SOLUTION

(20-25 mins.) Stand-alone revenue allocation

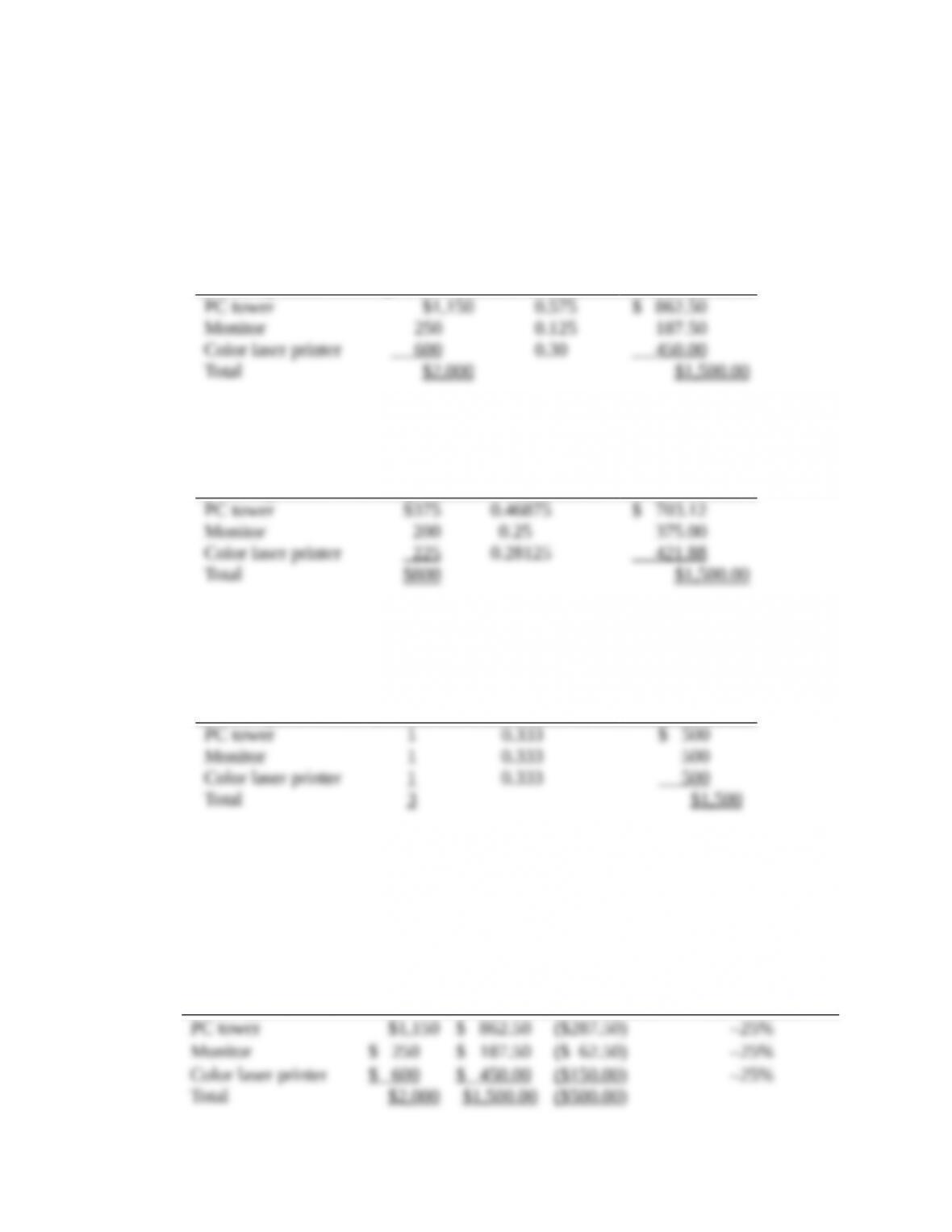

1. Allocation using individual selling price per unit.

Computer

Hardware

Component

Individual

Selling Price

per Unit

Percentage of

Total Price

Allocation

% × $1,500

2. Allocation using cost per unit

Computer

Hardware

Component Cost per Unit

Percentage of

Total Cost

Allocation

% × $1,500

3. Allocation using number of individual units of product sold per bundle

Computer

Hardware

Component

Individual

Units of

Product Sold

per Bundle

Percentage of

Total Price

Allocation

% × $1,500

4. Sharing on the basis of revenue makes the most sense. Using this method each

division takes a uniform percentage decrease in the revenue received regardless of the cost of

the division’s individual products. For example:

