Archives

978-0078025587 Appendix A Solution Manual

Appendix B Time Value of Money QUICK STUDIES Quick Study B-1 (10 minutes) 1. 2% 2. 12% 3. 3% 4. 1% Quick Study B-2 (10 minutes) In Table B.1, where n = 15 and p = $2,745/$10,000 = 0.2745, the […]

978-0078025587 Appendix B Lecture Note

B-1 APPENDIX B TIME VALUE OF MONEY © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, […]

978-0078025587 Appendix B Solution Manual

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

978-0078025587 Appendix B Solution Manual Part 1

. Title: Question 1 QA_Ori: Manufacturing overhead costs cannot be directly traced to units of product Title: Question 2 QA_Ori: In the first stage, service department costs are assigned to operating departments. In the second stage, a predetermined overhead rate […]

978-0078025587 Appendix B Solution Manual Part 2

Title: Exercise C-4 QA_Ori: 1. Total direct labor hours: Product A: 10,000 units x 0.20 DLH/unit = 2,000 DLH Plant-wide overhead rate: $249,000/2,500 DLH = $99.60/DLH Product A Product B Direct materials A: 10,000 units x $2/unit $20,000 B: 2,000 […]

978-0078025587 Appendix B Solution Manual Part 3

Title: Problem C-4A QA_Ori: 1. Plantwide overhead rate: Engineering support $24,500 Product A 10,000 units x 0.3 DLH/unit = 3,000 DLH Product B 2,000 units x 1.6 DLH/unit = 3,200 DLH 6,200 DLH Product A Product B Direct materials per […]

978-0078025587 Appendix B Solution Manual Part 4

Title: Problem C-3B QA_Ori: 1. The major costs of making the boxes are designing the boxes, setting up machines to make the right cuts, cutting the cardboard, printing the boxes, 3. Yes. Lakeside’s old customers bought the same type of […]

978-0078025587 Appendix C Lecture Note

C-1 APPENDIX C ACTIVITY-BASED COSTING © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted […]

978-0078025587 Appendix C Solution Manual Part 1

Appendix C Activity-Based Costing QUESTIONS 1. Manufacturing overhead costs cannot be directly traced to units of product like direct materials and direct labor. Assigning overhead costs to units of product requires some sort of allocation on some “reasonable” basis. 2. […]

978-0078025587 Appendix C Solution Manual Part 2

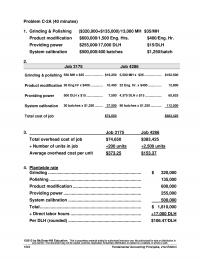

Problem C-2A (40 minutes) 1. Grinding & Polishing ($320,000+$135,000)/13,000 MH $35/MH Product modification $600,000/1,500 Eng. Hrs. $400/Eng. Hr. Providing power $255,000/17,000 DLH $15/DLH System calibration $500,000/400 batches $1,250/batch 2. Job 3175 Job 4286 Grinding & polishing 550 MH x $35 […]

978-0078025587 Appendix C Solution Manual Part 3

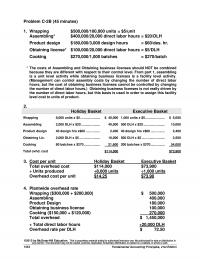

Problem C-2B (45 minutes) 1. Wrapping $500,000/100,000 units = $5/unit Assembling* $400,000/20,000 direct labor hours = $20/DLH Product design $180,000/3,000 design hours = $60/des. hr. Obtaining license* $100,000/20,000 direct labor hours = $5/DLH Cooking $270,000/1,000 batches = $270/batch * The […]

978-0078025587 Chapter 1 Excel

Student Name: Class: Liabilities + Equity Accounts Office Accounts H. Graham H. Graham Date Cash Receivable Equipment Payable Capital Withdrawals Revenues Expenses May 1 $40,000 40,000 1 (2,200) (2,200) 3 1,890 1,890 5 (750) (750) 8 5,400 5,400 12 2,500 […]

978-0078025587 Chapter 1 Lecture Note

1-1 CHAPTER 1 ACCOUNTING IN BUSINESS © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025587 Chapter 1 Solution Manual Part 1

Chapter 1 Accounting in Business QUESTIONS 1. The purpose of accounting is to provide decision makers with relevant and reliable information to help them make better decisions. Examples include information for people making investments, loans, and business plans. 2. Technology […]

978-0078025587 Chapter 1 Solution Manual Part 2

Exercise 1-13 (20 minutes) a. Purchased land for $4,000 cash. b. Purchased $1,000 of office supplies on credit. c. Billed a client $1,900 for services provided. d. Paid the $1,000 account payable created by the credit purchase of office supplies […]

978-0078025587 Chapter 1 Solution Manual Part 3

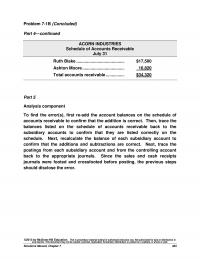

Problem 1-8A (Concluded) Part 3—continued Ander Electric Statement of Cash Flows For Month Ended December 31 Cash flows from operating activities Cash received from customers1 …………………………… $ 6,200 Cash paid for rent ……………………………………………….. (1,000) Cash paid for supplies ………………………………………… (800) […]

978-0078025587 Chapter 1 Solution Manual Part 4

©2013 by McGraw–Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

978-0078025587 Chapter 1 Solution Manual Part 5

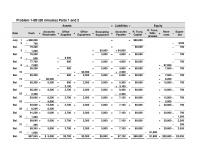

Title: Problem 1-5B QA_Ori: HalfLife Co. Statement of Cash Flows For Year Ended December 31, 2013 Cash used by operating activities ($3,000 ) Title: Problem 1-6B QA_Ori: ATV Company Statement of Owner’s Equity For Year Ended December 31, 2013 A.T. […]

978-0078025587 Chapter 1 Solution Manual Part 6

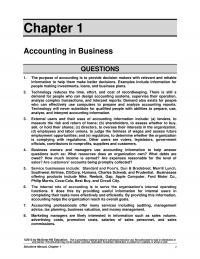

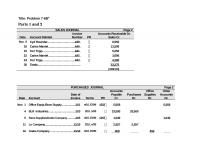

Title: Problem 1-8B QA_Ori: Parts 1 and 2 Assets = Liabilitie s + Equity Date Cash + Accounts Receivabl e +Office Supplies + Office Equipmen t + Excavatin g Equipmen t = Account s Payable +R. Truro, Capital – R. […]

978-0078025587 Chapter 1 Solution Manual Part 7

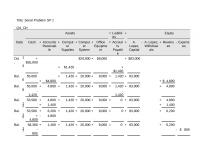

Title: Serial Problem SP 1 QA_Ori: Assets = Liabiliti es + Equity Date Cash + Accounts Receivab le + Comput er Supplies + Comput er System + Office Equipme nt = Accoun ts Payabl e + A. Lopez, Capital – […]

978-0078025587 Chapter 10 Excel

Student Name: Class: Estimated Market Percent Apportioned Value of Total Cost Building $508,800 53% $477,000 «- Correct! Land 297,600 31% 279,000 «- Correct! Land Improvements 28,800 3% 27,000 «- Correct! Vehicles 124,800 13% 117,000 «- Correct! Totals $960,000 100% $900,000 […]

978-0078025587 Chapter 10 Lecture Note

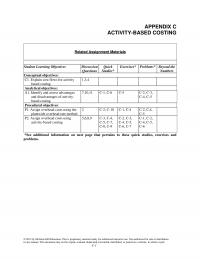

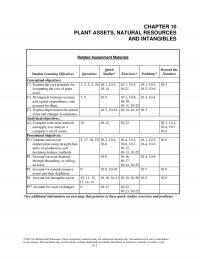

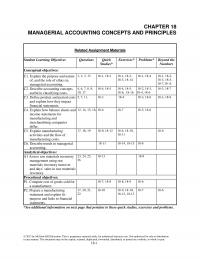

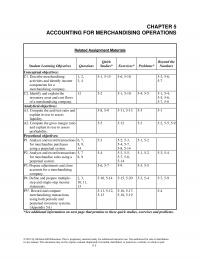

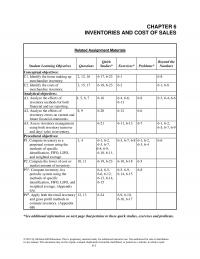

10-1 AND INTANGIBLES Related Assignment Materials Student Learning Objectives Questions Quick Studies* Exercises* Problems* Beyond the Numbers Conceptual objectives: C1. Explain the cost principle for computing the cost of plant asset. 1, 2, 3, 4, 20 10-1, 10-2, 10-14 10-1, […]

