SOLUTION

(25 min.) Dropping a customer, activity-based costing, ethics.

1. CRS would not benefit from dropping Donnelly’s Pizza because it would lose $43,680 in

revenues and save $43,344 in costs resulting in a $336 decrease in operating income.

Difference:

Incremental

(Loss in Revenues)

and Savings in Costs from

Dropping Donnelly’s Pizza

Revenues

Effect on operating income (loss)

$(43 ,680)

2. The drop in gross margin percentage indicates that Sara may be giving Donnelly’s Pizza

excessive discounts, perhaps in excess of company guidelines. If CRS awards bonuses based on

3. Justin could suggest that Sara approach Donnelly’s Pizza about reducing the number of

Justin should not rework the numbers. Referring to “Standards of Ethical Conduct for

Management Accountants,” in Exhibit 1-7, Justin Anders should consider the request of Sara

Brinkley to be unethical for the following reasons.

Competence

Integrity

11-?

Refrain from either actively or passively subverting the attainment of the organization’s

Communicate unfavorable as well as favorable information and professional judgments or

Refrain from engaging in or supporting any activity that would discredit the profession.

Credibility

Communicate information fairly and objectively. Justin needs to perform an objective

Disclose fully all relevant information that could reasonably be expected to influence an

Confidentiality

Not affected by this decision.

Justin should indicate to Sara that the costs he has derived are correct. If Sara still insists on