Computer

Hardware

Component

Individual

Price per

Unit

(a)

Allocated

Revenue

per Unit

(b)

Decrease in

Price

(c) = (a) –(b)

Percentage

Decrease in Price

by Product

(d) = (c)÷(a)

Furthermore, the cost-based method might actually discourage cost efficiencies. Increasing the

cost per unit of product relative to other products would give the division a greater share of the

overall revenue.

Last, under the physical unit allocation method, the motivation of the divisional managers to

produce for the bundled purchase would likely change significantly. The PC Tower Division

15-34 Support-department cost allocations; single-department cost pools; direct,

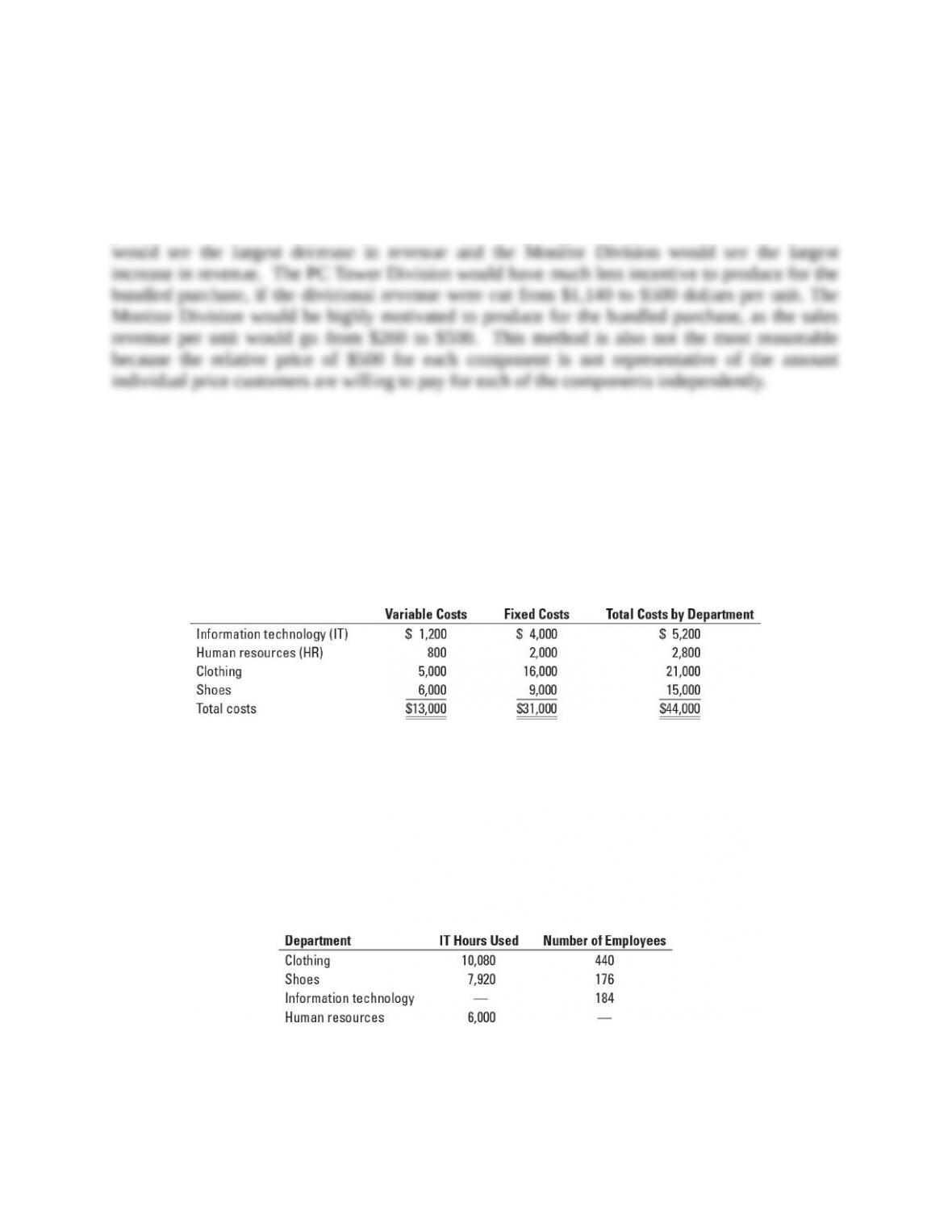

step-down, and reciprocal methods. Sportz, Inc., manufactures athletic shoes and athletic

clothing for both amateur and professional athletes. The company has two product lines (clothing

and shoes), which are produced in separate manufacturing facilities; however, both

manufacturing facilities share the same support services for information technology and human

resources. The following shows costs (in thousands) for each manufacturing facility and for each

support department.

The total costs of the support departments (IT and HR) are allocated to the production

departments (clothing and shoes) using a single rate based on the following:

Information technology: Number of IT labor-hours worked by department

Human resources: Number of employees supported by department

Data on the bases, by department, are given as follows:

Required:

1. What are the total costs of the production departments (clothing and shoes) after the

support-department costs of information technology and human resources have been allocated

using (a) the direct method, (b) the step-down method (allocate information technology first),

(c) the step-down method (allocate human resources first), and (d) the reciprocal method?

2. Assume that all of the work of the IT department could be outsourced to an independent

company for $97.50 per hour. If Sportz no longer operated its own IT department, 30% of the

fixed costs of the IT department could be eliminated. Should Sportz outsource its IT

services?

SOLUTION

(40-60 min.) Support-department cost allocations: single-department cost pools; direct,

step-down, and reciprocal methods.

