct

Materials

Conversion

Costs

* from Solution Exhibit 17-36B

**from Solution Exhibit 17-38B

The cost per equivalent unit differs between the two methods because each method uses different

costs as the numerator of the calculation. FIFO uses only the costs added during the current

period whereas weighted-average uses the costs from the beginning work-in-process as well as

costs added during the current period. Both methods also use different equivalent units in the

denominator.

The following table summarizes the costs assigned to units completed and those still in

process under the weighted-average and FIFO process-costing methods for our example.

Weighted

Average

(Solution

Exhibit 17-36B)

FIFO

(Solution

Exhibit 17-38B) Difference

The FIFO ending inventory is lower than the weighted-average ending inventory by $8,650. This

is because FIFO assumes that all the higher-cost prior-period units in work in process are the first

to be completed and transferred out while ending work in process consists of only the lower-cost

Hoffman’s managers should consider the FIFO method because even though it shows

lower operating income and higher cost of goods sold, it lowers taxes. Managers may have an

17-39 Transferred-in costs, weighted-average method (related to 17-36 to 17-38). Hoffman

Company, as you know, is a manufacturer of car seats. Each car seat passes through the assembly

department and testing department. This problem focuses on the testing department. Direct

materials are added when the testing department process is 90% complete. Conversion costs are

added evenly during the testing department’s process. As work in assembly is completed, each

unit is immediately transferred to testing. As each unit is completed in testing, it is immediately

transferred to Finished Goods.

Hoffman Company uses the weighted-average method of process costing. Data for the testing

department for October 2017 are as follows:

Physical

Units (Car

Seats)

Transferred-

In Costs

Direct

Materials

Conversion

Costs

Work in process, October 1a5,500 $2,931,000 $ 0 $ 499,790

Transferred in during

October 2017

?

Completed during October

2017

29,800

Work in process, October

31b

1,700

Total costs added during

October 2017

$8,094,000 $10,877,000 $4,696,260

aDegree of completion: transferred-in costs,?%; direct materials,?%; conversion costs,

65%.

bDegree of completion: transferred-in costs,?%; direct materials,?%; conversion costs,

45%.

Required:

1. What is the percentage of completion for (a) transferred-in costs and direct materials in

beginning work-in-process inventory and (b) transferred-in costs and direct materials in

ending work-in-process inventory?

2. For each cost category, compute equivalent units in the testing department. Show physical

units in the first column of your schedule.

3. For each cost category, summarize total testing department costs for October 2017, calculate

the cost per equivalent unit, and assign costs to units completed (and transferred out) and to

units in ending work in process.

4. Prepare journal entries for October transfers from the assembly department to the testing

department and from the testing department to Finished Goods.

SOLUTION

(30 min.) Transferred-in costs, weighted-average method (related to 17-36 to 17-38).

1. Transferred-in costs are 100% complete, and direct materials are 0% complete in both

beginning and ending work-in-process inventory. The reason is that transferred-in costs are

always 100% complete as soon as they are transferred in from the Assembly Department to the

2. Solution Exhibit 17-39A computes the equivalent units of work done to date in the

Testing Department for transferred-in costs, direct materials, and conversion costs.

3. Solution Exhibit 17-39B summarizes total Testing Department costs for October 2017,

4. Journal entries:

a. Work in Process––Testing Department 8,094,000

Work in Process––Assembly Department 8,094,000

Cost of goods completed and transferred out

during October from the Assembly

Department to the Testing Department

SOLUTION EXHIBIT 17-39A

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

Weighted-Average Method of Process Costing,

Testing Department of Hoffman Company for October 2017.

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-i

n

Costs

Direct

Materials

Conversio

n

Costs

Work in process, beginning (given) 5,500

Transferred in during current period (given) 26 ,000

30,565

SOLUTION EXHIBIT 17-39B

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign Costs

to the Units Completed and Units in Ending Work-in-Process Inventory;

Weighted-Average Method of Process Costing,

Testing Department of Hoffman Company for October 2017.

Total

Production

Costs

Transferred

-in Costs

Direct

Materials

(Step 3)Work in process, beginning (given) $ 3,430,790 $ 2,931,000 $ 0

Costs added in current period (given) 23,667,260 8 ,094,000 10

Total costs to account for $ 27,098,050 $ 11 ,025,000 $ 10

*Equivalent units completed and transferred out from Solution Exhibit 17-39A, Step 2.

†Equivalent units in ending work in process from Solution Exhibit 17-39A, Step 2.

