A local accounting firm employs 24 full-time professionals. The budgeted annual

compensation per employee is $45,000. The average chargeable time is 420 hours per

client annually. All professional labor costs are included in a single direct-cost category

and are allocated to jobs on a per-hour basis.

Other costs are included in a single indirect-cost pool, allocated according to

professional labor-hours. Budgeted indirect costs for the year are $790,000, and the

firm expects to have 90 clients during the coming year.

What is the budgeted direct labor cost rate per hour? (Round the final answer to the

nearest cent.)

A) $28.57 per hour

B) $20.90 per hour

C) $4.46 per hour

D) $107.14 per hour

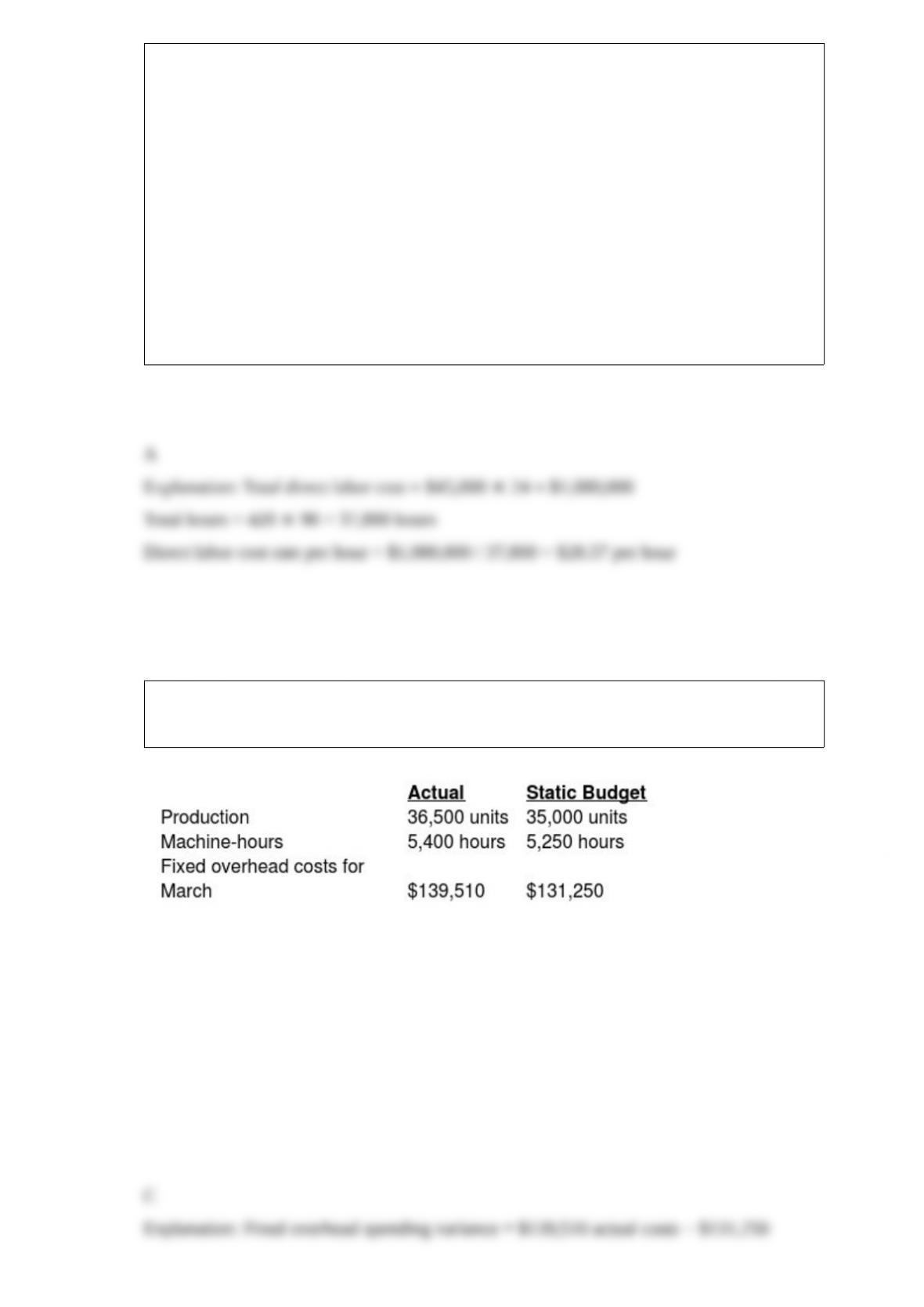

Castleton Corporation manufactured 36,500 units during March. The following fixed

overhead data relates to March:

What is the fixed overhead spending variance?

A) $2,635.00 unfavorable

B) $8,260.00 favorable

C) $8,260.00 unfavorable

D) $2,635.00 favorable

Cool Air Inc., manufactures single room sized air conditioners. The cost accounting

system estimates manufacturing costs to be $230 per air conditioner, consisting of 60%

variable costs and 40% fixed costs. The company has surplus capacity available. It is

Cool Air Inc.’s policy to add a 30% markup to full costs.

Cool Air Inc., is invited to bid on a one-time-only special order to supply 110 air

conditioners. What is the lowest price Cool Air Inc. should bid on this special order?