978-0078025587 Chapter 10 Solution Manual Part 1

Chapter 10 Plant Assets, Natural Resources, and Intangibles QUESTIONS 1. A plant asset is tangible; it is used in the production or sale of other assets or services; and it has a useful life longer than one accounting period. 2. […]

978-0078025587 Chapter 10 Solution Manual Part 2

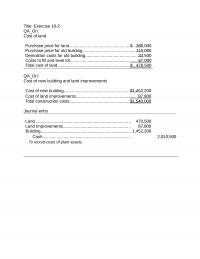

Title: Exercise 10-2 QA_Ori: Cost of land Purchase price for land……………………………………………………..$ 280,000 QA_Ori: Cost of new building and land improvements Cost of new building………………………………………………………….$1,452,200 Cost of land improvements……………………………………………….. 87,800 Total construction costs……………………………………………………..$1,540,000 Journal entry Land……………………………………………………………………… 470,500 Land Improvements………………………………………………… 87,800 Building…………………………………………………………………. […]

978-0078025587 Chapter 10 Solution Manual Part 2

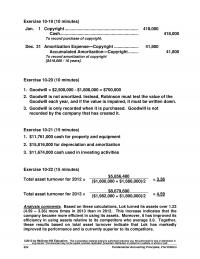

Exercise 10-19 (10 minutes) Jan. 1 Copyright ………………………………………………………. 418,000 Cash…………………………..……………………………..……. 418,000 To record purchase of copyright. Dec. 31 Amortization Expense—Copyright ………………………. 41,800 Accumulated Amortization—Copyright ……………. 41,800 To record amortization of copyright [$418,000 / 10 years]. Exercise 10-20 (10 minutes) 1. […]

978-0078025587 Chapter 10 Solution Manual Part 3

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

978-0078025587 Chapter 10 Solution Manual Part 4

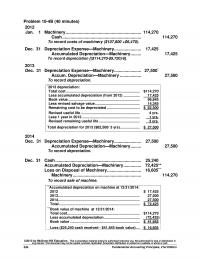

Title: Problem 10-8A QA_Ori: 1. 2013 (a) (b) July 1 Prepaid Rent…………………………………………………………80,000 Cash………………………………………………………………. 80,000 To record prepaid annual lease rental. (c) July 5 Leasehold Improvements………………………………………..130,000 Cash………………………………………………………………. 130,000 To record costs of leasehold improvements. 2. 2013 (a) Dec. 31 Rent Expense………………………………………………………..10,000 […]

978-0078025587 Chapter 10 Solution Manual Part 5

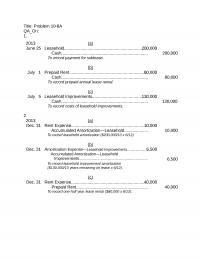

Title: Problem 10-8B 1. 2013 (a) Jan. 1 Leasehold……………………………………………………………..40,000 Cash………………………………………………………………. 40,000 To record payment for sublease. (b) Jan. 1 Prepaid Rent…………………………………………………………36,000 Cash………………………………………………………………. 36,000 To record prepaid annual lease rental. (c) Jan. 3 Leasehold Improvements………………………………………..20,000 Cash………………………………………………………………. 20,000 To record costs of […]

978-0078025587 Chapter 11 Excel

Student Name: Class: National Fargo Locust Bank Bank 1. May 19 Jul 8 Nov 28 90 120 60 Aug 17 Nov 5 Jan 27 Correct! Correct! Correct! $35,000 $80,000 $42,000 10% 9% 8% 90/360 120/360 60/360 2. Interest due at […]

978-0078025587 Chapter 11 Lecture Note

11–1 CHAPTER 11 CURRENT LIABILITIES AND PAYROLL ACCOUNTING © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025587 Chapter 11 Solution Manual Part 1

Chapter 11 Current Liabilities and Payroll Accounting QUESTIONS 1. A current liability is expected to be paid within one year or the company’s operating cycle, whichever is longer. Any liability that is not current is considered to be long term. […]

978-0078025587 Chapter 11 Solution Manual Part 2

Exercise 11-17 (concluded) (b) Aug 31 Salaries (or Wages) Expense ………………………….. 10,020.00 FICA—Social Sec. Taxes Payable ………….……. 298.84 FICA—Medicare Taxes Payable ……………..……. 145.29 Employee Fed. Inc. Taxes Payable ………………. 2,380.00 Employee State Inc. Taxes Payable ……….……. 388.00 Employee Benefits Plan […]

978-0078025587 Chapter 11 Solution Manual Part 3

Problem 11-2B (60 minutes) 1. Each employee’s FICA withholdings for Social Security Ahmed Carlos June Marie Total Maximum base ………… $110,100 $110,100 $110,100 $110,100 Earned through 9/23 … 108,500 36,650 6,650 22,200 Amount subject to tax $ 1,600 $ 73,450 […]

978-0078025587 Chapter 11 Solution Manual Part 4

Comprehensive Problem (Continued) Part 3 2013 (a) Miscellaneous Expenses …………………………………….. 15 Accounts Payable ……………………………………………….. 1,287 Interest Revenue ……………………………………………. 52 Cash ……………………………………………………………… 1,250 Adjust cash account. (Separate entries are acceptable.) (b1) Allowance for Doubtful Accounts …………………………. 679 Accounts Receivable ……………………………………… 679 […]

978-0078025587 Chapter 11 Solution Manual Part 5

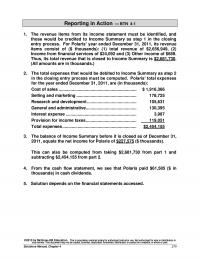

Title: Reporting in Action 1 QA_Ori: Times interest earned ($ thousands) 2011 2010 2009 Net income $227,575 $147,138 $101,017 Times interest earned ratio 87.9a82.5b37.8c a$350,613/$3,987 b$221,221/$2,680 c$155,285/$4,111 Analysis comment : For each of these fiscal years, it is obvious that […]

978-0078025587 Chapter 12 Excel

Student Name: Class: Plans a and c 40% «- Correct! 60% «- Correct! Plan b 33.33% «- Correct! 66.67% «- Correct! Plans c and d 72,000$ «- Correct! Plan d 4,200$ «- Correct! 6,300 «- Correct! Income (Loss) Year 1 […]

978-0078025587 Chapter 12 Lecture Note

12-1 CHAPTER 12 ACCOUNTING FOR PARTNERSHIPS © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025587 Chapter 12 Solution Manual Part 1

Title: Question 1 QA_Ori: Under the circumstances described, the death, bankruptcy, or legal inability of a partner to execute a contract ends a partnership. In addition, if a partnership is Title: Question 2 QA_Ori: Mutual agency means that each partner […]

978-0078025587 Chapter 12 Solution Manual Part 1

Chapter 12 Accounting for Partnerships QUESTIONS 1. Under the circumstances described, the death, bankruptcy, or legal inability of a partner to execute a contract ends a partnership. In addition, if a partnership is organized for the purpose of completing a […]

978-0078025587 Chapter 12 Solution Manual Part 2

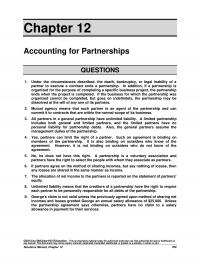

Title: Exercise 12-11 QA_Ori: a. Loss from selling assets Total book value of assets $126,000 b. Loss and deficit allocation Turner Roth Lowe Total Capital balances before loss $ 2,500 $ 14,000 $ 31,500 $ 48,000 Allocation of loss $76,000 […]

978-0078025587 Chapter 12 Solution Manual Part 2

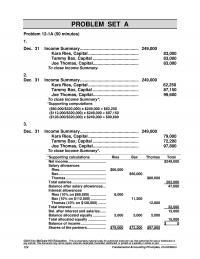

PROBLEM SET A Problem 12-1A (50 minutes) 1. Dec. 31 Income Summary …………………………………………..… 249,000 Kara Ries, Capital …………………………………….… 83,000 Tammy Bax, Capital …………………………………… 83,000 Joe Thomas, Capital …………………………………… 83,000 To close Income Summary. 2. Dec. 31 Income Summary …………………………………………..… 249,000 […]

978-0078025587 Chapter 12 Solution Manual Part 3

Title: Problem 12-5A QA_Ori: Note: All entries in this problem are dated May 31. 1. (a) Cash 600,000 (b) Gain on Sale of Inventory 62,800 Kendra, Capital ($62,800 x 3/6) 31,400 Cogley, Capital ($62,800 x 2/6) 20,933 Mei, Capital ($62,800 […]