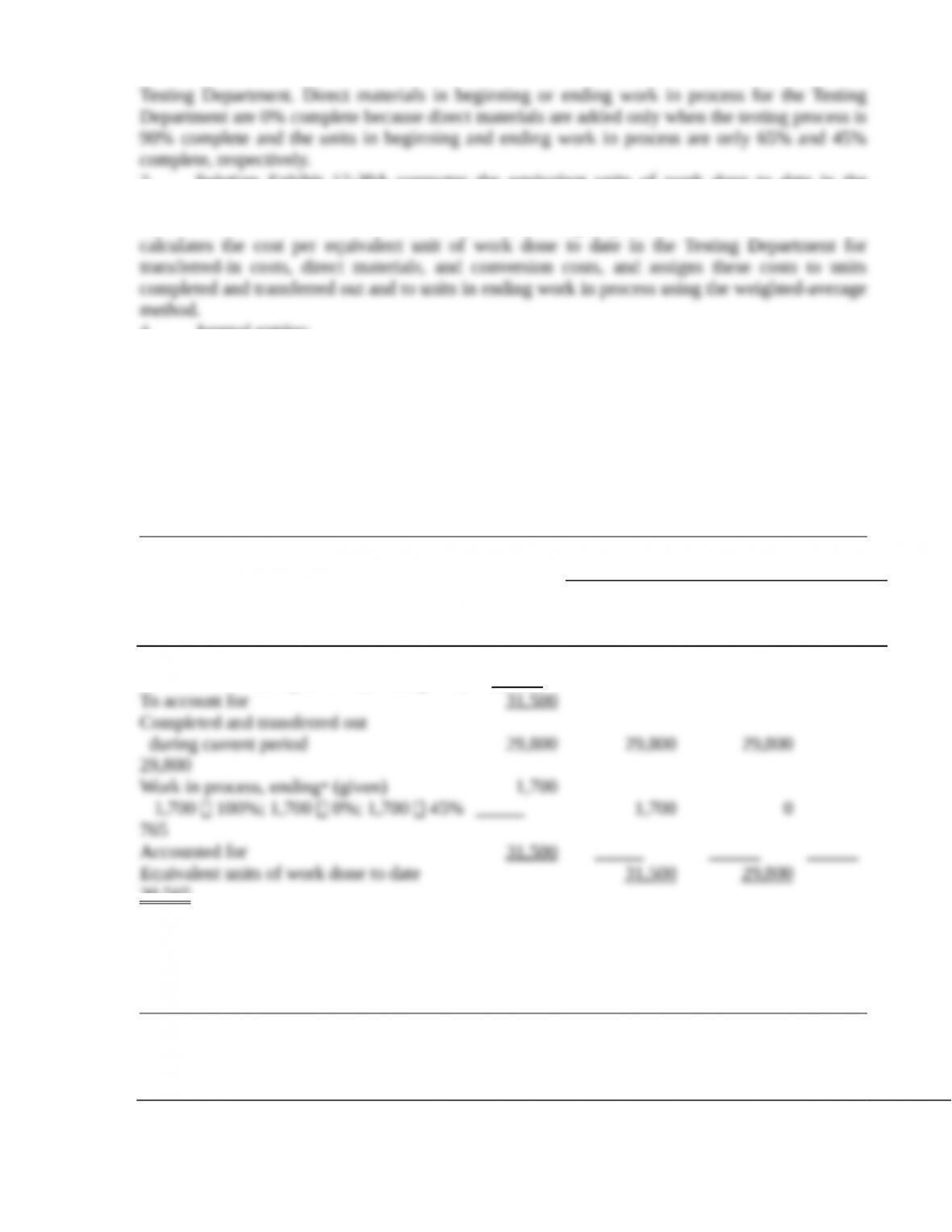

17-40 Transferred-in costs, FIFO method (continuation of 17-39). Refer to the information

in Problem 17-39. Suppose that Hoffman Company uses the FIFO method instead of the

weighted-average method in all of its departments. The only changes to Problem 17-39 under the

FIFO method are that total transferred-in costs of beginning work in process on October 1 are

$2,879,000 (instead of $2,931,000) and that total transferred-in costs added during October are

$9,048,000 (instead of $8,094,000).

Required:

Using the FIFO process-costing method, complete Problem 17-39.

SOLUTION

(30 min.) Transferred-in costs, FIFO method (continuation of 17-39).

1. As explained in Problem 17-39, requirement 1, transferred-in costs are 100% complete

and direct materials are 0% complete in both beginning and ending work-in-process inventory.

2. The equivalent units of work done in October 2017 in the Testing Department for

3. Solution Exhibit 17-40B summarizes total Testing Department costs for October 2017,

4. Journal entries:

Cost of goods completed and transferred out

during October from the Testing Department

to Finished Goods inventory.

SOLUTION EXHIBIT 17-40A

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

FIFO Method of Process Costing,

Testing Department of Hoffman Company for October 2017.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Transferred-in during current period (given)

To account for

5,500

26 ,000

31 ,500

(work done before current period)

Completed and transferred out during current

period:

§ Degree of completion in this department: Transferred-in costs, 100%; direct materials, 0%; conversion costs, 65%.

†29,800 physical units completed and transferred out minus 5,500 physical units completed and transferred out from

beginning work-in-process inventory.

*Degree of completion in this department: transferred-in costs, 100%; direct materials, 0%; conversion costs, 45%.

