Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

An unfavorable production-volume variance always infers that management made a bad

planning decision regarding the plant capacity.

The nominal rate of return is made up of a risk-free element when there is no expected

inflation, a business-risk element, and an inflation element.

Inflation can distort data that are compared over time so purely inflationary effects

should be removed.

Management control systems is designed only for top level managers and is not

applicable to line managers.

Companies implementing kaizen budgeting believe that employees who actually do the

job have the best knowledge of how the job can be done better.

In a backflush-costing system, no record of work in process appears in the accounting

records.

Manufacturing cycle times affect both revenues and costs.

The flexible-budget variance is the total of price variance and efficiency variance.

A time driver is any factor that causes a change in the speed of an activity when the

factor changes.

When goods are finished, the Finished Goods Control account is debited while the

Work-in-Process Control account is credited.

A variance within an acceptable range is considered to be an "in-control occurrence"

and calls for no investigation or action by managers.

Appraisal costs are costs incurred to preclude the production of products that do not

conform to specifications.

In cost-plus pricing, the markup definitively determines the actual selling price.

As product diversity and indirect costs increase, it is usually best to switch away from a

broad averaging system to an activity-based cost system.

The t-value of a coefficient measures how large the value of the estimated coefficient is

relative to its standard error.

An advantage of the single-rate method is that it is the most accurate method of

cost-allocation.

The selling prices method under stand-alone revenue-allocation method is best because

the weights explicitly consider the prices customers are willing to pay for the individual

products

The costs of storage space owned are always relevant costs of carrying inventory.

A cost object is anything for which a measurement of costs is desired.

Under the weighted-average method, the costs of normal spoilage are added to the costs

of their related good units. Hence, the cost per good unit completed and transferred out

equals the total costs transferred out divided by the number of good units produced.

Standard costing is a cost system that allocates overhead costs on the basis of overhead

cost rates based on actual overhead costs times the standard quantities of the allocation

bases allowed for the actual outputs produced.

Using the fairness criterion, the costs are allocated among the beneficiaries in

proportion to the benefits each receives.

Surveys indicate that decisions made most frequently at the corporate level are related

to sources of supplies and products to manufacture.

Downsizing is an integrated approach of configuring processes, products, and people to

match costs to the activities that need to be performed to operate effectively and

efficiently in the present and future.

The high-low method relies on only two observations, the highest and lowest, to

estimate a linear cost function.

Multiple regression analysis estimates the relationship between the dependent variable

and two or more independent variables.

Today, companies are simplifying their cost systems and moving toward less-detailed

and less-complex cost allocation bases.

Cross-sectional data pertain to the same entity (organization, plant, activity, and so on)

over successive past periods.

Implementing activity-based costing system involves use of different cost rates for

different activities to compute indirect costs of a product.

The weighted-average process costing method does not distinguish between units

started in the previous period but completed during the current period and units started

and completed during the current period.

Sensitivity analysis is a useful tool that helps managers evaluate risks.

In activity based costing systems, limiting cost-allocation bases to only units of output

strengthens the cause-and-effect relationship between the cost-allocation base and the

costs in a cost pool.

The Swivel Chair Company manufacturers a standard recliner. During February, the

firm's Assembly Department started production of 155,000 chairs. During the month,

the firm completed 185,000 chairs and transferred them to the Finishing Department.

The firm ended the month with 18,000 chairs in ending inventory. All direct materials

costs are added at the beginning of the production cycle. Weighted-average costing is

used by Swivel. What were the equivalent units for conversion costs for February if the

beginning inventory was 70% complete as to conversion costs and the ending inventory

was 45% complete as to conversion costs?

A) 193,100

B) 163,100

C) 185,000

D) 171,200

The Green Company processes unprocessed goat milk up to the split-off point where

two products, condensed goat milk and skim goat milk result. The following

information was collected for the month of October:

The costs of purchasing the of unprocessed goat milk and processing it up to the split-off

point to yield a total of 105,000 gallons of saleable product was $191,480. There were no

inventory balances of either product. Condensed goat milk may be processed further to

yield 45,000 gallons (the remainder is shrinkage) of a medicinal milk product, Xyla, for an

additional processing cost of $5 per usable gallon. Xyla can be sold for $20 per gallon.

Skim goat milk can be processed further to yield 58,200 gallons of skim goat ice cream,

for an additional processing cost per usable gallon of $5. The product can be sold for $12

per gallon.

There are no beginning and ending inventory balances.

Using the sales value at split-off method, what is the gross-margin percentage for skim

goat milk at the split-off point? (Round intermediary percentages to the nearest hundredth.)

A) 46.25%

B) 50.00%

C) 56.75%

D) 53.75%

If a company has excess capacity, the most it would pay for buying a product that it

currently makes would be the ________.

A) total variable cost of producing the product

B) full cost of producing the product

C) total cost of producing the product

D) business function cost of the product

Sunk costs ________.

A) are relevant

B) are differential

C) have future implications

D) are ignored when evaluating alternatives

Efficiency is ________.

A) the degree to which a predetermined objective or target is met

B) the difference between an actual input quantity and a budgeted input quantity

C) the continuous process of comparing a firm's performance levels against the best

levels of performance in competing companies

D) the relative amount of inputs used to achieve a given output level

An unfavorable sales-volume variance could result from ________.

