SOLUTION

(25 min.) Cost allocation, downward demand spiral.

SOLUTION EXHIBIT 9-45

2017

Master

Budget

(1)

Practical

Capacity

(2)

2018

Master

Budget

(3)

Budgeted fixed cost per meal

Budgeted fixed costs

¸

Denominator level

¸

1. The 2017 budgeted fixed costs are $1,533,000. Mealman budgets for 1,050,000 meals in

2017, and this is used as the denominator level to calculate the fixed cost per meal. $1,533,000

¸

2. In 2018, 3 hospitals have dropped out of the purchasing group and the master budget is

912,500 meals. If this is used as the denominator level, fixed cost per meal = $1,533,000

¸

912,500 = $1.68 per meal, and the total budgeted cost per meal would be $6.38 (see column (3)

3. The basic problem is that Mealman has excess capacity and associated excess fixed costs.

If Wright uses the practical capacity of 1,460,000 meals as the denominator level, the fixed cost

per meal will be $1.05 (see column (2) in Solution Exhibit 9-45), and the total budgeted cost per

9-46 Cost allocation, responsibility accounting, ethics (continuation

of Problem 9-45). In 2018, only 876,000 Mealman meals were produced and sold to the

hospitals. Wright suspects that hospital controllers had systematically inflated their 2018 meal

estimates.

Required:

1. Recall that Mealman uses the master-budget capacity utilization to allocate fixed costs and to

price meals. What was the effect of production-volume variance on Mealman’s operating

income in 2018?

2. Why might hospital controllers deliberately overestimate their future meal counts?

3. What other evidence should Meals To Go’s president seek to investigate Wright’s concerns?

4. Suggest two specific steps that Wright might take to reduce hospital controllers’ incentives to

inflate their estimated meal counts.

SOLUTION

(20 min.) Cost allocation, responsibility accounting, ethics (continuation of 9-45).

1. (See Solution Exhibit 9-45). If Mealman uses the rate based on its master budget capacity

utilization to allocate fixed costs in 2018, it would allocate 876,000

´

$1.68 = $1,471,680.

Budgeted fixed costs are $1,533,000. Therefore, the production volume variance = $1,533,000 –

$1,471,680 = $61,320 U. An unfavorable production volume variance will reduce operating

income by this amount. (Note: in this business, there are no inventories. All variances are

written off to cost of goods sold).

2. Hospitals are charged a budgeted variable cost rate and allocated budgeted fixed costs.

By overestimating budgeted meal counts, the denominator-level is larger, hence the amount

charged to individual hospitals is lower. Consider 2018 where the budgeted fixed cost rate is

computed as follows:

If in fact, the hospital administrators had better estimated and revealed their true demand (say,

876,000 meals), the allocated fixed cost per meal would have been

3. Evidence that could be collected include:

(a) Budgeted meal-count estimates and actual meal-count figures each year for each

hospital controller. Over an extended time period, there should be a sizable number of both

underestimates and overestimates. Controllers could be ranked on both their percentage of

overestimation and the frequency of their overestimation.

(b) Look at the underlying demand estimates by patients at individual hospitals. Each

hospital controller has other factors (such as hiring of nurses) that give insight into their

4. (a) Highlight the importance of a corporate culture of honesty and openness. Wright

could institute a Code of Ethics that highlights the upside of individual hospitals providing

honest estimates of demand (and the penalties for those who do not).

(b) Have individual hospitals contract in advance for their budgeted meal count. Unused

9-47 Absorption, variable, and throughput costing. Tesla Motors

assembles the fully electric Model S-85 automobile at its Fremont, California, plant. The

standard variable manufacturing cost per vehicle in 2017 is $58,800, which consists of:

Direct materials $36,000

Direct manufacturing labor $10,800

Variable manufacturing overhead $12,000

Variable manufacturing overhead is allocated to vehicles on the basis of assembly time. The

standard assembly time per vehicle is 20 hours.

The Fremont plant is highly automated and has a practical capacity of 4,000 vehicles per

month. The budgeted monthly fixed manufacturing overhead is $45 million. Fixed manufacturing

overhead is allocated on the basis of the standard assembly time for the budgeted normal capacity

utilization of the plant. For 2017, the budgeted normal capacity utilization is 3,000 vehicles per

month.

Tesla started production of the Model S-85 in 2017. The actual production and sales figures for

the first three months of the year are:

January February March

Production 3,200 2,400 3,800

Sales 2,000 2,900 3,200

Franz Holzhausen is SVP of Tesla and director of the Fremont plant. His compensation

includes a bonus that is 0.25% of monthly operating income, calculated using absorption costing.

