SOLUTION

(25 min.) Considerations other than cost in pricing decisions.

1.

Guest nights on weeknights:

18 weeknights × 100 rooms × 70% = 1,260

Guest nights on weekend nights:

Total costs for June:

2.

New weeknight guest nights

Total costs for June:

13-1

Yes, this pricing arrangement would increase operating income by $5,220 from an operating

loss of $4,620 to an operating income of $11,400 ($11,400 + $4,620 = $16,020).

3. Guests typically do not come to the amusement park on weekdays because adults are

busy at work and children have to attend school. The weeknight guests are families who stay at

In contrast, weekends are really the only time when families can conveniently come to

the amusement park given their busy weekday schedules. The demand of pleasure travelers on

2. Happy Times Hotel would need to charge a minimum of $39 per night for the last-minute

13-26 Cost-plus, target pricing, working backward. The new CEO of Rusty Manufacturing

has asked for information about the operations of the firm from last year. The CEO is given the

following information, but with some data missing:

Total sales revenue ?

Number of units produced and sold 500,000 units

Selling price ?

Operating income $180,000

Total investment in assets $2,250,000

Variable cost per unit $4.00

Fixed costs for the year $2,500,000

Required:

1. Find (a) total sales revenue, (b) selling price, (c) rate of return on investment, and (d) markup

percentage on full cost for this product.

2. The new CEO has a plan to reduce fixed costs by $225,000 and variable costs by $0.30 per

unit while continuing to produce and sell 500,000 units. Using the same markup percentage

as in requirement 1, calculate the new selling price.

3. Assume the CEO institutes the changes in requirement 2 including the new selling price.

However, the reduction in variable cost has resulted in lower product quality resulting in 5%

13-2

fewer units being sold compared with before the change. Calculate operating income (loss).

4. What concerns, if any, other than the quality problem described in requirement 3, do you see

in implementing the CEO’s plan? Explain briefly.

SOLUTION

(25 min.) Cost-plus, target pricing, working backward.

1. In the following table, work backward from operating income to calculate the selling price.

Selling price $ 9.36 (plug)

Less: Variable cost per unit 4.00

´

b) Selling price = $9.36 (from above)

Alternatively,

Operating income $ 180,000

Sales revenue $4,680,000

Selling price = $9.36

Units sold 500,000

= =

c) Rate of return on investment =

Operating income $180,000 8%

Total investment in assets $2,250,000

= =

d) Markup % on full cost

´

Unit cost =

$4,500,000 $9.00

500,000 units =

Markup % =

$9.36 $9.00 4%

$9.00

–=

13-3

Or

$4,680,000 $4,500,000 4%

$4,500,000

–=

2. New fixed costs =$2,500,000 – $225,000 = $2,275,000

´

Budgeted Operating Income

for the Year Ending December 31, 20xx

Revenues ($8.58

´

475,000 units)

$4,075,500

Variable costs ($3.70

´

475,000 units)

4. The CEO has not considered customers in these pricing decisions. Will customers

13-27 Value engineering, target pricing, and target costs. Westerly Cosmetics manufactures

and sells a variety of makeup and beauty products. The company has developed its own patented

formula for a new anti-aging cream The company president wants to make sure the product is

priced competitively because its purchase will also likely increase sales of other products. The

company anticipates that it will sell 400,000 units of the product in the first year with the

following estimated costs:

Product design and licensing $1,700,000

Direct materials 4,000,000

Direct manufacturing labor 1,600,000

Variable manufacturing overhead 400,000

13-4

Fixed manufacturing overhead 2,500,000

Fixed marketing 3,000,000

Required:

1. The company believes that it can successfully sell the product for $45 a bottle. The

company’s target operating income is 30% of revenue. Calculate the target full cost of

producing the 400,000 units. Does the cost estimate meet the company’s requirements? Is

value engineering needed?

2. A component of the direct materials cost requires the nectar of a specific plant in South

America. If the company could eliminate this special ingredient, the materials cost would

decrease by 25%. However, this would require design changes of $300,000 to engineer a

chemical equivalent of the ingredient. Will this design change allow the product to meet its

target cost?

3. The company president does not believe that the formula should be altered for fear it will

tarnish the company’s brand. She prefers that the company become more efficient in

manufacturing the product. If fixed manufacturing costs can be reduced by $250,000 and

variable direct manufacturing labor costs are reduced by $1 per unit, will Westerly achieve its

target cost?

4. Would you recommend the company follow the proposed solution in requirement 2 or

requirement 3?

SOLUTION

(30 min.) Value engineering, target pricing, and target costs.

1.

Product design and licensing $ 1,700,000

Direct materials 4,000,000

The original cost estimate of $13,200,000 does not meet the company’s requirements. Value

engineering will be needed to reduce the cost per unit to the target cost. Westerly Cosmetic’s

2.