A) an inappropriate assignment of labor or machines to specific jobs

B) competitors taking market share

C) an inefficiency of a purchasing manager in bargaining with suppliers

D) a decrease in actual selling price compared to anticipated selling price

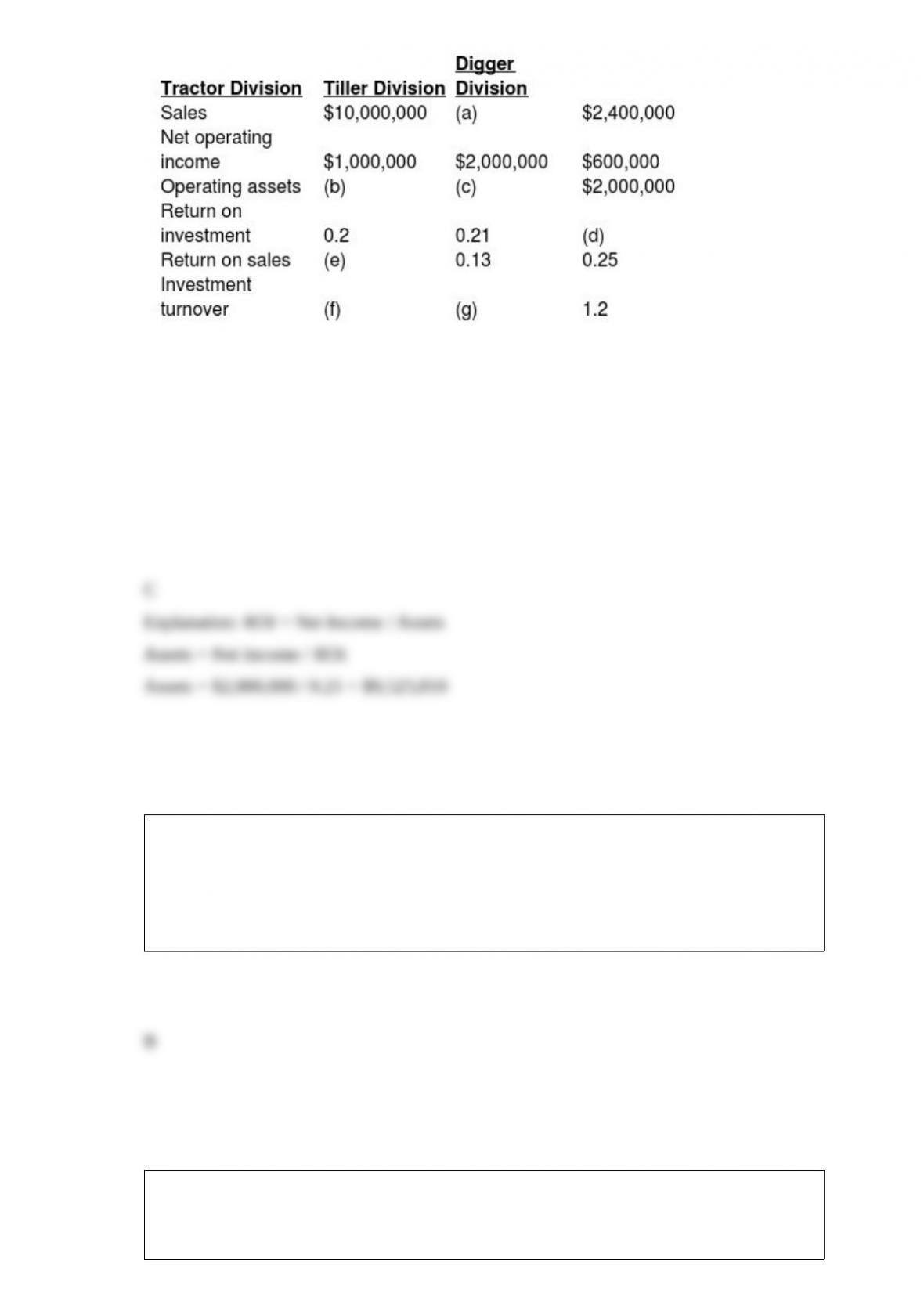

The top management at Groundsource Company, a manufacturer of lawn and garden

equipment, is attempting to recover from a fire that destroyed some of their accounting

records. The main computer system was also severely damaged. The following

information was salvaged:

What is the value of the operating assets belonging to the Tiller Division?

A) $10,000,000

B) $15,384,615

C) $9,523,810

D) $260,000

Work-in-process inventory would normally include ________.

A) direct materials in stock and awaiting use in the manufacturing process

B) goods partially worked on but not yet fully completed

C) goods fully completed but not yet sold

D) goods returned after being sold to be re-worked on further improvements and quality

Foodiez Inn is a fast-food restaurant that sells burgers and hot dogs in a 1980s

environment. The fixed operating costs of the company are $10,000 per month. The

controlling shareholder, interested in product profitability and pricing, wants all costs

allocated to either the burgers or the hot dogs. The following information is provided

for the operations of the company:

Required:

a. What amount of fixed operating costs is assigned to the burgers and hot dogs when

actual sales are used as the allocation base for January? For February?

b. Hot dog sales for January and February remained constant. Did the amount of fixed

operating costs allocated to hot dogs also remain constant for January and February?

Explain why or why not. Comment on any other observations.

The cost to be predicted and managed is referred to as the ________.

A) independent variable

B) dependent variable

C) cost driver

D) regression

Which of the following statements is true of the internal-business-process perspective

of a balanced scorecard?

A) Internal-business-process perspective is composed of three subprocesses: innovation

process; learning-and-growth process; and post sales-service process.

B) Internal-business-process perspective evaluates the profitability of the strategy and

the creation of shareholder value.

