Process-costing systems using standard costs record standard direct material costs in

Direct Materials Control and standard conversion costs in Conversion Costs Control.

Joint costs are the costs of a production process that yields multiple products

simultaneously.

In the “obtain information” stage of capital budgeting, a company gathers information

from all parts of the value chain to evaluate alternative projects.

COQ measures such as measures of customer satisfaction and employee satisfaction are

useful indicators of long-run performance.

Line management is directly responsible for attaining the goals of the organization.

Cost of Quality (COQ) reports provide more insight about quality improvements and

allow managers to compare trends over time.

Cost management not only helps reduce costs but also improve customer satisfaction

and the quality of a firm’s products.

To maximize profits, managers should produce more of the product with the greatest

contribution margin per unit of the constraining resource.

Value engineering entails improvements in product designs, and changes in materials

specifications.

One advantage of the total factor productivity is that operations managers can use it to

easily understand specific labor productivity issues.

When distribution costs are high, managers can use standard costing to analyze

variances for spending and efficiency variances.

Throughput costing results in a higher amount of manufacturing costs being placed in

inventory than either variable or absorption costing.

Because the variable costs are directly and causally linked to usage, charging them as a

function of the actual usage is appropriate.

Creating a little anxiety among managers and staff with challenging budgets helps

employee work harder to achieve goals.

If a managerial accountant suspected his or her immediate superior of unethical

behavior, who happens to be a chief executive officer or equivalent, the managerial

accountant should request an immediate meeting with the executive committee or the

audit committee.

Direct costs are allocated to the cost object using a cost-allocation method.

A decision table is a summary of the alternative actions, events, outcomes, and

probabilities of events.

The constant gross-margin percentage NRV method allocates joint costs to joint

products in such a way that the gross margin on each joint product is the same as it was

in the previous year.

Underestimating the degree of completion of ending work in process leads to increase

in operating income.

All products yielded from joint product processing have some positive value to the

firm.

To comply with antitrust laws, a company must not engage in predatory pricing,

dumping, or collusive pricing which lessen competition, put another company at a

competitive disadvantage, or harm consumers.

Cost accounting helps to aids managers in formulating strategies, setting prices for

products and services and making decisions about the mix of products and services to

be offered to customers.

If variance analysis is used for performance evaluation, managers are encouraged to

meet targets using creativity and resourcefulness.

When a joint production process yields one product with a high total sales value

compared to the total sales value of the other products of the process, that product is

called a joint product.

In nominal rate of return, the inflation element is the premium above the real rate.

All costs reported on the income statement of a service-sector company are

inventoriable costs.

Variances are used for evaluating performance and for motivating managers.

Management accounting has to strictly follow the rules of generally accepted

accounting principles for the purposes of measurement and reporting.

Direct material costs are the acquisition costs of all materials that eventually become

part of the cost object and cannot be traced to the cost object in an economically

feasible way.

There should be strict congruence between the performance evaluation of a subunit and

the performance evaluation of that subunit’s manager.

Measures which monitor critical performance variables that help managers track

progress toward achieving a company’s strategic goals are collectively called diagnostic

control systems.

Cost of goods sold budget is calculated as follows: beginning finished-goods inventory

+cost of goods manufactured – ending finished-goods inventory

Operating plans are generally expressed through long-run budgets.

The journal entry for transfer from Department B to finished goods is:

Debit: Work in Process—Department B

Credit: Finished Goods Control

The accounting entry to record the conversion cost of the Assembly Department is:

Work in Process-Assembly Department

Accounts Payable Control

Identifying and minimizing the sources of non-value-added manufacturing time

increases a firm’s responsiveness to its customers and reduces its costs.

Engineered costs contain a higher level of uncertainty than discretionary costs.

Timekeeper Corporation has two divisions, Distribution and Manufacturing. The

company’s primary product is high-end watches. Each division’s costs are provided

below:

Manufacturing: Variable costs per unit $2.45

Fixed costs per unit $9.04

Distribution: Variable costs per unit $0.60

Fixed costs per unit $1.20

The Distribution Division has been operating at a capacity of 4,010,000 units a week

and usually purchases 2,005,000 units from the Manufacturing Division and 2,005,000

units from other suppliers at $15.00 per unit.

What is the transfer price per watch from the Manufacturing Division to the

Distribution Division, assuming the method used to place a value on each transfer is

125% of full costs?

A) $11.49

B) $14.36

C) $15.00

D) $19.25

Innovative Metal Products Company manufactures pipes and applies manufacturing

costs to production at a budgeted indirect-cost rate of $12 per direct labor-hour. The

following data are obtained from the accounting records for June 2018:

Direct materials $400,000

Direct labor (16,000 hours @ $11/hour) $ 240,000

Indirect labor $ 25,000

Plant facility rent $ 100,000

Depreciation on plant machinery and equipment $ 42,000

Sales commissions $ 30,000

Administrative expenses $ 40,000

Required:

a. What actual amount of manufacturing overhead costs was incurred during June

2018?

b. What amount of manufacturing overhead was allocated to all jobs during June 2018?

c. For June 2018, was manufacturing overhead underallocated or overallocated?

Explain.

Which of the following is a reason why top managers want lower-level managers to

participate in the budgeting process?

A) To benefit from their experience with the day-to-day aspects of running the business.

B) To reduce the time and cost expended in the budgeting process.

C) To ensure that they do not introduce any budgetary slack.

D) To ensure that the budgets are administered rigidly given the changing market

conditions.

Which of the following correctly describes customer-response time?

