SOLUTION

(45 min.) Static and flexible budgets, service sector.

1.

Static Budget

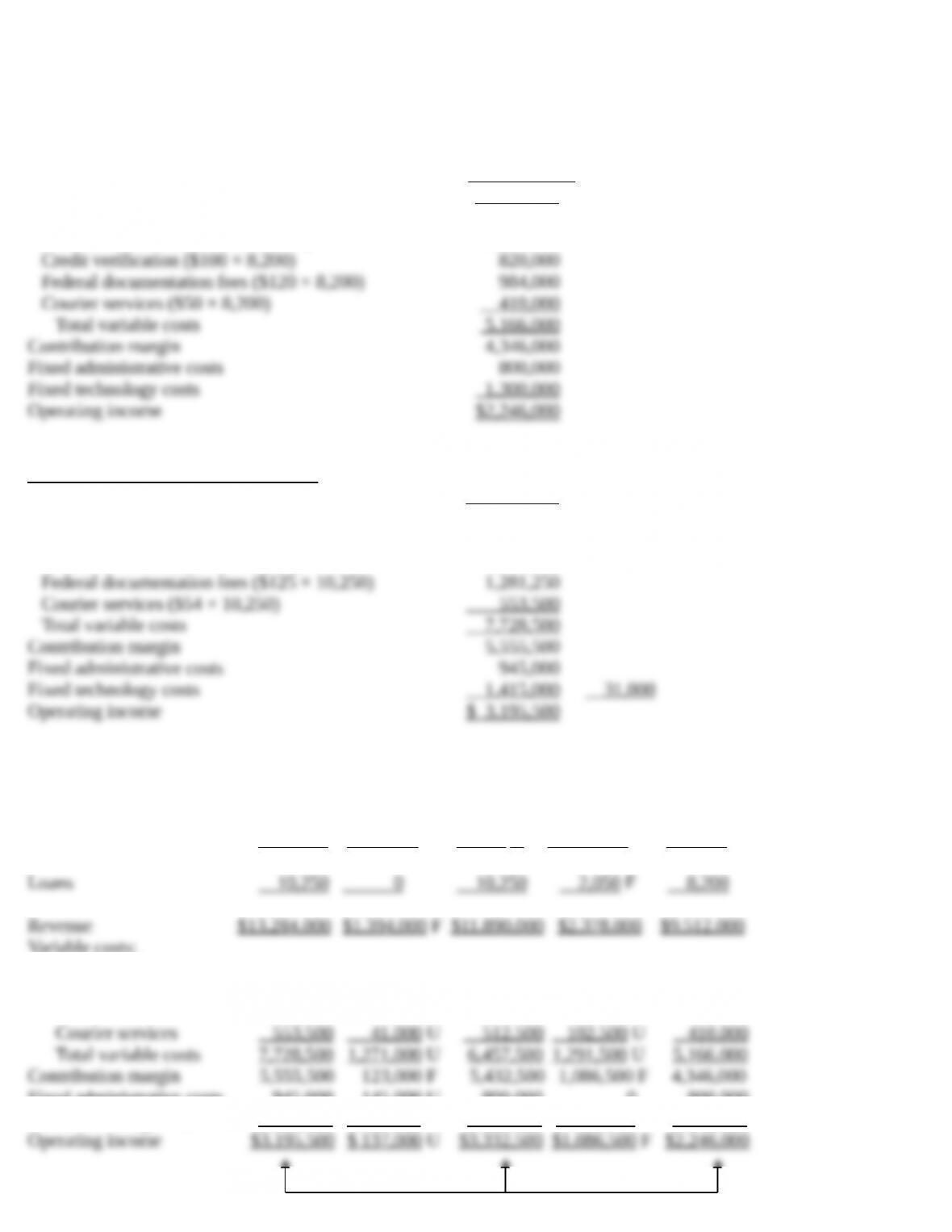

Revenue (8,200 × 0.8% × $145,000) $9,512,000

Variable costs:

Professional labor (8 × $45 × 8,200) 2,952,000

2.