C) Internal-business-process improvement targets are often determined after

benchmarking against an organization's main competitors standards.

D) Internal-business-process perspective is composed of three subprocesses: operations

process; learning-and-growth process; and post sales-service process.

When benchmarking, management accountants are most valuable when they ________.

A) present differences in the benchmarking data to management

B) highlight differences in the benchmarking data to management

C) provide insight into why costs or revenues differ across companies

D) provide complex mathematical analysis

When the purpose of cost allocation is to provide information for economic decisions or

to motivate managers and employees, which of the following would be the best criteria?

A) the cause-and-effect and the ability-to bear criteria

B) the cause-and-effect and the benefits-received criteria

C) the benefits-received and the fairness criteria

D) the fairness and the ability-to-bear criteria

When variable overhead spending variance is unfavorable, it can be safely assumed that

________.

A) actual rate per unit of cost-allocation base is higher than budgeted rate

B) actual quantity of cost-allocation base used is higher than budgeted quantity

C) actual rate per unit of cost-allocation base is lower than budgeted rate

D) actual quantity of cost-allocation base used is lower than budgeted quantity

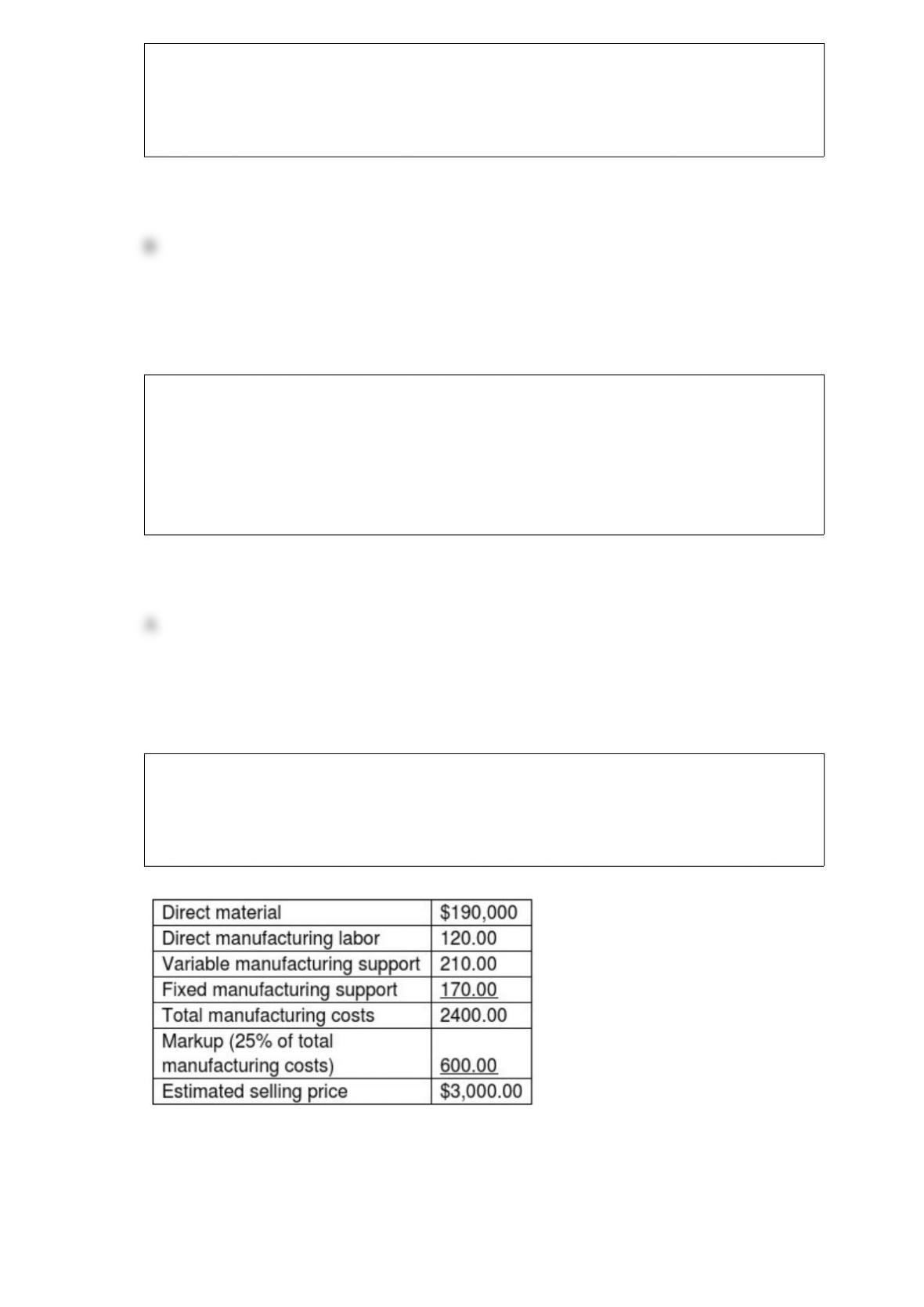

Golden Generator Supply is approached by Mr. Stephen, a new customer, to fulfill a

large one-time-only special order for a product similar to one offered to regular

customers. Golden Generator Supply has excess capacity. The following per unit data

apply for sales to regular customers:

If Golden Generator Supply accepts the order at $2640, what is the amount contributed

towards fixed costs and profit on a sales order of 1600 units?

A) $384,000

B) $656,000

C) $1,232,000

D) $992,000

Which of the following statements is true?

