SOLUTION

(20-30 min.) CVP, alternative cost structures.

1. Variable cost per unit = $10

Contribution margin per unit = Selling price –Variable cost per unit

Fixed Costs:

2. Target number of sunglasses =

Fixed costs + Target operating income

Contribution margin per unit

=

$7,200 + $5,300 625 sunglasses

$20 =

3. Contribution margin per unit = Selling price – Variable cost per sunglass

Fixed costs = Manager’s salary + Rent = $3,000 + $1,000 = $4,000

SOLUTION

(30 min.) CVP analysis, income taxes, sensitivity.

1a.To breakeven, Thompson Engine Company must sell 1,112 units. This amount represents the

point where revenues equal total costs.

Let Q denote the quantity of engines sold.

Breakeven can also be calculated using contribution margin per unit.

1b. To achieve its net income objective, Thompson Engine Company must sell 1,412 units.

This amount represents the point where revenues equal total costs plus the corresponding

operating income objective to achieve net income of $900,000.

2. Alternative b will help Thompson Engine Company achieve its net income objective of

$900,000. Alternative b, where variable costs are reduced by $750 and selling price is reduced

by $800 resulting in 1,130 additional units being sold through the end of the year, yields the

highest net income of $920,100. Calculations for the three alternatives are shown below.

Alternative a

Alternative b

Alternative c

3-48 Choosing between compensation plans, operating leverage. (CMA, adapted)