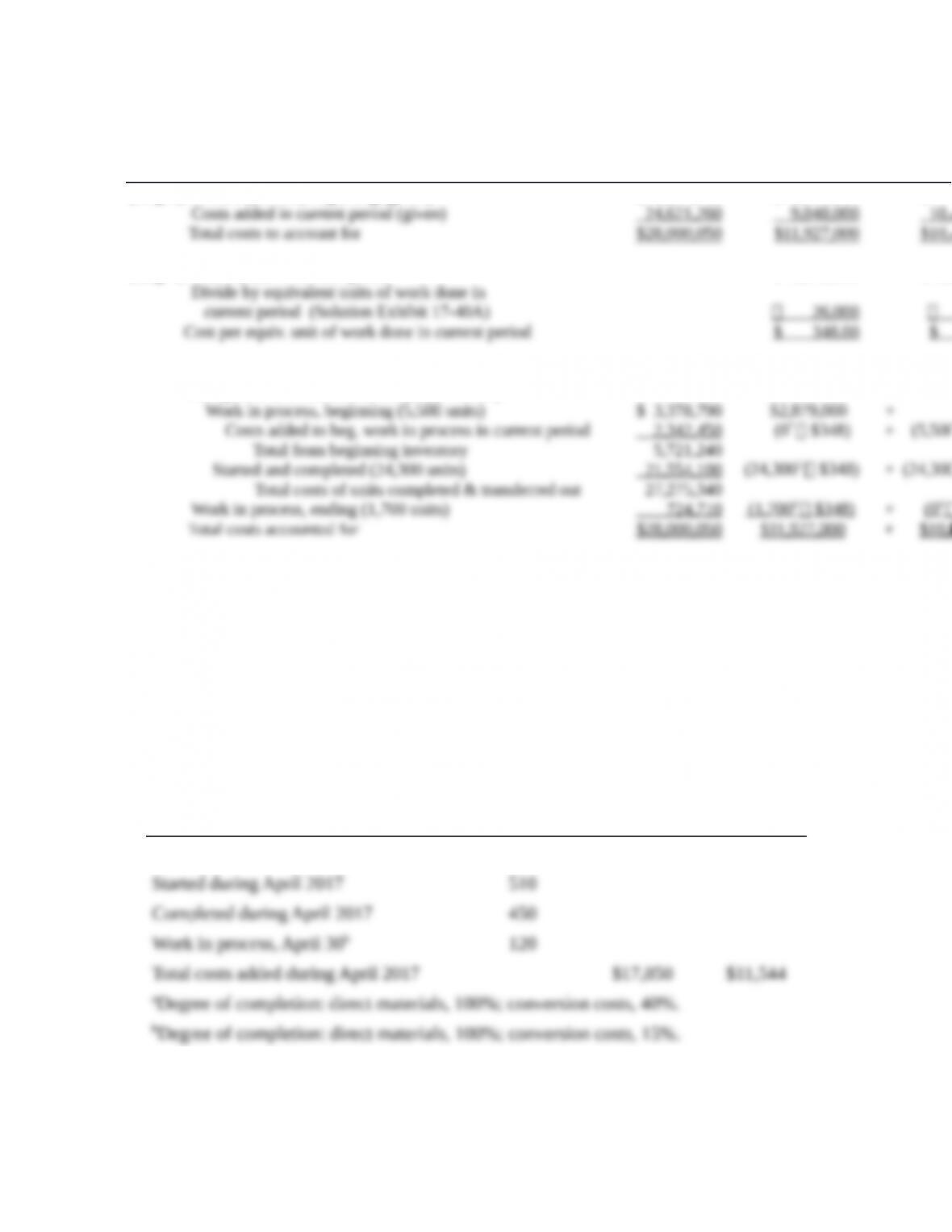

SOLUTION EXHIBIT 17-40B

Total

Production

Costs

Transferred-in

Costs

Direct

Materials

(Step 3) Work in process, beginning (given) $ 3,378,790 $ 2,879,000 $ 0

(Step 4) Costs added in current period $ 9,048,000 $10,877,000

(Step 5) Assignment of costs:

Completed and transferred out (29,800 units):

*Equivalent units used to complete beginning work in process from Solution Exhibit 17-40A, Step 2.

†Equivalent units started and completed from Solution Exhibit 17-40A, Step 2.

#Equivalent units in ending work in process from Solution Exhibit 17-40A, Step 2. 17-41 Weighted-average

method. McKnight Handcraft is a manufacturer of picture frames for large retailers. Every picture frame passes

through two departments: the assembly department and the finishing department. This problem focuses on the

assembly department. The process-costing system at McKnight has a single direct-cost category (direct materials)

and a single indirect-cost category (conversion costs). Direct materials are added when the assembly department

process is 10% complete. Conversion costs are added evenly during the assembly department’s process.

McKnight uses the weighted-average method of process costing. Consider the following data

for the assembly department in April 2017:

Physical Unit

(Frames)

Direct

Materials

Conversio

n Costs

Work in process, April 1a60 $ 1,530 $ 156

Required:

1. Summarize the total assembly department costs for April 2017, and assign them to units

completed (and transferred out) and to units in ending work in process.

2. What issues should a manager focus on when reviewing the equivalent units calculation?