978-0078025587 Chapter 12 Solution Manual Part 3

Problem 12-4B (50 minutes) Part 1 a) Apr. 30 Gibbs, Capital ………………………………………………….. 606,000 Brady, Capital …………………………………………….. 606,000 To record admission of Brady. b) Apr. 30 Gibbs, Capital ………………………………………………….. 606,000 Cannon, Capital…………………………………………… 606,000 To record admission of Cannon. c) Apr. 30 […]

978-0078025587 Chapter 12 Solution Manual Part 4

Title: Problem 12-5B QA_Ori: Note: All entries in this problem are dated Jan. 18. 1. (a) Cash 650,000 (b) Gain on Sale of Equipment 32,800 Lasure, Capital ($32,800 x 2/5) 13,120 Ramirez, Capital ($32,800 x 1/5) 6,560 Toney, Capital ($32,800 […]

978-0078025587 Chapter 13 Lecture Note Part 1

13-1 CHAPTER 13 ACCOUNTING FOR CORPORATIONS Related Assignment Materials Student Learning Objectives Questions Quick Studies* Exercises* Problems* Beyond the Numbers Conceptual objectives: C1. Identify characteristics of corporations and their organization. 1, 2, 3, 4 13-1 13-1 C2. Explain characteristics of, […]

978-0078025587 Chapter 13 Lecture Note Part 2

13–10 Chapter Outline Notes B. Reissuing Treasury Stock 1. Sale at cost—Treasury stock is reduced (credited) for the cost of the reissued shares and Cash is debited for the amount received. 2. Sale above cost—the amount received in excess of […]

978-0078025587 Chapter 13 Solution Manual Part 1

Title: Question 1 QA_Ori: Organization expenses (costs) are incurred in creating a corporation. Title: Question 2 QA_Ori: Organization expenses (costs) are reported as expenses when incurred —as part of operating expenses—because the amount and timing of their future benefit is […]

978-0078025587 Chapter 13 Solution Manual Part 1

Chapter 13 Accounting for Corporations QUESTIONS 1. Organization expenses (costs) are incurred in creating a corporation. Examples include: legal fees, promoter fees, accountant fees, costs of printing stock certificates, and fees paid to obtain a state charter. 2. Organization expenses […]

978-0078025587 Chapter 13 Solution Manual Part 2

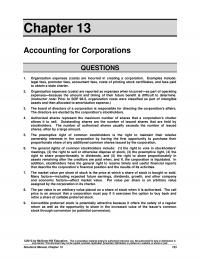

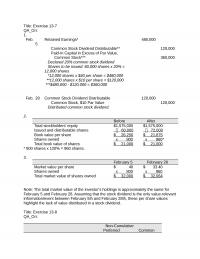

Title: Exercise 13-7 QA_Ori: 1. Feb. 5 Retained Earnings* 480,000 Common Stock Dividend Distributable** 120,000 Paid-In Capital in Excess of Par Value, Feb. 28 Common Stock Dividend Distributable 120,000 Common Stock, $10 Par Value 120,000 Distributed common stock dividend. 2. […]

978-0078025587 Chapter 13 Solution Manual Part 2

Exercise 13-10 (25 minutes) 1. (a) Oct. 11 Treasury Stock (5,000 x $25) ………………………….. 125,000 Cash ……………………………………………………………….. 125,000 Purchased treasury stock. (b) Nov. 1 Cash (1,000 x $31) ………………………………………….…….. 31,000 Treasury Stock (1,000 x $25) ……………………..…… 25,000 Paid-In Capital, Treasury […]

978-0078025587 Chapter 13 Solution Manual Part 3

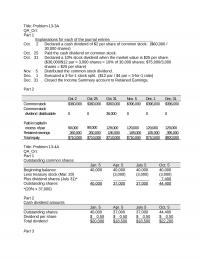

Title: Problem 13-3A QA_Ori: Part 1 Explanations for each of the journal entries Oct. 2 Declared a cash dividend of $2 per share of common stock. ($60,000 / 30,000 shares) Part 2 Oct. 2 Oct. 25 Oct. 31 Nov. 5 […]

978-0078025587 Chapter 13 Solution Manual Part 3

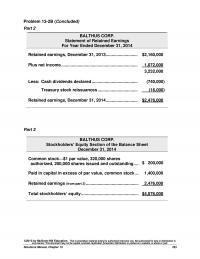

Problem 13-2B (Concluded) Part 2 BALTHUS CORP. Statement of Retained Earnings For Year Ended December 31, 2014 Retained earnings, December 31, 2013 ………………………. $2,160,000 Plus net income ………………………………………………………… 1,072,000 3,232,000 Less: Cash dividends declared …………………………………. (740,000) Treasury stock reissuances …………………………….. […]

978-0078025587 Chapter 13 Solution Manual Part 4

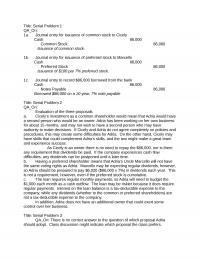

Title: Serial Problem 1 QA_Ori: 1a. Journal entry for issuance of common stock to Cicely 1b. Journal entry for issuance of preferred stock to Marcello Cash 86,000 Preferred Stock 86,000 Issuance of $100 par 7% preferred stock. 1c. Journal entry […]

978-0078025587 Chapter 14 Excel

Student Name: Class: Part 1. Date Account Titles Debit Credit 2013 Jan 1 3,456,448 543,552 «- Correct! 4,000,000 Part 2. 120,000$ «- Correct! 18,118 «- Correct! 138,118 «- Correct! Part 3. 3,600,000$ 4,000,000 7,600,000$ (3,456,448) 4,143,552$ «- Correct! 3,600,000$ 543,552 […]

978-0078025587 Chapter 14 Lecture Note Part 1

14-1 Chapter 14 Long-Term Liabilities Student Learning Objectives and Related Assignment Materials* Student Learning Objectives Discussion Questions Quick Studies Exercises Problems Beyond the Numbers Conceptual objectives: C1. Explain the types and payment patterns of notes. 1, 12 14-8 14-14 14-9 […]

978-0078025587 Chapter 14 Lecture Note Part 2

14–10 Chapter Outline Notes 3. Present value of an annuity of $1 table is used to compute present value of a series of equal payments (annuity). C. Applying a Present Value Table (Complete tables in Appendix B) 1. Determine the […]

978-0078025587 Chapter 14 Solution Manual Part 1

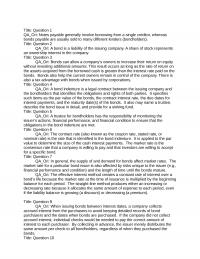

Title: Question 1 QA_Ori: Notes payable generally involve borrowing from a single creditor, whereas Title: Question 2 QA_Ori: A bond is a liability of the issuing company. A share of stock represents an ownership interest in the company. Title: Question […]

978-0078025587 Chapter 14 Solution Manual Part 1

Chapter 14 Long-Term Liabilities QUESTIONS 1. Notes payable generally involve borrowing from a single creditor, whereas bonds payable are usually sold to many different lenders (bondholders). 2. A bond is a liability of the issuing company. A share of stock […]

978-0078025587 Chapter 14 Solution Manual Part 2

Title: Exercise 14-5 QA_Ori: 1. Premium = Issue price – Par value = $409,850 – $400,000 = $9,850 2. Total bond interest expense over the life of the bonds Amount repaid Six payments of $26,000* $ 156,000 Par value at […]

978-0078025587 Chapter 14 Solution Manual Part 2

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

978-0078025587 Chapter 14 Solution Manual Part 3

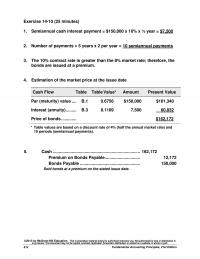

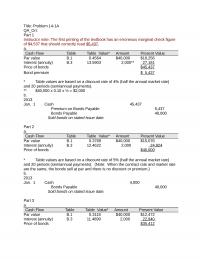

Title: Problem 14-1A QA_Ori: Part 1 Instructor note: The first printing of the textbook has an erroneous marginal check figure of $4,537 that should correctly read $5,437. a. Cash Flow Table Table Value* Amount Present Value Par value B.1 0.4564 […]

978-0078025587 Chapter 14 Solution Manual Part 3

Problem 14-5AB (45 minutes) Part 1 Ten payments of $8,125* ……………….…….. $ 81,250 Par value at maturity ……………………..…… 250,000 Total repaid ………………………………………….. 331,250 Less amount borrowed ………………….…….. (255,333) Total bond interest expense …………..…….. $ 75,917 *$250,000 x 0.065 x ½ […]