A) There is a cause-and-effect relationship between the cost driver and the amount of

cost.

B) Fixed costs have cost drivers over the short run.

C) Over the short run all costs have cost drivers.

D) Volume of production is a cost driver of distribution costs.

Nonfinancial performance measures ________.

A) are usually used in combination with financial measures for control purposes

B) are rarely used to evaluate overall efficiency

C) allow managers to make informed tradeoffs

D) are often the sole basis of a manager's performance evaluations

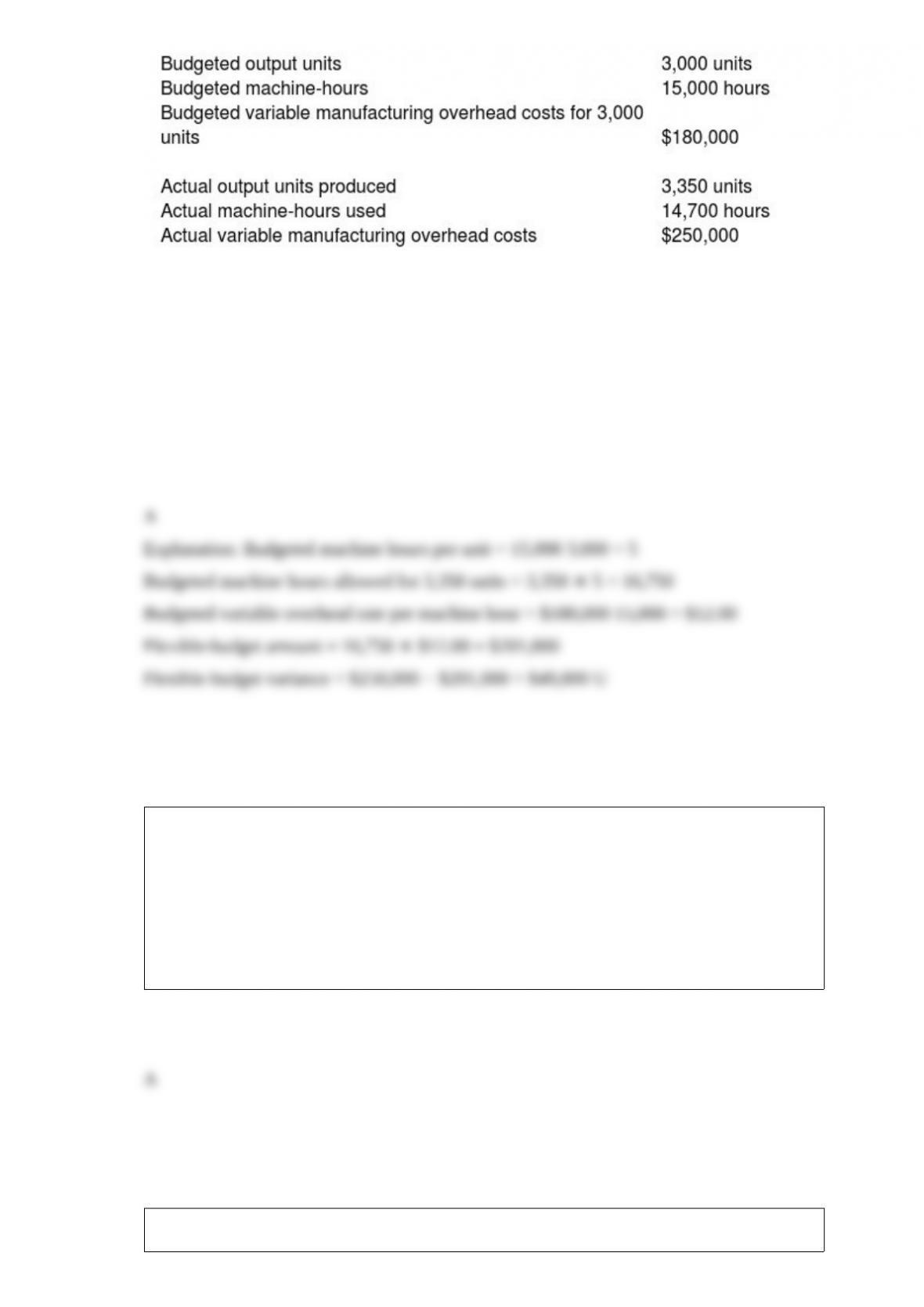

Lancelot Corporation manufactures tennis gear and uses budgeted machine-hours to

allocate variable manufacturing overhead. The following information relates to the

company's manufacturing overhead data:

What is the flexible-budget variance for variable manufacturing overhead?

A) $49,000 unfavorable

B) $49,000 favorable

C) $70,000 unfavorable

D) $70,000 favorable

Bennet Company employs 20 individuals. Eighteen employees are paid $18 per hour

and the rest are salaried employees paid $3,000 a month. Which of the following is the

total cost function of personnel?

A) y = a + bX

B) y = b

C) y = bX

D) y = a

Which of the following issues is addressed by the Sarbanes-Oxley legislation?

A) safety aspects of products

B) environmental damages caused by industries

C) disclosure practices of public corporations

D) disclosure practices of private companies

Which of the following is the best description of price discrimination?

A) setting different prices for different products

B) charging different prices for quantity amounts

C) using variable costing for some products and full costing for other products when

setting prices

D) charging different prices to different customers or clients for the same products or

services

Direct materials inventory costs would normally include ________.