A) the amount of time from when an order is ready to start on the production line to

when the product or service is delivered to the customer

B) the amount of time it takes to deliver a completed order to a customer

C) the amount of time from when a customer places an order for a product or requests a

service to when the product or service is delivered to the customer

D) the amount of time from when an order is ready to start on the production line to

when it becomes a finished good

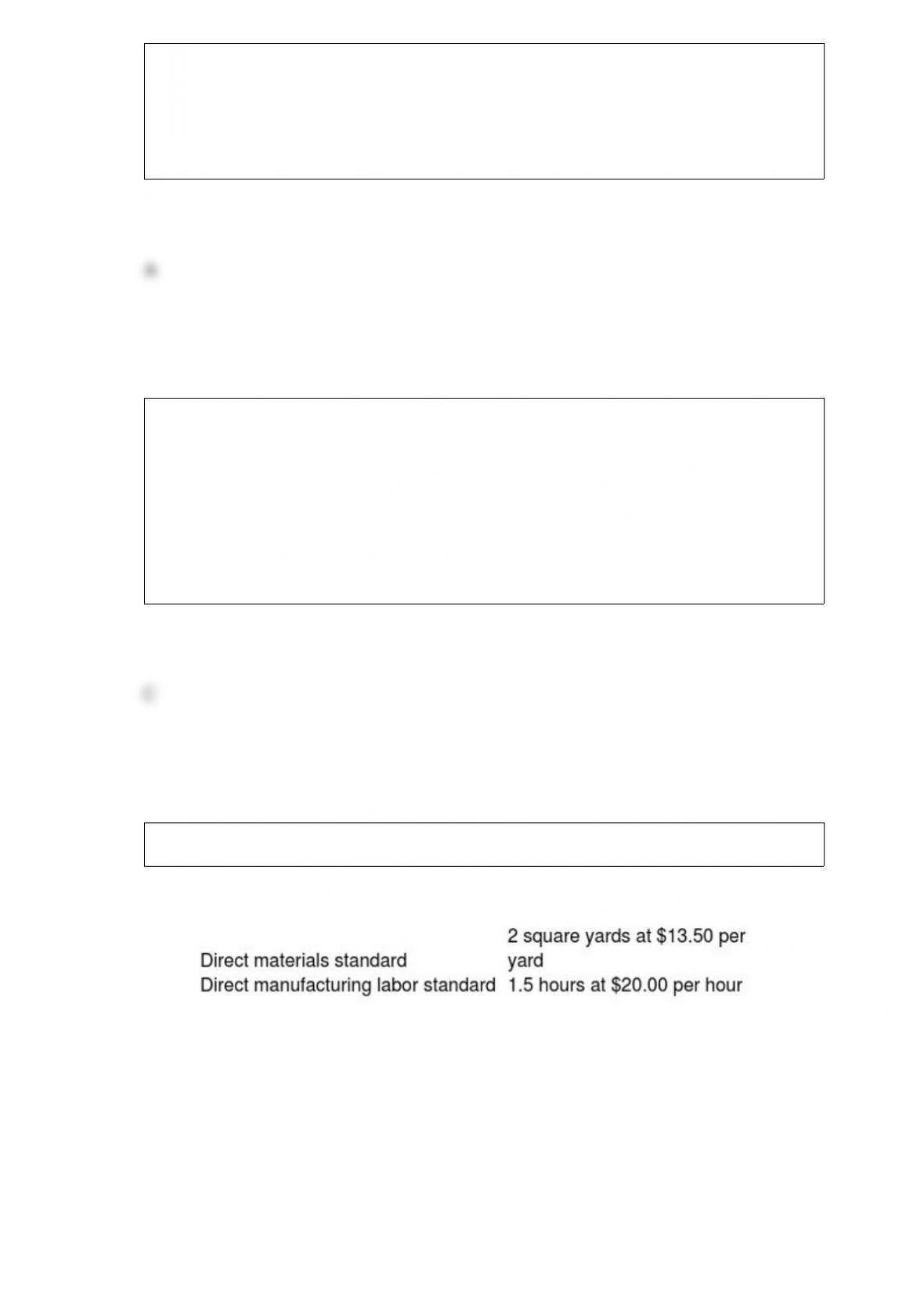

Fine Lumber Inc. mills and finishes furniture kits. A certain kit requires the following:

During the third quarter, the company made 1,500 kits and used 3,150 square yards of

wood costing $42,600. Direct labor totaled 2,100 hours for $46,150.

Required:

a. Compute the direct materials price and efficiency variances for the quarter.

b. Compute the direct manufacturing labor price and efficiency variances for the quarter.

Jupiter Corporation incurred fixed manufacturing costs of $18,000 during 2017. Other

information for 2017 includes:

The budgeted denominator level is 2,400 units.

Units produced total 2,700 units.

Units sold total 1,600 units.

Variable cost per unit is $4

Beginning inventory is zero.

The fixed manufacturing cost rate is based on the budgeted denominator level.

The operating income using variable costing will be ________ as compared to the

operating income under absorption costing. (Round any intermediary calculations to the

nearest cent and your final answer to the nearest dollar.)

A) lower by $8,250.00

B) lower by $2,250.00

C) higher by $8,250.00

D) higher by $2,250.00

Revenue allocation is used when ________.

A) revenues cannot be estimated but can be traced to specific cost objects

B) revenues are related to a particular revenue object but cannot be traced to it in an

economically feasible way

C) revenues are not related to a particular object but can be traced to that object in an