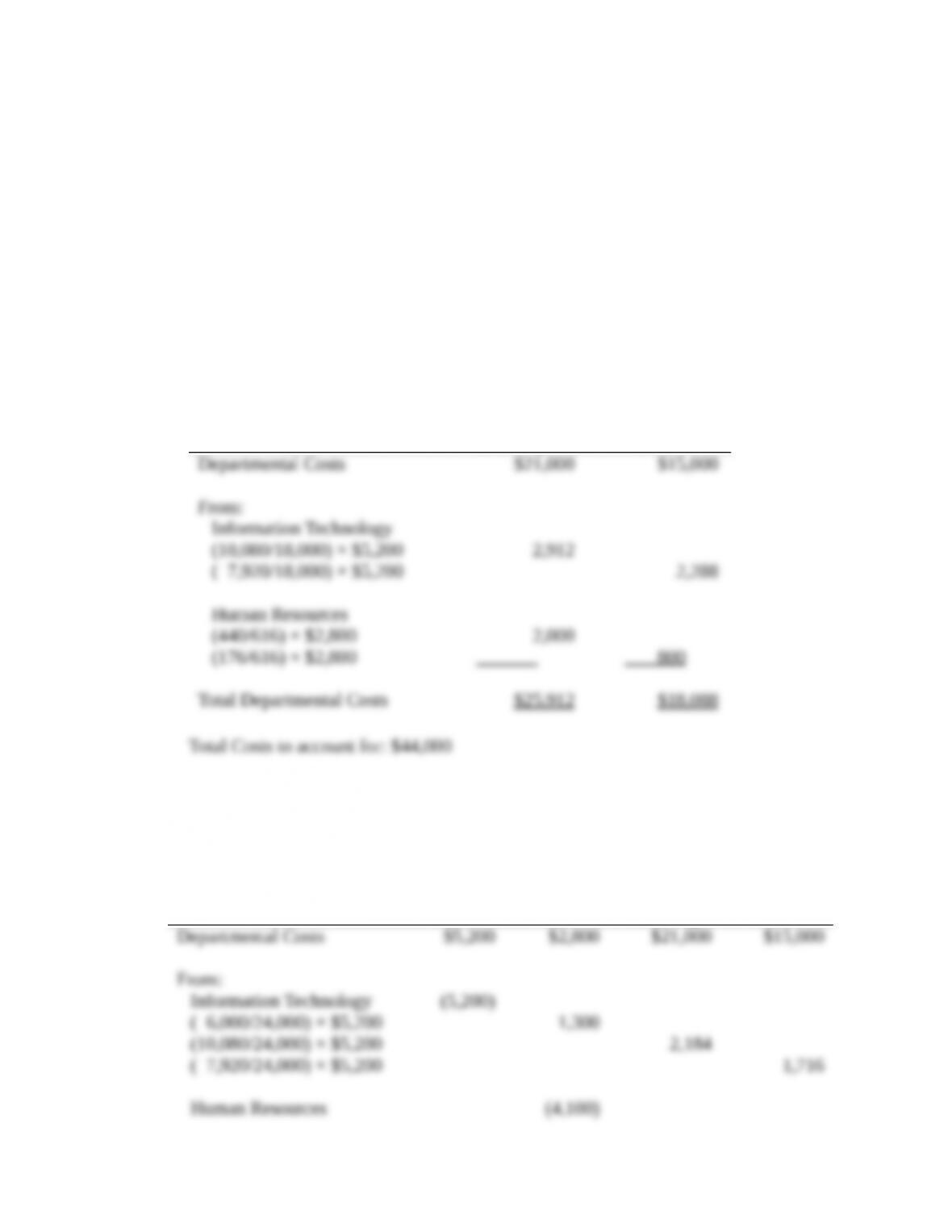

1. a. Allocate the total Support Department costs to the production departments under the

Direct Allocation Method:

Clothing Shoes

b. Allocate the Support Department Costs to the Production Department under the

Step-down (Sequential) Allocation Method IT first sequentially:

To:

IT HR Clothing Shoes

c. Allocate the Support Department Costs to the Production Department under the

Step-down (Sequential) Allocation Method HR first sequentially:

To:

