CHAPTER 9

INVENTORY COSTING AND CAPACITY ANALYSIS

9-1 Differences in operating income between variable costing and absorption costing are due

solely to accounting for fixed costs. Do you agree? Explain.

9-2 Why is the term direct costing a misnomer?

The term direct costing is a misnomer for variable costing for two reasons:

9-3 Do companies in either the service sector or the merchandising sector make choices about

absorption costing versus variable costing?

9-4 Explain the main conceptual issue under variable costing and absorption costing

regarding the timing for the release of fixed manufacturing overhead as expense.

Variable costing uses (a) and absorption costing uses (b).

9-5 “Companies that make no variable-cost/fixed-cost distinctions must use absorption

costing, and those that do make variable-cost/fixed-cost distinctions must use variable costing.”

Do you agree? Explain.

9-6 The main trouble with variable costing is that it ignores the increasing importance of

fixed costs in manufacturing companies. Do you agree? Why?

9-7 Give an example of how, under absorption costing, operating income could fall even

though the unit sales level rises.

9-8 What are the factors that affect the breakeven point under (a) variable costing and (b)

absorption costing?

(a) The factors that affect the breakeven point under variable costing are:

(b) The factors that affect the breakeven point under absorption costing are:

9-9 Critics of absorption costing have increasingly emphasized its potential for leading to

undesirable incentives for managers. Give an example.

9-10 What are two ways of reducing the negative aspects associated with using absorption

costing to evaluate the performance of a plant manager?

Approaches used to reduce the negative aspects associated with using absorption costing include:

a. Change the accounting system:

inventory.

b. Extend the time period used to evaluate performance. By evaluating performance

9-11 What denominator-level capacity concepts emphasize the output a plant can supply?

What denominator-level capacity concepts emphasize the output customers demand for products

produced by a plant?

9-12 Describe the downward demand spiral and its implications for pricing decisions.

9-13 Will the financial statements of a company always differ when different choices at the

start of the accounting period are made regarding the denominator-level capacity concept?

9-14 What is the IRS’s requirement for tax reporting regarding the choice of a

denominator-level capacity concept?

For tax reporting in the U.S., the IRS requires only that indirect production costs are “fairly”

apportioned among all items produced. Overhead rates based on normal or master-budget

9-15 “The difference between practical capacity and master-budget capacity utilization is the

best measure of management’s ability to balance the costs of having too much capacity and

having too little capacity.” Do you agree? Explain.

9-16 In comparing the absorption and variable cost methods, each of the following statements is

true except:

a. SG&A fixed expenses are not included in inventory in either method.

b. Only the absorption method may be used for external financial reporting.

c. Variable costing charges fixed overhead costs to the period they are incurred.

d. When inventory increases over the period, variable net income will exceed absorption net

income.

SOLUTION

Choice “d” is correct. Inventory under the absorption method includes fixed overhead costs,

while the variable cost method includes fixed overhead costs as period costs. Fixed overhead

9-17 Queen Sales, Inc. has just completed its first year of operations. The company has not had

any sales to date. Queen has incurred the following costs associated with its production as of

December 31, Year 1:

Direct materials $45,000

Production labor 35,000

Bookkeeper salary 28,000

Factory utilities 18,500

Office rent 12,000

Factory supervisor salary 9,600

Machine maintenance contract 7,500

Under absorption costing, what is the inventory amount shown on the balance sheet at December

31, Year 1?

a. $155,600

b. $115,600

c. $98,500

d. $80,000

SOLUTION

Choice “b” is correct. Absorption costing, which is required under U.S. GAAP, requires all

product costs to be included in inventory. No segregation is made between fixed and variable

costs, and the costs are expensed when the product is sold. All of the costs listed, except for the

bookkeeper salary and the office rent, are product costs.

9-18 King Tooling has produced and sold the following number of units of their only product

during their first two years in business:

Produced Sold

Year ended December 31, Year 1 50,000 40,000

Production costs per unit have not changed over the two-year period. Under variable costing,

what is the amount of cost of sales relative to the cost of sales shown on the GAAP income

statement of the company?