Tesla prepares absorption-costing income statements monthly, which include an adjustment for the

production-volume variance occurring in that month. There are no variable cost variances or fixed

overhead spending variances in the first three months of 2017.

The Fremont plant is credited with revenue (net of marketing costs) of $96,000 for the sale of

each Tesla S-85 vehicle.

Required:

1. Compute (a) the fixed manufacturing cost per unit and (b) the total manufacturing cost per

unit.

2. Compute the monthly operating income for January, February, and March under absorption

costing. What amount of bonus is paid each month to Franz Holzhausen?

3. How much would the use of variable costing change Holzhausen’s bonus each month if the

same 0.25% figure were applied to variable-costing operating income?

4. Explain the differences in Holzhausen’s bonuses in requirements 2 and 3.

5. How much would the use of throughput costing change Holzhausen’s bonus each month if

the same 0.25% figure were applied to throughput-costing operating income?

6. What are the different approaches Tesla Motors could take to reduce possible undesirable

behavior associated with the use of absorption costing at its Fremont plant?

SOLUTION

(60 min.) Absorption, variable, and throughput costing.

1.

(a)

Fixed manufacturing

overhead cost per unit

=

$45,000,000

3,000 vehicles 20 standard hours´

=

$45,000,000

60,000

= $750 per standard assembly hour or $15,000

per vehicle

(b) Direct materials per unit $ 36,000

Direct manufacturing labor per unit 10,800

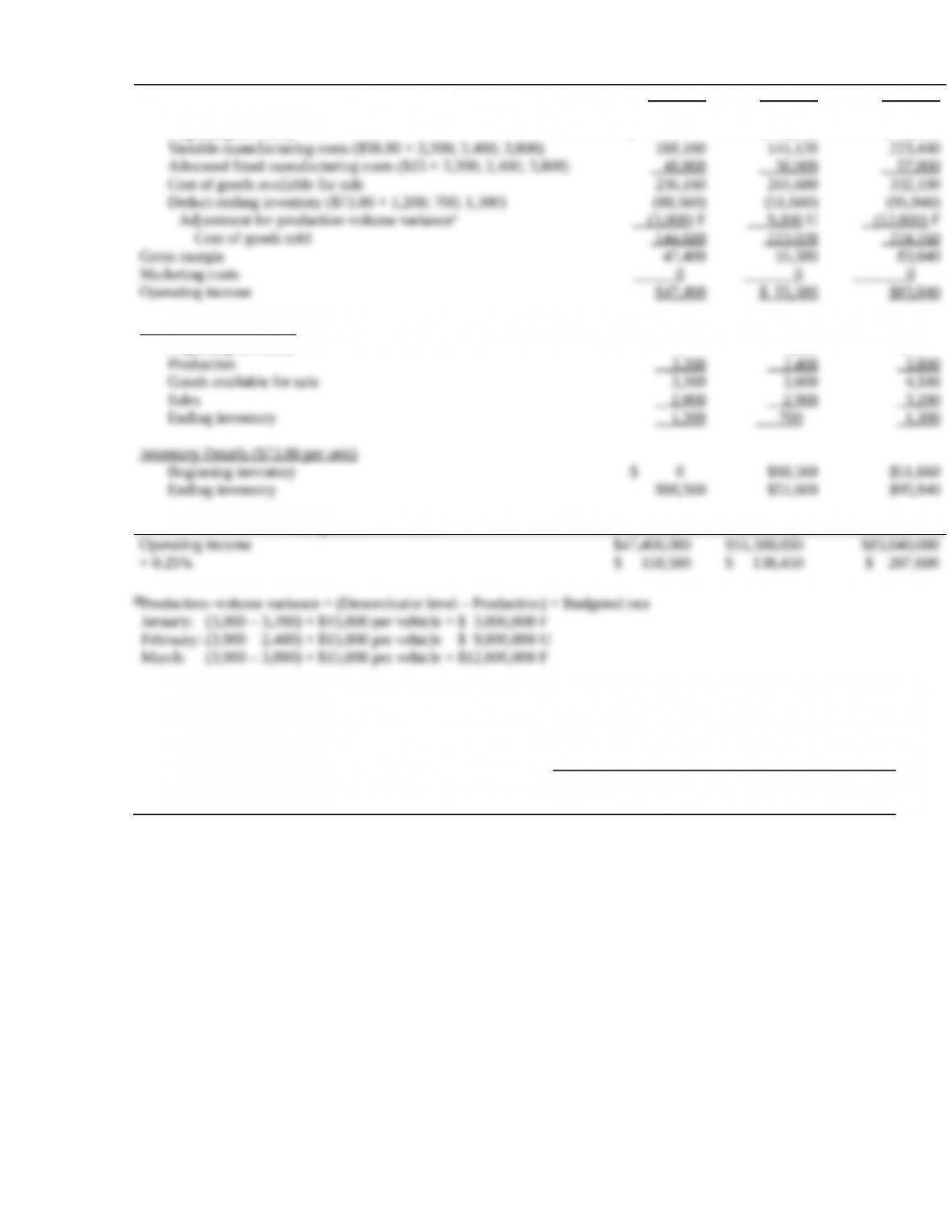

2. Amounts in thousands.

Absorption Costing

January February March

Revenues ($96,000 × 2,000; 2,900; 3,200)

Cost of goods sold

Beginning inventory

Inventory Details (Units)

Beginning inventory

$192 ,000

$ 0

0

$278 ,400

$ 88,560

1,200

$307 ,200

$ 51,660

700

Computation of Bonus January February March

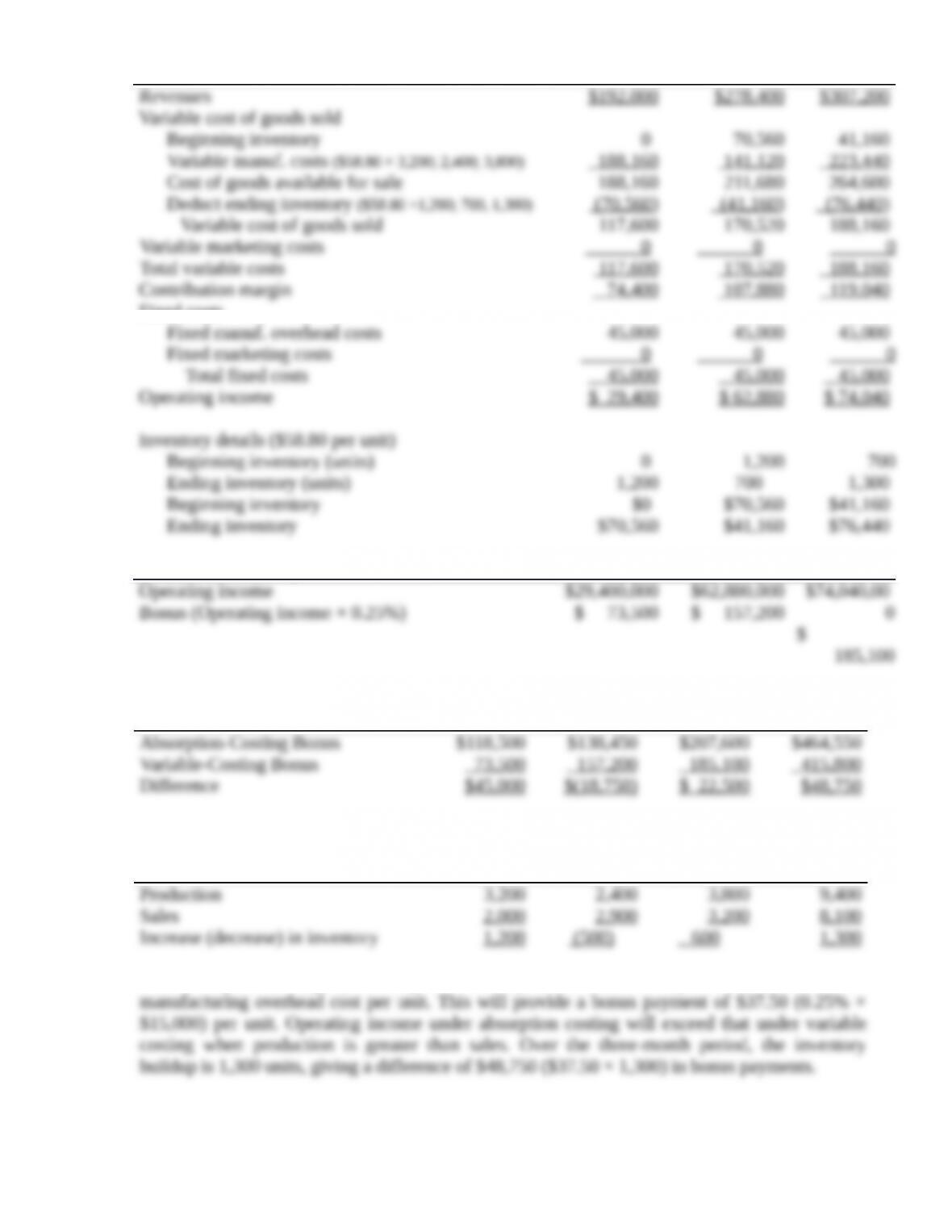

3. Amounts in thousands.

Variable Costing

January February March

Variable cost of goods sold

Beginning inventory

0

70,560

41,160

Computation of Bonus January February March

4.