978-0078025587 Chapter 14 Solution Manual Part 4

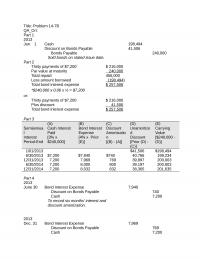

Title: Problem 14-8A QA_Ori: Part 1 2013 Jan. 1 Cash 184,566 Part 2 Six payments of $9,900 $ 59,400 Par value at maturity 180,000 Total repaid 239,400 Less amount borrowed (184,566) Total bond interest expense $ 54,834 *$180,000 x 0.11 […]

978-0078025587 Chapter 14 Solution Manual Part 4

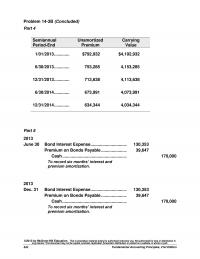

Fundamental Accounting Principles, 21st Edition 842 Problem 14-3B (Concluded) Part 4 Semiannual Period-End Unamortized Premium Carrying Value 1/01/2013 ………….…….. $792,932 $4,192,932 6/30/2013 ………….…….. 753,285 4,153,285 12/31/2013 ………….…….. 713,638 4,113,638 6/30/2014 ………….…….. 673,991 4,073,991 12/31/2014 ………….…….. 634,344 4,034,344 Part 5 2013 […]

978-0078025587 Chapter 14 Solution Manual Part 5

Title: Problem 14-7B QA_Ori: Part 1 2013 Jan. 1 Cash 198,494 Part 2 Thirty payments of $7,200*$ 216,000 Par value at maturity 240,000 Total repaid 456,000 Less amount borrowed (198,494) Total bond interest expense $ 257,506 *$240,000 x 0.06 x […]

978-0078025587 Chapter 14 Solution Manual Part 5

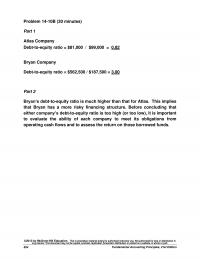

Fundamental Accounting Principles, 21st Edition 854 Problem 14-10B (30 minutes) Part 1 Atlas Company Debt–to-equity ratio = $81,000 / $99,000 = 0.82 Bryan Company Debt–to-equity ratio = $562,500 / $187,500 = 3.00 Part 2 Bryan’s debt–to-equity ratio is much higher […]

978-0078025587 Chapter 15 Lecture Note

15-1 INTERNATIONAL OPERATIONS Related Assignment Materials Student Learning Objectives Questions Quick Studies* Exercises* Problems* Beyond the Numbers Conceptual objectives: C1. Distinguish between debt and equity securities and between long-term investments and short-term investments. 1, 2, 5 15-5, 15-6 15-4, 15-12 […]

978-0078025587 Chapter 15 Solution Manual Part 1

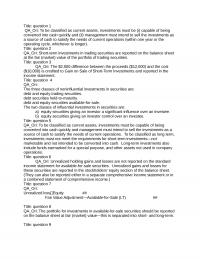

Title: question 1 QA_Ori: To be classified as current assets, investments must be (i) capable of being converted into cash quickly and (ii) management must intend to sell the investments as Title: question 2 QA_Ori: Short-term investments in trading securities […]

978-0078025587 Chapter 15 Solution Manual Part 1

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

978-0078025587 Chapter 15 Solution Manual Part 2

Title: Exercise 15-8 QA_Ori: 2013 (a) Feb. 15 Short-Term Investments—HTM (A.G.) 160,000 (b) Mar. 22 Long-Term Investments—AFS (Fran) 35,850 Cash 35,850 Purchased 700 shares of Fran common stock ([700 x $51] + $150). (c) May 15 Cash 164,000 Short-Term Investments—HTM […]

978-0078025587 Chapter 15 Solution Manual Part 2

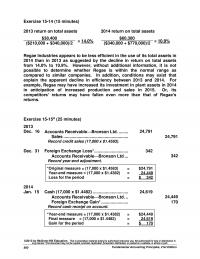

Fundamental Accounting Principles, 21st Edition 880 Exercise 15-14 (15 minutes) 2013 return on total assets 2014 return on total assets = 14.0% = 10.9% $38,400 $60,300 Regae Industries appears to be less efficient in the use of its total assets […]

978-0078025587 Chapter 15 Solution Manual Part 3

Title: Problem 15-3A QA_Ori: Part 1 2013 Jan. 20 Long-Term Investments—AFS (J&J) 20,740 Feb. 9 Long-Term Investments—AFS (Sony) 55,665 Cash 55,665 Purchased Sony shares [(1,200 x $46.20) + $225]. June 12 Long-Term Investments—AFS (Mattel) 40,695 Cash 40,695 Purchased Mattel shares […]

978-0078025587 Chapter 15 Solution Manual Part 3

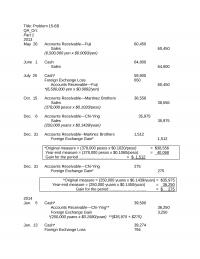

Problem 15-6AA (60 minutes) Part 1 2013 Apr. 8 Cash …………………………………………………………..…………………. 5,938 Sales …………………………………………………….… 5,938 July 21 Accounts Receivable⎯Sumito …………………….……. 14,100 Sales …………………………………………………….… 14,100 (1,500,000 yen x $0.0094/yen) Oct. 14 Accounts Receivable⎯Smithers ………………………….. 27,675 Sales …………………………………………………….… 27,675 (19,000£ x $1.4566/£) […]

978-0078025587 Chapter 15 Solution Manual Part 4

Title: Problem 15-1B QA_Ori: Part 1 2013 Mar. 10 Short-Term Investments—Trading (AOL) 143,505 May 7 Short-Term Investments—Trading (MTV) 184,105 Cash 184,105 Purchased MTV shares [(5,000 x $36.25) + $2,855]. Sept. 1 Short-Term Investments—Trading (UPS) 69,950 Cash 69,950 Purchased UPS shares […]

978-0078025587 Chapter 15 Solution Manual Part 4

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

978-0078025587 Chapter 15 Solution Manual Part 5

Title: Problem 15-6B QA_Ori: Part 1 2013 May 26 Accounts Receivable—Fuji 60,450 Sales 60,450 (6,500,000 yen x $0.0093/yen) June 1 Cash 64,800 Sales 64,800 July 25 Cash* 59,800 Foreign Exchange Loss 650 Accounts Receivable—Fuji 60,450 *(6,500,000 yen x $0.0092/yen) Oct. […]

978-0078025587 Chapter 16 Excel

Student Name: Class: 136,000$ (12,000) (75,000) 16,000 3,000 54,000 122,000$ «- Correct! (36,000) «- Correct! 60,000 (89,000) (29,000) «- Correct! 57,000$ «- Correct! 107,000 «- Correct! 164,000$ «- Correct! Net cash provided by operating activities Cash flows from investing activities: […]

978-0078025587 Chapter 16 Lecture Note Part 1

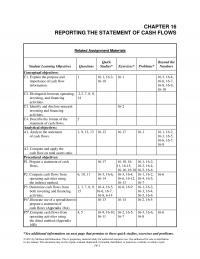

16-1 CHAPTER 16 REPORTING THE STATEMENT OF CASH FLOWS Related Assignment Materials Student Learning Objectives Questions Quick Studies* Exercises* Problems* Beyond the Numbers Conceptual objectives: C1. Explain the purpose and importance of cash flow information. 1 16-1, 16-2, 16-18 16-1 […]

978-0078025587 Chapter 16 Lecture Note Part 2

16–10 VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to • Customers for cash sales • Collections on credit sales • Borrowers for interest • Dividends received • Lawsuit settlements • […]

978-0078025587 Chapter 16 Solution Manual Part 1

Title: Question 1 QA_Ori: The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users to answer questions such as: How does a company obtain its […]

978-0078025587 Chapter 16 Solution Manual Part 1

Chapter 16 Reporting the Statement of Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users to answer questions such as: […]

978-0078025587 Chapter 16 Solution Manual Part 2

Title: Quick Study 16-18 QA_Ori: 2. IFRS and US GAAP differ on the classification of the following cash flows as operating, investing or financing: Cash flow source U.S. GAAP IFRS _ a. Interest paid Operating Financing or Operating b. Dividends […]

978-0078025587 Chapter 16 Solution Manual Part 2

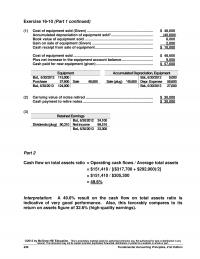

Fundamental Accounting Principles, 21st Edition 936 Exercise 16-10 (Part 1 continued) (1) Cost of equipment sold (Given) ………………………………………………………..… $ 48,600 Accumulated depreciation of equipment sold* …………………………………..… (40,600) Book value of equipment sold ………………………………………………………….… 8,000 Gain on sale of equipment (Given) […]