Year 1 Year 2

a. Higher Higher

b. Higher Lower

c. Lower Higher

d. Lower Lower

SOLUTION

Choice “b” is correct. When more units are produced in a period than sold, a portion of the fixed

Choice “a” is incorrect. The cost of sales under variable costing is less than the cost of sales

Choice “c” is incorrect. If units produced in any period exceed the units sold during that period,

Choice “d” is incorrect. The cost of sales under variable costing is more than the cost of sales

9-19 The following information relates to Drexler Inc.’s Year 3 financials:

Direct labor $420,000

Direct materials 210,000

Variable overhead 205,000

Fixed overhead 355,000

Variable SG&A expenses 150,000

Fixed SG&A expenses 195,000

Year 3 period costs for Drexler, under both the absorption and variable cost methods, will be

Absorption Cost Method Variable Cost Method

a. $345,000 $700,000

Absorption Cost Method Variable Cost Method

b. $345,000 $905,000

c. $550,000 $700,000

d. $550,000 $905,000

SOLUTION

Choice “a” is correct. Under the absorption method, only variable and fixed SG&A expenses are

Choice “b” is incorrect. This answer choice incorrectly adds variable overhead as a period cost

Choice “c” is incorrect. This answer choice incorrectly adds variable overhead as a period cost

Choice “d” is incorrect. This answer choice incorrectly adds variable overhead as a period cost

9-20 Which of the following statements is not true regarding the use of variable and absorption

costing for performance measurement?

a. The net income reported under the absorption method is less reliable for use in performance

evaluations because the cost of the product includes fixed costs, which means the level of

inventory affects net income.

b. The net income reported under the contribution income statement is more reliable for use in

performance evaluations because the product cost does not include fixed costs.

c. Variable costing isolates contribution margins to aid in decision making.

d. The Internal Revenue Service allows either absorption or variable costing as long as the

method is not changed from year to year, while U.S. GAAP only allows absorption costing.

SOLUTION

The answer is choice “d”. This is not a true statement. The I.R.S. only allows absorption costing

Choice “a” is again a true statement. Under absorption costing, the choice of output and