HR IT Clothing Shoes

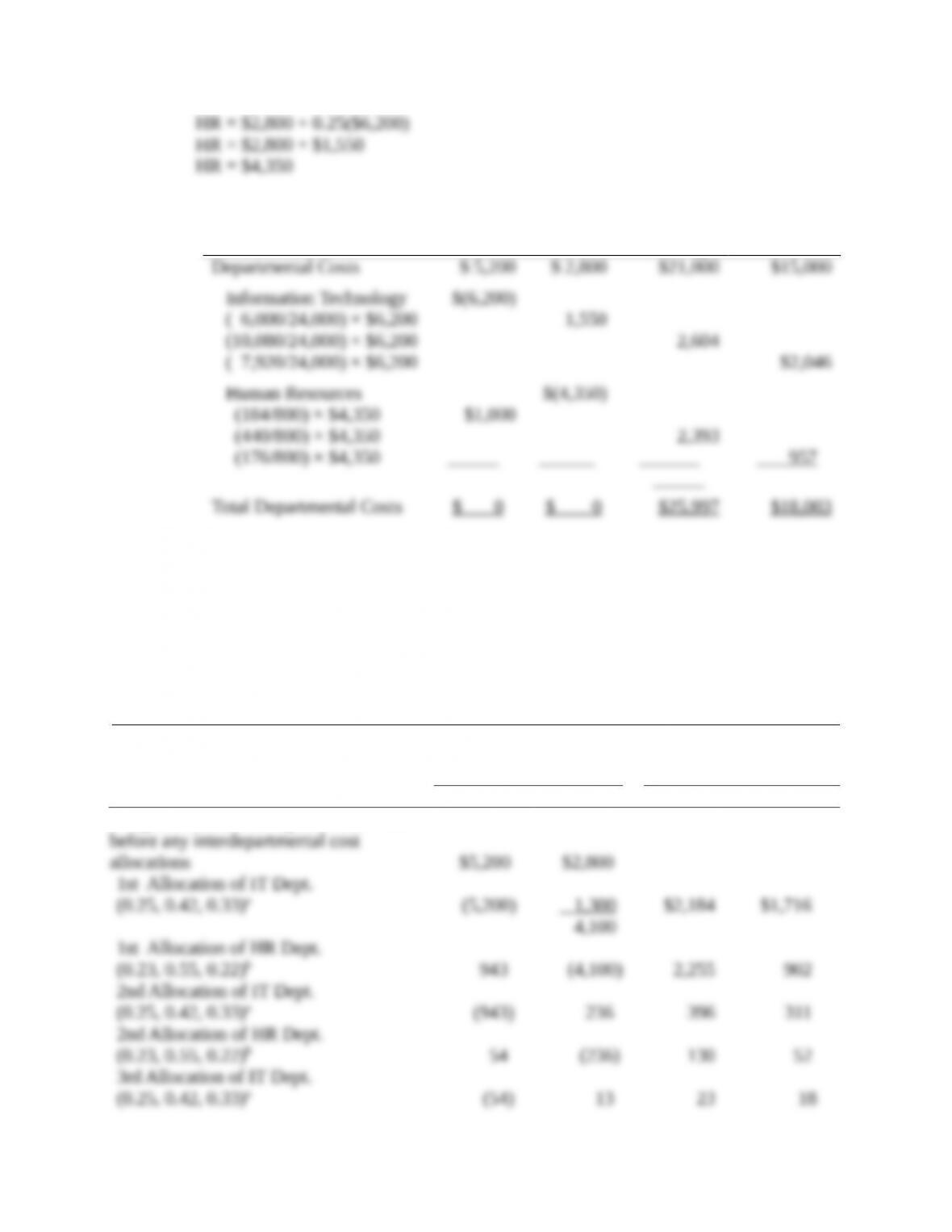

d. Allocate the Support Department Costs to the Production Department under the

Reciprocal Allocation Method:

i. Assign reciprocal equations to the support departments. Note that IT uses 184/800 or

0.23 of HR department resources (allocation based on number of employees) and HR uses

6,000/24,000 of IT department resources (allocation based on number of IT hours).

ii. Solve the equation to complete the reciprocal costs of the support departments

iii. Allocate Reciprocal costs to departments (all numbers rounded to nearest dollar)

IT HR Clothing Shoes

Costs allocated to the Clothing Department equal $4,997 ($2,604 + $2,393). Costs allocated to

the Shoes Department equal $3,003 ($2,046 + $957). Total Costs to account for is $44,000.

Solution Exhibit 15-34 shows the allocation of the IT and HR Department costs to the Clothing

Department ($4,997) and to the Shoes Department ($3,003) using repeated iterations.

SOLUTION EXHIBIT 15-34

Reciprocal Method of Allocating Support Department Costs for Sportz, Inc. Using

Repeated Iterations.

Support

Departments

Operating

Departments

IT HR Clothing Shoes

Budgeted manufacturing overhead costs

Total accounts allocated and reallocated (the numbers in parentheses in first two columns)

2. If Sportz decides to outsource its Information Technology needs, the company has to pay

$97.50 per hour for the 24,000 hours of IT services it needs, for a total outlay of $2,340,000. In

return, Sportz saves 30% of the IT department’s fixed costs ($4,000,000 × 0.30 = $1,200,000).

The issue then is how much it saves in variable costs. The key is to recognize that Sportz saves

more than the $1,200,000 of variable costs assigned to IT because of the interlinks between the

IT and HR groups. To quantify this, we have to calculate the reciprocated cost of the IT

department using the variable costs alone.