January February March Total

The difference between absorption and variable costing arises because of differences in

production and sales:

January February March Total

With absorption costing, by building for inventory, Holzhausen can capitalize $15,000 of fixed

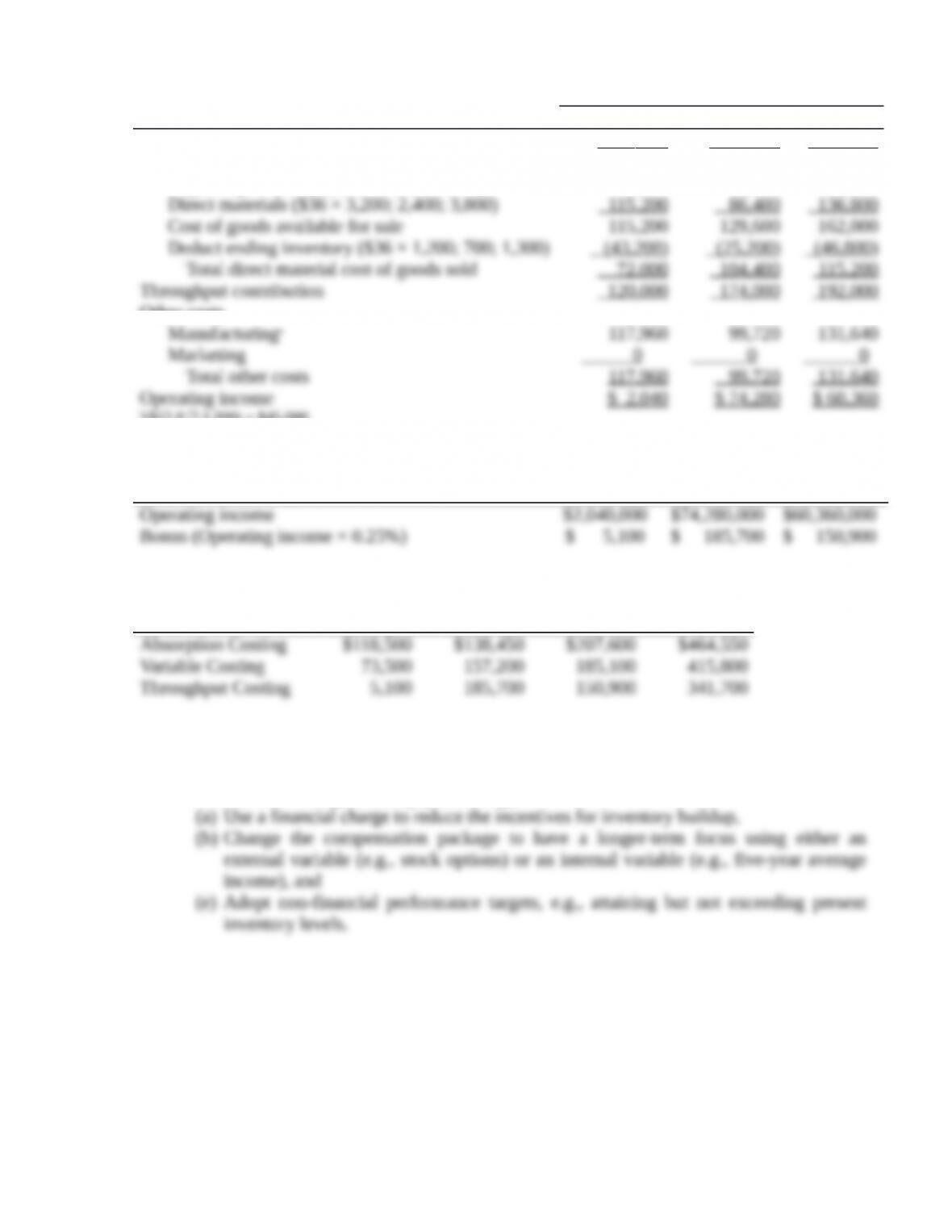

5. Amounts in thousands

Throughput Costing

January February March

Revenues

Direct material cost of goods sold

Beginning inventory ($36 × 0; 1,200; 700)