economically feasible way

D) revenue optimization is the goal

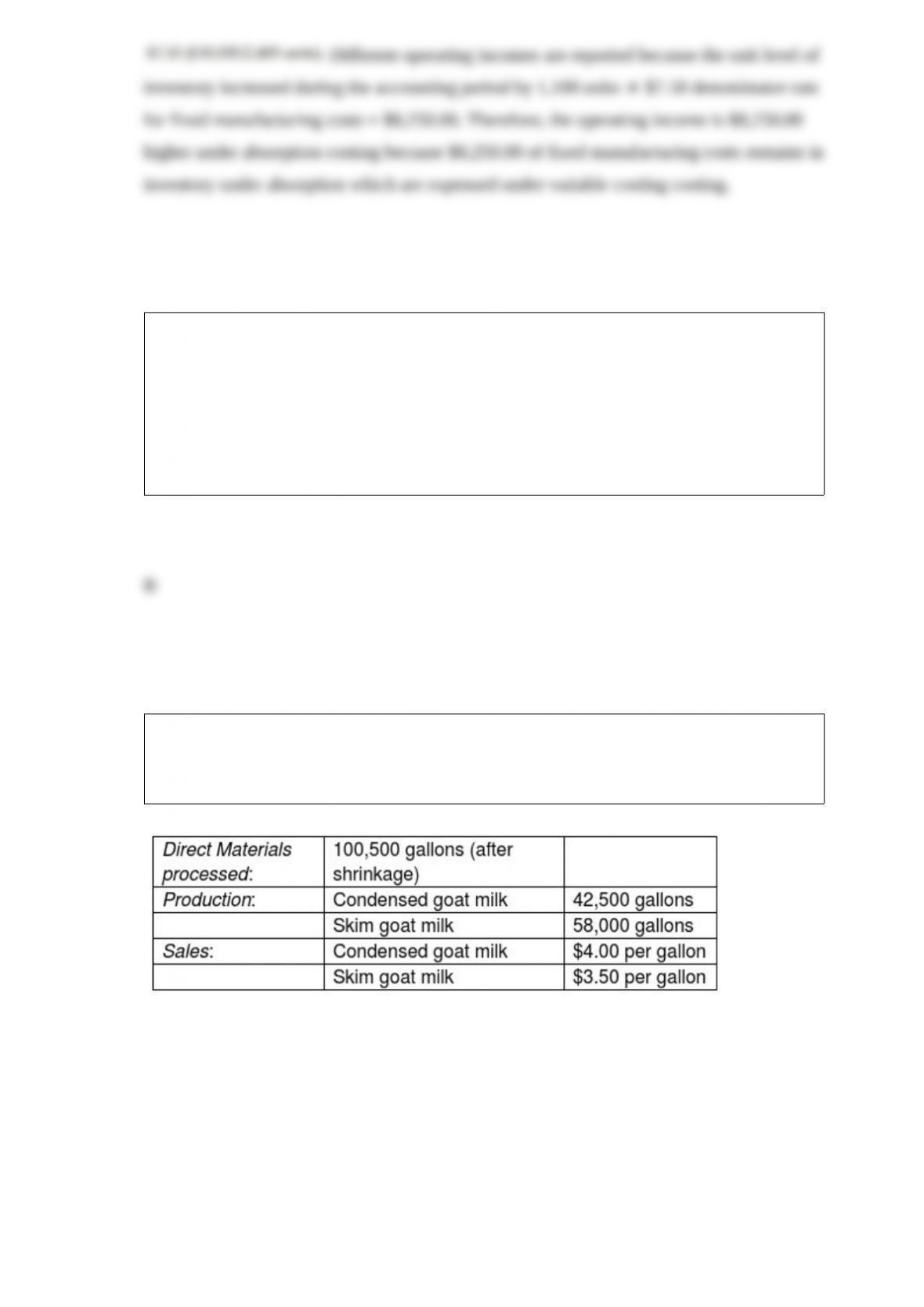

The Green Company processes unprocessed goat milk up to the split-off point where

two products, condensed goat milk and skim goat milk result. The following

information was collected for the month of October:

The costs of purchasing the of unprocessed goat milk and processing it up to the split-off

point to yield a total of 100,500 gallons of saleable product was $191,480. There were no

inventory balances of either product. Condensed goat milk may be processed further to

yield 42,000 gallons (the remainder is shrinkage) of a medicinal milk product, Xyla, for an

additional processing cost of $6 per usable gallon. Xyla can be sold for $21 per gallon.

Skim goat milk can be processed further to yield 56,700 gallons of skim goat ice cream,

for an additional processing cost per usable gallon of $6. The product can be sold for $14

per gallon.

There are no beginning and ending inventory balances.

What is the estimated net realizable value of Xyla at the split-off point?

A) $453,600

B) $464,000

C) $630,000

D) $637,500

Which of the following is false regarding net realizable value (NRV)?

A) it is better to use a product’s market value at the split-off point than its estimated

NRV

B) the estimated NRV at the split-off point is calculated by taking the sales value after

further processing and deducting additional processing costs

C) NRV is the estimated selling price after processing the product beyond the split-off

point.

D) the constant NRV method uses an identical gross-margin percentage for each

product to allocate joint costs

R&D, production, and customer service are business functions that are all included as

part of ________.

A) the value chain

B) benchmarking

C) customer relationship management

D) the supply chain

Each of the following are true of relevant information except:

A) Past costs are helpful when making predictions but not relevant when making

decisions

B) Different alternatives can be compared by examining differences in expected future