Beyond the financial perspective, Sportz should decide how important it is to the company to

have control over its own IT support. It may be critical, especially with information

technology, that the knowledge and expertise be maintained within the firm so critical

decisions do not depend on a third party. It may also be critical for security purposes to

maintain IT support internally so that company information is kept confidential. In addition,

by maintaining IT support in-house, the response time to production departments and other

support departments will likely be greater than if the services are outsourced. It is also

possible that the quality of the service would be higher as well. Finally, Sportz should

consider the internal repercussions of dismissing a large portion of its workforce. This could

create morale issues for the company’s remaining workers.

15-35 Revenue allocation, bundled products. Boca Resorts (BR) operates a five-star hotel

with a world-class spa. BR has a decentralized management structure, with three divisions:

Lodging (rooms, conference facilities)

Food (restaurants and in-room service)

Spa

Starting next month, BR will offer a two-day, two-person “getaway package” for $1,000.

This deal includes the following:

Jennifer Gibson, president of the spa division, recently asked the CEO of BR how her division

would share in the $1,000 revenue from the getaway package. The spa was operating at 100%

capacity. Currently, anyone booking the package was guaranteed access to a spa appointment.

Gibson noted that every “getaway” booking would displace $300 of other spa bookings not

related to the package. She emphasized that the high demand reflected the devotion of her team

to keeping the spa rated one of the “Best 10 Luxury Spas in the World” by Travel Monthly. As an

aside, she also noted that the lodging and food divisions had to turn away customers during only

“peak-season events such as the New Year’s period.”

Required:

1. Using selling prices, allocate the $1,000 getaway-package revenue to the three divisions

using:

a. The stand-alone revenue-allocation method

b. The incremental revenue-allocation method (with spa first, then lodging, and then food)

2. What are the pros and cons of the two methods in requirement 1?

3. Because the spa division is able to book the spa at 100% capacity, the company CEO has

decided to revise the getaway package to only include the lodging and food offerings shown

previously. The new package will sell for $800. Allocate the revenue to the lodging and food

divisions using the following:

a. The Shapley value method

b. The weighted Shapley value method, assuming that lodging is three times as likely to sell

as the food

SOLUTION

(20–25 min.) Revenue allocation, bundled products.

1.a. The stand-alone revenues (using unit selling prices) of the three components of the $800

package are:

Lodging

$750 $1,000 0.60 $1,000 $600

$1, 250 ´ = ´ =

Spa

$300 $1,000 0.24 $1,000 $240

$1, 250 ´ = ´ =

Food

$200 $1,000 0.16 $1,000 $160

$1, 250 ´ = ´ =

Total Allocated $ 1,0 00

b.

Product

Revenue

Allocated

Cumulative Revenue

Allocated

2. The pros of the stand-alone-revenue-allocation method include the following:

a. Each item in the bundle receives a positive weight, which means the resulting

b. It uses market-based evidence (unit selling prices) to decide the revenue allocations—

The cons of the stand-alone revenue-allocation method include the following:

a. It ignores the relative importance of the individual components in attracting

b. It ignores the opportunity cost of the individual components in the bundle. The spa

c. The weight can be artificially inflated by individual product managers setting “high”

The pros of the incremental method include the following:

a. It has the potential to reflect that some products in the bundle are more highly valued

b. Once the sequence is chosen, it is straightforward to implement.

3. Under the Shapley value method the revenue allocated represents an average of the

revenue that would have been received if each product or service were ranked as both the

primary party and the incremental party

a.

Product

Revenue Received under

Incremental Method

Product

Revenue Received under

Incremental Method

Revenue allocation under the Shapley value method, based on the data from the

incremental rankings above is:

b. Assuming that lodging is three times as likely to be sold as food, the revenue

allocated under the weighted Shapley value method, using data from the incremental

rankings above would be:

