SOLUTION

(30–35 min.) Comparison of variable costing and absorption costing.

1. Since production volume variance is unfavorable, the budgeted fixed manufacturing

overhead must be larger than the fixed manufacturing overhead allocated.

= –

2. The problem provides the beginning and ending inventory balances under both, variable

and absorption costing. Under variable costing, all fixed costs are written off as period costs, i.e.,

3. Note that the answer to (3) is independent of (1). The difference in operating income of

$215,000 ($1,610,000 – $1,395,000) is explained by the release of $215,000 of fixed

manufacturing costs when the inventories were decreased during 2017:

Fixed Manuf.

Absorption Variable Overhead

Costing Costing in Inventory

Inventories:

The above schedule in this requirement is a formal presentation of the equation:

=

4. Under absorption costing, operating income is a function of both sales and production

(i.e., change in inventory levels). During 2017, Gammaro experienced a severe decline in

inventory levels: sales were probably higher than anticipated, production was probably lower

9-36 Effects of differing production levels on absorption costing

income: Metrics to minimize inventory buildups. Mountain Press produces

textbooks for high school accounting courses. The company recently hired a new editor, Jan

Green, to handle production and sales of books for an introductory accounting course. Jan’s

compensation depends on the gross margin associated with sales of this book. Jan needs to

decide how many copies of the books to produce. The following information is available for the

fall semester of 2017:

Estimated sales 50,000 books

Beginning inventory 0 books

Average selling price $ 160 per book

Variable production costs $ 100 per book

Fixed production costs $750,000 per semester

The fixed-cost allocation rate is based on expected sales and is therefore equal

to $750,000/50,000 books = $15 per book.

Jan has decided to produce either 50,000, 65,000, or 70,000 books.

Required:

1. Calculate expected gross margin if Jan produces 50,000, 65,000, or 70,000 books. (Make

sure you include the production-volume variance as part of cost of goods sold.)

2. Calculate ending inventory in units and in dollars for each production level.

3. Managers who are paid a bonus that is a function of gross margin may be inspired to produce a

product in excess of demand to maximize their own bonus. The chapter suggested metrics to

discourage managers from producing products in excess of demand. Do you think the following

metrics will accomplish this objective? Show your work.

a. Incorporate a charge of 10% of the cost of the ending inventory as an expense for

evaluating the manager.

b. Include nonfinancial measures (such as the ones recommended on page 341) when

evaluating management and rewarding performance.

SOLUTION

(30 min.) Effects of differing production levels on absorption costing income: Metrics

to minimize inventory buildups.

1.

50,000

books

65,000

Books

70,000

Books

Revenues $8 ,000,000 $8 ,000,000 $8 ,000,000

Cost of goods sold 5,750,000a 5,750,000 5,750,000

2.

50,000

Books

65,000

Books

70,000

Books

Beginning inventory 0 0 0

+ Production 50,000 books 65,000 books 70,000 books

50,000 65,000 70,000

3a.

50,000

books

65,000

books

70,000

books

Gross margin $2,250,000 $2,475,000 $2,550,000

Less 10% Ending inventory 0 (172,500) (230,000)

3b.

50,000

Books

65,000

Books

70,000

Books

1) Inventory change:

A ratio of ending inventory to beginning inventory, as suggested in the book, is not

possible because beginning inventory was zero, so we substituted change in inventory

level.

At 70,000, we are producing 40% more books than we expect to sell. Look to frequency

of new publications as one way to determine the practicality of doing so.

For these nonfinancial measures to be useful they must be incorporated into the reward function

of the manager.