Actual results for third quarter 2017:

Revenue (10,250 × 0.8% × $162,000) $13,284,000

Variable costs:

Professional labor (9.5 × $50 × 10,250) 4,868,750

Credit verification ($100 × 10,250) 1,025,000

Level 2 Analysis

Flexible- Sales-

Actual Budget Flexible Volume Static

Results Variances Budget Variances Budget

(1) (1) – (3) (3) (3) – (5) (5)

Variable costs:

Professional labor 4,868,750 1,178,750 U 3,690,000 738,000 U 2,952,000

Credit verification 1,025,000 0 1,025,000 205,000 U 820,000

Federal doc. Fees 1,281,250 51,250 U 1,230,000 246,000 U 984,000

Fixed administrative costs 945,000 145,000 U 800,000 0 800,000

Fixed technology costs 1,415,000 115,000 U 1,300,000 0 1,300,000

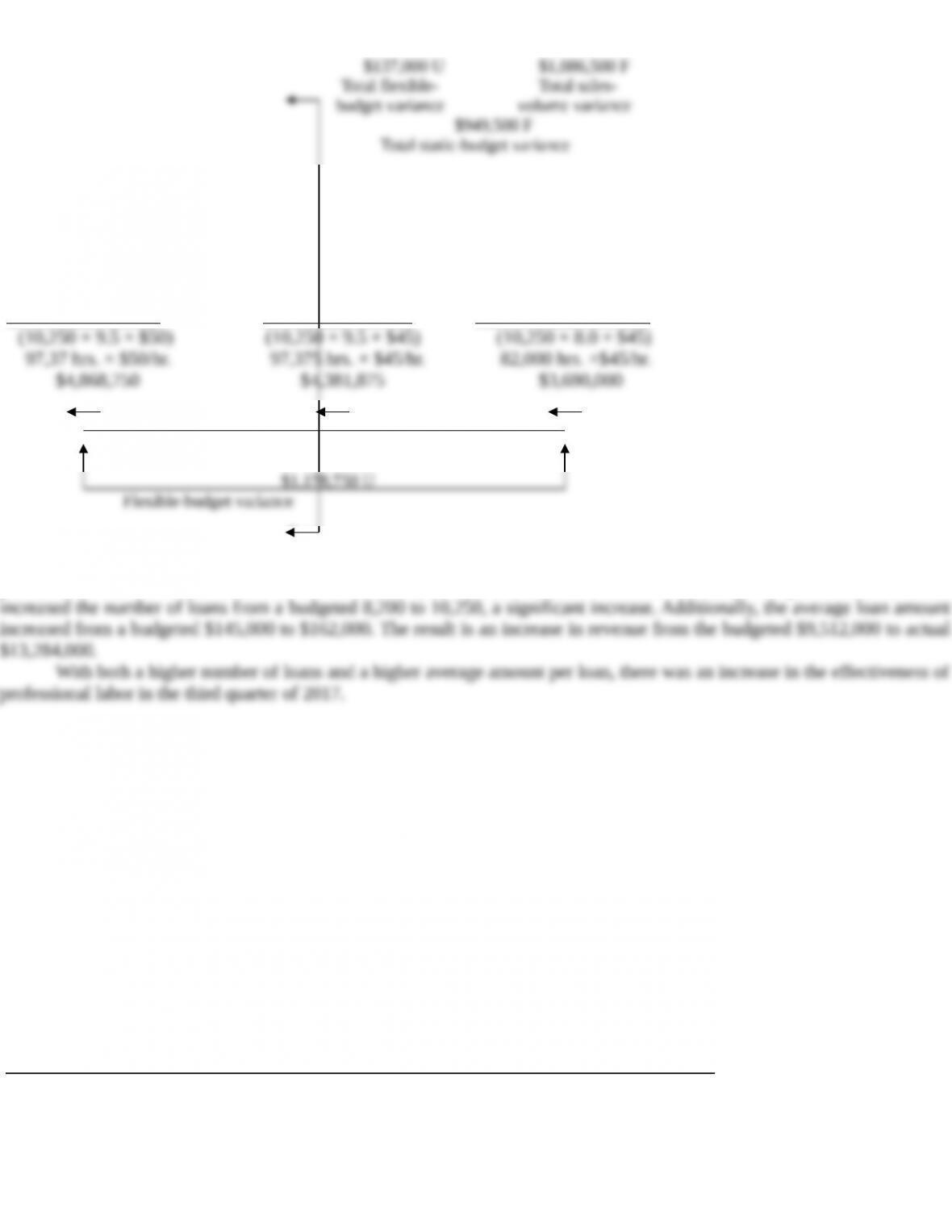

3.

Flexible Budget

Actual Costs (Budgeted Input

Incurred Qty. Allowed for

(Actual Input Qty. Actual Input Qty. Actual Output

× Actual Price) × Budgeted Price × Budgeted Price)

(1) (2) (3)

$486,875 U $691,875 U

Price variance Efficiency variance

4. Effectiveness refers to the degree to which a predetermined objective is accomplished. One objective of StuFi

professional labor is to maximize loan-based revenue (0.8% of loan amount × number of loans). The professional staff has

7-34 Flexible budget, direct materials, and direct manufacturing labor variances. Emerald Statuary manufactures bust

statues of famous historical figures. All statues are the same size. Each unit requires the same amount of resources. The follow-

ing information is from the static budget for 2017:

Expected production and sales 7,000 units

Expected selling price per unit $ 680

Total fixed costs $1,400,000

Standard quantities, standard prices, and standard unit costs follow for direct materials and direct manufacturing labor:

Standard Quantity Standard Price Standard Unit Cost

Direct materials 10 pounds $ 8 per pound $ 80

Direct manufacturing la-

bor

3.7 hours $50 per hour $185

During 2017, actual number of units produced and sold was 4,800, at an average selling price of $720. Actual cost of direct mate-

rials used was $392,700, based on 66,000 pounds purchased at $5.95 per pound. Direct manufacturing labor-hours actually used

were 18,300, at the rate of $48 per hour. As a result, actual direct manufacturing labor costs were $878,400. Actual fixed costs

were $1,170,000. There were no beginning or ending inventories.

Required:

1. Calculate the sales-volume variance and flexible-budget variance for operating income.

2. Compute price and efficiency variances for direct materials and direct manufacturing labor.

SOLUTION

(30 min.) Flexible budget, direct materials and direct manufacturing labor variances.

