SOLUTION

(20 min.) Plantwide, department, and ABC indirect cost rates.

1.

Actual plantwide variable MOH rate

based on machine hours, $280,000

¸

5,000 $56 per machine hour

Southern

Motors

Caesar

Motors

Jupiter

Auto Total

Variable manufacturing overhead, allocated based on machine hours

($56

´

300; $56

´

3,700; $56

´

1,000)

$56,00

2.

Departme

nt

MOH in

2017

Total

Driver Units Rate

Design $ 35,000 500 $70 per CAD-design hour

Production 25,000 500 $50 per engineering hour

Engineerin

g

220,000 5,000 $44

per machine hour

Souther

n

Motors

Caesar

Motors

Jupite

r Auto Total

Design-related overhead, allocated on

CAD-design hours

(150

´

$70; 250

´

$70; 100

´

$70)

$

$

$

Production-related overhead, allocated on

engineering hours

(130

´

$50; 100

´

$50; 270

´

$50)

Engineering-related overhead, allocated on

machine hours

´

´

´

13,200

0

0

0

5-1

3.

Southern

Motors

Caesar

Motors

Jupiter

Auto

a. Department rates

The manufacturing overhead allocated to Southern Motors increases by 80% under the

department rates, the overhead allocated to Caesar decreases by about 11%, and the overhead

The percentage of total driver units in each department used by the companies is:

Department

Cost

Driver

Southern

Motors

Caesar

Motors

Jupiter

Auto

Design

Engineering

Production

CAD-design hours

Engineering hours

Machine hours

30%

26

6

50%

20

74

20%

54

20

The Southern Motors contract uses only 6% of total machines hours in 2017, yet uses

30% of CAD design-hours and 26% of engineering hours. The result is that the plantwide rate,

In contrast, the Caesar Motors contract uses less of design (50%) and engineering (20%)

Caesar Motors was probably complaining under the use of the simple system because its

contract was being overcosted relative to its consumption of MOH resources. Southern and

Jupiter, on the other hand, were having their contracts undercosted and underpriced by the simple

4. Other than for pricing, RC can also use the information from the department-based

system to examine and streamline its own operations so that there is maximum value-added from

all indirect resources. It might set targets over time to reduce both the consumption of each

5-2

5. It would not be worthwhile to further refine the cost system into an ABC system if (1) a

single activity accounts for a sizable proportion of the department’s costs or (2) significant costs

¸

overhead.