A) $15,180

B) $25,300

C) $35,420

D) $32,890

Using master-budget capacity to allocate budgeted fixed manufacturing costs can result

in a

A) stable measure; avoiding the recalculation of unit costs when expected demand

levels change

B) fixed costs spread over available capacity

C) can result in a downward demand spiral

D) in fixed overhead costs calculated based on capacity available

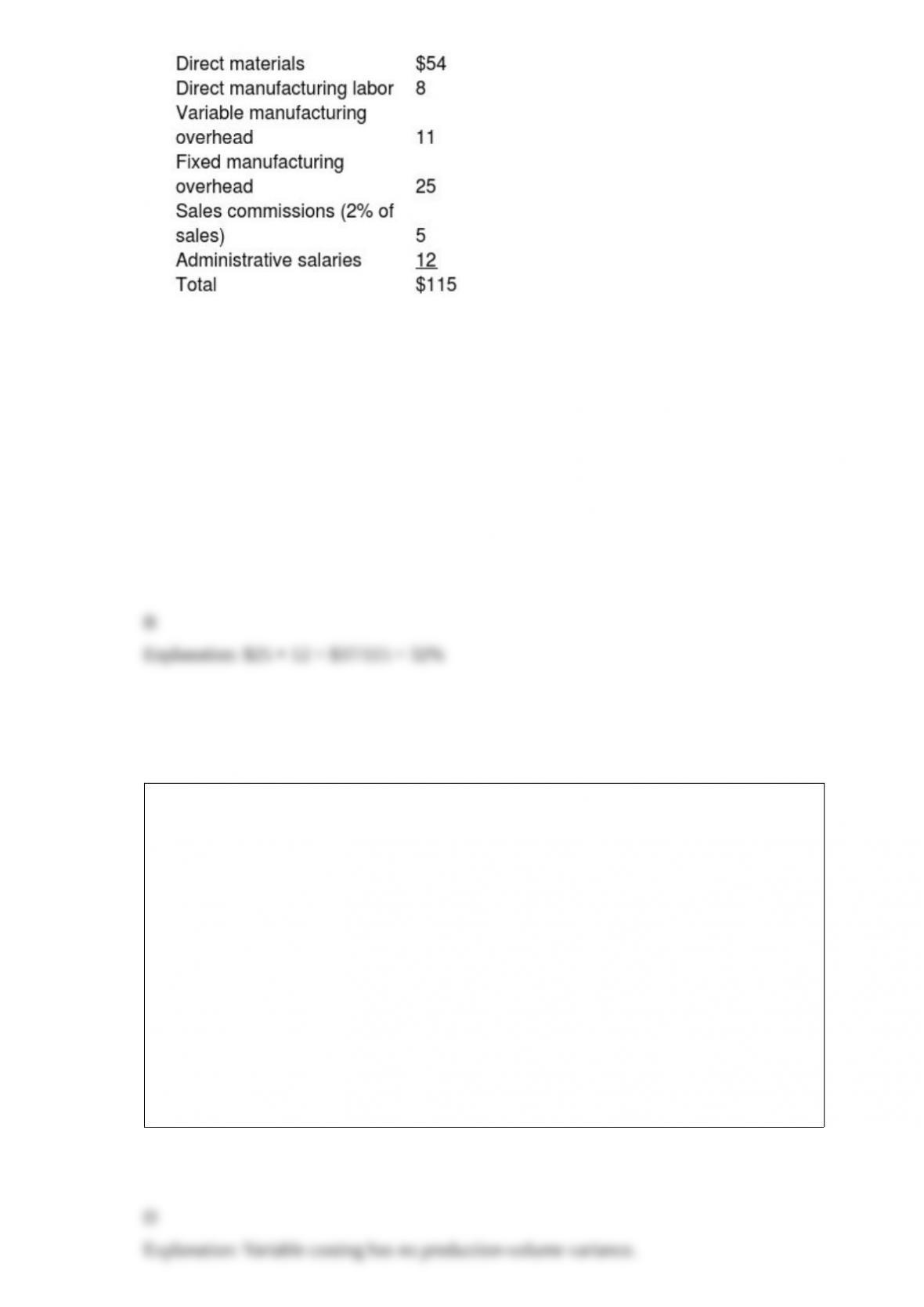

The East Company manufactures several different products. Unit costs associated with

Product ORD105 are as follows:

What is the percentage of the total fixed costs per unit associated with Product ORD105

with respect to total cost?

A) 37%

B) 32%

C) 15%

D) 26%

Venus Corporation incurred fixed manufacturing costs of $6,600 during 2017. Other

information for 2017 includes:

The budgeted denominator level is 1,600 units.

Units produced total 770 units.

Units sold total 600 units.

Beginning inventory was zero.

The company uses variable costing and the fixed manufacturing cost rate is based on

the budgeted denominator level. Manufacturing variances are closed to cost of goods

sold.

The production-volume variance totals ________.

A) $1,457

B) $701

C) $3,424

D) 0

Benny Industries allocates manufacturing overhead at a predetermined rate of 160% of

direct labor cost. Any overallocated or underallocated overhead is closed to the cost of

goods sold at the end of the month. Below is information on job 205 that was in process

at the end of the month of October

Direct materials $4,000

Direct labor $3,000

Allocated manufacturing overhead $4,800

Jobs 206, 207, and 208 were started in November. Direct materials that were used in

November were $26,000 and direct labor costs were $21,000. For the month of

November, actual manufacturing overhead was $32,000. The only job still in process on

the last day of November was job 104 with the following costs: $3,000 for direct

materials and $1,500 for direct labor.

Required:

a. Calculate the cost of goods manufacturered for November.

b. Calculate the amount of overallocated or underallocated manufacturing overhead that

should be closed to cost of goods sold on November 30. Be sure to label the answer as

either overallocated or underallocated.

c. What are the accounting entries to close the overallocated or underallocated

manufacturing overhead on November 30?