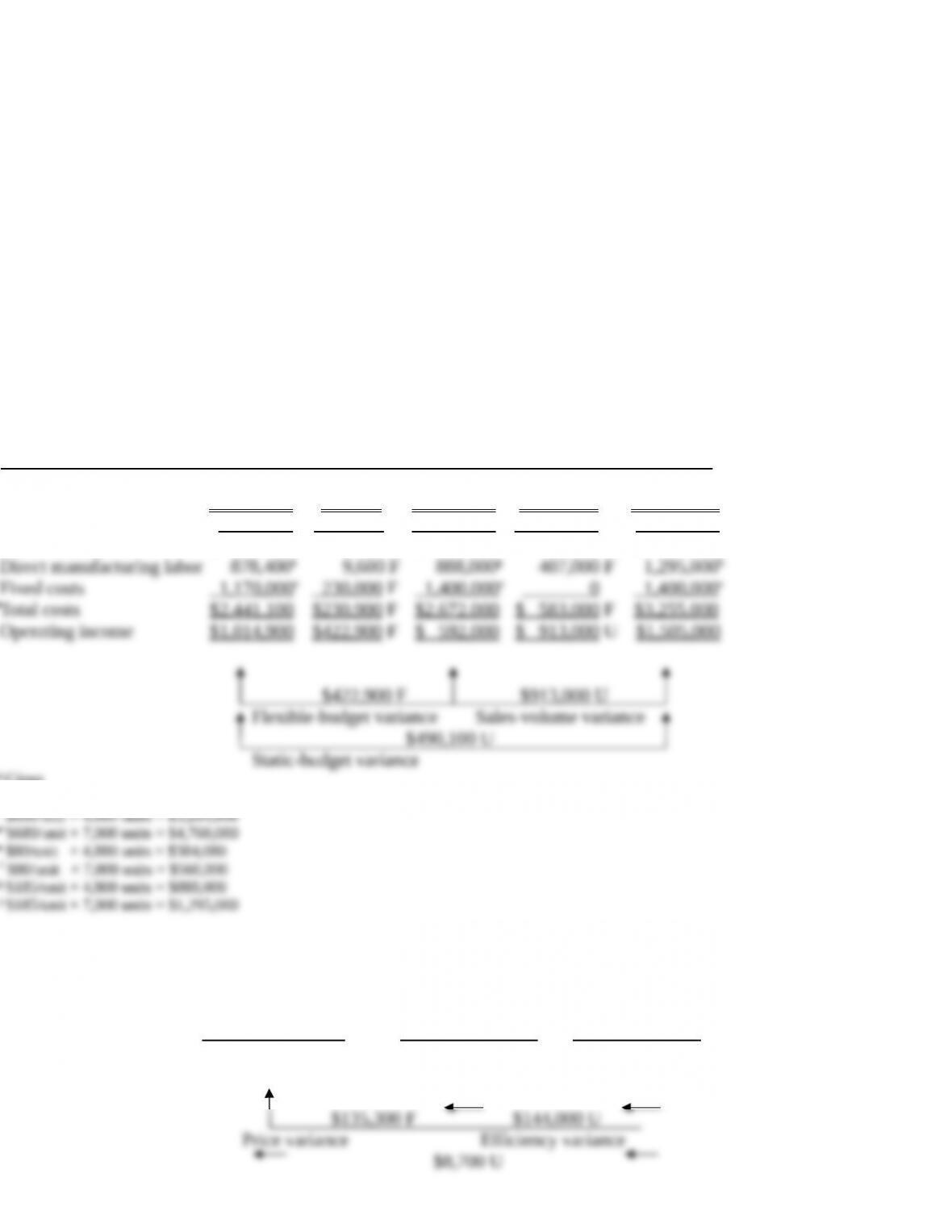

1. Variance Analysis for Emerald Statuary for 2017

Flexible- Sales-

Actual Budget Flexible Volume Static

Results Variances Budget Variances Budget

(1) (2) = (1) – (3) (3) (4) = (3) – (5) (5)