978-0078025587 Chapter 16 Solution Manual Part 3

Title: Exercise 16-11B QA_Ori: IKIBAN, INC. Statement of Cash Flows (Direct Method) For Year Ended June 30, 2013 Cash flows from operating activities Cash received from customers (Note 1)…………… $664,000 Cash paid for merchandise (Note 2)………………… (393,300) (See notes on […]

978-0078025587 Chapter 16 Solution Manual Part 3

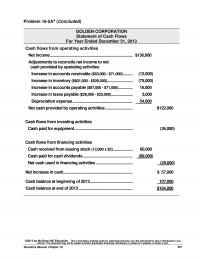

Problem 16-5AA (Concluded) GOLDEN CORPORATION Statement of Cash Flows For Year Ended December 31, 2013 Cash flows from operating activities Net income ……………………………………………………………………….. $136,000 Adjustments to reconcile net income to net cash provided by operating activities Increase in accounts receivable […]

978-0078025587 Chapter 16 Solution Manual Part 4

Title: Problem 16-1A QA_Ori: Part 1 FORTEN COMPANY Statement of Cash Flows For Year Ended December 31, 2013 Cash flows from operating activities Net income……………………………………………………………………..$114,975 Adjustments to reconcile net income to net Cash flows from investing activities Cash received from […]

978-0078025587 Chapter 16 Solution Manual Part 4

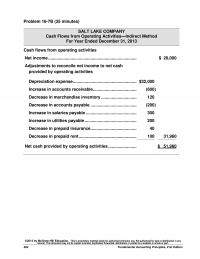

Fundamental Accounting Principles, 21st Edition 964 Problem 16-7B (35 minutes) SALT LAKE COMPANY Cash Flows from Operating Activities—Indirect Method For Year Ended December 31, 2013 Cash flows from operating activities Net income ………………………………………………………………….… $ 20,000 Adjustments to reconcile net income […]

978-0078025587 Chapter 16 Solution Manual Part 5

Title: Problem 16-1B QA_Ori: Part 1 GAZELLE CORPORATION Statement of Cash Flows For Year Ended December 31, 2013 Cash flows from operating activities Net income……………………………………………………………………..$158,100 Adjustments to reconcile net income to net cash provided by operating activities Cash flows from […]

978-0078025587 Chapter 16 Solution Manual Part 6

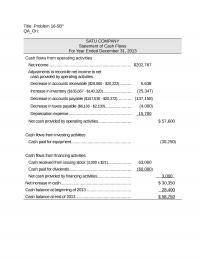

Title: Problem 16-5BA QA_Ori: SATU COMPANY Statement of Cash Flows For Year Ended December 31, 2013 Cash flows from operating activities Net income……………………………………………………………. $202,767 Adjustments to reconcile net income to net cash provided by operating activities Cash flows from investing […]

978-0078025587 Chapter 16 Solution Manual Part 7

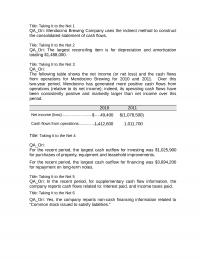

Title: Taking It to the Net 1 QA_Ori: Mendocino Brewing Company uses the indirect method to construct the consolidated statement of cash flows. Title: Taking It to the Net 2 QA_Ori: The largest reconciling item is for depreciation and amortization […]

978-0078025587 Chapter 17 Excel

Student Name: Class: Assets Liabilities Ratio 52,390$ 22,800$ 2.3 «- Correct! 37,924 19,960 1.9 «- Correct! 51,748 20,300 2.5 «- Correct! 2014 2013 2012 100.00% 100.00% 100.00% 51.08% 62.50% 55.36% 48.92% 37.50% 44.64% 18.54% 13.80% 18.27% 9.13% 8.80% 8.20% 27.67% […]

978-0078025587 Chapter 17 Lecture Note

17–1 CHAPTER 17 ANALYSIS OF FINANCIAL STATEMENTS © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, […]

978-0078025587 Chapter 17 Solution Manual Part 1

Title: Question 1 QA_Ori: Financial reporting includes the entire process of preparing and issuing financial Title: Question 2 QA_Ori: With comparative statements, financial statement items for two or more successive accounting periods are placed side by side on a single […]

978-0078025587 Chapter 17 Solution Manual Part 1

Chapter 17 Analysis of Financial Statements QUESTIONS 1. Financial reporting includes the entire process of preparing and issuing financial information about a company. Financial statements are an important part of financial reporting but they are less than the whole. 2. […]

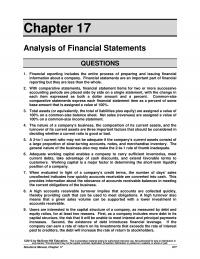

978-0078025587 Chapter 17 Solution Manual Part 2

Title: Exercise 17-7 QA_Ori: Simon Company Common-Size Comparative Balance Sheets December 31, 2012-2014 At December 31 2014 2013*2012 Assets Cash………………………………………………………….. 6.1% 8.0% 10.0% Liabilities and Equity Accounts payable………………………………………… 24.8% 16.9% 13.6% Long-term notes payable secured by mortgages on plant assets […]

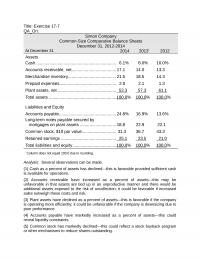

978-0078025587 Chapter 17 Solution Manual Part 2

Fundamental Accounting Principles, 21st Edition 992 Exercise 17-14 (15 minutes) RANDA MERCHANDISING, INC. Income Statement For Year Ended December 31, 2013 Net sales ……………………………………………………………….. $2,900,000 Expenses Cost of goods sold ……………………………………………… $1,480,000 Salaries expense ………………………………………………… 640,000 Depreciation expense …………………………………………. 232,500 […]

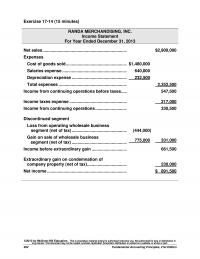

978-0078025587 Chapter 17 Solution Manual Part 3

Title: Problem 17-2A QA_Ori: Part 1 HAROUN COMPANY Income Statement Trends For Years Ended December 31, 2014-2008 2014 2013 2012 2011 2010 2009 2008 Sales……………………………….. 182.5% 161.2% 147.6% 136.2% 127.8% 119.6% 100.0% HAROUN COMPANY Balance Sheet Trends December 31, 2014-2008 […]

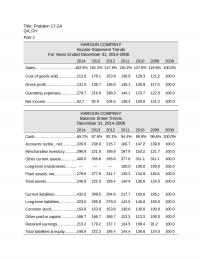

978-0078025587 Chapter 17 Solution Manual Part 3

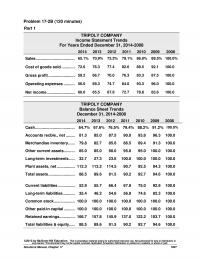

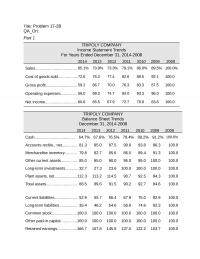

Problem 17-2B (120 minutes) Part 1 TRIPOLY COMPANY Income Statement Trends For Years Ended December 31, 2014-2008 2014 2013 2012 2011 2010 2009 2008 Sales ………………………………. 65.1% 70.9% 73.3% 79.1% 86.0% 89.5% 100.0% Cost of goods sold ………….. 72.6 76.3 […]

978-0078025587 Chapter 17 Solution Manual Part 4

Title: Problem 17-2B QA_Ori: Part 1 TRIPOLY COMPANY Income Statement Trends For Years Ended December 31, 2014-2008 2014 2013 2012 2011 2010 2009 2008 Sales……………………………….. 65.1% 70.9% 73.3% 79.1% 86.0% 89.5% 100.0% TRIPOLY COMPANY Balance Sheet Trends December 31, 2014-2008 […]

978-0078025587 Chapter 17 Solution Manual Part 4

SERIAL PROBLEM — SP 17 Serial Problem — SP 17, Success Systems (45 minutes) 1. Gross margin with services revenue Gross margin = Total revenue – Cost of goods sold = $43,853 – $14,052 = $29,801 Gross margin ratio = […]

978-0078025587 Chapter 17 Solution Manual Part 5

Title: Serial Problem 2 QA_Ori: Current ratio = $105,209 / $875 = 120.2 Acid-test ratio = $100,205 / $875 = 114.5 QA_Edit: Title: Serial Problem 3 QA_Ori: Debt ratio = $875 / $129,909 = 0.7% Equity ratio = $129,034/$129,909 = […]