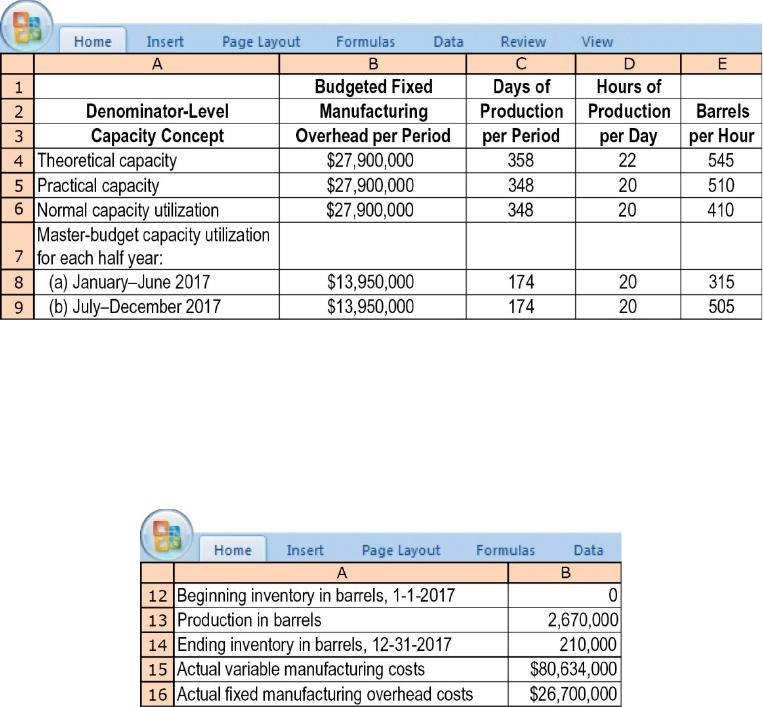

9-37 Alternative denominator-level capacity concepts, effect on operating income. Castle Lager has

just purchased the Jacksonville Brewery. The brewery is two years old and uses absorption costing. It will “sell” its product to Castle

Lager at $47 per barrel. Peter Bryant, Castle Lager’s controller, obtains the following information about Jacksonville Brewery’s

capacity and budgeted fixed manufacturing costs for 2017:

Required:

1. Compute the budgeted fixed manufacturing overhead rate per barrel for each of the denominator-level capacity concepts. Explain

why they are different.

2. In 2017, the Jacksonville Brewery reported these production results:

There are no variable cost variances. Fixed manufacturing overhead cost variances are written off to cost of goods sold in the period in

which they occur. Compute the Jacksonville Brewery’s operating income when the denominator-level capacity is (a) theoretical

capacity, (b) practical capacity, and (c) normal capacity utilization.

SOLUTION

(25–30 min.) Alternative denominator-level capacity concepts, effect on operating income.

1.

Budgeted Fixed

Budgeted Fixed Days of Hours of Budgeted Manufacturing

Denominator-Level

Capacity Concept

Manuf. Overhead

per Period

Production

per Period

Production

per Day

Barrels

per Hour

Denominator Level

(Barrels)

Overhead Rate

per Barrel

(1) (2) (3) (4)

(5) = (2)

´

(3)

´

(4) (6) = (1)

¸

(5)

The differences arise for several reasons:

a. The theoretical and practical capacity concepts emphasize supply factors and are consequently

higher, while normal capacity utilization and master-budget utilization emphasize demand

factors.

b. The two separate six-month rates for the master-budget utilization concept differ because of

seasonal differences in budgeted production.

2. Using column (6) from above,

Per Barrel

Denominator-Level

Capacity Concept

Budgeted

Fixed Mfg.

Overhead

Rate per Barrel

(6)

Budgeted

Variable

Mfg.

Cost Rate

(7)

Budgeted

Total Mfg

Cost Rate

(8) =

(6) + (7)

Fixed Mfg.

Overhead

Costs Allocated

(9) =

2,670,000

´

(6)

Fixed

Mfg. Overhead

Variance

(10) =

$26,700,000 – (9)

Theoretical capacity $6.50 $30.20a$36.70 $17,355,000 $9,345,000 U

Practical capacity 7.86 30.20 38.06 20,986,200 5,713,800 U

¸

Absorption-Costing Income Statement

Theoretical

Capacity

Practical

Capacity

Normal

Capacity

Utilization

Revenues (2,460,000 bbls.

´

$47 per bbl.)

$115,620,000 $115,620,000 $115,620,000

Cost of goods sold

Fixed mfg. overhead costs allocated

(2,670,000 units

´

$6.50; $7.86; $9.78 per unit)

Deduct ending inventory

(210,000 units

´

$36.70; $38.06; $39.98 per unit)

9-38 Motivational considerations in denominator-level capacity

selection (continuation of 9-37).

Required:

1. If the plant manager of the Jacksonville Brewery gets a bonus based on operating income,

which denominator-level capacity concept would he prefer to use? Explain.

2. What denominator-level capacity concept would Castle Lager prefer to use for U.S.

income-tax reporting? Explain.

3. How might the IRS limit the flexibility of an absorption-costing company like Castle Lager

attempting to minimize its taxable income?