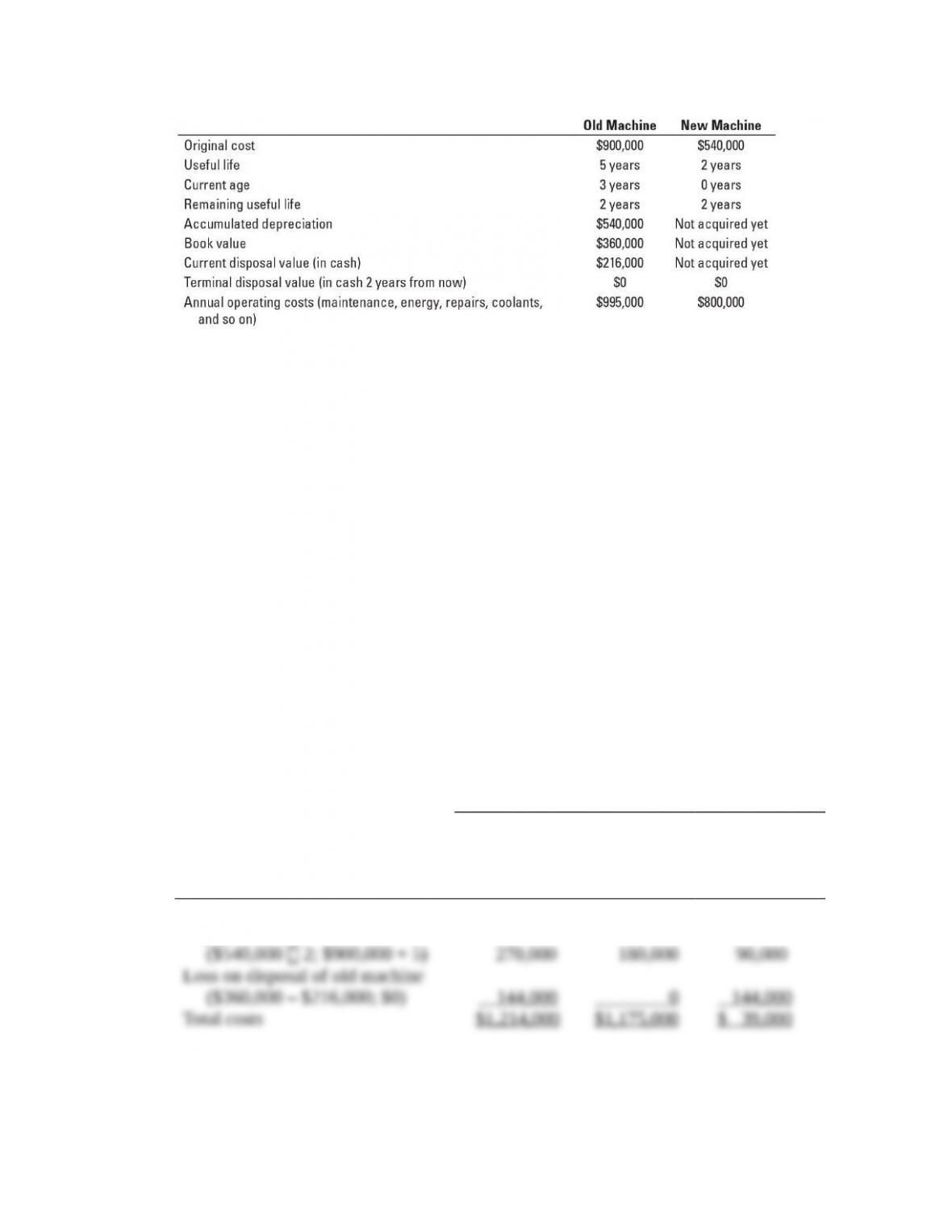

11-50 Equipment replacement decisions and performance evaluation. Susan Smith manages

the Wexford plant of Sanchez Manufacturing. A representative of Darnell Engineering

approaches Smith about replacing a large piece of manufacturing equipment that Sanchez uses in

its process with a more efficient model. While the representative made some compelling

arguments in favor of replacing the 3-year-old equipment, Smith is hesitant. Smith is hoping to

be promoted next year to manager of the larger Detroit plant, and she knows that the

accrual-basis net operating income of the Wexford plant will be evaluated closely as part of the

promotion decision. The following information is available concerning the

equipment-replacement decision:

11-?

Sanchez uses straight-line depreciation on all equipment. Annual depreciation expense for the

old machine is $180,000 and will be $270,000 on the new machine if it is acquired. For

simplicity, ignore income taxes and the time value of money.

Required:

1. Assume that Smith’s priority is to receive the promotion and she makes the

equipment-replacement decision based on the next one year’s accrual-based net operating

income. Which alternative would she choose? Show your calculations.

2. What are the relevant factors in the decision? Which alternative is in the best interest of the

company over the next 2 years? Show your calculations.

3. At what cost would Smith be willing to purchase the new equipment? Explain.

SOLUTION

(30 min.) Equipment replacement decisions and performance evaluation.

1. Operating income for the first year under the keep and replace alternatives are shown

below.

Year 1

Replace

With New

Machine

Keep Old

Machine

Cost

Difference

by Replacing

(1) (2) (3) = (1) – (2)

Cash operating costs $ 800,000 $ 995,000 $(195,000)

Depreciation

11-?

1. Based on the analysis in the table below, Sanchez Manufacturing will be better off by

$66,000 over two years if it replaces the current equipment.

Over 2 Years Cash Outflow

Comparing Relevant Costs of Replace Keep By Replacing

Replace and Keep Alternatives (1) (2) (3) = (1) – (2)

Cash operating costs $1,600,000 $1,990,000 $(390,000)

Note that the book value of the current machine ($360,000) would either be written off as

depreciation over two years under the keep option, or, all at once in the current year under the

replace option. Its net effect would be the same in both alternatives: to increase costs by

$360,000 over two years; hence, it is irrelevant in this analysis.

3. Smith would be willing to purchase the new equipment if the effect on operating income

in the first year would be zero or positive, that is, if the cost of operating the new equipment in

the first year were equal to or lower than the cost of operating the old machine.

11-?