revenues and expected total future costs

C) significant past investment amounts are relevant to decision making

D) Not all future revenues and expenses are relevant

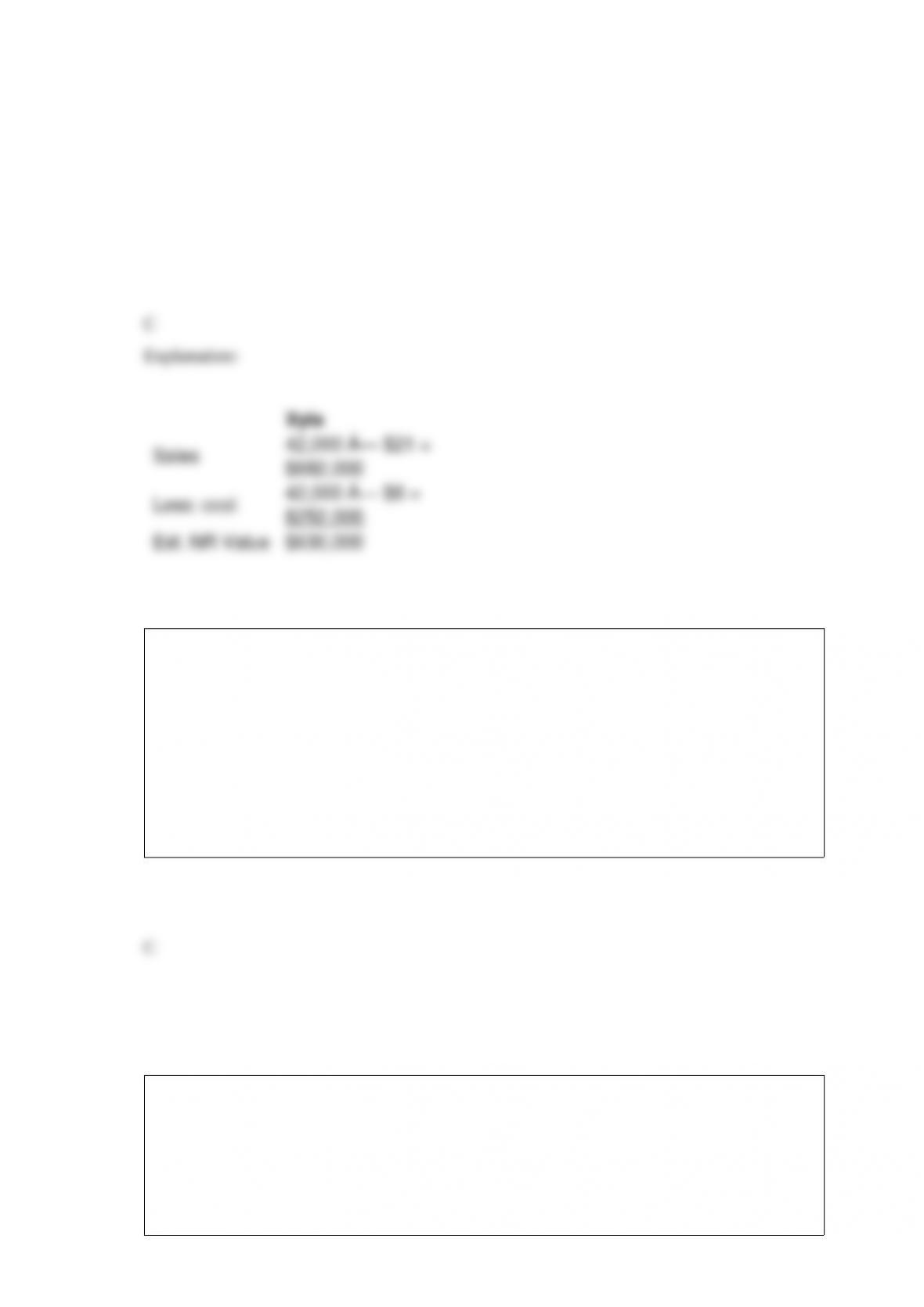

The following information is for High Corp:

If targeted operating income is $50,000, then targeted sales revenue is ________. (Round

the final answer to the nearest dollar.)

A) $540,000

B) $390,000

C) $150,000

D) $180,000

A purchasing manager’s performance is best evaluated using information such as

A) usage efficiency and direct materials price variance

B) direct materials flexible-budget variance

C) direct manufacturing labor flexible-budget variance

D) price and terms bargaining effectiveness, achievement of quality goals, and direct

materials price variance

What role does a trade-in allowance on old equipment play in a decision to retain or

replace equipment?

A) It is relevant since it increases the cost of the new equipment.

B) It is irrelevant since it reduces the cost of the old equipment.

C) It is irrelevant to the decision since it does not impact the cost of the new equipment.

D) It is relevant since it reduces the cost of the new equipment.

Allocating indirect costs to departments based on the relative revenue earned by those

departments is done based on which of the following criterion?

A) direct hours utilized

B) benefits received

C) material resources used

D) cause-and-effect relationships

Standard material cost per kg of raw material is $6.50. Standard material allowed per

unit is 5 Kg. Actual material used per unit is 6.00 Kg. Actual cost per kg is $6.00. What

is the standard cost per output unit?

A) $30.00

B) $36.00

C) $32.50

D) $39.00

Ventaz Corp manufactures small windows for back yard sheds. Historically, its demand

has ranged from 30 to 50 windows per day with an average of 41. Alex is one of the

production workers and he works eight hours a day, five days a week. Each order is one

window and each window takes 10 minutes.

What is the cycle time for an order?