Units sold 4,800a 0 4,800 2,200 U 7,000a

Revenues $3,456,000b $192,000 F $3,264,000c $1,496,000 U $4,760,000d

Direct materials $ 392,700 $ 8,700 U $ 384,000e $ 176,000 F $ 560,000f

a Given

b $720/unit × 4,800 units = $3,456,000

c $680/unit × 4,800 units = $3,264,000

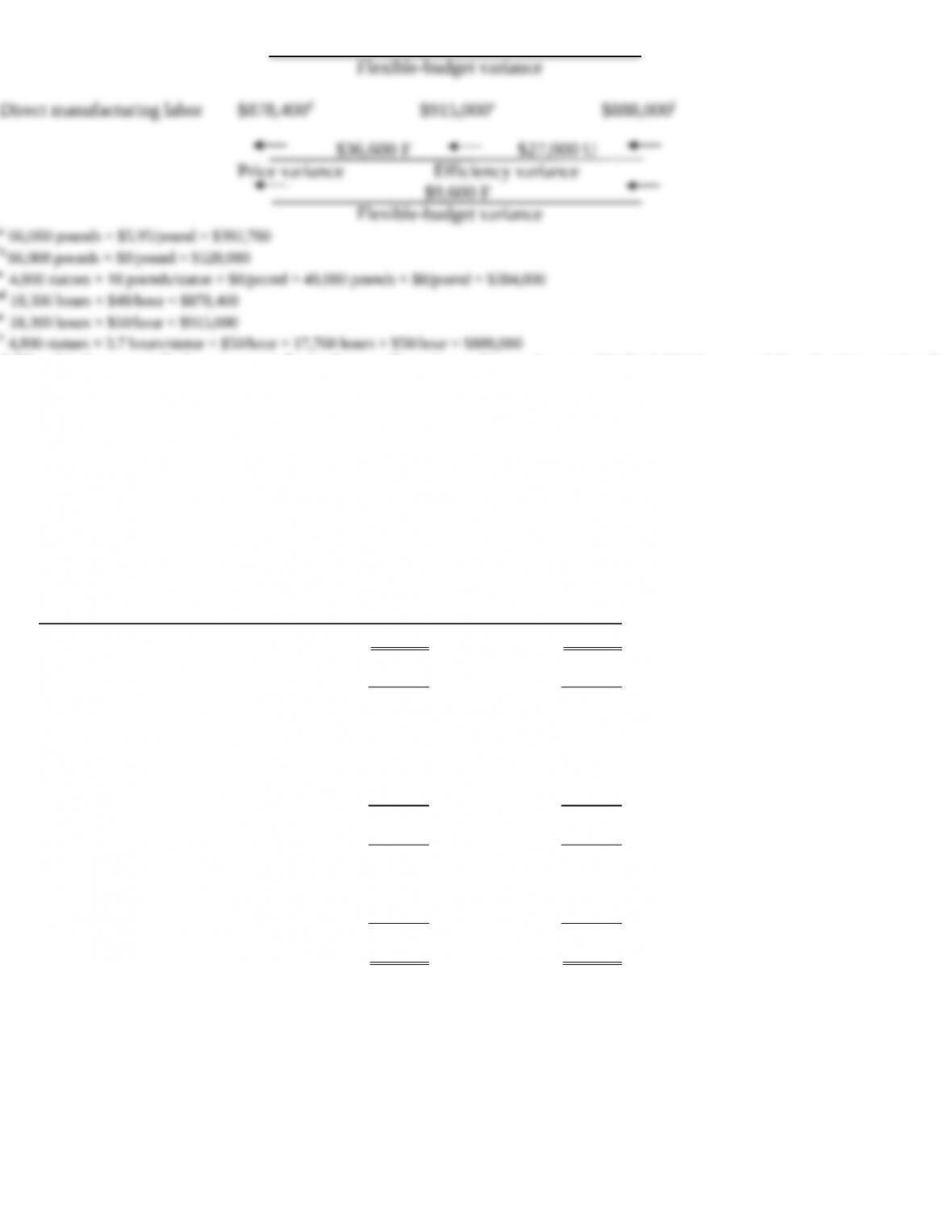

2. Flexible Budget

(Budgeted Input

Actual Incurred Qty. Allowed for

(Actual Input Qty. Actual Input Qty. Actual Output ×

× Actual Price) × Budgeted Price Budgeted Price)

Direct materials $392,700a$528,000b$384,000c

7-35 Variance analysis, nonmanufacturing setting. Joyce Brown has run Medical Maids, a specialty cleaning service for

medical and dental offices, for the past 10 years. Her static budget and actual results for April 2017 are shown below. Joyce has one

employee who has been with her for all 10 years that she has been in business. In addition, at any given time she also employs two

other less-experienced workers. It usually takes each employee 2 hours to clean an office, regardless of his or her experience.