Other costs

Manufacturinga

$192 ,000

0

117,960

$278 ,400

43,200

99,720

$307 ,200

25,200

131,640

Marketing

0

0

0

a($22.8 3,200) + $45,000

($22.8 2,400) + $45,000

($22.8 3,800) + $45,000

Computation of Bonus January February March

A summary of the bonuses paid is:

January February March Total

6. Alternative approaches include:

(a) Careful budgeting and inventory planning,

(b) Use an alternative income computation approach to absorption costing (such as

variable costing or throughput costing),

9-48 Costing methods and variances, comprehensive. Rob Kapito, the

controller of Blackstar Paint Supply Company, has been exploring a variety of internal

accounting systems. Rob hopes to get the input of Blackstar’s board of directors in choosing one.

To prepare for his presentation to the board, Rob applies four different cost accounting methods

to the firm’s operating data for 2017. The four methods are actual absorption costing, normal

absorption costing, standard absorption costing, and standard variable costing.

With the help of a junior accountant, Rob prepares the following alternative income statements:

A B C D

Sales Revenue $

90

0,

00

0

$

9

0

0

,

0

0

0

$

90

0,

00

0

$

90

0,0

00

Cost of Goods Sold $

37

5,

00

0

$

2

5

0

,

0

0

0

$

42

0,

00

0

$

39

5,0

00

(+) Variances:

Direct Materials 15,000 15,000 — —

Direct Labor 5,000 5,000 — —

Manufacturing

Overhead

25,000 — — 25,000

(+) (All Fixed) 350,0

00

475,0

0

0

350,00

0

350,00

0

Total Costs $

77

0,

00

0

$

7

4

5,

0

0

0

$

77

0,

00

0

$

77

0,0

00

Net Income $

13

0,

$

1

5

$

13

0,

$

13

0,0

A B C D

00

0

5,

0

0

0

00

0

00

Where applicable, Rob allocates both fixed and variable manufacturing overhead using direct

labor hours as the driver. Blackstar carries no work-in-process inventory. Standard costs have been

stable over time, and Rob writes off all variances to cost of goods sold. For 2017, there was no

flexible budget variance for fixed overhead. In addition, the direct labor variance represents a price

variance.

Required:

1. Match each method below with the appropriate income statement (A, B, C, or D):

Actual Absorption costing

Normal Absorption costing

Standard Absorption costing

Standard Variable costing

2. During 2017, how did Blackstar’s level of finished-goods inventory change? In other words,

is it possible to know whether Blackstar’s finished-goods inventory increased, decreased, or

stayed constant during the year?

3. From the four income statements, can you determine how the actual volume of production

during the year compared to the denominator (expected) volume level?

4. Did Blackstar have a favorable or unfavorable variable overhead spending variance during

2017?

SOLUTION

(30 min.) Costing methods and variances, comprehensive.

1. Actual Absorption costing – C

2. The net income under standard variable costing (B; $155,000) exceeds that under

standard absorption costing (A; $130,000). Since there are no work-in-process inventories, this

3. From statement B, the aggregate variance for variable overhead is zero. So, the $25,000

variance for total overhead in A must all be for fixed overhead. We are told that there is no

4. The aggregate variable overhead variance of zero is the sum of the spending and

efficiency variances. Note that variable overhead is applied using direct labor hours as the

Try It! 9-1

(a) Under variable costing, all variable manufacturing costs are inventoriable costs. This

includes direct materials, direct manufacturing labor, and variable overhead. Therefore,

the inventoriable cost per unit under variable costing is $20 + $4 + $1 = $25.

(b) Absorption costing considers all variable manufacturing costs and all fixed

manufacturing costs as inventoriable costs. Therefore, the inventoriable cost per unit

Try It! 9-2

(a) Variable costing

Revenues: 24,000 × $50 $1,200,000

(b) Absorption costing

Revenues: 24,000 × $50 $1,200,000

Operating income $ 260,200

Absorption costing treats fixed manufacturing cost as a product cost, while variable costing treats

it as a period cost. ZB Toys has 6,000 units in ending inventory. Under absorption costing, these

Try It! 9-3

(a) Absorption costing: $87.50 + $50.00 + $62.50 = $200

Try It! 9-4

(a) Theoretical capacity: 1,000 × 3 × 8 × 30 = 720,000 units