Cash Outflow

by Replacing

Try It 11-1 Solution

The relevant revenues and costs are the expected future revenues and costs that differ as a result

of Rainier accepting the special offer:

The fixed landscaping costs and all marketing costs (including variable marketing costs) are

irrelevant in this case because these costs will not change in total whether the special order is

Try It 11-2 Solution

Rainier could use either the Total Alternatives Approach or the Opportunity-Cost Approach to

make a decision.

Total Alternatives Approach

The two options available to Rainier are

1. Do 8,000 hours of landscaping work for its current customers and 2,000 hours of work for

Victoria

2. Do 9,000 hours of landscaping work for its current customers

Current customers: 8,000 hours

Victoria: 2,000 hours Current customers: 9,000 hours

11-?

Relevant revenues

Relevant costs

Variable landscaping costs

The Opportunity Cost Approach

In the opportunity-cost approach, the options are defined as follows

1. Accept Victoria’s offer for 2,000 hours of landscaping work

2. Reject Victoria’s offer

The analysis focuses only on the Victoria offer.

We first calculate the opportunity cost of accepting Victoria’s offer.

There is no opportunity cost for the first 1,000 hours of equipment time since Rainier has 10,000

hours of equipment time and its current customers require only 9,000 hours.

For using the next 1,000 hours of equipment time on the Victoria offer, Rainier will have to forgo

contribution margin on the 1,000 hours of services it would have sold to its existing customers.

The opportunity cost of accepting Victoria’s offer is $26,000.

We next focus only on Victoria’s offer and the effect on operating income from accepting it.

Accept Victoria’s offer Reject Victoria’s offer

11-?

Incremental future costs

The opportunity cost approach yields the same conclusions as the total alternatives approach.

Rainier’s operating income decreases by $12,000 if it accepts Victoria’s offer. Note that by

considering only the incremental revenues and incremental costs, it would appear that Rainier

should accept Victoria’s offer because incremental revenues exceeds incremental costs of the

Try It 11-3 Solution

This problem is one of making product (or customer)-mix decisions with capacity constraints.

Rainier’s managers should choose the product with the highest contribution margin per unit of

the constraining resource (equipment hours). That’s the resource that restricts or limits the sale

of Rainier’s services.

Contribution margin from regular customers:

Revenues ($80 × 9,000 hours) $720 ,000

Variable landscaping costs (including materials and labor), which vary

Contribution margin per hour of equipment time from regular customers

11-?

Contribution margin from Hudson Corporation:

Variable landscaping costs (including materials and labor), which vary

Contribution margin per hour of equipment time from Hudson Corporation

To maximize operating income, Rainier should allocate as much of its capacity to customers who

generate the most contribution margin per unit of the constraining resource (equipment). That is,

Rainier should first allocate equipment capacity to existing customers ($26 per hour) and only

Try It 11-4 Solution

1. Irving should close down the Oakland store (see Exhibit Try It 11-4, Column 1). Closing

down the store results in a loss of revenues of $1,700,000 but cost savings of $1,720,000 (from

cost of goods sold, rent, labor, utilities, and corporate costs). Note that by closing down the

2. Exhibit Try It 11-4, Column 2, presents the relevant revenues and relevant costs of

opening another store like the Oakland store and shows that it increases Irving’s operating

income by $15,000. Incremental revenues of $1,700,000 exceed the incremental costs of

The key reason that Irving’s operating income increases either if it closes down the

Oakland store or if it opens another store like it is the behavior of corporate overhead costs. By

closing down the Oakland store, Irving can significantly reduce corporate overhead costs

presumably by reducing the corporate staff that oversees the Oakland operation. On the other

11-?

EXHIBIT TRY-IT 11-4

Relevant-Revenue and Relevant-Cost Analysis of Closing Oakland Store and Opening Another

Store Like It.

Incremental

(Loss in Revenues) Revenues and

and Savings in (Incremental Costs)

Costs from Closing of Opening New Store

Oakland Store Like Oakland Store

(1) (2)

Revenues $(1,700,000) $1,700,000

11-?