A) the cost of materials in stock are part of the cost object (product) and can be traced

to that cost object in an economically feasible way

B) the cost of goods partially worked on but not yet fully completed

C) the cost of goods fully completed but not yet sold

D) the cost of products in their original form intended to be sold without changing their

basic form

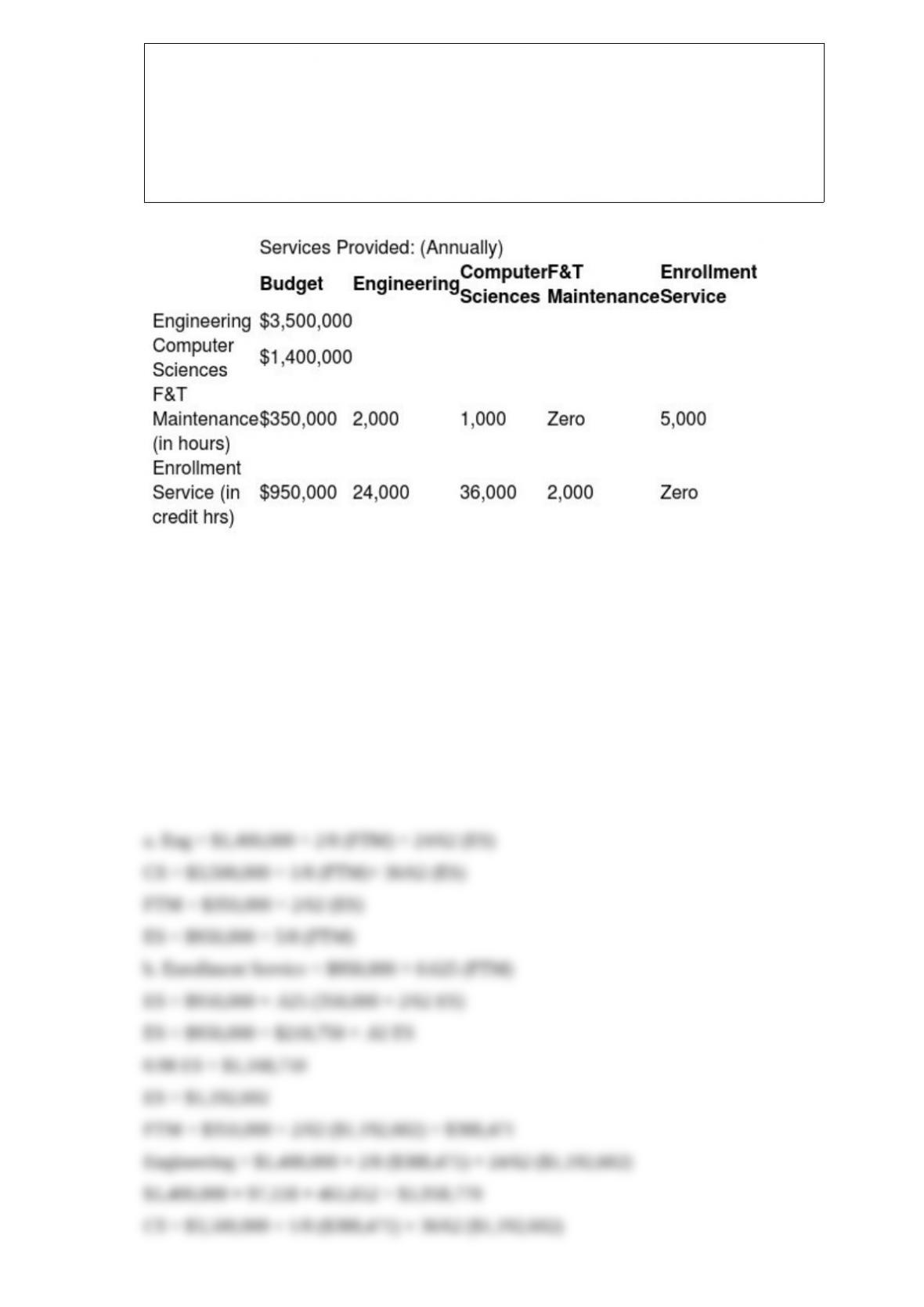

Gotham University offers only high-tech graduate-level programs. Gotham has two

principal operating departments, Engineering and Computer Sciences, and two support

departments, Facility and Technology Maintenance and Enrollment Services. The base

used to allocate facility and technology maintenance is budgeted total maintenance

hours. The base used to allocate enrollment services is number of credit hours for a

department. The Facility and Technology Maintenance budget is $350,000, while the

Enrollment Services budget is $950,000. The following chart summarizes budgeted

amounts and allocation-base amounts used by each department:

Required:

a. Set up algebraic equations in linear equation form for each activity.

b. Determine total costs for each department by solving the equations from part (a) using

the reciprocal method.

(Engineering= Eng; Computer Sciences = CS; Facility and Technical Maintenance = FTM;

Enrollment Service = ES)

Which one of the following budgets would be prepared using activity based budgeting

techniques?

A) direct materials purchase budget

B) revenues budget

C) manufacturing overhead cost budget

D) production budget

Fixed costs remain constant at $450,000 per month. During high-output months

variable costs are $300,000, and during low-output months variable costs are $125,000.

What are the respective high and low indirect-cost rates if budgeted professional

labor-hours are 24,000 for high-output months and 5,000 for low-output months?

A) $31.25 per hour; $115.00 per hour

B) $31.25 per hour; $31.25 per hour

C) $18.75 per hour; $25.00 per hour

D) $12.50 per hour; $115.00 per hour

Which of the following statements best defines backflush costing system?