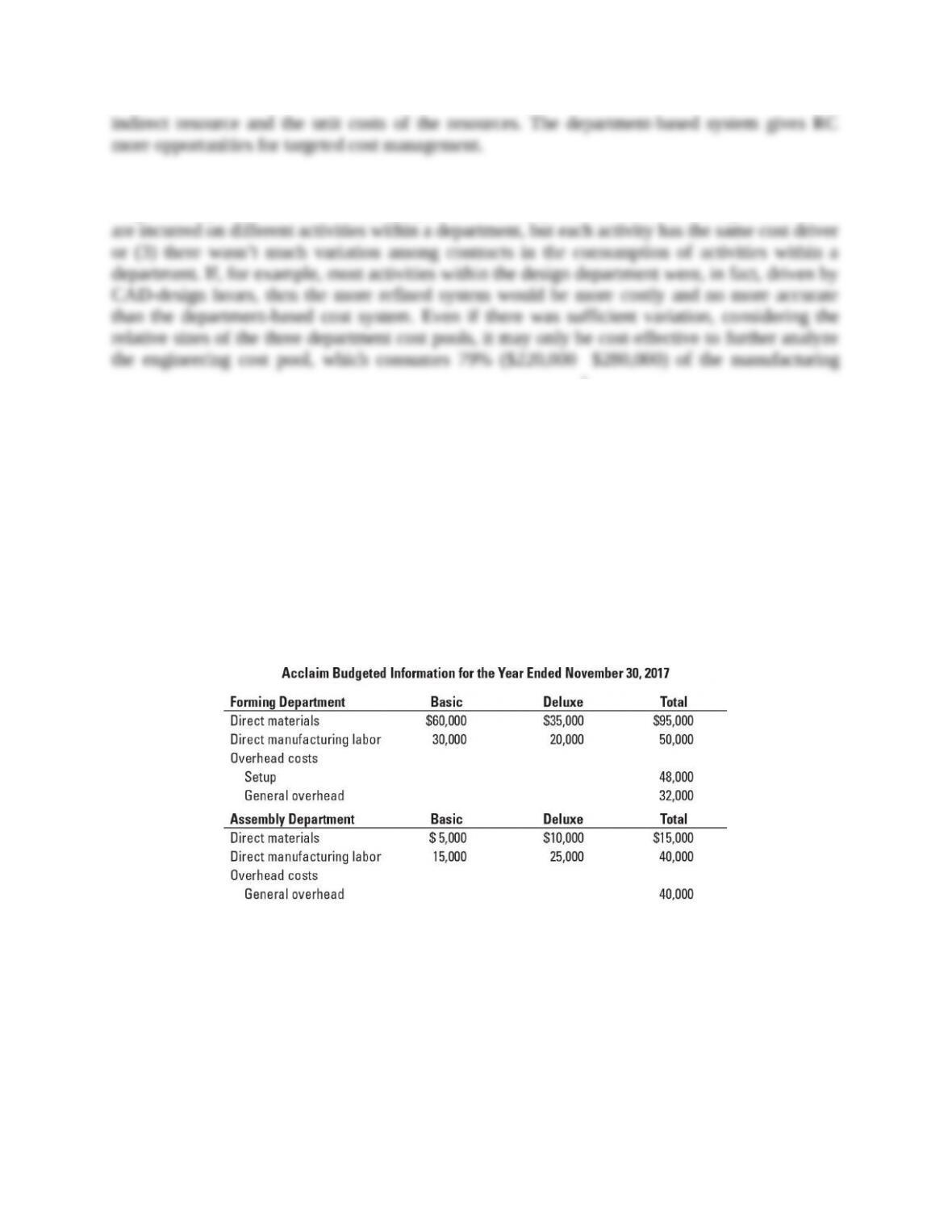

5-22 Plant-wide, department, and activity-cost rates. Acclaim Inc. makes two styles of

trophies, basic and deluxe, and operates at capacity. Acclaim does large custom orders. Acclaim

budgets to produce 10,000 basic trophies and 5,000 deluxe trophies. Manufacturing takes place

in two production departments: forming and assembly. In the forming department, indirect

manufacturing costs are accumulated in two cost pools, setup and general overhead. In the

assembly department, all indirect manufacturing costs are accumulated in one general overhead

cost pool. The basic trophies are formed in batches of 200 but because of the more intricate detail

of the deluxe trophies, they are formed in batches of 50.

The controller has asked you to compare plant-wide, department, and activity-based cost

allocation.

Required

1. Calculate the budgeted unit cost of basic and deluxe trophies based on a single plant-wide

overhead rate, if total overhead is allocated based on total direct costs. (Don’t forget to

include direct material and direct manufacturing labor cost in your unit cost calculation.)

2. Calculate the budgeted unit cost of basic and deluxe trophies based on departmental overhead

rates, where forming department overhead costs are allocated based on direct manufacturing

labor costs of the forming department and assembly department overhead costs are allocated

based on total direct manufacturing labor costs of the assembly department.

5-3

3. Calculate the budgeted unit cost of basic and deluxe trophies if Acclaim allocates overhead

costs in each department using activity-based costing, where setup costs are allocated based

on number of batches and general overhead costs for each department are allocated based on

direct manufacturing labor costs of each department.

4. Explain briefly why plant-wide, department, and activity-based costing systems show

different costs for the basic and deluxe trophies. Which system would you recommend and

why?

SOLUTION

(50 min.) Plantwide, department, and activity-cost rates.

1.

Basic Deluxe Total

Direct materials

Forming $ 60,000 $35,000

Direct manufacturing labor

Forming 30,000 20,000

Budgeted

overhead rate

=

($48, 000 $32,000 $40,000) $120,000

$200,000 $200,000

+ + =

=

$0.60 per dollar of direct cost

Basic Deluxe Total

Direct materials $ 65,000 $ 45,000 $110,000

5-4

2.