Which of the following types of costs are incurred in precluding the production of

products that do not conform to specifications?

A) prevention costs

B) appraisal costs

C) internal failure costs

D) external failure costs

H.J. Manufacturing produces 10,000 units of a part that is used in their assembly

process. The production costs are as follows:

Direct materials $ 50,000

Direct manufacturing labor 20,000

Variable support costs 35,000

Fixed support costs 25,000

Total costs $130,000

H.J. Manufacturing has the option of purchasing these units from an outside supplier at

$10.75 per unit. If the part is outsourced, 40% of the fixed costs cannot be immediately

converted to other uses.

a. Describe avoidable costs. What amount of the part’s production costs is avoidable?

b. Should H.J. outsource the part? Why or why not?

c. What other items should H.J. consider before outsourcing any of the parts it currently

manufactures?

Which of the following best describes a belief control system?

A) it describes standards of behavior and codes of conduct expected of all executives

and board of directors

B) it articulates the mission, purpose, and core values of a company

C) they are formal information systems managers use to focus the company’s attention

and learning on key strategic issues

D) it describes standards of behavior and codes of conduct expected of all employees

Which of the following is true of cost accounting?

A) It is a subset of management accounting and therefore its information is used only to

meet the needs of managers.

B) It is used only by manufacturers.

C) It is part of both management and financial accounting systems.

D) The distinction between management accounting and cost accounting is clear-cut.

Axelia Corporation has two divisions, Refining and Extraction. The company’s primary

product is Luboil Oil. Each division’s costs are provided below:

Extraction: Variable costs per barrel of oil $16

Fixed costs per barrel of oil $9

Refining: Variable costs per barrel of oil $26

Fixed costs per barrel of oil $38

The Refining Division has been operating at a capacity of 40,900 barrels a day and

usually purchases 25,600 barrels of oil from the Extraction Division and 15,400 barrels

from other suppliers at $64 per barrel.

Assume 260 barrels are transferred from the Extraction Division to the Refining

Division for a transfer price of $26 per barrel. The Refining Division sells the 260

barrels at a price of $220 each to customers. What is the operating income of both

divisions together?

A) $13,520

B) $34,060

C) $16,380

D) $50,440

Home Plate Corporation manufactures baseball uniforms and uses budgeted

machine-hours to allocate variable manufacturing overhead. The following information

pertains to the company’s manufacturing overhead data:

What is the budgeted variable overhead cost rate per output unit?

A) $6.26

B) $6.00

C) $17.00

D) $18.00

For companies in which full allocation is not followed, which of the following is true of

corporate sustaining costs?

A) allocated to divisions using cause-and-effect relationship

B) allocated to customers using cause-and-effect relationship

C) added to aggregate operating incomes of the divisions

D) subtracted as a lump-sum amount after aggregating operating incomes of the

divisions

Using ________ as the denominator level also gives the manager a more accurate idea

of the resources needed and used to produce a unit by excluding the cost of unused

capacity.