A) an integrated costing system covering a company's accounting, distribution,

manufacturing, purchasing, human resources, and other functions

B) a costing system that omits recording some of the journal entries relating to the

stages from the purchase of direct materials to the sale of finished goods

C) a push-through system in which each component in a production line is produced

immediately as needed by the next step in the production line

D) a costing system that comprises a single database that collects data and feeds it into

software applications supporting all of a company's business activities

In the merchandising sector ________.

A) only variable costs are subtracted to determine gross margin

B) fixed overhead costs are subtracted to determine gross margin

C) fixed overhead costs are subtracted to determine contribution margin

D) all operating costs are subtracted to determine contribution margin

The actual information pertains to the month of June. As a part of the budgeting

process, Great Cabinets Company developed the following static budget for June. Great

Cabinets is in the process of preparing the flexible budget and understanding the results.

The flexible-budget variance for variable costs is ________.

A) $2,210 unfavorable

B) $202,275 unfavorable

C) $89,270 favorable

D) $137,930 favorable

Activity-based costing information can be used for ________.

A) product-mix decisions

B) pricing decisions

C) advertisement decisions

D) inventory valuation

The costs of normal spoilage are allocated to the units in ending work-in-process

inventory, in addition to completed units if the units ________.

A) in ending inventory have not passed the inspection point

B) in ending work-in-process inventory have passed the inspection point

C) in ending work in process inventory are more than 25% complete

D) in ending work-in-process inventory are less than 25% complete

The contribution income statement highlights ________.

A) gross margin

B) the segregation of costs into period costs and inventoriable costs

C) different product lines

D) variable and fixed costs

Block Island TV currently sells large televisions for $380. It has costs of $290. A

competitor is bringing a new large television to market that will sell for $310.

Management believes it must lower the price to $310 to compete in the market for large

televisions. Marketing believes that the new price will cause sales to increase by 10%,

even with a new competitor in the market. Block Island TV sales are currently 110,000

televisions per year.

What is the target cost per unit if target operating income is 35% of sales?

A) $108.50

B) $133.00

C) $201.50

D) $247.00

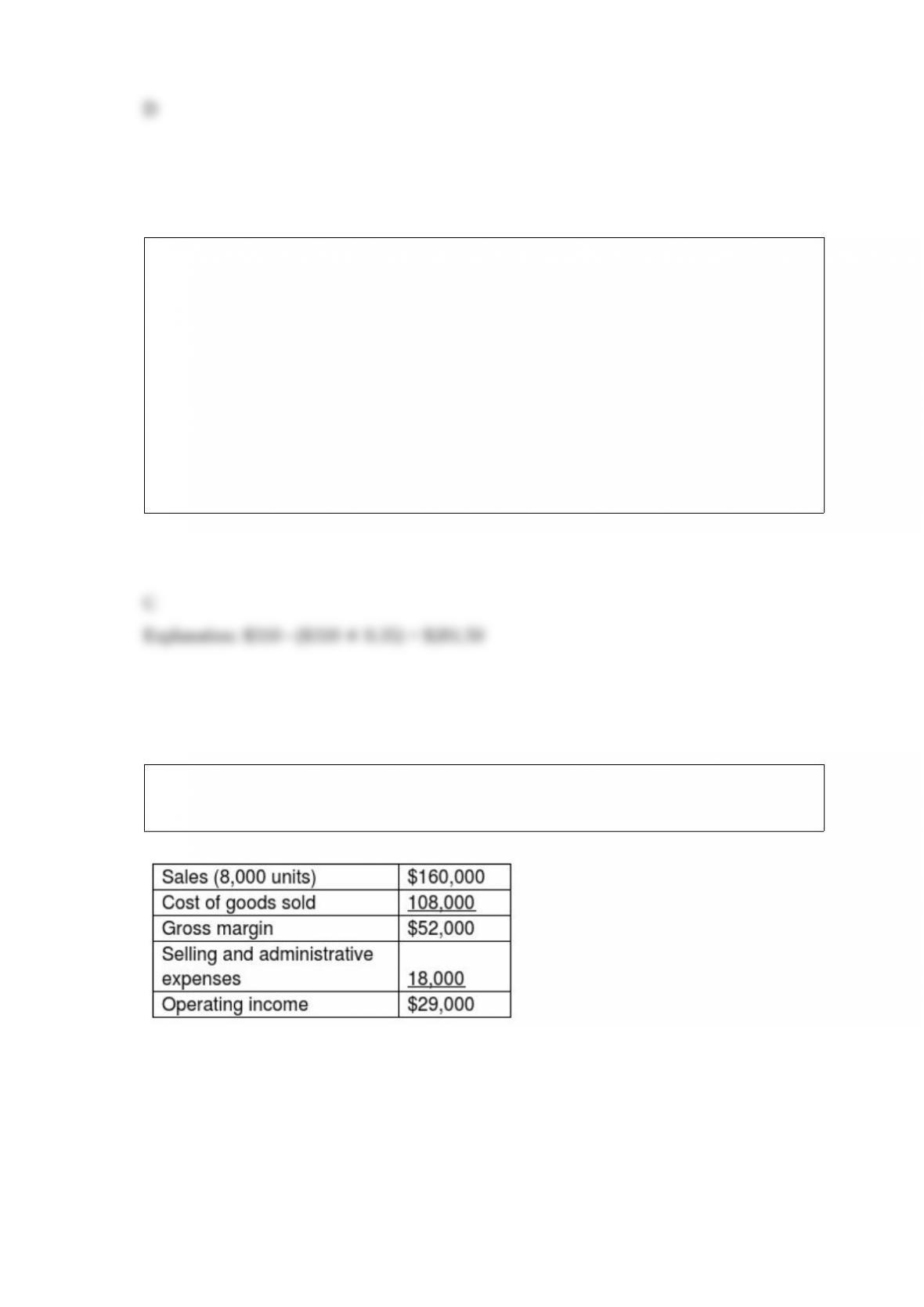

Aspen Popular Company prepared the following absorption-costing income statement

for the year ended May 31, 2017.