A) 10 minutes per window

B) 100.00 minutes per window

C) 39.29 minutes per window

D) 500.00 minutes per window

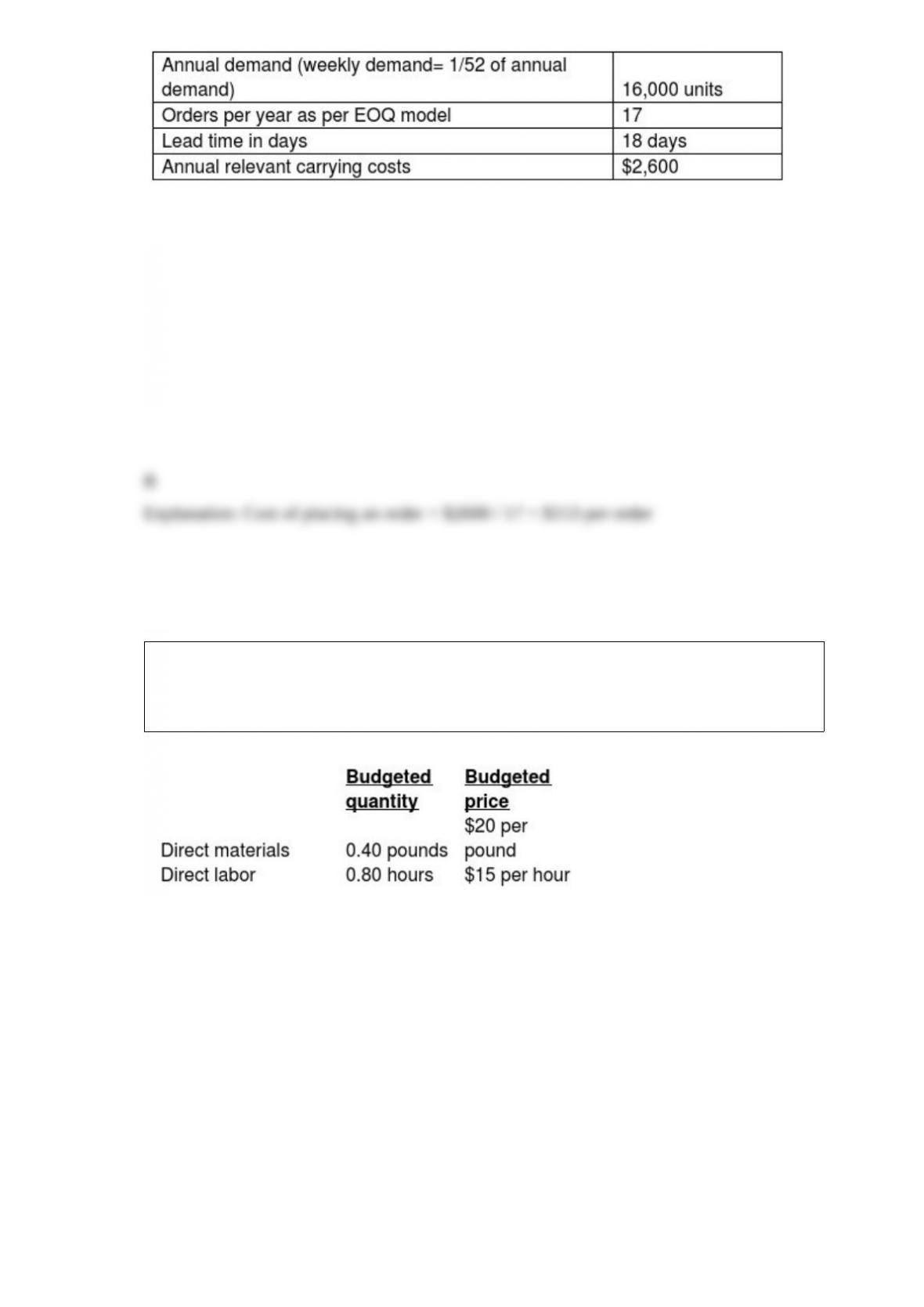

The following information applies to Krynton Corp. which supplies microscopes to

laboratories throughout the country. Krynton purchases the microscopes from a

manufacturer which has a reputation for very high quality in its manufacturing

operation.

Assuming each order was made at the economic order quantity amount, what is the cost of

placing an order?

A) $850 per order

B) $153 per order

C) $144 per order

D) $900 per order

Genent Industries, Inc. (GII), developed standard costs for direct material and direct

labor. In 2017, GII estimated the following standard costs for one of their major

products, the 30-gallon heavy-duty plastic container.

During July, GII produced and sold 4,000 containers using 1,700 pounds of direct

materials at an average cost per pound of $15 and 3,225 direct manufacturing labor hours

at an average wage of $15.25 per hour.

The direct material price variance during July is ________.

A) $20,000 unfavorable

B) $8,500 favorable

C) $8,500 unfavorable

D) $2,000 unfavorable

Harold’s Picture manufactures various picture frames. Each new employee takes 6

hours to make the first picture frame and 4.8 hours to make the second. The

manufacturing overhead charge per hour is $25.

Required:

a. What is the learning-curve percentage, assuming the cumulative average method?

b. What is the time needed to build 8 picture frames by a new employee using the

cumulative average-time method? You may use an index of −0.1520.

c. What is the time needed to produce the 16th frame by a new employee using the

incremental unit-time method? You may use an index of −0.3219.

d. How much manufacturing overhead would be charged to the 16 picture frames using

the average-time approach?