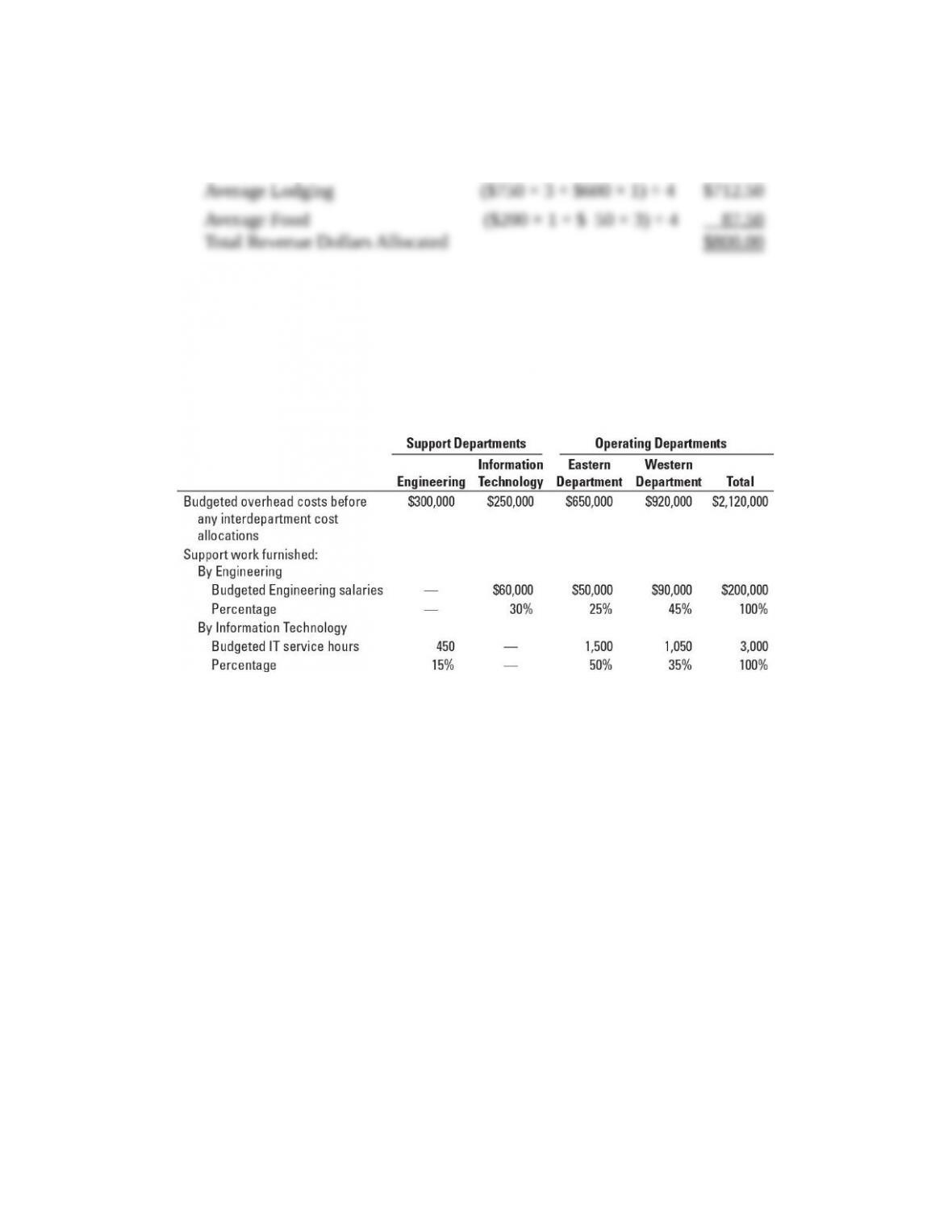

15-36 Support-department cost allocations; direct, step-down, and reciprocal methods.

Ballantine Corporation has two operating departments: Eastern Department and Western

Department. Each of the operating departments uses the services of the company’s two support

departments: Engineering and Information Technology. Additionally, the Engineering and

Information Technology departments use the services of each other. Data concerning the past

year are as follows:

Required:

1. What are the total overhead costs of the operating departments (Eastern and Western) after

the support-department costs of Engineering and Information Technology have been

allocated using (a) the direct method, (b) the step-down method (allocate Engineering first),

(c) the step-down method (allocate Information Technology first), and (d) the reciprocal

method?

2. Which method would you recommend that Ballantine Corporation use to allocate

service-department costs? Why?