978-0078025587 Chapter 18 Excel

Student Name: Class: Merchandising Business 200,000$ 300,000 500,000 175,000 325,000$ Correct! Manufacturing Business Partial Income Statement SNO-BOARD MANUFACTURING 500,000$ 875,000 1,375,000 225,000 1,150,000$ Correct! Part 2 To: Memorandum From: Date: Subject: Problem 18-06A McGraw-Hill/Irwin Instructor For Year Ended December 31, […]

978-0078025587 Chapter 18 Lecture Note

18-1 CHAPTER 18 MANAGERIAL ACCOUNTING CONCEPTS AND PRINCIPLES © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025587 Chapter 18 Solution Manual Part 1

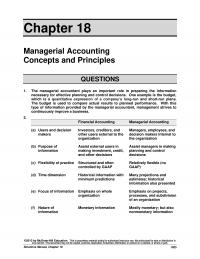

Title: Question 1 QA_Ori: The managerial accountant plays an important role in preparing the information necessary for effective planning and control decisions. One example is the budget, which Title: Question 2 QA_Ori: Financial Accounting Managerial Accounting (a) Users and decision […]

978-0078025587 Chapter 18 Solution Manual Part 1

Chapter 18 Managerial Accounting Concepts and Principles QUESTIONS 1. The managerial accountant plays an important role in preparing the information necessary for effective planning and control decisions. One example is the budget, which is a quantitative expression of a company’s […]

978-0078025587 Chapter 18 Solution Manual Part 2

Title: Exercise 18-5 QA_Ori: 1. Cost by Behavior Cost by Traceability Product Cost Variable Fixed Direct Indirect 1. Leather cover for soccer balls…………….. X X 2. Annual flat fee paid for office security…………………………………………. X X 2. Most fixed costs are […]

978-0078025587 Chapter 18 Solution Manual Part 2

Fundamental Accounting Principles, 21st Edition 1040 Exercise 18-11 (25 minutes) Account Balance Sheet Income Statement Manufacturing Statement Overhead Report Accounts receivable ………………………. ✓ Computer supplies used in office ……. ✓ Beginning finished goods inventory ✓ Beginning goods in process inventory […]

978-0078025587 Chapter 18 Solution Manual Part 3

Title: Exercise 18-15 QA_Ori: a. b. If customers rate any of the factors on the survey as anything other than “very satisfied,” managers should investigate the reasons for the customer’s lack of satisfaction. The survey itself does not identify the […]

978-0078025587 Chapter 18 Solution Manual Part 3

PROBLEM SET B Problem 18-1B (20 minutes) The managerial accounting professional must do more than assign value to ending inventory and cost of goods sold. S/he must understand the industry and the current business environment of the company. The managerial […]

978-0078025587 Chapter 18 Solution Manual Part 4

Part 2 DE LEON COMPANY Income Statement For Year Ended December 31, 2013 Sales…………………………………………………………………….. $4,525,000 167,350 Cost of goods manufactured…………………………………… 1,935,65 0 Goods available for sale…………………………………………2,103,000 Less finished goods inventory, December 31, 2013………… 136,49 0 Cost of goods sold………………………………………………… 1,966,510 […]

978-0078025587 Chapter 18 Solution Manual Part 4

Fundamental Accounting Principles, 21st Edition 1066 SERIAL PROBLEM — SP 18 Serial Problem, Success Systems (50 minutes) 1. Cost by Behavior . Cost by Traceability . Product Costs Variable Fixed Direct Indirect 1. Monthly flat fee to clean workshop …….. […]

978-0078025587 Chapter 18 Solution Manual Part 5

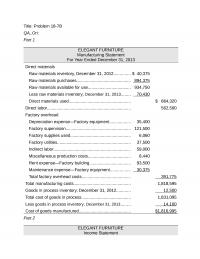

Title: Problem 18-7B QA_Ori: Part 1 ELEGANT FURNITURE Manufacturing Statement For Year Ended December 31, 2013 Direct materials Raw materials inventory, December 31, 2012………….. $ 40,375 Direct labor…………………………………………………………….. 562,500 Factory overhead Depreciation expense—Factory equipment……………… 35,400 Factory supervision………………………………………………. 121,500 Factory supplies […]

978-0078025587 Chapter 18 Solution Manual Part 6

Title: Ethics Challenge 1 QA_Ori: Raw materials are part of inventory and should be capitalized (set up as assets). Their costs are subsequently reported as part of cost of goods Title: Ethics Challenge 2 QA_Ori: The challenge is how to […]

978-0078025587 Chapter 19 Excel

Student Name: Class: 1,500,000 «- Correct! 2,500,000 «- Correct! 60% «- Correct! b. Overhead costs charged to jobs: Direct Applied Labor Overhead 604,000$ 362,400$ «- Correct! 563,000 337,800 «- Correct! 298,000 178,800 «- Correct! 716,000 429,600 «- Correct! 314,000 188,400 […]

978-0078025587 Chapter 19 Lecture Note

19-1 CHAPTER 19 JOB ORDER COST ACCOUNTING © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, […]

978-0078025587 Chapter 19 Solution Manual Part 1

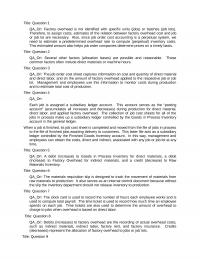

Title: Question 1 QA_Ori: Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between factory overhead cost and job Title: Question 2 QA_Ori: Several other factors (allocation bases) […]

978-0078025587 Chapter 19 Solution Manual Part 1

Chapter 19 Job Order Cost Accounting QUESTIONS 1. Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between factory overhead cost and job or job lot are necessary. […]

978-0078025587 Chapter 19 Solution Manual Part 2

Title: Exercise 19-8 QA_Ori: 1. Raw Materials Inventory……………………………………………210,000 Cash………………………………………………………………… 210,000 To record materials purchases. Title: Exercise 19-9 QA_Ori: 1. Factory Payroll………………………………………………………..345,000 Cash………………………………………………………………… 345,000 To record factory payroll. 2. Goods in Process Inventory………………………………………265,000 Factory Payroll………………………………………………….. 265,000 To assign direct labor to […]

978-0078025587 Chapter 19 Solution Manual Part 2

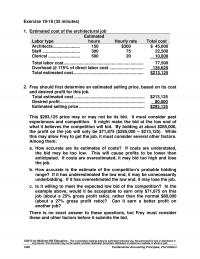

1092 Fundamental Accounting Principles, 21st Edition Exercise 19-18 (35 minutes) 1. Estimated cost of the architectural job Labor type Estimated hours Hourly rate Total cost Architects ………………………….. 150 $300 $ 45,000 Staff ………………………….. 300 75 22,500 Clerical ……………………….…. 500 20 […]

978-0078025587 Chapter 19 Solution Manual Part 3

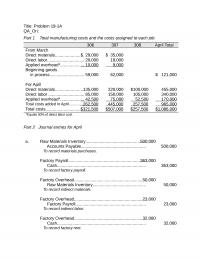

Title: Problem 19-1A QA_Ori: Part 1 Total manufacturing costs and the costs assigned to each job 306 307 308 April Total From March Direct materials……………………$ 29,000 $ 35,000 Direct labor…………………………. 20,000 18,000 *Equals 50% of direct labor cost. Part 2 […]

978-0078025587 Chapter 19 Solution Manual Part 3

Problem 19-5A (Continued) GENERAL JOURNAL a. Raw Materials Inventory ……………………………………….. 78,700 Accounts Payable ………………………………………..….. 78,700 To record materials purchases ($62,500+$16,200). d. Factory Payroll ………………………………………………….….. 174,250 Cash ……………………………………………………………….. 174,250 To record factory payroll. Factory Overhead ……………………………………………..….. 102,000 Cash ……………………………………………………………….. 102,000 To […]

978-0078025587 Chapter 19 Solution Manual Part 4

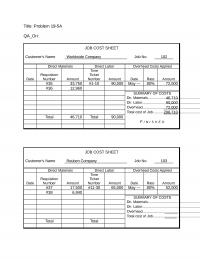

Title: Problem 19-5A QA_Ori: JOB COST SHEET Customer’s Name Worldwide Company Job No. 102 Direct Materials Direct Labor Overhead Costs Applied Date Requisition Number Amount Time Ticket Number Amount Date Rate Amount #35 33,750 #1-10 90,000 May — 80% 72,000 […]

978-0078025587 Chapter 19 Solution Manual Part 4

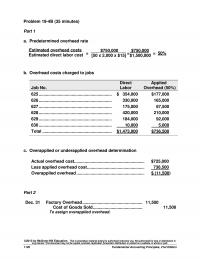

1120 Fundamental Accounting Principles, 21st Edition Problem 19-4B (35 minutes) Part 1 a. Predetermined overhead rate = = = 50% Estimated overhead costs $750,000 $750,000 b. Overhead costs charged to jobs Direct Applied Job No. Labor Overhead (50%) 625 ………………………………………………………. […]