A) practical capacity

B) normal capacity utilization

C) theoretical capacity

D) master-budget capacity utilization

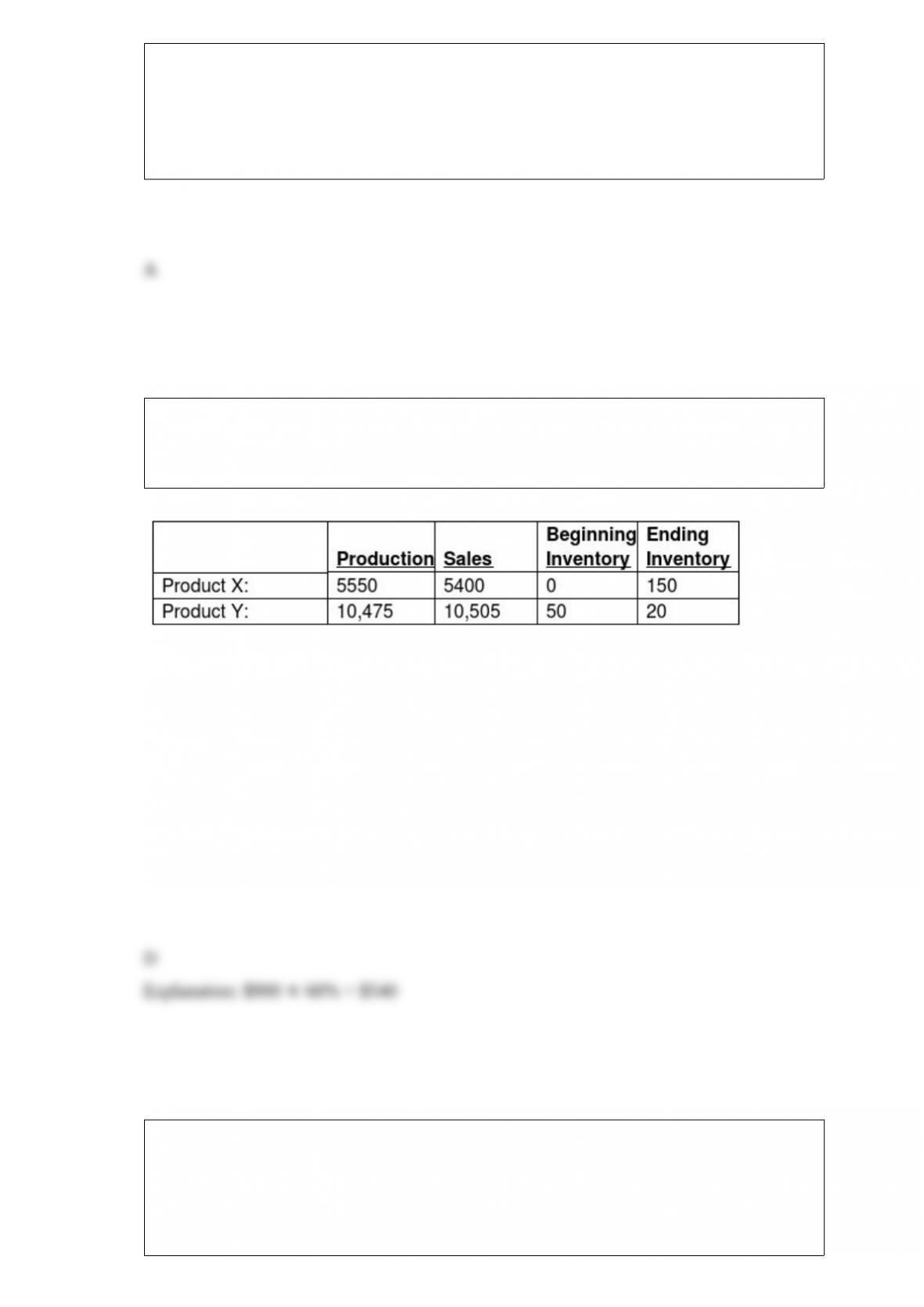

Torid Company processes 18,175 gallons of direct materials to produce two products,

Product X and Product Y. Product X sells for $6 per gallon and Product Y, the main

product, sells for $190 per gallon. The following information is for December:

The manufacturing costs totalled $29,000.

If the byproduct inventory is recorded at NRV less profit margin of 40%, the balance sheet

will report ________ of byproduct inventory.

A) $900

B) $0

C) $3800

D) $540

An annuity is ________.

A) a noncash expense

B) a series of equal cash flows at equal time intervals

C) an investment product whose funds are invested in the stock market

D) a rate at which an investment’s present value of all expected cash inflows equals the

present value of project’s expected cash outflows.

Harbor Corp currently leases a corporate suite in an office building for a cost of

$360,000 a year. Only 80% of the corporate suite is currently being used. A start-up

business has proposed a plan that would use the other 20% of the suite and increase the

overall costs of maintaining the space by $20,484. If the incremental method were used,

what amount of cost would be allocated to the start-up business?

A) $20,484

B) $380,484

C) $76,097

D) $88,387

Henry Chapman Manufacturing Inc. incurred the following expenses during 2017:

b

What will be the breakeven point if variable costing is used? (Round your final answer up

to the next whole unit.)

A) 891 units

B) 1,000 units

C) 720 units

D) 385 units

A manufacturer utilizes three separate indirect cost pools. Which of the following is

true?

A) Each indirect cost pool utilizes a separate cost-allocation rate

B) Each indirect cost pool is a subset of total direct costs

C) Each indirect cost pool relates to multiple cost centers

D) Each indirect cost pool utilizes the same cost-allocation rate for all costs incurred

Which of the following statements about ABC is not true?

A) A byproduct of ABC implementation can improve the efficiency of operations

B) ABC should be implemented solely by the accountants as they are the guardians of

the accounting information system

C) ABC may empower employees to also implement cost saving projects

D) Although implementation of ABC can be a refinement of a cost system, it has its

limitations

The following information is for High Corp:

The number of units that High Corp must sell to reach targeted operating income of

$25,000 is ________. (Round up to the nearest unit.)

A) 6,750 units

B) 8,000 units

C) 1,250 units

D) 2,667 units

Stones Manufacturing sells a marble slab for $1,100. Fixed costs are $33,000, while the

variable costs are $550 per slab. The company currently plans to sell 210 slabs this

month. What is the margin of safety assuming 85 slabs are actually sold? (Round

interim calculations and final calculations to the nearest whole number.)

A) $165,000

B) $49,500

C) $27,500

D) $33,000

A push-through system that manufactures finished goods for inventory on the basis of

demand forecasts and produces a master schedule for quantity and timing of units to be

produced.