Budgeted

overhead rate

Forming Dept.

—

=

Budgeted Forming Department overhead costs

Budgeted Forming Department direct manufacturing labor costs

=

$48,000 $32,000

$30,000 $20,000

+

+

=

$80,000

$50,000 =

$1.60 per Forming Department direct manuf.-labor dollar

Budgeted

overhead rate

Assembly Dept.

—

=

Budgeted Assembly Department overhead costs

Budgeted Assembly Department direct manufacturing labor costs

=

$40,000

($15, 000 $25, 000)+

=

$40,000

$40,000 =

$1 per Assembly Department direct manuf.-labor dollar

Basic Deluxe Total

Direct materials $ 65,000 $ 45,000 $110,000

Direct manufacturing labor 45 ,000 45 ,000 90 ,000

Allocated overhead

3.

Number of batches of basic trophies = 10,000 ÷ 200 trophies per batch = 50 batches

Forming Department

Budgeted setup rate

=

$48,000

150 batches

= $320 per batch

5-5

Budgeted general oerhead rate

=

$32,000

$50,000

= $0.64 per direct manuf.-labor dollar

Assembly Department

Budgeted general overhead rate

=

$40,000

$40,000

= $1 per direct manuf.-labor dollar

Basic Deluxe Total

Direct material costs $ 65,000 $ 45,000 $110,000

Direct labor costs 45 ,000 45 ,000 90 ,000

Forming Dept. overhead

Set up

General overhead

$0.64

´

$30,000; $20,000

Assembly Department overhead

General overhead

$1

´

$15,000; $25,000

15 ,000 25 ,000 40 ,000

4. As Triumph uses more refined cost pools, the costs of basic trophies decreases, and costs of

deluxe trophies increases. This is because deluxe trophies use a higher proportion of cost drivers

Department costing systems increase the costs of deluxe trophies relative to basic

trophies because the forming and assembly department costs are allocated based on direct

I would recommend that Acclaim use the activity-based costing system because

disaggregated information can improve decisions by allowing managers to see the details that

5-6

pricing and product-mix decisions, cost reduction and process-improvement decisions, design

decisions, and to plan and manage activities. However, too much detail can overload managers

5-23 ABC, process costing. Sander Company produces mathematical and financial calculators

and operates at capacity. Data related to the two products are presented here:

Total manufacturing overhead costs are as follows:

Required

1. Choose a cost driver for each overhead cost pool and calculate the manufacturing overhead

cost per unit for each product.

2. Compute the manufacturing cost per unit for each product.

3. How might Sander’s managers use the new cost information from its activity-based costing

system to better manage its business?

SOLUTION

(10–15 min.) ABC, process costing.

1. Rates per unit cost driver.

Activity Cost Driver Rate

Machining Machine-hours $360,000 ÷ (30,000 + 60,000)

= $4 per machine hour

Manufacturing overhead cost per unit:

5-7

Mathematical Financial

Machining: $4 × 30,000; 60,000 $120,000 $240,000

Set up: $1,200 × 45; $1,200 × 45 54,000 54,000

2.

Mathematical Financial

Manufacturing cost per unit:

Direct materials

Direct manufacturing labor

3. Disaggregated information can improve decisions by allowing managers to see the details

that help them understand how different aspects of cost influence total cost per unit. Managers

5-24 Department costing, service company. DLN is an architectural firm that designs and

builds buildings. It prices each job on a cost plus 20% basis. Overhead costs in 2017 are

$8,100,000. DLN’s simple costing system allocates overhead costs to its jobs based on number

of jobs. There were three jobs in 2017. One customer, Chandler, has complained that the cost and

price of its building in Chicago was not competitive.

As a result, the controller has initiated a detailed review of the overhead allocation to determine

if overhead costs should be charged to jobs in proportion to consumption of overhead resources

by jobs. She gathers the following information:

Required

5-8

1. Compute the overhead allocated to each project in 2017 using the simple costing system that

allocates overhead costs to jobs based on the number of jobs.

2. Compute the overhead allocated to each project in 2017 using department overhead cost

rates.