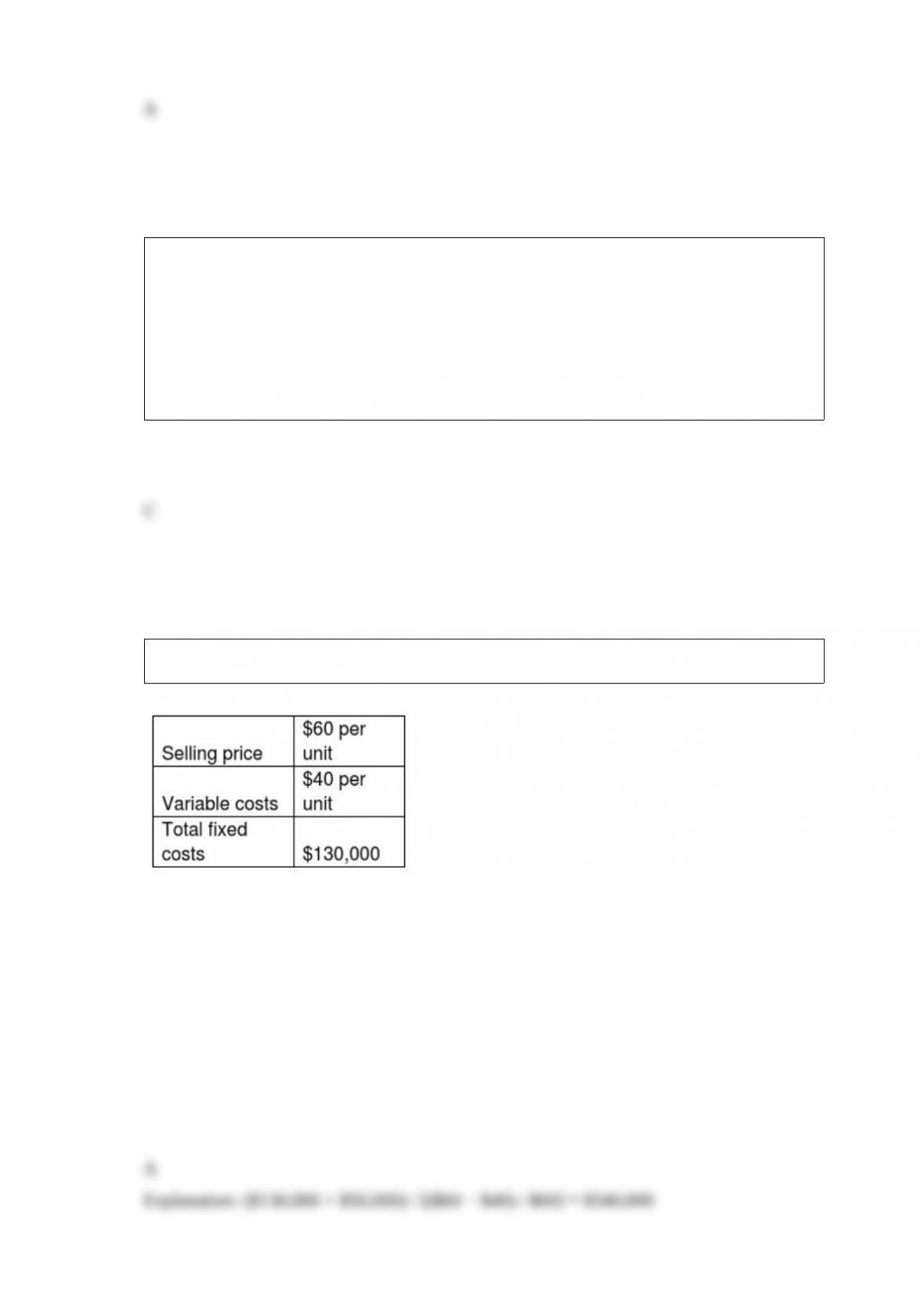

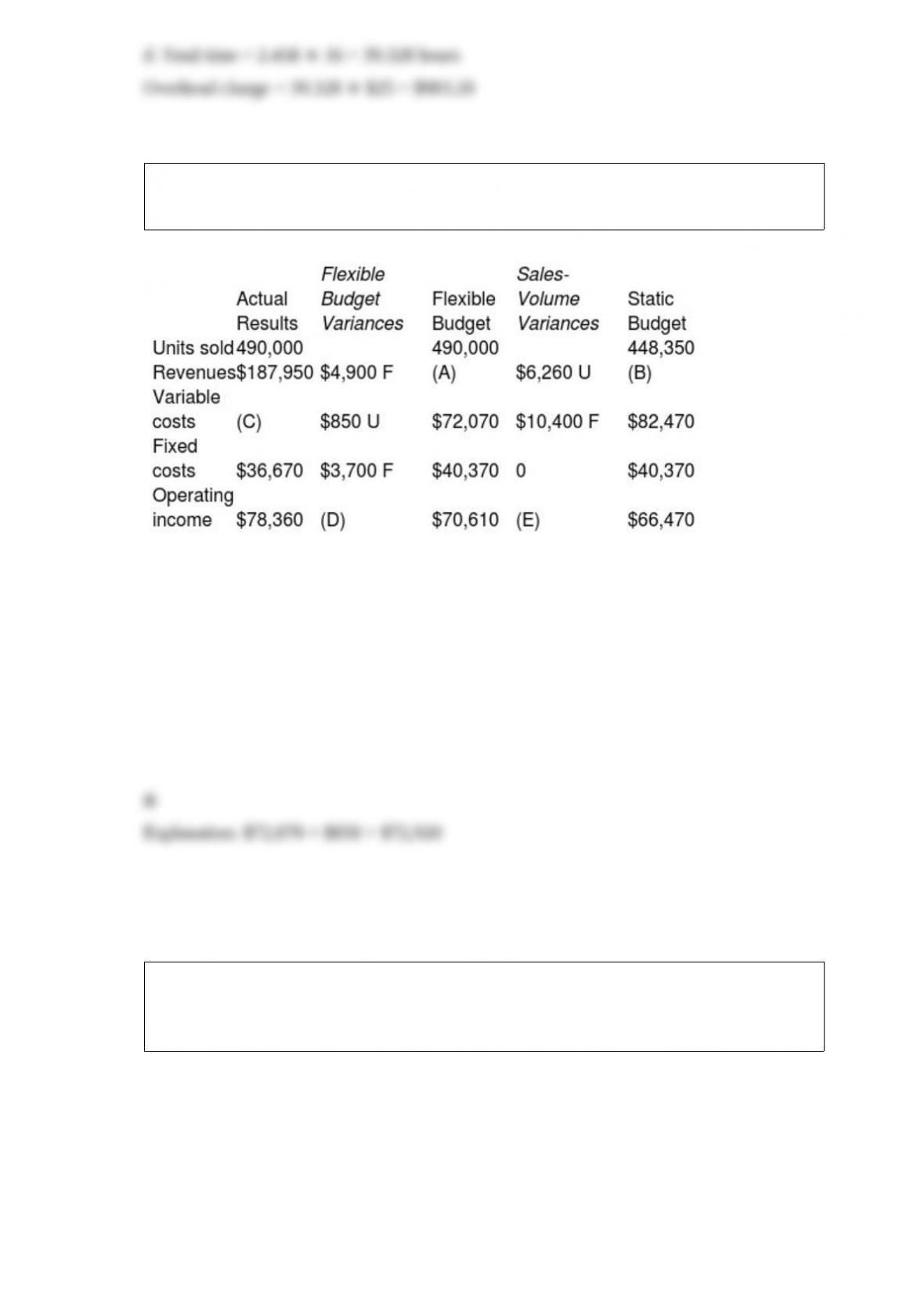

Classic Products Company manufactures colonial style desks. Some of the company’s

data was misplaced. Use the following information to replace the lost data:

What are the actual variable costs (C)?

