CHAPTER 13

PRICING DECISIONS AND COST MANAGEMENT

13-1 What are the three major influences on pricing decisions?

The three major influences on pricing decisions are

13-2 “Relevant costs for pricing decisions are full costs of the product.” Do you agree?

Explain.

Not necessarily. For a one-time-only special order, the relevant costs are only those costs that

13-3 Describe four purposes of cost allocation.

Four purposes of cost allocation are as follows:

1. To provide information for economic decisions

13-4 How is activity-based costing useful for pricing decisions?

Activity-based costing helps managers in pricing decisions in two ways.

1. It gives managers more accurate product-cost information for making pricing decisions.

13-5 Describe two alternative approaches to long-run pricing decisions.

Two alternative approaches to long-run pricing decisions are the following:

1. Market-based pricing, an important form of which is target pricing. The market-based

2. Cost-based pricing which asks, “What does it cost us to make this product and, hence,

13-6 What is a target cost per unit?

13-7 Describe value engineering and its role in target costing.

Value engineering is a systematic evaluation of all aspects of the value-chain business functions,

with the objective of reducing costs while satisfying customer needs. Value engineering via

13-1

13-8 Give two examples of a value-added cost and two examples of a non-value-added cost.

A value-added cost is a cost that customers perceive as adding value, or utility, to a product or

service. Examples are costs of materials, direct labor, tools, and machinery. A nonvalue-added

13-9 “It is not important for a company to distinguish between cost incurrence and locked-in

costs.” Do you agree? Explain.

13-10 What is cost-plus pricing?

13-11 Describe three alternative cost-plus pricing methods.

Cost-plus pricing methods vary with the bases used to calculate prices. Examples are

13-12 Give two examples in which the difference in the costs of two products or services is

much smaller than the difference in their prices.

Two examples where the difference in the costs of two products or services is much smaller than

the differences in their prices are:

1. The difference in prices charged for a telephone call, hotel room, or car rental during

2. The difference in costs for an airplane seat sold to a passenger traveling on business or a

passenger traveling for pleasure is roughly the same. However, airline companies price

13-13 What is life-cycle budgeting?

13-14 What are three benefits of using a product life-cycle reporting format?

Three benefits of using a product life-cycle reporting format are the following:

1. The full set of revenues and costs associated with each product becomes more visible.

13-2

13-15 Define predatory pricing, dumping, and collusive pricing.

Predatory pricing occurs when a business deliberately prices below its costs in an effort to drive

competitors out of the market and restrict supply and then raises prices rather than enlarge

13-16 Which of the following statements regarding price elasticity is incorrect?

a. A product with a perfectly inelastic demand would have the same demand even as prices

change.

b. A product with a perfectly inelastic demand would see demand change as prices change.

c. When demand is price elastic, lower prices stimulate demand.

d. When demand is price elastic, higher prices reduce demand.

SOLUTION

Choice “b” is the correct answer. The statement is incorrect because a product with a perfectly inelastic

demand would not see demand change as prices change.Choice “a” is incorrect. This statement is true.

13-17 Value-added, non-value-added costs. The Magill Repair Shop repairs and services

machine tools. A summary of its costs (by activity) for 2017 is as follows:

a. Materials and labor for servicing machine tools $1,100,000

b. Rework costs 90,000

c. Expediting costs caused by work delays 65,000

d. Materials-handling costs 80,000

e. Materials-procurement and inspection costs 45,000

13-3

f. Preventive maintenance of equipment 55,000

g. Breakdown maintenance of equipment 75,000

Required:

1. Classify each cost as value-added, non-value-added, or in the gray area between.

2. For any cost classified in the gray area, assume 60% is value-added and 40% is

non-value-added. How much of the total of all seven costs is value-added and how much is

non-value-added?

3. Magill is considering the following changes: (a) introducing quality-improvement programs

whose net effect will be to reduce rework and expediting costs by 40% and materials and

labor costs for servicing machine tools by 5%; (b) working with suppliers to reduce

materials-procurement and inspection costs by 20% and materials-handling costs by 30%; and

(c) increasing preventive-maintenance costs by 70% to reduce breakdown-maintenance costs

by 50%. Calculate the effect of programs (a), (b), and (c) on value-added costs,

non-value-added costs, and total costs. Comment briefly.