A) just-in-time purchasing

B) materials requirements planning

C) relevant total costs

D) economic order quantity

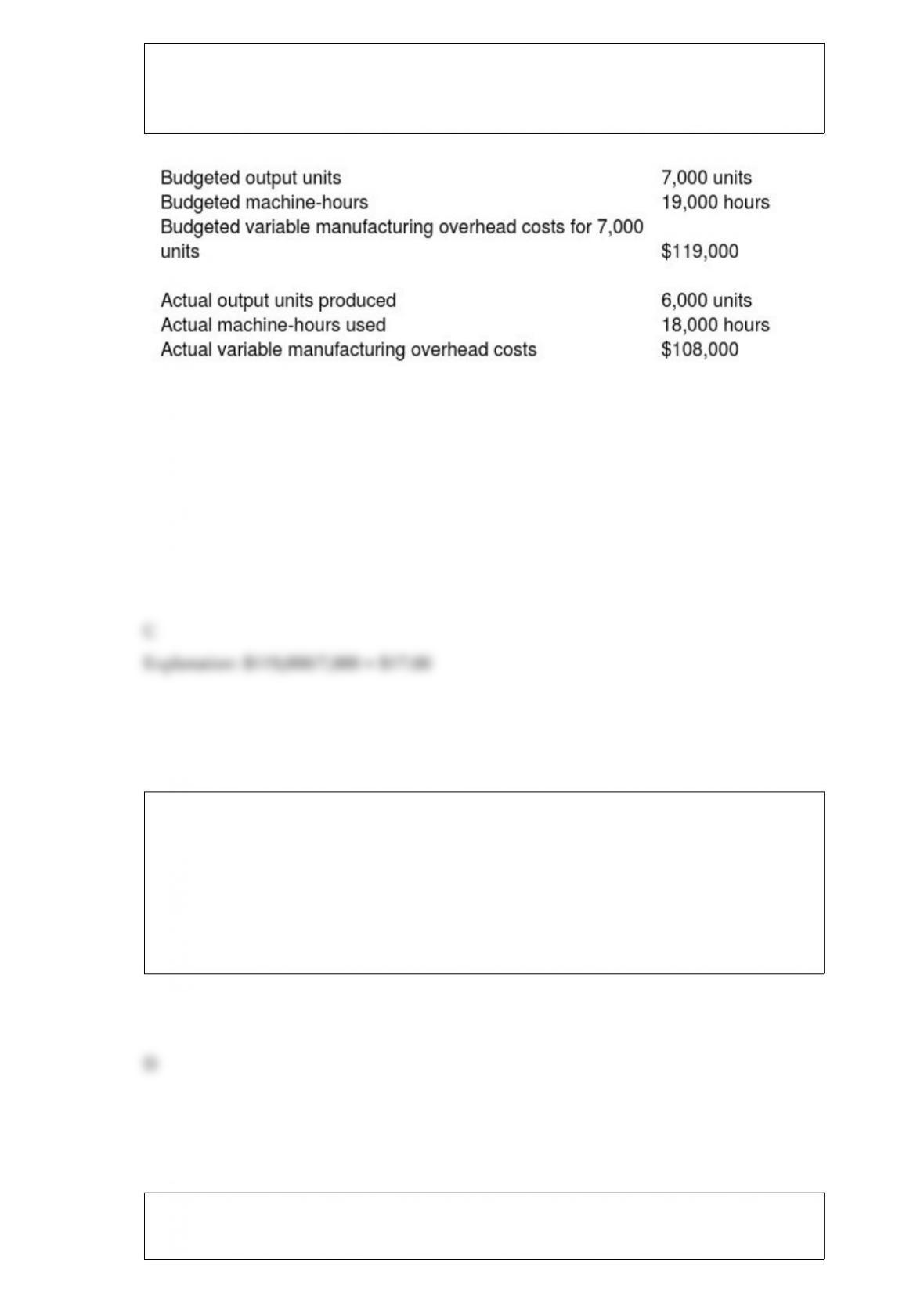

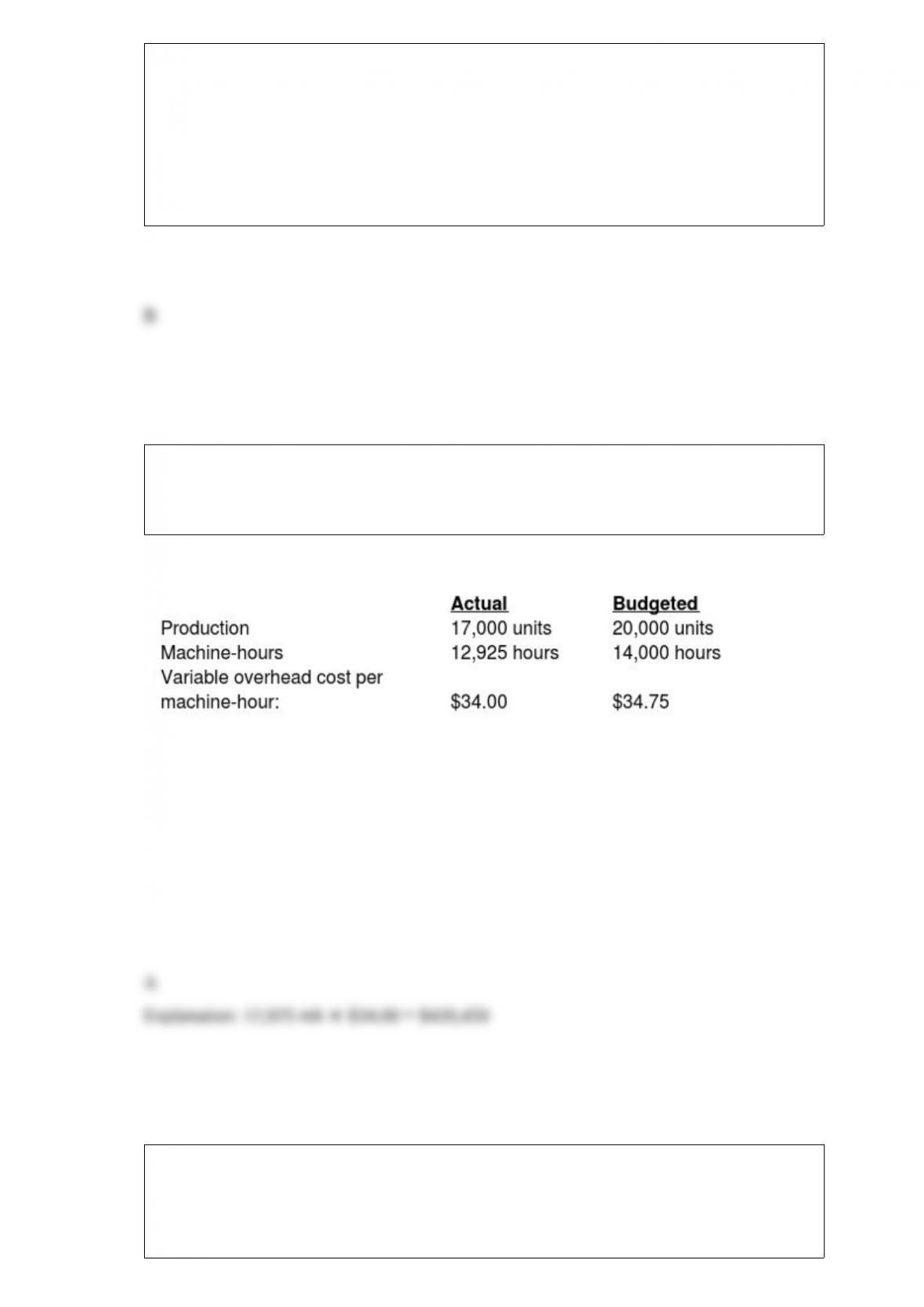

Russo Corporation manufactured 17,000 air conditioners during November. The

overhead cost-allocation base is $34.75 per machine-hour. The following variable

overhead data pertain to November:

What is the actual variable overhead cost?

A) $439,450

B) $476,000

C) $449,144

D) $486,500

Managers find operation costing useful in cost management because it ________.

A) often results in profit maximization

B) results in cost minimization

C) focuses on control of physical processes of a given production system

D) uses job costing to account for the conversion costs and process costing for the

material and customizable components

If there is an ethical conflict concerning your direct supervisor, when is it appropriate to

contact authorities or individuals not employed by the organization?