Brown pays her experienced employee $30 per office and the other two employees $15 per office. There were no wage increases in

April.

Medical Maids Actual and Budgeted Income

Statements For the Month Ended April 30, 2017

Budget Actual

Offices cleaned 140

160

Revenue $26,600 $36,000

Variable costs:

Costs of supplies 630 680

Labor 3,360 4,200

Total variable costs 3,990 4,880

Contribution margin 22,610 31,120

Fixed costs 4,900 4,900

Operating income $17,710

$26,220

Required:

1. How many offices, on average, did Brown budget for each employee? How many offices did each employee actually

clean?

2. Prepare a flexible budget for April 2017.

3. Compute the sales price variance and the labor efficiency variance for each labor type.

4. What information, in addition to that provided in the income statements, would you want Brown to gather, if you wanted to

improve operational efficiency?

SOLUTION

(30 min.) Variance analysis, nonmanufacturing setting

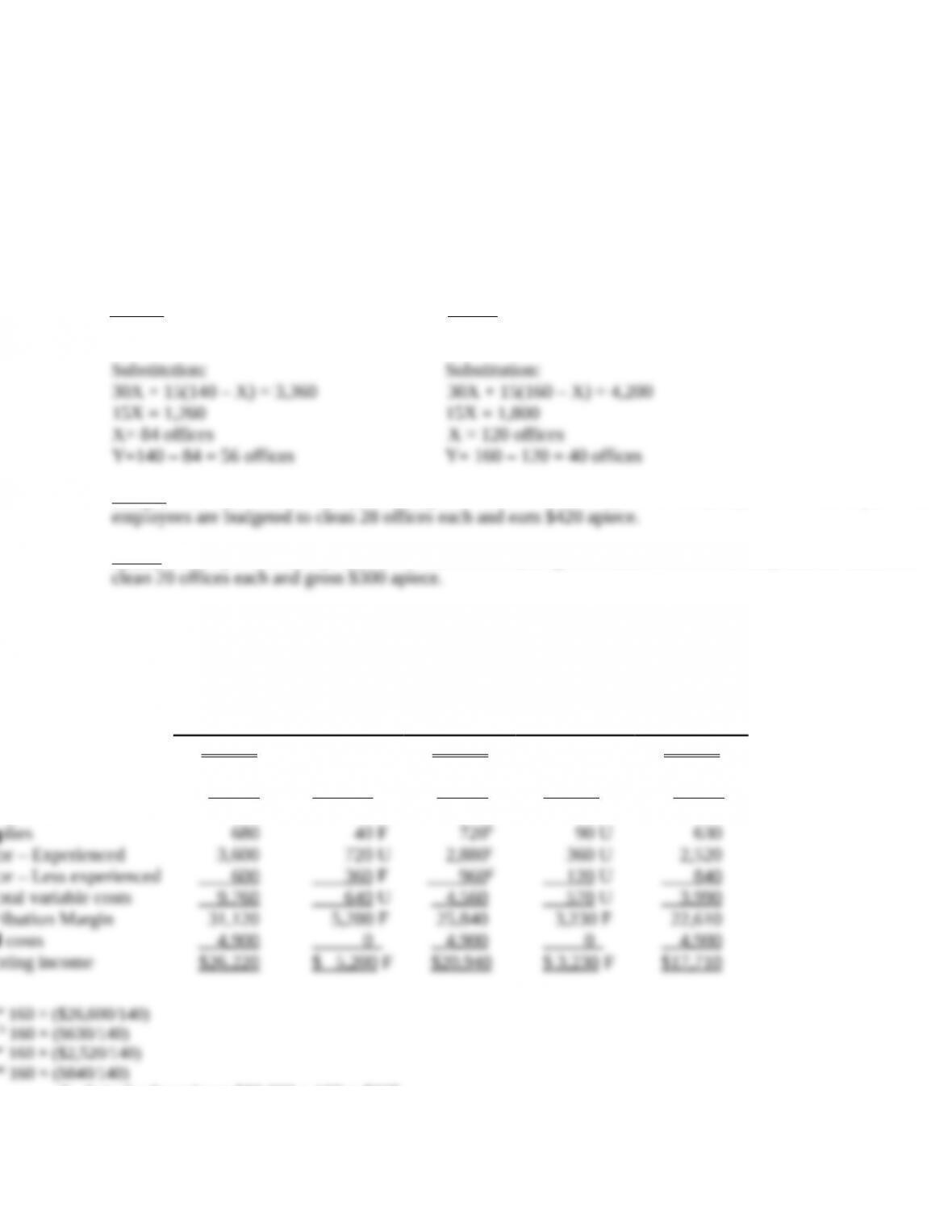

1. This is a problem of two equations & two unknowns. The two equations relate to the number of offices cleaned and the

labor costs (the wages paid to the employees).

X = number of offices cleaned by the experienced employee

Y = number of offices cleaned by the less experienced employees (combined)

Budget: X + Y = 140 Actual: X + Y = 160

$30X + $15Y = $3,360 $30X + $15Y = $4,200

Budget: The experienced employee is budgeted to clean 84 offices (and earn $2,520), and the less experienced

Actual: The experienced employee cleans 120 offices (and grosses $3,600 for the month), and the other two

2.

Actual

Results

(1)

Flexible-

Budget

Variances

(2) = (1) –

(3)

Flexible

Budget

(3)

Sales –

Volume

Variance

(4) = (3) –

(5)

Static

Budget

(5)

Offices cleaned 160 160 140

Revenues $36,000 $ 5,600 F $30,400a $ 3,800 F $ 26,600

Variable costs

3. Actual sales price = $36,000 ÷ 160 = $225

Sales Price Variance

= (Actual sales price – Budgeted sales price) × Actual number of offices cleaned:

Labor efficiency for experienced worker:

Standard offices expected to be completed by experienced worker based on actual number of offices cleaned = (84 ÷