SOLUTION

(25–30 min.) Value-added, nonvalue-added costs.

1.

Category Examples

Value-added costs a. Materials and labor for regular repairs $1,100,000

Classifications of value-added, nonvalue-added, and gray area costs are often not clear-cut.

Other classifications of some of the cost categories are also plausible. For example, some

students may include materials handling, materials procurement, and inspection costs and

2. Total costs in the gray area are $180,000. Of this, we assume 60%, or $108,000, are

value-added and 40%, or $72,000, are nonvalue-added.

Total value-added costs: $1,100,000 + $108,000 $1,208,000

13-4

3. Effect on Costs Classified as

Program

Value-Add

ed

Nonvalue-

Added

Gray

Area

(a) Quality improvement programs to

• reduce rework costs by 40% (0.40 $90,000)

• reduce expediting costs by 40%

–$ 36,000

(b) Working with suppliers to

• reduce materials procurement and inspection costs by

20% (0.20 $45,000)

• reduce materials handling costs by 30%

Total effect

Transferring 60% of gray area costs (0.60

$33,000 = $19,800) as value-added and 40%

–$ 9,000

– 33,000

(c) Maintenance programs to

• increase preventive maintenance costs by 70%

$15,400) as nonvalue-added

Effect on value-added and nonvalue-added costs

+$ 23 ,100

+$ 23 ,100

+ 15 ,400

–$ 22 ,100

– 38 ,500

$ 0

Total effect of all programs

Value-added and nonvalue-added costs calculated in

requirement 2

Expected value-added and nonvalue-added costs after

–$ 51,700

1 ,208,000

–$ 97,300

302 ,000

If these programs had been implemented, total costs would have decreased from $1,510,000

Some students might question whether Magill should implement program (c) because the

13-5

Magill may wish to not do preventive maintenance reducing costs by another $1,000. This may

also cause students to debate why preventive maintenance is in the gray area of costs. It is value

added only when the preventive maintenance activity reduces breakdown maintenance costs.

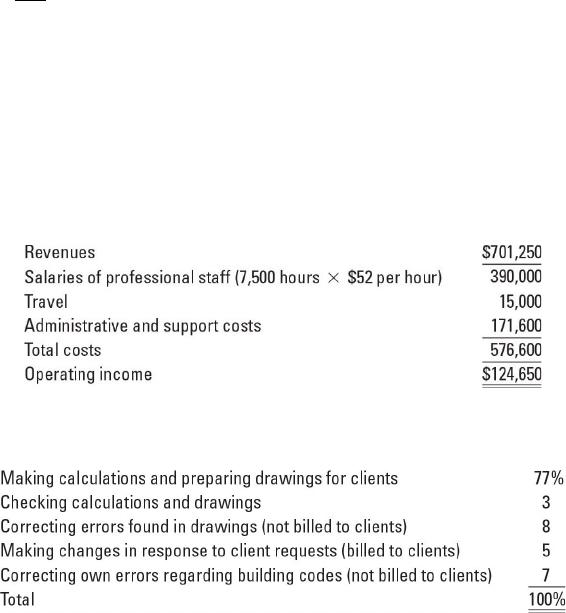

13-18 Target operating income, value-added costs, service company. Calvert Associates

prepares architectural drawings to conform to local structural-safety codes. Its income statement

for 2017 is as follows:

The percentage of time spent by professional staff on various activities follows:

Assume administrative and support costs vary with professional-labor costs. Consider each

requirement independently.

Required:

1. How much of the total costs in 2017 are value-added, non-value-added, or in the gray area

between? Explain your answers briefly. What actions can Calvert take to reduce its costs?

2. What are the consequences of misclassifying a non-value-added cost as a value-added

cost? When in doubt, would you classify a cost as a value-added or non-value-added

cost? Explain briefly.

3. Suppose Calvert could eliminate all errors so that it did not need to spend any time making

corrections and, as a result, could proportionately reduce professional-labor costs. Calculate

Calvert’s operating income for 2017.

4. Now suppose Calvert could take on as much business as it could complete, but it could not

add more professional staff. Assume Calvert could eliminate all errors so that it does not need

to spend any time correcting errors. Assume Calvert could use the time saved to increase

revenues proportionately. Assume travel costs will remain at $15,000. Calculate Calvert’s

operating income for 2017.