978-0078025587 Chapter 19 Solution Manual Part 5

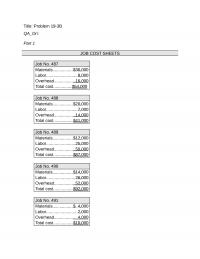

Title: Problem 19-3B QA_Ori: Part 1 JOB COST SHEETS Job No. 487 Materials…………………….$30,000 Job No. 488 Materials…………………….$20,000 Labor………………………… 7,000 Overhead…………………… 14,000 Total cost……………………$41,000 Job No. 489 Materials…………………….$12,000 Labor………………………… 25,000 Overhead…………………… 50,000 Total cost……………………$87,000 Job No. 490 Materials…………………….$14,000 Labor………………………… 26,000 Overhead…………………… […]

978-0078025587 Chapter 19 Solution Manual Part 6

Title: Reporting in Action 1 QA_Ori: We would anticipate that at least two types of costs will increase as a percent of sales with Polaris’s growth in domestic sales. The first type is broadly QA_Edit: Title: Reporting in Action 2 […]

978-0078025587 Chapter 2 Excel

Student Name: Class: Date Explanation Debit Credit Mar 1 150,000 22,000 172,000 «- Correct! 6,000 «- Correct! 33,000 Office Equipment 1,200 4,200 «- Correct! 64,000 Cash 4,000 «- Correct! 97,500 Accounts Receivable 7,500 «- Correct! 12 4,200 Accounts Payable 4,200 […]

978-0078025587 Chapter 2 Lecture Note

2-1 CHAPTER 2 ANALYZING AND RECORDING TRANSACTIONS © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, […]

978-0078025587 Chapter 2 Solution Manual Part 1

Title: Question 1 QA_Ori: a. Common asset accounts: cash, accounts receivable, notes receivable, Title: Question 2 QA_Ori: A note payable is formal promise, usually denoted by signing a promissory note to pay a future amount. A note payable can be […]

978-0078025587 Chapter 2 Solution Manual Part 1

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies, equipment, building, and land. b. Common liability accounts: accounts payable, notes payable, and unearned […]

978-0078025587 Chapter 2 Solution Manual Part 2

Title: Exercise 2-8 QA_Ori: Cash Photography Equipment Aug. 1 6,500 Aug. 2 2,100 Aug. 1 33,50 0 Office Supplies Photography Fees Earned Aug. 5 880 Aug. 20 3,331 Prepaid Insurance Utilities Expense Aug. 2 2,100 Aug. 31 675 POSE-FOR-PICS Trial […]

978-0078025587 Chapter 2 Solution Manual Part 2

Exercise 2-17 (15 minutes) (a) (b) (c) (d) Answers $(28,000) $42,000 $73,000 $(45,000) Computations: Equity, Dec. 31, 2012 ………….. $ 0 $ 0 $ 0 $ 0 Owner’s investments …..…….. 110,000 42,000 87,000 210,000 Owner’s withdrawals ………….. (28,000) (47,000) (10,000) […]

978-0078025587 Chapter 2 Solution Manual Part 3

Title: Exercise 2-22 QA_Ori: a. Co. Liabilities / Assets = Debt Ratio Net Income / Average Assets = ROA 1 $11,765 $ 90,500 0.13 $20,000 $100,000 0.200 2 46,720 64,000 0.73 3,800 40,000 0.095 Title: Exercise 2-23 QA_Ori: BMW Balance […]

978-0078025587 Chapter 2 Solution Manual Part 3

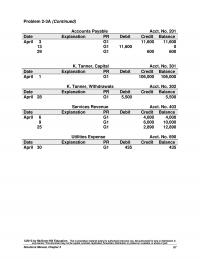

Problem 2-3A (Continued) Accounts Payable Acct. No. 201 Date Explanation PR Debit Credit Balance April 3 G1 11,600 11,600 13 G1 11,600 0 29 G1 600 600 K. Tanner, Capital Acct. No. 301 Date Explanation PR Debit Credit Balance April […]

978-0078025587 Chapter 2 Solution Manual Part 4

Title: Problem 2-3A QA_Ori: Part 1 1-Apr Cash 101 80,00 0 26,00 2-Apr Prepaid Rent 131 9,000 Cash 101 9,000 Prepaid twelve months’ rent. 3-Apr Office Equipment 163 8,000 Office Supplies 124 3,600 Accounts Payable 201 11,600 Purchased equip. & […]

978-0078025587 Chapter 2 Solution Manual Part 4

Problem 2-3B (90 minutes) Part 1 Sept. 1 Cash …………………………………………………. 101 38,000 Office Equipment ………………………………. 163 15,000 H. Humble, Capital ……………………… 301 53,000 Owner invested in the business. 2 Prepaid Rent …………………………………….. 131 9,000 Cash ………………………………………….. 101 9,000 Prepaid twelve […]

978-0078025587 Chapter 2 Solution Manual Part 5

Part 3 HV Consulting Trial Balance 30-Sep Debit Credit Cash $12,665 Accounts receivable 2,250 Office supplies 2,000 Office equipment 50,900 Title: Problem 2-1B QA_Ori: Part 1 a. Cash 101 65,000 Office Equipment 163 5,750 Computer Equipment 164 30,000 B. Grechus, […]

978-0078025587 Chapter 2 Solution Manual Part 5

Serial Problem, Success Systems (Continued) Part 2 General Ledger accounts Cash Acct. No. 101 Date Explanation PR Debit Credit Balance Oct. 1 55,000 55,000 2 3,300 51,700 5 2,220 49,480 8 1,420 48,060 15 4,800 52,860 17 805 52,055 20 […]

978-0078025587 Chapter 2 Solution Manual Part 6

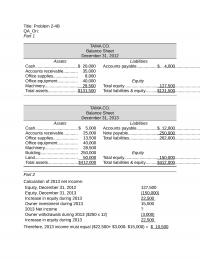

Title: Problem 2-4B QA_Ori: Part 1 TAMA CO. Balance Sheet December 31, 2012 Assets Liabilities Cash………………………………$ 20,000 Accounts payable…………………………………………………………………….$ 4,000 Accounts receivable………… 35,000 TAMA CO. Balance Sheet December 31, 2013 Assets Liabilities Cash……………………………… $ 5,000 Accounts payable…………………………………………………………………….$ 12,000 Accounts receivable………… […]

978-0078025587 Chapter 2 Solution Manual Part 7

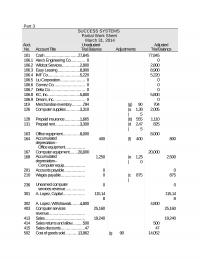

Part 3 SUCCESS SYSTEMS Trial Balance 30-Nov Debit Credit Cash $48,052 Accounts receivable 12,618 Computer supplies 2,545 Prepaid insurance 2,220 Prepaid rent 3,300 Office equipment 8,000 Computer equipment 20,000 Accounts payable $0 A. Lopez, Capital 83,000 A. Lopez, Withdrawals 5,600 […]

978-0078025587 Chapter 20 Excel

Student Name: Class: Part 1 (a) and (b) Direct Direct Materials Labor 700,000 700,000 180,000 54,000 880,000 754,000 Correct! Correct! Direct Direct Materials Labor 420,000$ 139,000$ Cost per equivalent unit of production Costs of beginning goods in process 2,220,000 3,254,000 […]

978-0078025587 Chapter 20 Lecture Note

20-1 CHAPTER 20 PROCESS COST ACCOUNTING © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025587 Chapter 20 Solution Manual Part 1

Title: Question 1 QA_Ori: The main deciding factor in choosing between a job order costing system or a process costing system is the type of product or service. Examples where a process Title: Question 2 QA_Ori: The main focus in […]

978-0078025587 Chapter 20 Solution Manual Part 1

Chapter 20 Process Cost Accounting QUESTIONS 1. The main deciding factor in choosing between a job order costing system or a process costing system is the type of product or service. Examples where a process costing system is likely appropriate […]

978-0078025587 Chapter 20 Solution Manual Part 10

Title: Problem 20-8B QA_Ori: Part 1: Equivalent units with respect to direct materials and direct labor Direct Direct Equivalent units of production (EUP) Materials Labor Units to complete beginning goods in process Direct materials (2,000 x 0%)…………………………… 0 Part 2 […]

978-0078025587 Chapter 20 Solution Manual Part 11

Part 2 (Using weighted-average) MAJOR LEAGUE BAT CO. Process Cost Summary (Weighted Average) For Month Ended July 31 Costs Charged to Production Costs of beginning goods in process Direct materials…………………………………………………………. $ 2,660 Unit cost information Units to account for Units […]