140) × 160 = 96 offices

Labor efficiency variance = Budgeted wage rate per office × (Actual offices cleaned – budgeted offices cleaned)

Labor efficiency for less-experienced workers:

Standard offices expected to be completed by less-experienced workers based on actual number of offices cleaned =

4. In addition to understanding the variances computed above, Brown should attempt to keep track of the number of

7-36 Comprehensive variance analysis review. Ellis Animal Health, Inc., produces a generic medication used to

treat cats with feline diabetes. The liquid medication is sold in 100 ml vials. Ellis employs a team of sales representatives who are

paid varying amounts of commission.

Given the narrow margins in the generic veterinary drugs industry, Ellis relies on tight standards and cost controls to manage its

operations. Ellis has the following budgeted standards for the month of April 2017:

Average selling price per vial $ 8.30

Total direct materials cost per vial $ 3.60

Direct manufacturing labor cost per hour $ 15.00

Average labor productivity rate (vials per hour) 100

Sales commission cost per vial $ 0.72

Fixed administrative and manufacturing over-

head

$990,000

Ellis budgeted sales of 700,000 vials for April. At the end of the month, the controller revealed that actual results for April had

deviated from the budget in several ways:

Unit sales and production were 90% of plan.

Actual average selling price decreased to $8.20.

Productivity dropped to 90 vials per hour.

Actual direct manufacturing labor cost was $15.20 per hour.

Actual total direct material cost per unit increased to $3.90.

Actual sales commissions were $0.70 per vial.

Fixed overhead costs were $110,000 above budget.

Calculate the following amounts for Ellis for April 2017:

Required:

1. Static-budget and actual operating income

2. Static-budget variance for operating income

3. Flexible-budget operating income

4. Flexible-budget variance for operating income

5. Sales-volume variance for operating income

6. Price and efficiency variances for direct manufacturing labor

7. Flexible-budget variance for direct manufacturing labor