SOLUTION

(2530 min.) Target operating income, value-added costs, service company.

13-6

1. The classification of total costs in 2017 into value-added, nonvalue-added, or in the gray

area in between follows:

Value Gray Nonvalue- Total

Added Area added (4) =

(1) (2) (3) (1)+(2)+(3)

Doing calculations and preparing drawings

77% × $390,000 $300,300 $300,300

Checking calculations and drawings

3% × $390,000 $11,700 11,700

Correcting errors found in drawings

Doing calculations and responding to client requests for changes are value-added costs because

customers perceive these costs as necessary for the service of preparing architectural drawings.

Costs incurred on correcting errors in drawings and making changes because they were

2. The consequences of classifying a non-value-added cost as a value-added cost is that

managers may hesitate to reduce these costs thinking that if they eliminate these costs it would

For these reasons, managers who are unsure if a cost is value-added or nonvalue-added,

often classify costs as nonvalue-added. The nonvalue-added classification focuses organization

13-7

3. Reduction in professional labor-hours by

a. Correcting errors in drawings (8% × 7,500) 600 hours

b. Correcting errors to conform to building code (7% × 7,500) 525 hours

Total 1 ,125 hours

4. Currently 85% × 7,500 hours = 6,375 hours are billed to clients generating revenues of

$701,250. The remaining 15% of professional labor-hours (15% × 7,500 = 1,125 hours) is lost in