3. Do you think Chandler had a valid reason for dissatisfaction with the cost and price of its

building? How does the allocation based on department rates change costs for each project?

4. What value, if any, would DLN get by allocating costs of each department based on the

activities done in that department?

SOLUTION

(20 mins.) Department costing, service company

1. Using the simple costing system, total overhead costs are equally allocated to projects.

There were 3 projects in 2017, so the overhead cost per project is

Overhead cost

per project in 2017

$8,100,000

3

=

2. Rates per unit cost driver.

Activity Cost Driver Rate

Design Design department hours $3,000,000 ÷ (2,000 + 10,000 + 8,000)

Overhead cost allocated to each project using department overhead cost rates:

Chandler Henry Manley

Design: $150 × 2,000; 10,000; 8,000 $ 300,000 $1,500,000 $1,200,000

3.

Chandler Henry Manley

5-9

a. Department rates

The overhead allocated to Chandler decreases by 23% under the department rates, the overhead

allocated to Henry increases by about 17%, and the overhead allocated to Manley increases by

The percentage of total driver units in each department used by the companies is:

Department

Cost

Driver Chandler Henry Manley

Design

Engineering

Construction

Design-hours

Engineering-hours

Labor-hours

10%

32

35

50%

32

33

40%

36

32

The Chandler project uses only 10% of design-hours in 2017 and uses 32% of

In contrast, the Henry and Manley projects use more of design (50% and 40%,

Chandler was probably complaining about the costs resulting from using the simple

4. It would not be worthwhile to further refine the cost system into an ABC system if (1) a

single activity accounts for a sizable proportion of the department’s costs or (2) significant costs

5-10

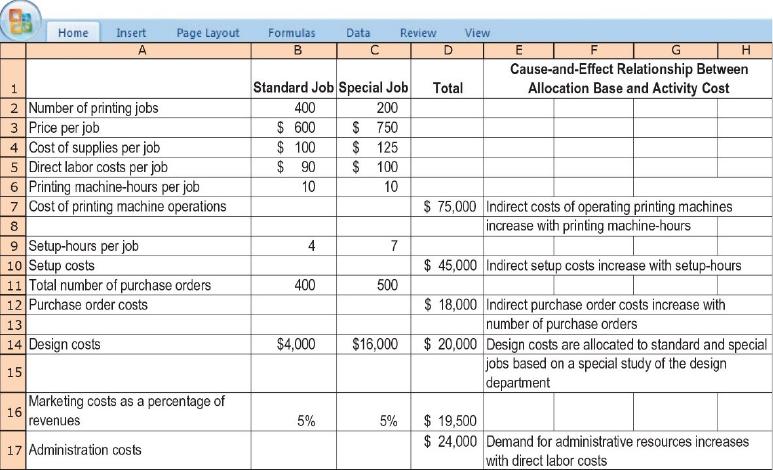

5-25 Activity-based costing, service company. Speediprint Corporation owns a small printing

press that prints leaflets, brochures, and advertising materials. Speediprint classifies its various

printing jobs as standard jobs or special jobs. Speediprint’s simple job-costing system has two

direct-cost categories (direct materials and direct labor) and a single indirect-cost pool.

Speediprint operates at capacity and allocates all indirect costs using printing machine-hours as

the allocation base.

Speediprint is concerned about the accuracy of the costs assigned to standard and special

jobs and therefore is planning to implement an activity-based costing system. Speediprint’s

ABC system would have the same direct-cost categories as its simple costing system. However,

instead of a single indirect-cost pool there would now be six categories for assigning indirect

costs: design, purchasing, setup, printing machine operations, marketing, and administration. To

see how activity-based costing would affect the costs of standard and special jobs, Speediprint

collects the following information for the fiscal year 2017 that just ended.

Required

1. Calculate the cost of a standard job and a special job under the simple costing system.

2. Calculate the cost of a standard job and a special job under the activity-based costing system.

3. Compare the costs of a standard job and a special job in requirements 1 and 2. Why do the

simple and activity-based costing systems differ in the cost of a standard job and a special

job?

4. How might Speediprint use the new cost information from its activity-based costing system

to better manage its business?

5-11