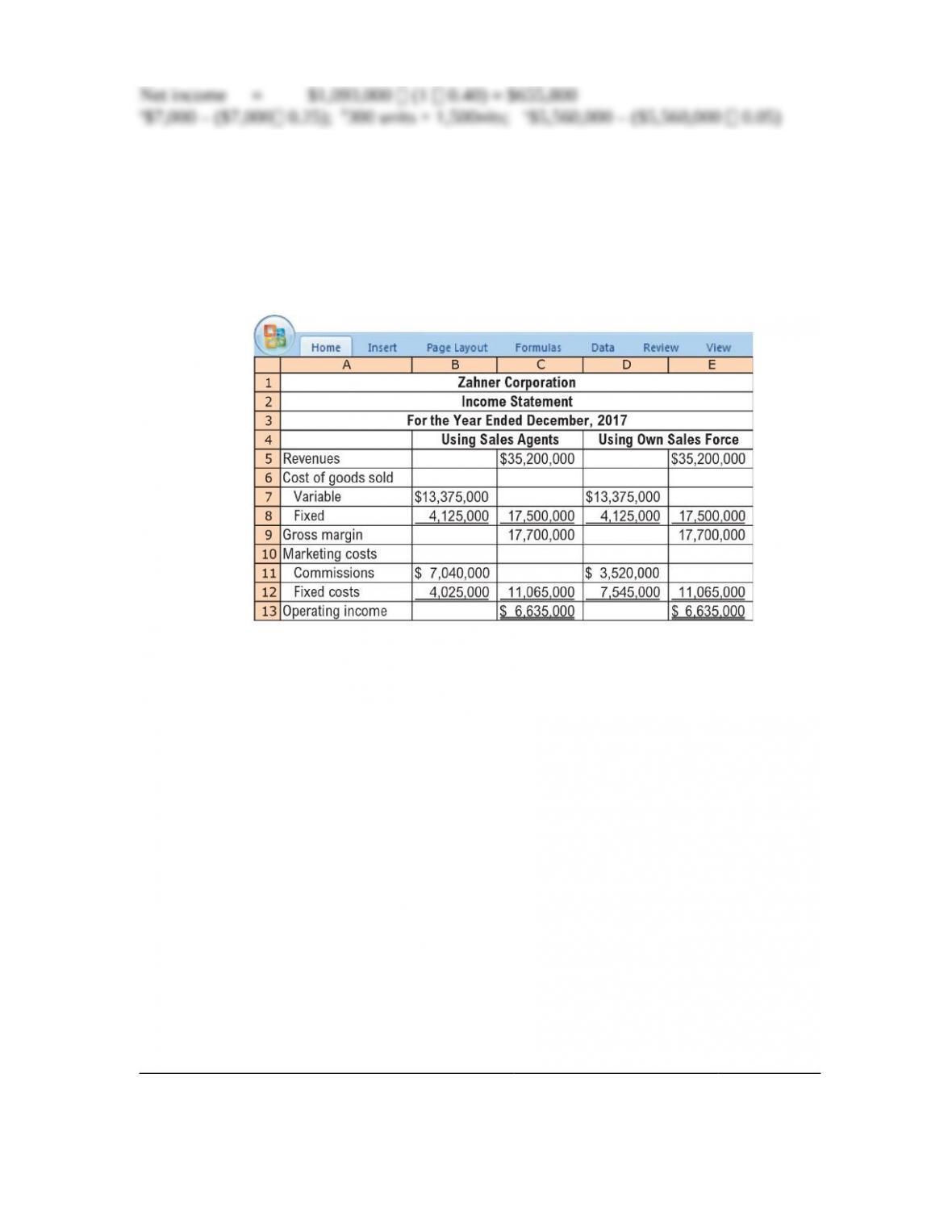

Zahner Corporation manufactures housewares products that are sold through a network of

external sales agents. The agents are paid a commission of 20% of revenues. Zahner is

considering replacing the sales agents with its own salespeople, who would be paid a

commission of 10% of revenues and total salaries of $3,520,000. The income statement for

the year ending December 31, 2017, under the two scenarios is shown here.

Required:

1. Calculate Zahner’s 2017 contribution margin percentage, breakeven revenue, and degree of

operating leverage under the two scenarios.

2. Describe the advantages and disadvantages of each type of sales alternative.

3. In 2018, Zahner uses its own salespeople, who demand a 15% commission. If all other

cost-behavior patterns are unchanged, how much revenue must the salespeople generate in

order to earn the same operating income as in 2017?

SOLUTION

(30 min.) Choosing between compensation plans, operating leverage.

1. We can recast Zahner Corporation’s income statement to emphasize contribution margin, and

then use it to compute the required CVP parameters.

Zahner Corporation

Income Statement for the Year Ended December 31, 2017

Using Sales Agents Using Own Sales Force

Revenues

$35,200,00

0 $35,200,000

Variable Costs

$13,375,00

$13,375,00

Contribution margin percentage

¸

¸

0.52)

19,404,762

42,308

Degree of operating leverage

¸

¸

2. The calculations indicate that at sales of $35,200,000, a percentage change in sales and

contribution margin will result in 2.23 times that percentage change in operating income if

Zahner continues to use sales agents and 2.76 times that percentage change in operating income

3. Variable costs of marketing = 15% of Revenues

3-49 Sales mix, three products. The Ronowski Company has three product lines of belts—A,

B, and C— with contribution margins of $3, $2, and $1, respectively. The president foresees

sales of 200,000 units in the coming period, consisting of 20,000 units of A, 100,000 units of B,

and 80,000 units of C. The company’s fixed costs for the period are $255,000.

Required:

1. What is the company’s breakeven point in units, assuming that the given sales mix is

maintained?

2. If the sales mix is maintained, what is the total contribution margin when 200,000 units are

sold? What is the operating income?

3. What would operating income be if 20,000 units of A, 80,000 units of B, and 100,000 units

of C were sold? What is the new breakeven point in units if these relationships persist in the

next period?

SOLUTION

(15–25 min.) Sales mix, three products.

1. Sales of A, B, and C are in ratio 20,000 : 100,000 : 80,000. So for every 1 unit of A, 5

(100,000 ÷ 20,000) units of B are sold, and 4 (80,000 ÷ 20,000) units of C are sold.