13-5

The design change allows the cream to meet its goal of target costs less than

70% of revenue and target operating income greater than 30% of revenue.

3.

4. The company must take into account many considerations, when deciding between the

preceding requirements 2 and 3. Both options meet the target costing objectives, and generate

In the long run, however, there are other considerations that are important to consider if the

company chooses the alternative in requirement 2 by using the chemical equivalent of the nectar

obtained from the plant in South America. For example, will the nectar become more expensive

Some students might point out that Westerly Cosmetics could implement both the

alternatives presented in requirements 2 and 3. They could reduce the cost of direct materials by

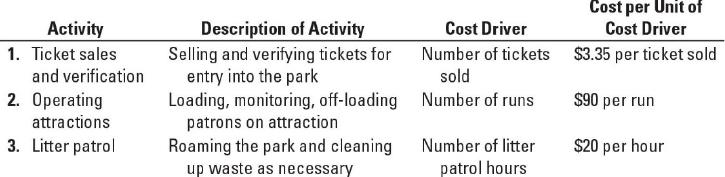

13-28 Target service costs, value engineering, activity-based costing. Lagoon is an

amusement park that offers family-friendly entertainment and attractions. The park boasts more

than 25 acres of fun. The admission price to enter the park, which includes access to all

attractions, is $35. To earn the required rate of return on investment, Lagoon’s target operating

income is 35% of total revenues. Lagoon’s managers have identified the major activities that

13-6

drive the cost of operating the park. The activity cost pools, the cost driver for each activity, and

the cost per unit of the cost driver for each pool are:

The following information describes the existing operations:

a. The average number of patrons per week is 55,000.

b. The total number of runs across all attractions is 11,340 runs each week.

c. It requires 1,750 hours of litter patrol hours to keep the park clean.

In response to competitive pressures and to continue to attract 55,000 patrons per week, Lagoon

has decided to lower ticket prices to $33 per patron. To maintain the same level of profits as

before, Lagoon is looking to make the following changes to reduce operating costs:

a. Reduce the cost of selling and verifying tickets by $0.35 per ticket sold.

b. Reduce the total number of runs across all attractions by 1,000 runs by reducing the operating

hours of some of the attractions that are not very popular.

c. Increase the number of refuse containers in the park at an additional cost of $250 per week.

This will decrease the litter patrol hours by 20%.

Required:

The cost per unit of cost driver for all other activities will remain the same.

a. Will Lagoon achieve its target operating income of 35% of revenues at ticket prices of $35

per ticket before any operating changes?

b. After Lagoon reduces ticket prices and makes the changes and improvements described above,

will Lagoon achieve its target operating income in dollars calculated in requirement 1? Show

your calculations.

c. What challenges might managers at Lagoon encounter in achieving the target cost? How

might they overcome these challenges?

4. A new carbon tax of $3 per run is proposed to be levied on the energy consumed to operate

the attractions. Will Lagoon achieve its target operating income calculated in requirement 1?

If not, by how much will Lagoon have to reduce its costs through value engineering to

achieve the target operating income calculated in requirement 1?

SOLUTION

(30 min.) Target service costs, value engineering, activity-based costing.

1.

Weekly Revenue:

55,000 patrons $35 per patron $1,925,000

Desired profit margin:

13-7

2.

Weekly Revenue:

55,000 patrons $33 per patron $1,815,000

Weekly costs

This profit is slightly greater than Lagoon’s current profitability.

Yes, the changes and improvements will allow Lagoon to achieve the target operating income in

3. The challenges that Lagoon might encounter in achieving the target cost are mostly

13-29 Cost-plus, target return on investment pricing. Sweet Tastings makes candy bars for

vending machines and sells them to vendors in cases of 30 bars. Although Sweet Tastings makes

a variety of candy, the cost differences are insignificant, and the cases all sell for the same price.

Sweet Tastings has a total capital investment of $10,000,000. It expects to produce and sell

400,000 cases of candy next year. Sweet Tastings requires a 12% target return on investment.

Expected costs for next year are:

Variable production costs $3.00 per case

13-8

Variable marketing and distribution costs $2.00 per case

Fixed production costs $400,000

Fixed marketing and distribution costs $700,000

Other fixed costs $500,000

Sweet Tastings prices the cases of candy at full cost plus markup to generate profits equal to the

target return on capital.

Required:

1. What is the target operating income?

2. What is the selling price Sweet Tastings needs to charge to earn the target operating income?

Calculate the markup percentage on full cost.

3. Sweet Tastings is considering increasing its selling price to $13 per case. Assuming production

and sales decrease by 10%, calculate Sweet Tastings’ return on investment. Is increasing the

selling price a good idea?

13-9