A) $71,220

B) $72,920

C) $72,070

D) $82,470

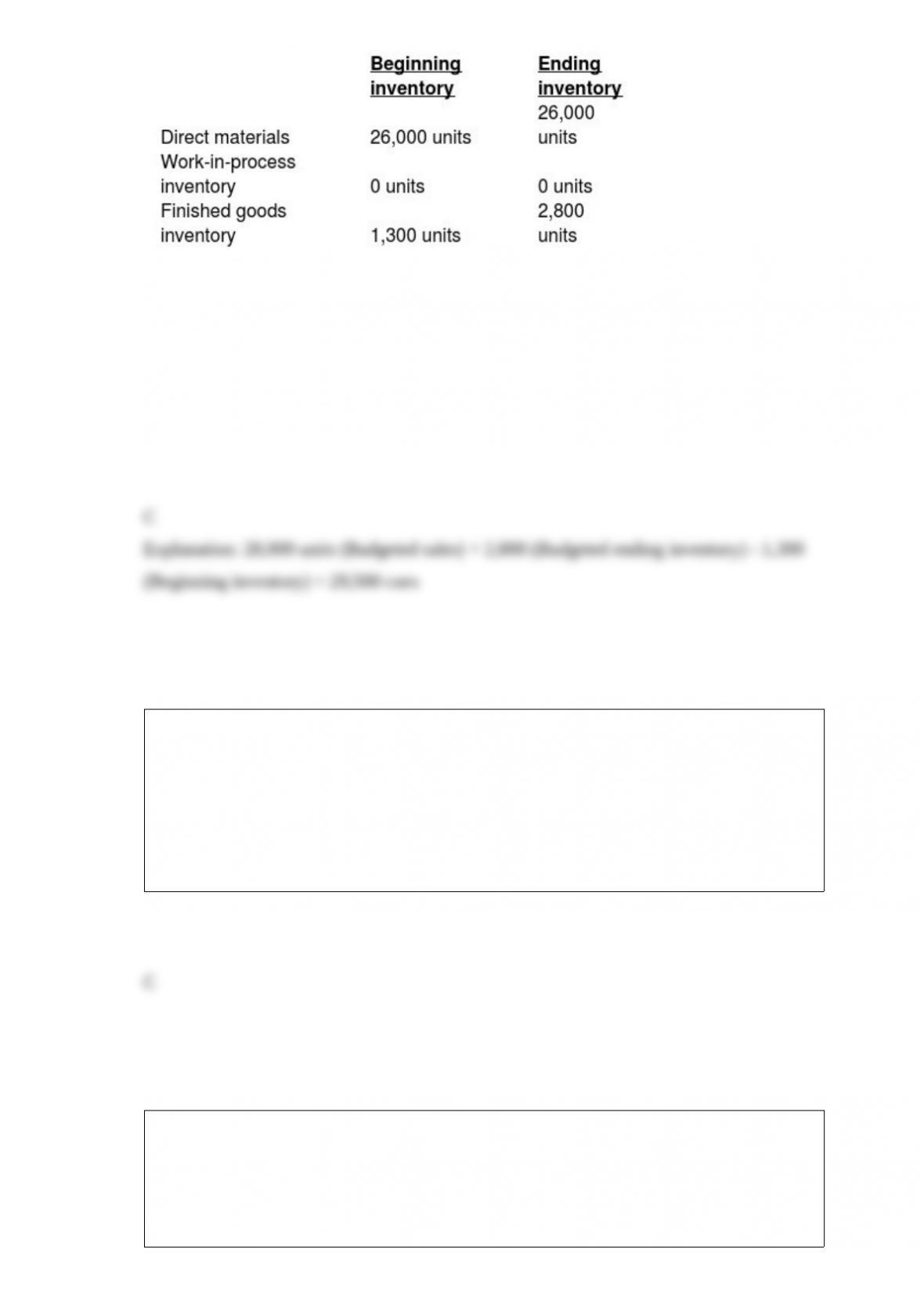

First Class, Inc., expects to sell 28,000 pool cues for $14 each. Direct materials costs

are $3, direct manufacturing labor is $5, and manufacturing overhead is $0.82 per pool

cue. The following inventory levels apply to 2019:

How many pool cues need to be produced in 2019?

A) 30,800 cues

B) 29,300 cues

C) 29,500 cues

D) 26,500 cues

Financial planning models:

A) are primarily used to evaluate the differences between actual and planned volume

B) are not part of sensitivity analysis

C) are mathematical representations of the relationships among factors such as

operating and financing activities that affect the budget

D) allow for analysis of changes in predicted data but not the other underlying

assumptions of the budget

Which of the following would make life-cycle budgeting particularly important to

implement?

A) a very short R&D period with minimal costs but with an emphasis on speed to

market

B) a product that will be brought to market very quickly and will only be offered for a

limited time

C) the development period for a product is long and that the R&D needed and the

design activities are costly

D) a service that will be offered once this year and then eliminated as a result of a

proposed sale of a division

Which of the following is an advantage of internal rate of return method?

A) Sum of IRRs of individual projects gives an IRR of a combination or portfolio of

projects.

B) The percentage returns computed under the IRR method are easy to understand and

compare.

C) It can be expressed as a unique number.

D) It can be used when the required rate of return varies over the life of a project.

Ralph Johnson is paid $30 an hour for straight-time and $40 an hour for overtime. One

week he worked 39 hours, which included 9 hours of overtime, and 4 hours of idle time

caused by material shortages. What is the direct labor cost incurred to the company?

A) $1,050

B) $1,260

C) $1,140

D) $1,100

Product-sustaining costs in activity-based costing are similar to ________.