Additional information follows:

Selling and administrative expenses include $1.50 of variable cost per unit sold. There was

no beginning inventory, and 8,750 units were produced. Variable manufacturing costs were

$11 per unit. Actual fixed costs were equal to budgeted fixed costs

Required:

Prepare a variable-costing income statement for the same period.

Briefly explain each of the three methods used to determine a transfer price.

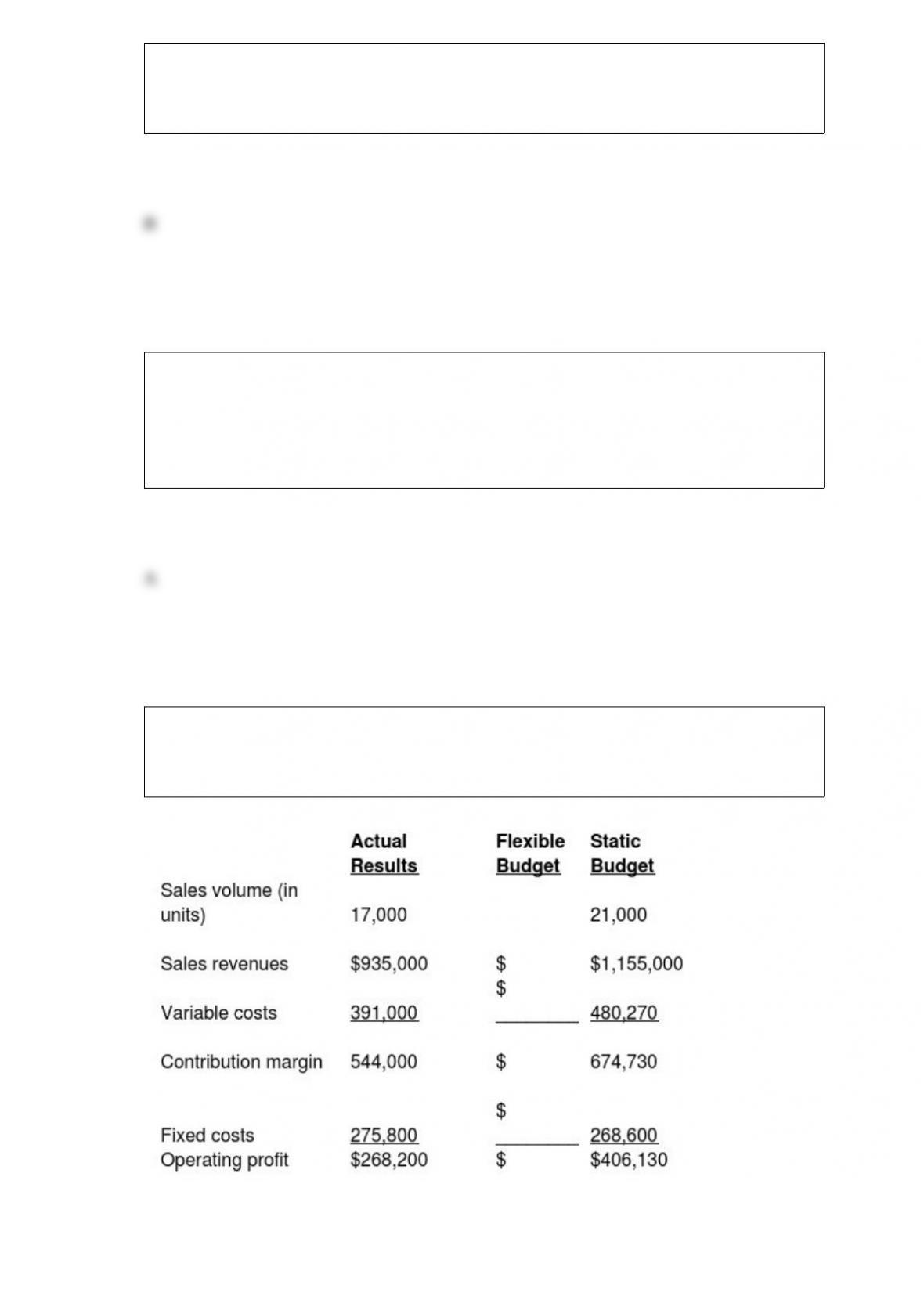

Bennett Street Table Company manufactures tables for schools. The 2018 operating

budget is based on sales of 45,000 units at $55 per table. Operating income is

anticipated to be $240,000. Budgeted variable costs are $35 per unit, while fixed costs

total $660,000.

Actual income for 2018 was a surprising $569,000 on actual sales of 46,000 units at

$60 each. Actual variable costs were $34 per unit and fixed costs totaled $627,000.

Required:

Prepare a variance analysis report with both flexible-budget and sales-volume

variances.

Cape Cod Technolgy Inc. manufactures heavy duty flash lights. January and February

operations were identical in every way except for the planned production.

January had a production denominator of 80,000 units.