$255,000

$17

Breakeven point in units is:

Total number of units to breakeven 150,000 units

Alternatively,

Contribution margin – Fixed costs = Zero operating income

2. Contribution margin:

A: 20,000 $3

3. Contribution margin

A: 20,000 $3 $ 60,000

Sales of A, B, and C are in ratio 20,000 : 80,000 : 100,000. So for every 1 unit of A, 4

(80,000 ÷ 20,000) units of B and 5 (100,000 ÷ 20,000) units of C are sold.

Contribution margin – Fixed costs = Breakeven point

Breakeven point increases because the new mix contains less of the higher contribution

margin per unit, product B, and more of the lower contribution margin per unit, product C.

3-50 Multiproduct CVP and decision making. Crystal Clear Products produces two types of

water filters. One attaches to the faucet and cleans all water that passes through the faucet. The

other is a pitcher-cum-filter that only purifies water meant for drinking.

The unit that attaches to the faucet is sold for $90 and has variable costs of $25.

The pitcher-cum-filter sells for $110 and has variable costs of $20.

Crystal Clear sells two faucet models for every three pitchers sold. Fixed costs equal $1,200,000.

Required:

1. What is the breakeven point in unit sales and dollars for each type of filter at the current sales

mix?

2. Crystal Clear is considering buying new production equipment. The new equipment will

increase fixed cost by $208,000 per year and will decrease the variable cost of the faucet and

the pitcher units by $5 and $10, respectively. Assuming the same sales mix, how many of each

type of filter does Crystal Clear need to sell to break even?

3. Assuming the same sales mix, at what total sales level would Crystal Clear be indifferent

between using the old equipment and buying the new production equipment? If total sales are

expected to be 24,000 units, should Crystal Clear buy the new production equipment?

SOLUTION

(40 min.) Multi-product CVP and decision making.

1. Faucet filter:

Selling price $90

Each bundle contains two faucet models and three pitcher models.

Each bundle contains two faucet models and three pitcher models.

Operating income using new equipment = $440

x

– $1,200,000 – $208,000

At point of indifference:

x

x

x

Let x be the number of bundles,

When total sales are less than 26,000 units (5,200 bundles), $400 $1,200,000 >x–

$440 $1,408,000, x–

so Crystal Clear Products is better off with the old equipment.

When total sales are greater than 26,000 units (5,200 bundles), $440 $1,408,000 > x–

$400 $1,200,000,x–

so Crystal Clear Products is better off buying the new

equipment.

Check

3-51 Sales mix, two products. The Stackpole Company retails two products: a standard and a

deluxe version of a luggage carrier. The budgeted income statement for next period is as follows:

Required:

1. Compute the breakeven point in units, assuming that the company achieves its planned sales

mix.

2. Compute the breakeven point in units (a) if only standard carriers are sold and (b) if only

deluxe carriers are sold.

3. Suppose 250,000 units are sold but only 50,000 of them are deluxe. Compute the operating

income. Compute the breakeven point in units. Compare your answer with the answer to

requirement 1. What is the major lesson of this problem?

SOLUTION

(20–25 min.) Sales mix, two products.

1. Sales of standard and deluxe carriers are in the ratio of 187,500 : 62,500. So for every 1

unit of deluxe, 3 (187,500 ÷ 62,500) units of standard are sold.

2a. Unit contribution margins are: Standard: $28 – $18 = $10; Deluxe: $50 – $30 = $20

2b. If only Deluxe carriers were sold, the breakeven point would be:

3. Operating income = Contribution margin of Standard + Contribution margin of Deluxe – Fixed costs

Sales of standard and deluxe carriers are in the ratio of 200,000 : 50,000. So for every 1

dinner. Tickets for the dinner were $24 per attendee. The profit report for last year’s dinner

follows.

This year the dinner committee does not want to lose money on the dinner. To help achieve its

Required:

1. Prepare last year’s profit report using the contribution margin format.

2. The committee is considering expanding this year’s dinner invitation list to include volunteer

members (in addition to contributing members). If the committee expands the dinner

invitation list, it expects attendance to double. Calculate the effect this will have on the

profitability of the dinner assuming fixed costs will be the same as last year.