SOLUTION

(20 min.) Motivational considerations in denominator-level capacity selection

(continuation of 9-37).

1. If the plant manager gets a bonus based on operating income, he/she will prefer the

denominator-level capacity to be based on normal capacity utilization (or master-budget

utilization). In times of rising inventories, as in 2017, this denominator level will maximize the

fixed overhead trapped in ending inventories and will minimize COGS and maximize operating

2. Given the data in this question, the theoretical capacity concept reports the lowest

3. The IRS may restrict the flexibility of a company in several ways:

a. Restrict the denominator-level concept choice (to say, practical capacity).

9-39 Denominator-level choices, changes in inventory levels, effect

on operating income. Magic Me is a manufacturer of magic kits. It uses absorption

costing based on standard costs and reports the following data for 2017:

There are no price, spending, or efficiency variances. Actual operating costs equal budgeted

operating costs. The production-volume variance is written off to cost of goods sold. For each

choice of denominator level, the budgeted production cost per unit is also the cost per unit of

beginning inventory.

Required:

1. What is the production-volume variance in 2017 when the denominator level is (a)

theoretical capacity, (b) practical capacity, and (c) normal capacity utilization?

2. Prepare absorption costing–based income statements for Magic Me Corporation using

theoretical capacity, practical capacity, and normal capacity utilization as the denominator

levels.

3. Why is the operating income under normal capacity utilization lower than the other two

scenarios?

4. Reconcile the difference in operating income based on theoretical capacity and practical

capacity with the difference in fixed manufacturing overhead included in inventory.

SOLUTION

(25 min.) Denominator-level choices, changes in inventory levels, effect on operating

income.

1.

Normal

Theoretical Practical Capacity

Capacity Capacity Utilization

Denominator level in units 300,000 279,070 232,558

aPVV is unfavorable if budgeted fixed manuf. costs are greater than allocated fixed costs

2.

Normal

Theoretical Practical Capacity

Capacity Capacity Utilization

Units produced 240,000 240,000 240,000

Budgeted fixed mfg. cost allocated per unit $10.00 $10.75 $12.90

Budgeted var. mfg. cost per unit $10.00 $10.00 $10.00

Budgeted cost per unit of inventory or production $20.00 $20.75 $22.90

ABSORPTION-COSTING BASED INCOME

STATEMENTS

Revenues ($50 selling price per unit

´

units sold)

$ 13 ,000 ,000 $ 13 ,000 ,000 $13 ,00 0 ,000

Cost of goods sold

Beginning inventory (40,000 units

´

budgeted

Variable manufacturing costs

(240,000 units

´

$10 per unit)

Allocated fixed manufacturing overhead (240,000

units

´

budgeted fixed mfg. cost allocated per unit:

Deduct ending inventory (20,000b units

´

budgeted

3. Magic Me’s 2017 beginning inventory was 40,000 units; its ending inventory was 20,000

units. So, during 2017, there was a drop of 20,000 units in inventory levels (matching the 20,000

more units sold than produced). The smaller the denominator level, the larger is the budgeted

4.

Reconciliation

Theoretical Capacity Operating Income –

Practical Capacity Operating Income $15,000

20,00

9-40 Variable and absorption costing and breakeven points. LLAP

Company manufactures a specialized hoverboard. LLAP began 2017 with an inventory of 240

hoverboards. During the year, it produced 1,200 boards and sold 1,300 for $800 each. Fixed

production costs were $319,000, and variable production costs were $375 per unit. Fixed

advertising, marketing, and other general and administrative expenses were $150,000, and

variable shipping costs were $20 per board. Assume that the cost of each unit in beginning

inventory is equal to 2017 inventory cost.

Required:

1. Prepare an income statement assuming LLAP uses variable costing.

2. Prepare an income statement assuming LLAP uses absorption costing. LLAP uses a

denominator level of 1,100 units. Production-volume variances are written off to cost of

goods sold.

3. Compute the breakeven point in units sold assuming LLAP uses the following:

a. Variable costing

b. Absorption costing (Production = 1,200 boards)

4. Provide proof of your preceding breakeven calculations.

5. Assume that $44,000 of fixed administrative costs were reclassified as fixed production

costs. Would this reclassification affect the breakeven point using variable costing? What if

absorption costing were used? Explain.

6. The company that supplies LLAP with its specialized impact-resistant material has

announced a price increase of $20 for each board. What effect would this have on the

breakeven points previously calculated in requirement 3?