Costs remain unchanged

Calvert’s operating income would be

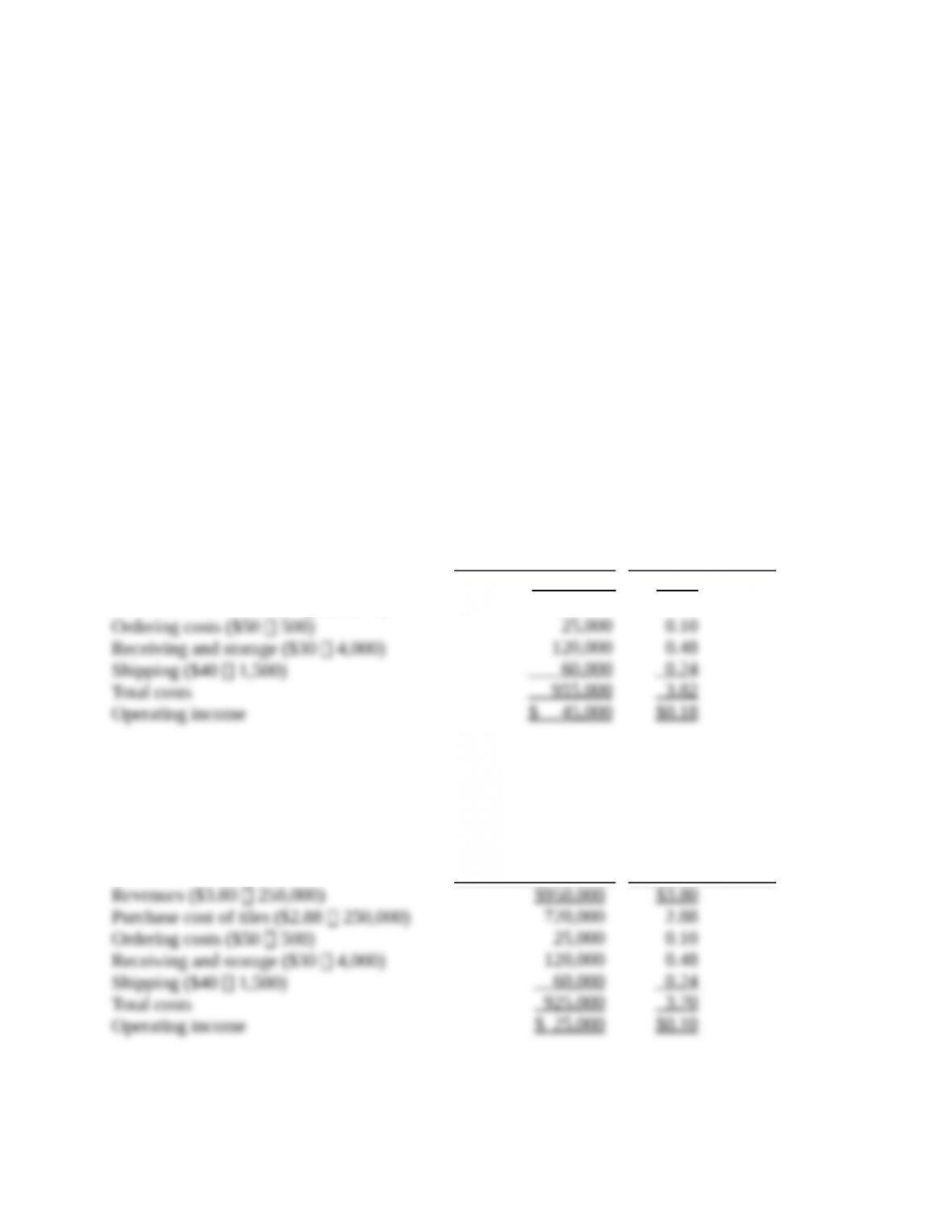

13-19 Target prices, target costs, activity-based costing. Snappy Tiles is a small distributor of

marble tiles. Snappy identifies its three major activities and cost pools as ordering, receiving and

storage, and shipping, and it reports the following details for 2016:

For 2016, Snappy buys 250,000 marble tiles at an average cost of $3 per tile and sells them to

retailers at an average price of $4 per tile. Assume Snappy has no fixed costs and no inventories.

Required:

13-8

1. Calculate Snappy’s operating income for 2016.

2. For 2017, retailers are demanding a 5% discount off the 2016 price. Snappy’s suppliers are

only willing to give a 4% discount. Snappy expects to sell the same quantity of marble tiles

in 2017 as in 2016. If all other costs and cost-driver information remain the same, calculate

Snappy’s operating income for 2017.

3. Suppose further that Snappy decides to make changes in its ordering and

receiving-and-storing practices. By placing long-run orders with its key suppliers, Snappy

expects to reduce the number of orders to 200 and the cost per order to $25 per order. By

redesigning the layout of the warehouse and reconfiguring the crates in which the marble

tiles are moved, Snappy expects to reduce the number of loads moved to 3,125 and the cost

per load moved to $28. Will Snappy achieve its target operating income of $0.30 per tile in

2017? Show your calculations.

SOLUTION

(25–30 min.) Target prices, target costs, activity-based costing.

1. Snappy’s operating income in 2016 is as follows:

Total for

250,000 Tiles

(1)

Per Unit

(2) = (1) ÷ 250,000

Revenues ($4 250,000)

Purchase cost of tiles ($3 250,000)

$1 ,000,000

750,000

$4.00

3.00

2. Price to retailers in 2017 is 95% of 2016 price = 0.95 $4 = $3.80; cost per tile in 2017

is 96% of 2016 cost = 0.96 $3 = $2.88.

Snappy’s operating income in 2017 is as follows:

Total for

250,000 Tiles

(1)

Per Unit

(2) = (1) ÷ 250,000

3. Snappy’s operating income in 2017, if it makes changes in ordering and material handling,

will be as follows:

13-9

Total for

250,000 Tiles

(1)

Per Unit

(2) = (1) ÷ 250,000

Through better cost management, Snappy will be able to achieve its target operating income of

$0.30 per tile despite the fact that its revenue per tile has decreased by $0.20 ($4.00 – $3.80),

while its purchase cost per tile has decreased by only $0.12 ($3.00 – $2.88).