A) mixed costs

B) variable costs

C) semi-variable costs

D) fixed costs

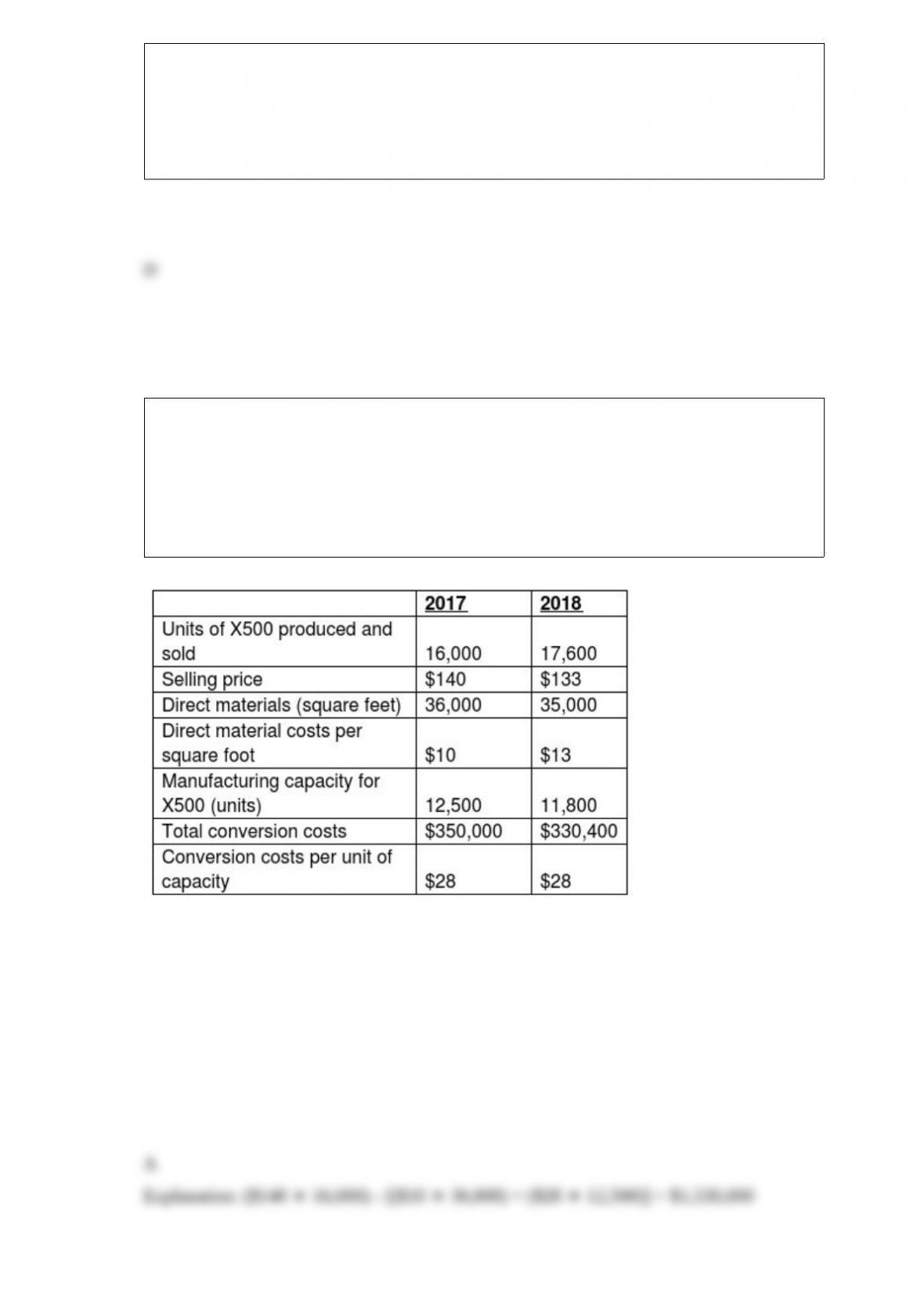

Foley Products Company makes a household appliance with model number X500. The

goal for 2018 is to reduce direct materials usage per unit. No defective units are

currently produced. Manufacturing conversion costs depend on production capacity

defined in terms of X500 units that can be produced. The industry market size for

appliances increased 10% from 2017 to 2018. The following additional data are

available for 2017 and 2018:

What is operating income for 2017?

A) $1,530,000

B) $2,240,000

C) $1,890,000

D) $1,880,000

Samuels Company is considering pricing its 10,000-gallon petroleum tanks using either

variable manufacturing or full product costs as the base. The variable cost base provides

a prospective price of $6,000 and the full cost base provides a prospective price of

$6,100. Which of the following explains the difference in the two prices?

A) the estimated amount of profit

B) the variable cost base estimates fixed costs in the markup percentage while the full

cost base includes an amount for fixed costs

C) there is no explanation since this is known as price discrimination

D) the difference is caused by the inability to estimate fixed cost per unit with any

degree of reliability

Which of the following is the formula for the sales-quantity variance?

A) deducting budgeted contribution margin based on actual units at actual mix from

budgeted contribution margin based on actual units sold at the actual mix

B) deducting budgeted contribution margin based on actual units at actual mix from

budgeted contribution margin based on actual units sold at the budgeted mix

C) deducting budgeted contribution margin based on budgeted units at actual mix from

budgeted contribution margin based on actual units sold at the budgeted mix

D) deducting budgeted contribution margin based on budgeted units at budgeted mix

from budgeted contribution margin based on actual units sold at the budgeted mix

Which of the following cost is included in cost of goods sold?

A) customer service cost

B) manufacturing labor cost

C) distribution cost

D) marketing cost

The use of theoretical capacity results in an unrealistically low fixed manufacturing cost

per unit because it is based on ________.

A) real available capacity

B) an unattainable and idealistic level of capacity

C) normal capacity utilization

D) normal costing

If a sales-volume variance was caused by poor-quality products, then the ________

would be in the best position to explain the variance.

A) production manager

B) sales supervisor

C) financial supervisor

D) logistic manager

What are the advantages of costing rework?

Explain the difference between a joint product and a byproduct. Can a byproduct ever

become a joint product? Also, can a joint product ever become a byproduct?

How does inspecting at various stages of completion affect the amount of normal and

abnormal spoilage?

What are the strengths and weaknesses of the accrual accounting rate-of-return (AARR)

method for evaluating long-term projects?

What are distress prices and which transfer prices should be used for judging

performance if distress prices prevail?

What are the direct costs of a job and in which source documents are they recorded?

Executive compensation plans are based on both financial and nonfinancial

performance measures. Discuss

In order, list the five steps in the decision-making process.

Under what conditions might a manufacturing firm sell a product for less than its

long-term price? Why?

Wilson’s Language School manufactures CDs and DVDs to teach English as a Second

Language. Wilson has just prepared a Cost of Quality Report, and the staff has noticed a

decline in prevention costs as a percentage of total sales over a three-year period. What

changes might Wilson expect to see in appraisal costs as a percentage of sales, internal

failure costs as a percentage of sales, and external failure costs as a percentage of sales

given this trend?

What are the relevant cash inflows and outflows for capital budgeting decisions?

There is uncertainty in defense contracts about the final cost to produce a new weapon

or equipment. Explain.

What are the two methods to account for byproducts. Which is the more appropriate

method to use and why?

Explain the term cost leadership. What are the possible ways through which a company

would try to become a cost leader? How far is it desirable to implement cost reduction

measures?

Under the benefits-received criterion, the physical-measure method is much less

desirable than the sales value at split-off method. Why?