February had a production denominator of 60,000 units.

Fixed manufacturing costs totaled $200,000.

Sales for both months totaled 62,000 units with variable manufacturing costs of $4 per

unit. Selling and administrative costs were $0.60 per unit variable and $51,000 of fixed.

The selling price was $10 per unit.

Required:

Compute the operating income for both months using absorption costing.

Backflush costing does not strictly adhere to generally accepted accounting principles.

Explain why. Also, describe the types of businesses that might use backflush costing.

A quality improvement program is very costly to implement across a large corporation.

Why do they do it? Explain.

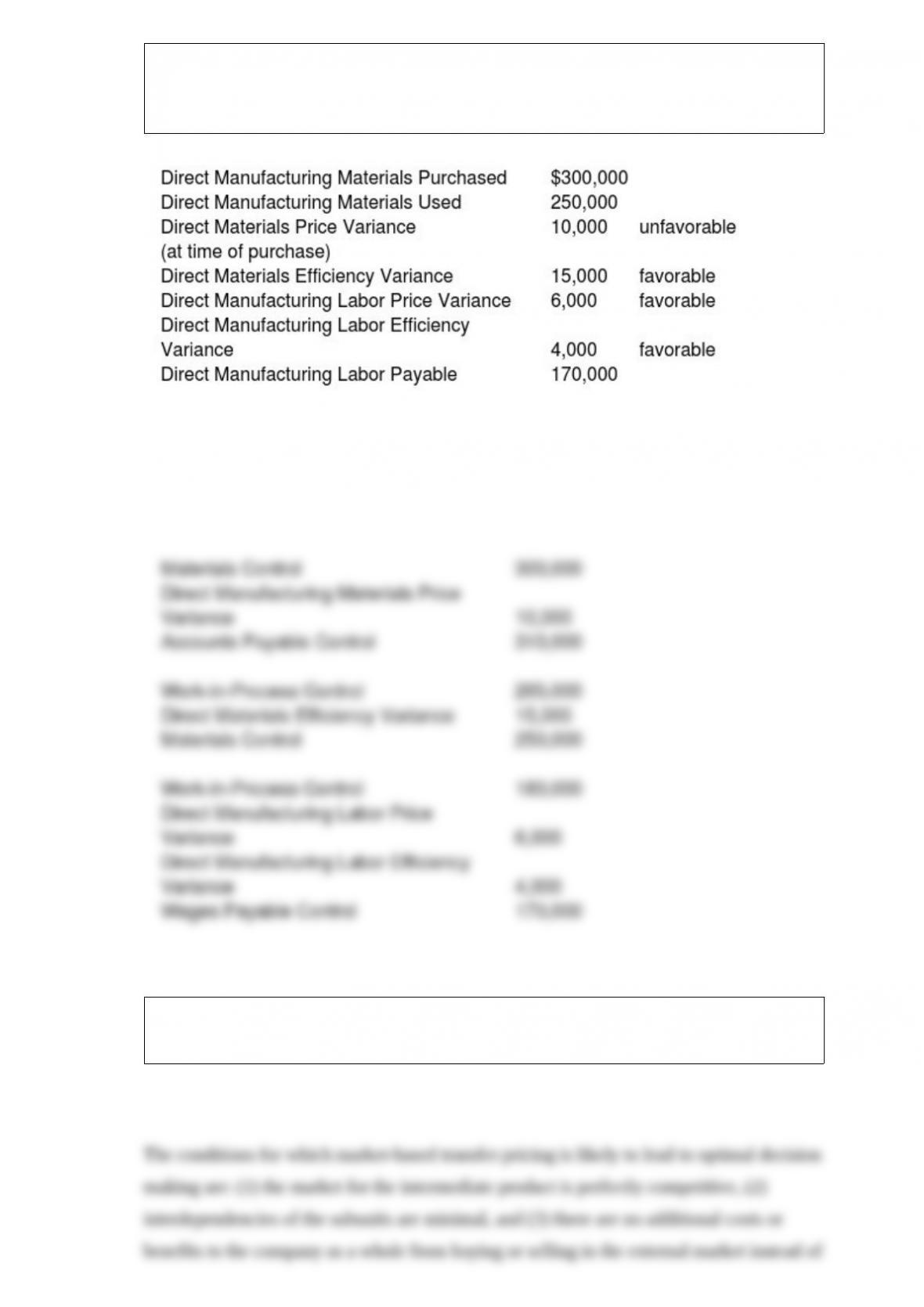

Waddell Productions makes separate journal entries for all cost accounting-related

activities. It uses a standard cost system for all manufacturing items. For the month of

June, the following activities have taken place:

Required:

Record the necessary journal entries to close the accounts for the month.

Briefly describe the conditions that should be met for market-based transfer pricing to

lead to optimal decision making among subunits of a large organization.

Why do we need to accumulate and calculate unit costs in process costing (and also job

costing)?

What are the two assumptions behind a simple linear cost function? Briefly explain the

three ways that a linear cost function may behave?

Distinguish between the two principal methods of accounting for byproducts, the

production byproduct method and the sale byproduct method. Briefly discuss the

relative merits (or lack thereof) of each.

Explain the difference between the cumulative average-time learning model and the

incremental unit-time learning model.

Describe some of the drawbacks of using the operating budget as a control device.

Briefly describe the four criteria used to guide cost-allocation decisions.

Explain why managers of small businesses prefer 3-variance analysis over 4-variance

analysis.

Why do firms often conduct multiple inspections?

What are the objectives in accounting for spoilage?