A) when there is a personal conflict

B) when your supervisor is about to be promoted

C) when there is a clear violation of the law

D) when you face injustice from your supervisor

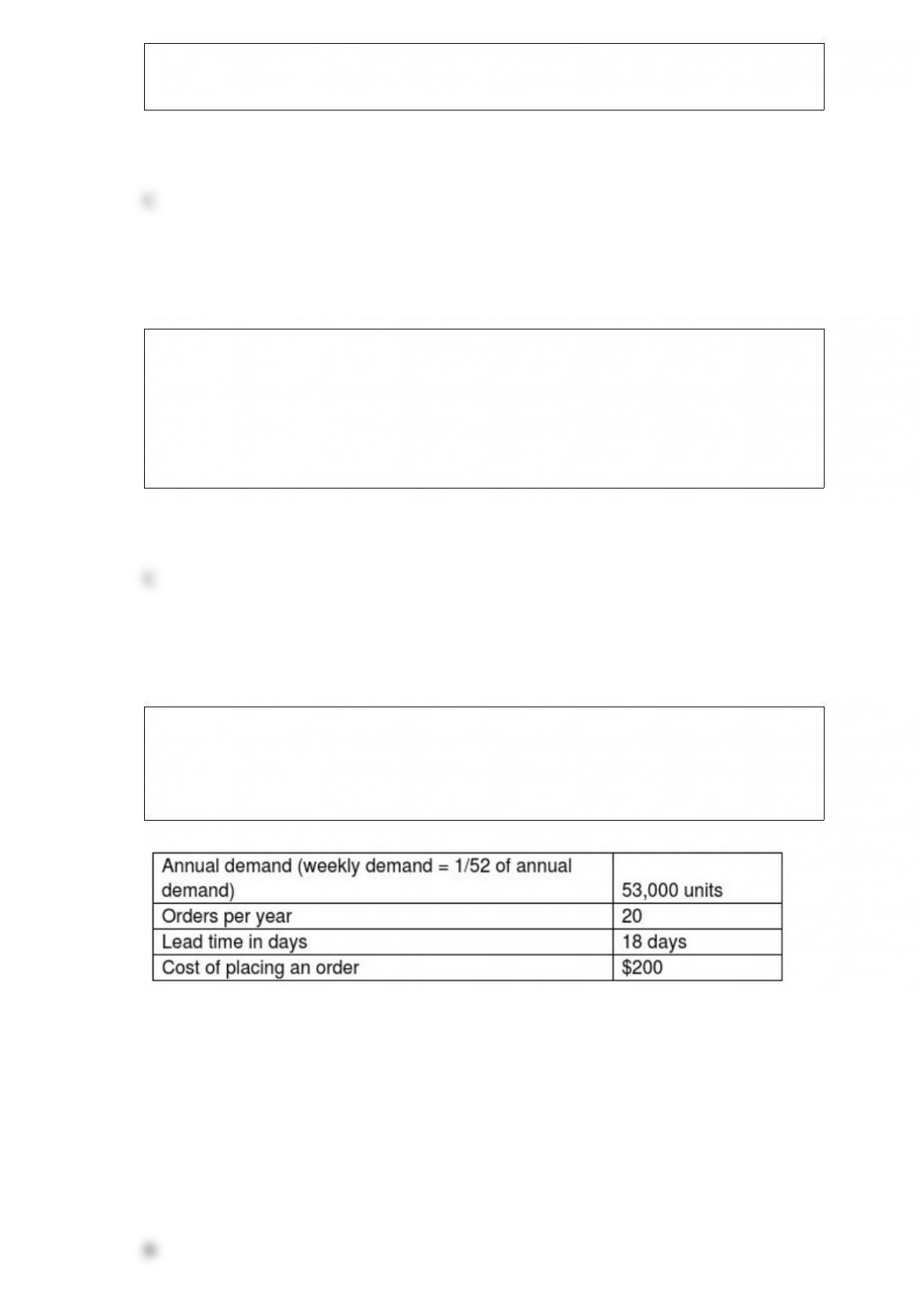

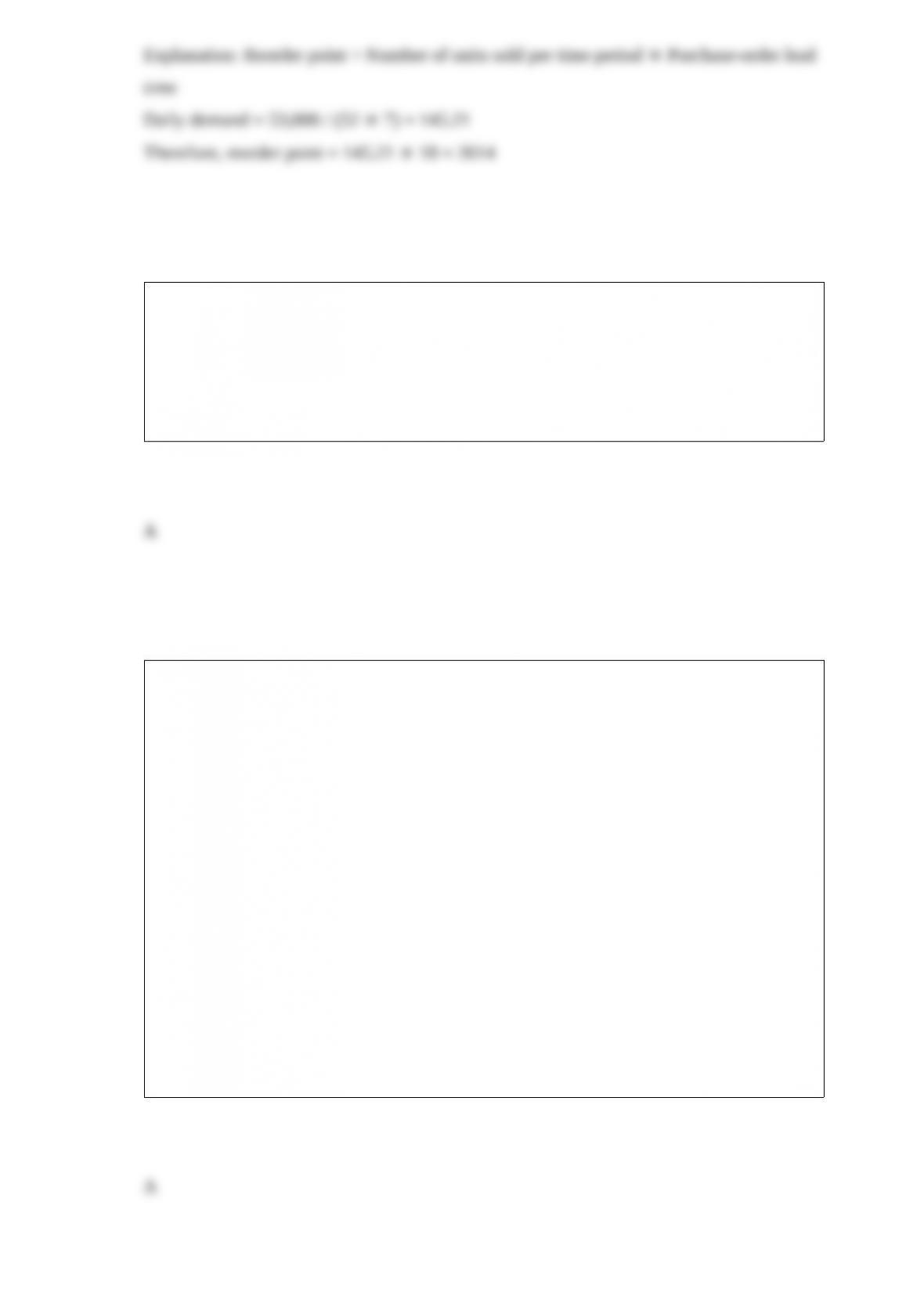

The following information applies to Krynton Company, which supplies microscopes to

laboratories throughout the country. Krynton purchases the microscopes from a

manufacturer which has a reputation for very high quality in its manufacturing

operation.

What is the reorder point? (Assume a 365 day year.)

A) 1040 units

B) 2614 units

C) 2650 units

D) 2944 units

Under absorption costing, if a manager’s bonus is tied to operating income, then

increasing inventory levels compared to last year would result in ________.

A) greater operating income and therefore increasing the manager’s bonus

B) less operating income and therefore decreasing the manager’s bonus

C) not affecting the manager’s bonus

D) being unable to determine the manager’s bonus using only the above information

LaCrosse Products has a budget of $907,000 in 2017 for prevention costs. If it decides

to automate a portion of its prevention activities, it will save $80,700 in variable costs.

The new method will require $40,200 in training costs and $102,000 in annual

equipment costs. Management is willing to adjust the budget for an amount up to the

cost of the new equipment. The budgeted production level is 155,000 units.

Appraisal costs for the year are budgeted at $600,000. The new prevention procedures

will save appraisal costs of $50,000. Internal failure costs average $15 per failed unit of

finished goods. The internal failure rate is expected to be 2% of all completed items.

