CHAPTER 11

DECISION MAKING AND RELEVANT INFORMATION

11-1 Outline the five-step sequence in a decision process.

The five steps in the decision process outlined in Exhibit 11-1 of the text are

1. Identify the problem and uncertainties.

11-2 Define relevant costs. Why are historical costs irrelevant?

11-3 “All future costs are relevant.” Do you agree? Why?

11-4 Distinguish between quantitative and qualitative factors in decision making.

Quantitative factors are outcomes that are measured in numerical terms. Some quantitative

11-5 Describe two potential problems that should be avoided in relevant-cost analysis.

Two potential problems that should be avoided in relevant cost analysis are

11-6 “Variable costs are always relevant, and fixed costs are always irrelevant.” Do you

agree? Why?

No. Some variable costs may not differ among the alternatives under consideration and, hence,

11-1

11-7 “A component part should be purchased whenever the purchase price is less than its total

manufacturing cost per unit.” Do you agree? Why?

No. Some of the total manufacturing cost per unit of a product may be fixed and, hence, will not

differ between the make and buy alternatives. These fixed costs are irrelevant to the make-or-buy

11-8 Define opportunity cost.

11-9 “Managers should always buy inventory in quantities that result in the lowest purchase

cost per unit.” Do you agree? Why?

No. When deciding on the quantity of inventory to buy, managers must consider both the

11-10 “Management should always maximize sales of the product with the highest contribution

margin per unit.” Do you agree? Why?

11-11 “A branch office or business segment that shows negative operating income should be

shut down.” Do you agree? Explain briefly.

11-12 “Cost written off as depreciation on equipment already purchased is always irrelevant.”

Do you agree? Why?

11-13 “Managers will always choose the alternative that maximizes operating income or

minimizes costs in the decision model.” Do you agree? Why?

11-2

11-14 Describe the three steps in solving a linear programming problem.

The three steps in solving a linear programming problem are

11-15 How might the optimal solution of a linear programming problem be determined?

The text outlines two methods of determining the optimal solution to an LP problem:

11-16 Qualitative and quantitative factors. Which of the following is not a qualitative factor

that Atlas Manufacturing should consider when deciding whether to buy or make a part used in

manufacturing their product?

a. Quality of the outside producer’s product.

b. Potential loss of trade secrets.

c. Manufacturing deadlines and special orders.

d. Variable cost per unit of the product.

SOLUTION

Choice “d” is correct. Calculating the costs of production of the part versus buying the part from an

outside source is a quantitative factor used by a company to determine the lowest cost alternative.

11-17 Special order, opportunity cost. Chade Corp. is considering a special order brought to it

by a new client. If Chade determines the variable cost to be $9 per unit, and the contribution

margin of the next best alternative of the facility to be $5 per unit, then if Chade has:

11-3

a. Full capacity, the company will be profitable at $4 per unit.

b. Excess capacity, the company will be profitable at $6 per unit.

c. Full capacity, the selling price must be greater than $5 per unit.

d. Excess capacity, the selling price must be greater than $9 per unit.

SOLUTION

Choice “d” is correct. At excess capacity, Chade will accept the special order as long as the sales price is

greater than the variable cost per unit. At $9 per unit for variable cost, Chade will accept the special order

11-18 Special order, opportunity cost. In order to determine whether a special order should be

accepted at full capacity, the sales price of the special order must be compared to the per unit:

a. Contribution margin of the special order.

b. Variable cost and contribution margin of the special order.

c. Variable cost and contribution margin of the next best alternative.

d. Variable cost of current production and the contribution margin of the next best alternative.

SOLUTION

Choice “d” is correct. If the selling price is greater than the variable cost per unit of the special order (at

full capacity) plus the contribution margin per unit of the next best alternative (the opportunity cost),

11-19 Keep or drop a business segment. Lees Corp. is deciding whether to keep or drop a

small segment of its business. Key information regarding the segment includes:

Contribution margin: 35,000

Avoidable fixed costs: 30,000

Unavoidable fixed costs: 25,000

Given the information above, Lees should:

a. Drop the segment because the contribution margin is less than total fixed costs.

b. Drop the segment because avoidable fixed costs exceed unavoidable fixed costs.

c. Keep the segment because the contribution margin exceeds avoidable fixed costs.

d. Keep the segment because the contribution margin exceeds unavoidable fixed costs.

11-4

SOLUTION

Choice “c” is correct. Whether to keep or drop a segment will depend on whether the contribution

margin of the segment in question exceeds avoidable fixed costs (relevant costs that wouldn’t exist if the

segment did not exist). Unavoidable fixed costs will be incurred regardless of whether or not the

11-20 Relevant costs. Ace Cleaning Service is considering expanding into one or more new

market areas. Which costs are relevant to Ace’s decision on whether to expand?

SOLUTION

Choice “a” is correct. Sunk costs are not relevant since they were incurred in the past and cannot be

recovered as a result of the company’s current decision. Variable costs are relevant as also any avoidable

11-21 Disposal of assets. Answer the following questions.