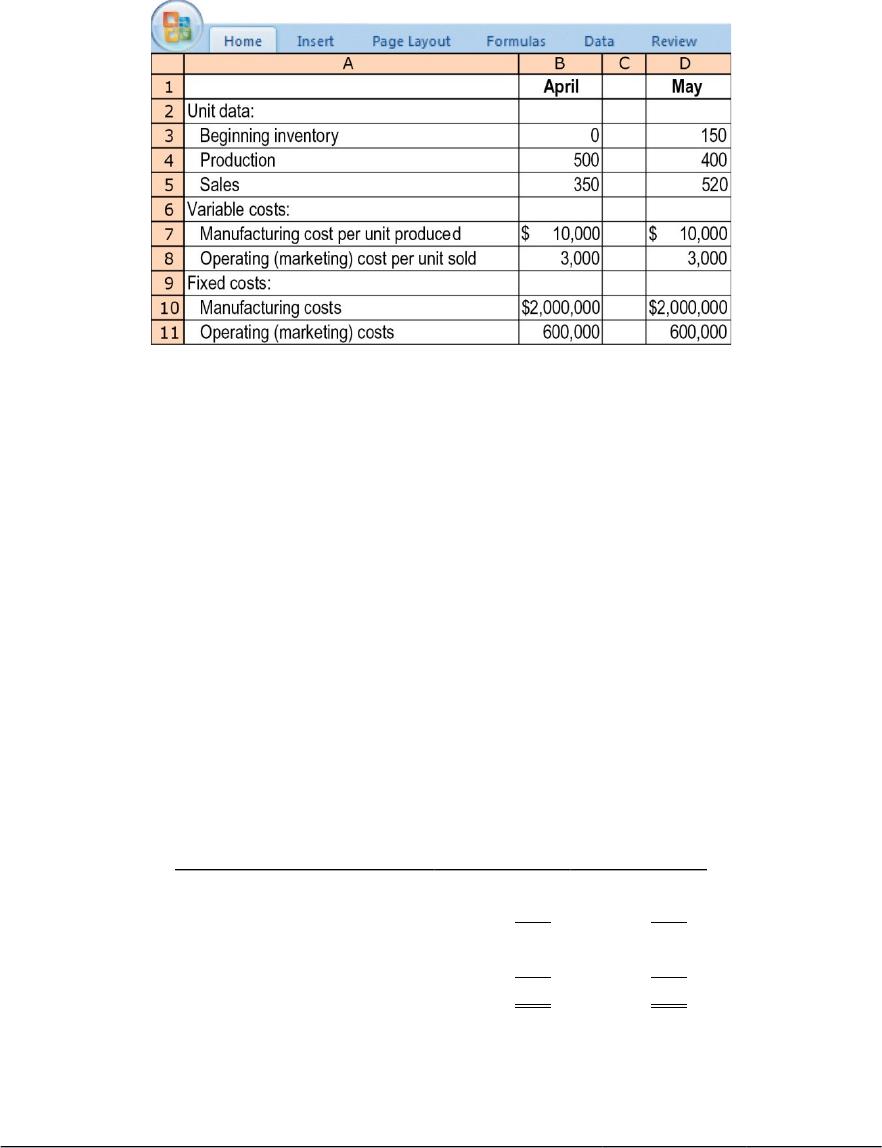

9-21 Variable and absorption costing, explaining operating-income differences. Nascar

Motors assembles and sells motor vehicles and uses standard costing. Actual data relating to

April and May 2017 are as follows:

The selling price per vehicle is $24,000. The budgeted level of production used to calculate the

budgeted fixed manufacturing cost per unit is 500 units. There are no price, efficiency, or

spending variances. Any production-volume variance is written off to cost of goods sold in the

month in which it occurs.

Required:

1. Prepare April and May 2017 income statements for Nascar Motors under (a) variable costing

and (b) absorption costing.

2. Prepare a numerical reconciliation and explanation of the difference between operating

income for each month under variable costing and absorption costing.

SOLUTION

(30 min.) Variable and absorption costing, explaining operating-income differences.

1. Key inputs for income statement computations are

April May

Beginning inventory

Production

Goods available for sale

Units sold

Ending inventory

0

500

500

350

150

150

400

550

520

30

The budgeted fixed cost per unit and budgeted total manufacturing cost per unit under absorption

costing are

April May

(a) Budgeted fixed manufacturing costs

$2,000,000

$2,000,000

(a) Variable costing

April 2017 May 2017

Revenuesa $8,400,000 $12,480,000

Variable costs

(b) Absorption costing

April 2017 May 2017

Revenuesa$8,400,000 $12,480,000

Cost of goods sold

Beginning inventory $ 0 $2,100,000

Cost of goods sold 4 ,900,000 7 ,680,000

Operating costs

Variable operating costsf1,050,000 1,560,000

Total operating costs 1 ,650,000 2 ,160,000

2.

Absorption-costing

operating income

–

Variable-costing

operating income

=

Fixed manufacturing costs

in ending inventory

–

Fixed manufacturing costs

in beginning inventory

April:

The difference between absorption and variable costing is due solely to moving fixed

manufacturing costs into inventories as inventories increase (as in April) and out of inventories

as they decrease (as in May).

9-22 Throughput costing (continuation of 9-21). The variable manufacturing costs per unit

of Nascar Motors are as follows:

Required:

1. Prepare income statements for Nascar Motors in April and May 2017 under throughput

costing.

2. Contrast the results in requirement 1 with those in requirement 1 of Exercise 9-21.

3. Give one motivation for Nascar Motors to adopt throughput costing.