The proposed changes will cut the internal failure rate by one-third. Internal failure

units are destroyed. External failure costs average $54 per failed unit. The company’s

average external failures average 2% of units sold. The new proposal will reduce this

rate by 45%. Assume all units produced are sold and there are no ending inventories.

How much will internal failure costs change if the internal product failures are reduced

by 1/3 with the new procedures? (Do not round intermediate calculations.)

A) $15,500 decrease

B) $19,582 decrease

C) $498,000 decrease

D) $755,000 decrease

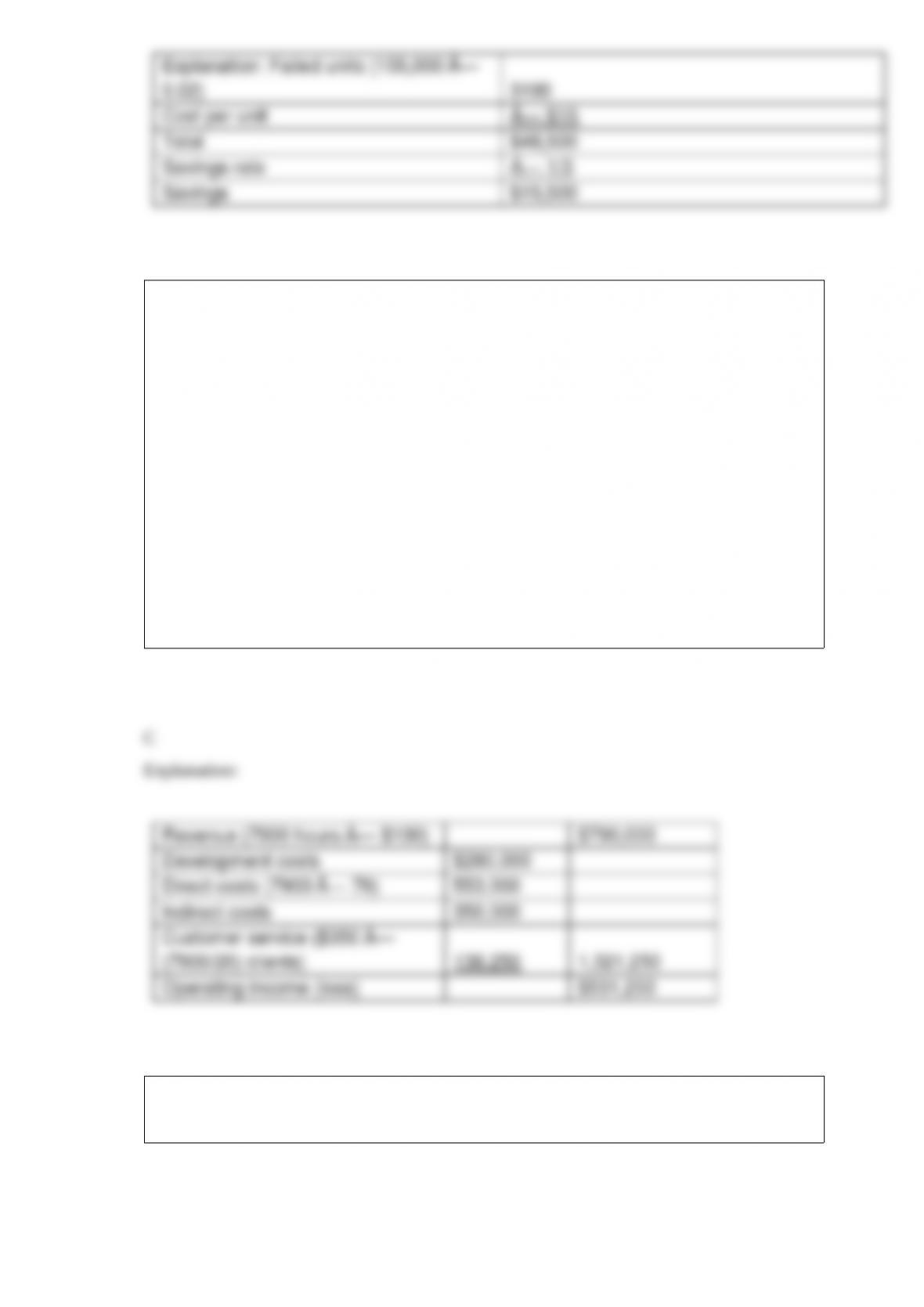

Knowledge Transfer Associates is in the process of evaluating its new client services for

the business systems consulting division.

∙ Server Planning, a new service, incurred $280,000 in development costs.

∙ The direct costs of providing the service, which is all labor, averages $70 per hour.

∙ Other costs for this service are estimated at $350,000 per year.

∙ The current program for server planning is expected to last for two years. At that time,

expected new operating systems are likely to make the service non viable.

∙ Customer service expenses average $350 per client, with each job lasting an average

of 20 hours. The current staff expects to bill 7900 hours for each of the two years the

program is in effect. Billing averages $100 per hour.

What is the estimated life-cycle operating income for the first year?

A) -$251,250

B) -$782,500

C) -$531,250

D) $531,250

Weighty Steel processes a single type of steel. For the current period the following

information is given:

All materials are added at the beginning of the production process. The beginning

inventory was 50% complete as to conversion, while the ending inventory was 25%

completed for conversion purposes.

Weighty uses the weighted-average costing method.

What is the total cost assigned to the units completed and transferred this period? (Round

intermediary dollar amounts to the nearest cent and total costs to the nearest whole dollar.)

A) $91,200

B) $115,050

C) $112,761

D) $121,600