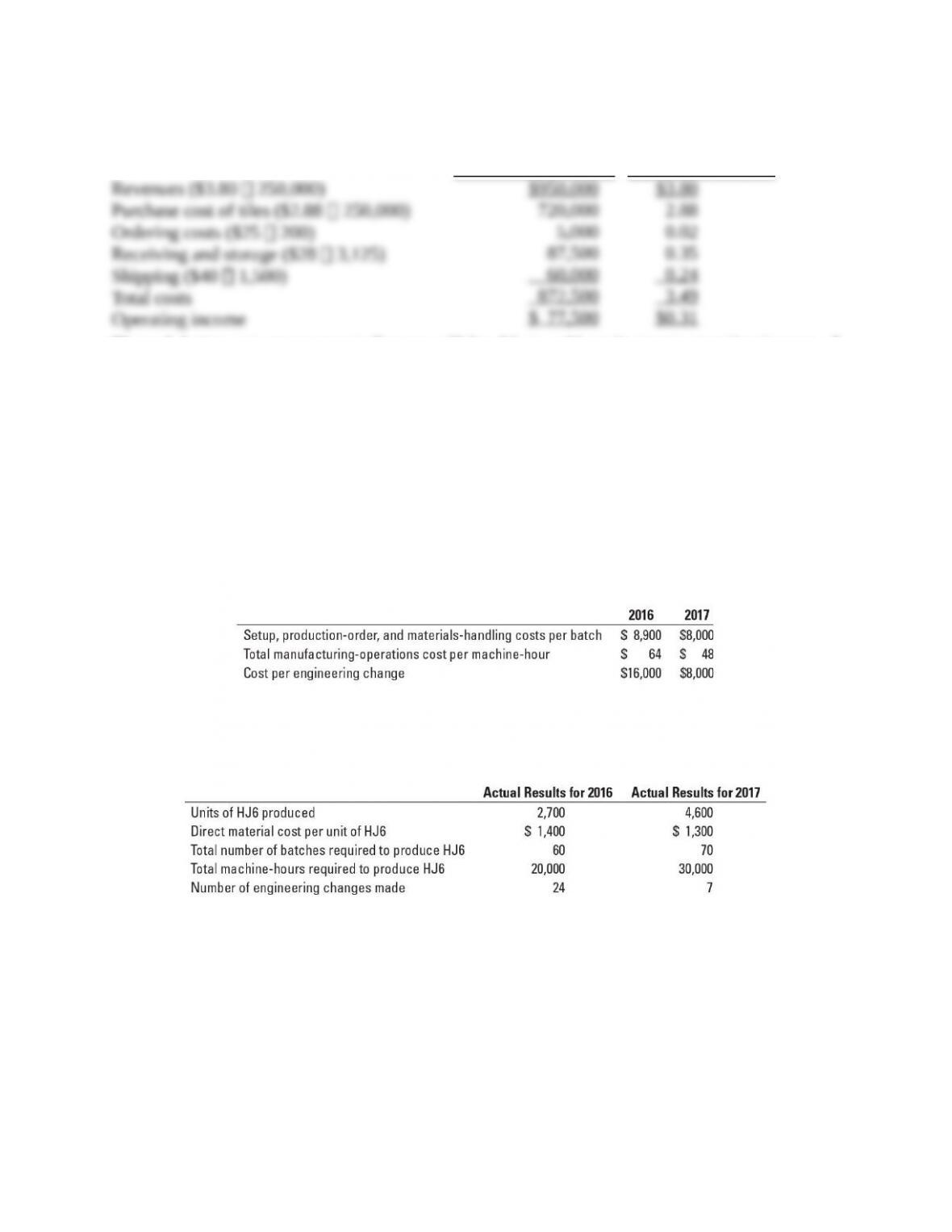

13-20 Target costs, effect of product-design changes on product costs. Neuro Instruments

uses a manufacturing costing system with one direct-cost category (direct materials) and three

indirect-cost categories:

a. Setup, production-order, and materials-handling costs that vary with the number of batches

b. Manufacturing-operations costs that vary with machine-hours

c. Costs of engineering changes that vary with the number of engineering changes made

In response to competitive pressures at the end of 2016, Neuro Instruments used

value-engineering techniques to reduce manufacturing costs. Actual information for 2016 and

2017 is as follows:

The management of Neuro Instruments wants to evaluate whether value engineering has

succeeded in reducing the target manufacturing cost per unit of one of its products, HJ6, by 5%.

Actual results for 2016 and 2017 for HJ6 are:

Required:

1. Calculate the manufacturing cost per unit of HJ6 in 2016.

2. Calculate the manufacturing cost per unit of HJ6 in 2017.

3. Did Neuro Instruments achieve the target manufacturing cost per unit for HJ6 in 2017?

Explain.

4. Explain how Neuro Instruments reduced the manufacturing cost per unit of HJ6 in 2017.

5. What challenges might managers at Neuro Instruments encounter in achieving the target

cost? How might they overcome these challenges?

13-10