1. A company has an inventory of 1,300 assorted parts for a line of missiles that has been

discontinued. The inventory cost is $71,000. The parts can be either (a) remachined at total

additional costs of $27,500 and then sold for $31,500 or (b) sold as scrap for $6,000. Which

action is more profitable? Show your calculations.

2. A truck, costing $102,500 and uninsured, is wrecked its first day in use. It can be either (a)

disposed of for $14,000 cash and replaced with a similar truck costing $105,500 or (b) rebuilt

for $86,000 and thus be brand-new as far as operating characteristics and looks are

concerned. Which action is less costly? Show your calculations.

11-5

SOLUTION

(20 min.) Disposal of assets.

1. This is an unfortunate situation, yet the $71,000 of inventory costs are irrelevant

regarding the decision to remachine or scrap. The only relevant factors are the future revenues

and future costs. By ignoring the accumulated costs and deciding on the basis of expected future

costs, operating income will be maximized (or losses minimized). The difference in favor of

selling as scrap is $2,000:

(a) (b)

Remachine Scrap

2. This, too, is an unfortunate situation. But the $102,500 original cost of the truck is

irrelevant to this decision. The difference in relevant costs in favor of rebuilding is $5,500 as

follows:

(a) (b)

Replace Rebuild

Note, here, that the current disposal price of $14,000 is relevant, but the original cost (or book

value, if the truck were not brand new) is irrelevant.

11-22 Relevant and irrelevant costs. Answer the following questions.

1. Robinson Computers makes 5,700 units of a circuit board, CB76, at a cost of $230 each.

Variable cost per unit is $180 and fixed cost per unit is $50. Peach Electronics offers to

supply 5,700 units of CB76 for $210. If Robinson buys from Peach, it will be able to save

$20 per unit in fixed costs but continue to incur the remaining $30 per unit. Should Robinson

accept Peach’s offer? Explain.

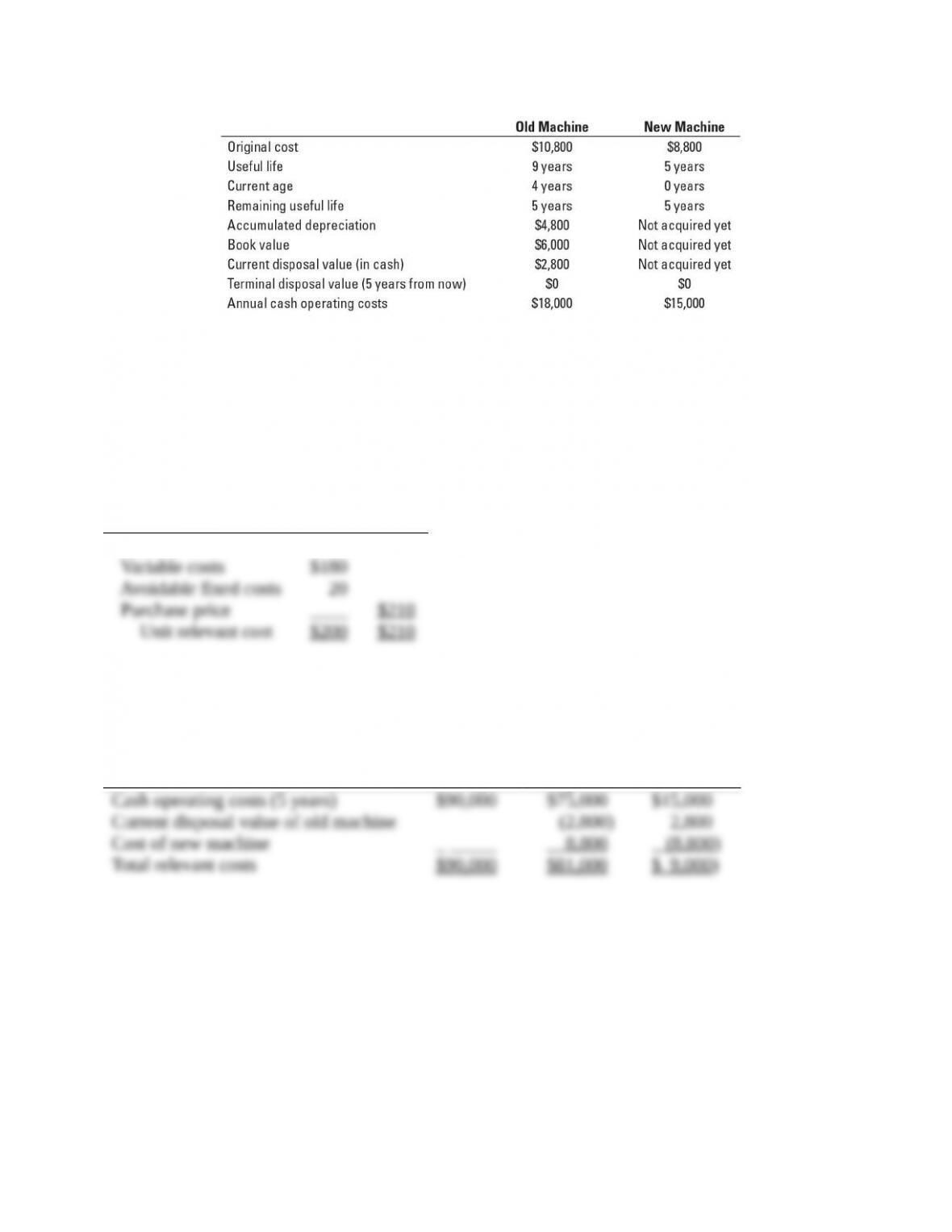

2. RT Manufacturing is deciding whether to keep or replace an old machine. It obtains the

following information:

11-6

RT Manufacturing uses straight-line depreciation. Ignore the time value of money and income

taxes. Should RT Manufacturing replace the old machine? Explain.

SOLUTION

(20 min.) Relevant and irrelevant costs.

1.

Make Buy

Relevant costs

Robinson Computers should reject Peach’s offer. The $30 of fixed costs is irrelevant because it

will be incurred regardless of this decision. When comparing relevant costs between the choices,

Peach’s offer price is higher than the cost to continue to produce.

2.

Keep Replace Difference

RT Manufacturing should replace the old machine. The cost to purchase the new machine are

less than the cost to keep and operate the old machine.

11-23 Multiple choice. (CPA) Choose the best answer.

1. The Cozy Company manufactures slippers and sells them at $10 a pair. Variable

manufacturing cost is $5.75 a pair, and allocated fixed manufacturing cost is $1.75 a pair. It

has enough idle capacity available to accept a one-time-only special order of 25,000 pairs of

slippers at $7.50 a pair. Cozy will not incur any marketing costs as a result of the special

order. What would the effect on operating income be if the special order could be accepted

without affecting normal sales: (a) $0, (b) $43,750 increase, (c) $143,750 increase, or (d)

11-7

$187,500 increase? Show your calculations.

2. The Manchester Company manufactures Part No. 498 for use in its production line. The

manufacturing cost per unit for 10,000 units of Part No. 498 is as follows:

The Remnant Company has offered to sell 10,000 units of Part No. 498 to Manchester for $71

per unit. Manchester will make the decision to buy the part from Remnant if there is an overall

savings of at least $45,000 for Manchester. If Manchester accepts Remnant’s offer, $11 per unit

of the fixed overhead allocated would be eliminated. Furthermore, Manchester has determined

that the released facilities could be used to save relevant costs in the manufacture of Part No.

575. For Manchester to achieve an overall savings of $45,000, the amount of relevant costs that

would have to be saved by using the released facilities in the manufacture of Part No. 575 would

be which of the following: (a) $30,000, (b) $115,000, (c) $125,000, or (d) $100,000? Show your

calculations. What other factors might Manchester consider before outsourcing to Remnant?

(15 min.) Multiple choice.

Effect on operating income = $1.75 25,000 units

Total relevant costs of making part No. 498:

Multiply by 10,000 units, so total

Before outsourcing to Remnant, Manchester must consider the consequence of increasing its

dependence on Remnant. Manchester would want to be sure about the quality of Remnant’s

product and the reliability of its delivery schedules over a long-run period. Manchester would

also want Remnant to continuously reduce costs. To achieve all these goals, Manchester may

want to build close partnerships and alliances with Remnant.

11-8

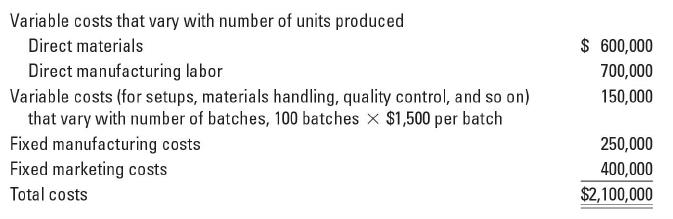

11-24 Special order, activity-based costing. (CMA, adapted) The Reward One Company

manufactures windows. Its manufacturing plant has the capacity to produce 12,000 windows

each month. Current production and sales are 10,000 windows per month. The company

normally charges $250 per window. Cost information for the current activity level is as follows:

Reward One has just received a special one-time-only order for 2,000 windows at $225 per

window. Accepting the special order would not affect the company’s regular business or its fixed

costs. Reward One makes windows for its existing customers in batch sizes of 100 windows (100

batches 100 windows per batch = 10,000 windows). The special order requires Reward One to

make the windows in 25 batches of 80 windows.

Required:

1. Should Reward One accept this special order? Show your calculations.

2. Suppose plant capacity were only 11,000 windows instead of 12,000 windows each month.

The special order must either be taken in full or be rejected completely. Should Reward One

accept the special order? Show your calculations.

3. As in requirement 1, assume that monthly capacity is 12,000 windows. Reward One is

concerned that if it accepts the special order, its existing customers will immediately

demand a price discount of $20 in the month in which the special order is being filled. They

would argue that Reward One’s capacity costs are now being spread over more units and

that existing customers should get the benefit of these lower costs. Should Reward One

accept the special order under these conditions? Show your calculations.

11-9