978-0078025587 Chapter 20 Solution Manual Part 12

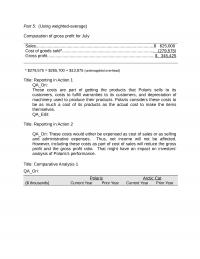

Part 5: (Using weighted-average) Computation of gross profit for July Sales……………………………………………………………………………………….$ 625,000 Title: Reporting in Action 1 QA_Ori: These costs are part of getting the products that Polaris sells to its customers, costs to fulfill warranties to its customers, and […]

978-0078025587 Chapter 20 Solution Manual Part 2

Title: Exercise 20-7 QA_Ori: a. Purchased raw materials on credit at a cost of $52,000. b. Used direct materials costing $42,000 in production. QA_Edit: a. Purchased raw materials on credit at a cost of $52,000. b. Used direct materials costing […]

978-0078025587 Chapter 20 Solution Manual Part 2

Fundamental Accounting Principles, 21st Edition 1148 Exercise 20-14 (Concluded) (1) Beginning goods in process $ 17,250 Direct materials $ ? Direct labor 47,250 Factory overhead 51,300 Total costs added ? Total costs in process $242,400 $17,250 + [Total costs added] […]

978-0078025587 Chapter 20 Solution Manual Part 3

Title: Exercise 20-15 QA_Ori: ASHAD COMPANY Process Cost Summary – Weighted Average Method For Month Ended July 31 Costs Charged to Production Unit Cost Information Units to Account For Units Accounted For Beginning goods in process…………………. 2,000 Completed & transferred […]

978-0078025587 Chapter 20 Solution Manual Part 3

Problem 20-3A (Concluded) Equivalent units of production Direct Materials Direct Labor Factory Overhead Units completed & transferred out …. 17,000 EUP 17,000 EUP 17,000 EUP Units of ending goods in process Direct materials (5,000 x 100%) …….. 5,000 EUP Direct […]

978-0078025587 Chapter 20 Solution Manual Part 4

Title: Exercise 20-22 QA_Ori: HI-TEST COMPANY Process Cost Summary (Weighted-Average Method) For Month Ended September 30 Costs Charged to Production Costs of beginning work in process Direct materials……………………………………………………………….$ 45,000 Unit Cost Information Units to Account For Units Accounted For Beginning […]

978-0078025587 Chapter 20 Solution Manual Part 4

Fundamental Accounting Principles, 21st Edition 1178 Problem 20-1B (Continued) d. June 30 Factory Payroll ………………………………………….…………. 400,000 Cash ………………………………………………………. 400,000 Incurred payroll cost. e. June 30 Goods in Process Inventory ……………………….…. 350,000 Factory Payroll …………………………………….…………. 350,000 Used direct labor. f. June […]

978-0078025587 Chapter 20 Solution Manual Part 5

Part 2 ELLIOTT COMPANY Process Cost Summary – Weighted Average Method For Month Ended March 31 Costs Charged to Production Costs of beginning goods in process Unit cost information Units to account for Units accounted for Beginning goods in process…………………………………2,000 […]

978-0078025587 Chapter 20 Solution Manual Part 5

Problem 20-8B (Concluded) Part 4 MEMORANDUM TO: FROM: DATE: RE: Percentage of Completion Error Analysis If the units in ending inventory are 75% complete instead of 25% with respect to labor, the number of equivalent units in ending inventory with […]

978-0078025587 Chapter 20 Solution Manual Part 6

Title: Problem 20-6A QA_Ori: Part 1 TAMAR CO. Process Cost Summary – FIFO Method For Month Ended May 31 Costs charged to Production Costs of beginning goods in process Direct materials………………………………………………………….$ 19,800 Unit cost information Units to account for Units […]

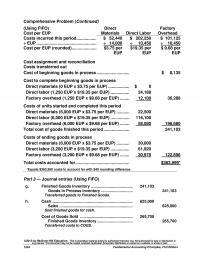

978-0078025587 Chapter 20 Solution Manual Part 6

Fundamental Accounting Principles, 21st Edition 1204 Comprehensive Problem (Continued) (Using FIFO) Cost per EUP Direct Materials Direct Labor Factory Overhead Costs incurred this period ……………… $ 52,440 $ 202,250 $ 101,125 ÷ EUP ……………………………………………. ÷ 14,000 ÷ 10,450 ÷ 10,450 […]

978-0078025587 Chapter 20 Solution Manual Part 7

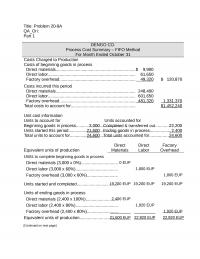

Title: Problem 20-9A QA_Ori: Part 1 DENGO CO. Process Cost Summary – FIFO Method For Month Ended October 31 Costs Charged to Production Costs of beginning goods in process Direct materials………………………………………………………….$ 9,900 Costs incurred this period Direct materials…………………………………………………………. 248,400 Direct […]

978-0078025587 Chapter 20 Solution Manual Part 8

Title: Problem 20-3B QA_Ori: Part 1 a. May 31 Raw Materials Inventory……………………………………………221,120 b. May 31 Goods in Process Inventory………………………………………197,120 Raw Materials Inventory……………………………………… 197,120 Direct materials used in production. c. May 31 Factory Overhead…………………………………………………….40,560 Raw Materials Inventory……………………………………… 40,560 Indirect materials used. […]

978-0078025587 Chapter 20 Solution Manual Part 9

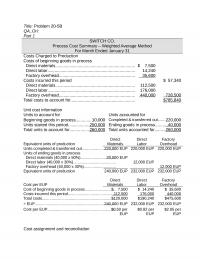

Title: Problem 20-5B QA_Ori: Part 1 SWITCH CO. Process Cost Summary – Weighted Average Method For Month Ended January 31 Costs Charged to Production Costs of beginning goods in process Direct materials…………………………………………………………. $ 7,500 Unit cost information Units to account […]

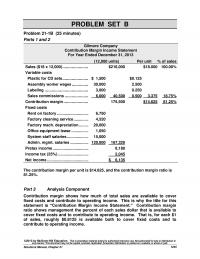

978-0078025587 Chapter 21 Excel

Student Name: Class: 270,000$ «- Correct! 60$ «- Correct! 4,500 «- Correct! 270,000$ «- Correct! 30.00% «- Correct! 900,000$ «- Correct! 900,000$ «- Correct! 630,000 «- Correct! 270,000$ «- Correct! 270,000 «- Correct! $0 «- Correct! Problem 21-02A McGraw-Hill/Irwin Instructor […]

978-0078025587 Chapter 21 Lecture Note

21–1 CHAPTER 21 COST-VOLUME-PROFIT ANALYSIS © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted […]

978-0078025587 Chapter 21 Solution Manual Part 1

Title: Question 1 QA_Ori: A variable cost is one that varies proportionately with the volume of activity. For Title: Question 2 QA_Ori: Variable costs per unit stay the same (remain constant) when output volume changes. This is because each unit […]

978-0078025587 Chapter 21 Solution Manual Part 1

Chapter 21 Cost-Volume-Profit Analysis QUESTIONS 1. A variable cost is one that varies proportionately with the volume of activity. For example, direct materials and direct labor (when the workers are paid for completed units) are treated as variable costs with […]

978-0078025587 Chapter 21 Solution Manual Part 2

Title: Exercise 21-7 QA_Ori: The scatter diagram and line of estimated cost behavior appear below. Selecting 0 and 2,400 units sold as the activity levels yields $2,500 as the estimate of fixed costs and the following estimate of variable costs […]

978-0078025587 Chapter 21 Solution Manual Part 2

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

978-0078025587 Chapter 21 Solution Manual Part 3

Title: Problem 21-3A QA_Ori: Parts 1 and 2 The scatter diagram and its estimated line of cost behavior appear below. Part 2 – Calculation of variable and fixed costs Variable costs = $220,000 – $64,000 = $0.60 per dollar of […]

978-0078025587 Chapter 21 Solution Manual Part 3

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

978-0078025587 Chapter 21 Solution Manual Part 4

Kyo Company 0 20 40 60 80 100 $120 0 $50 $100 $150 $200 $250 Sales Dollars Total Costs Title: Problem 21-3B QA_Ori: Parts 1 and 2 The scatter diagram and its estimated line of cost behavior appear below. Sales […]

978-0078025587 Chapter 21 Solution Manual Part 4

Fundamental Accounting Principles, 21st Edition 1254 Problem 21-7B (50 minutes) Part 1 BREAK–EVEN ANALYSIS ASSUMING USE OF SAME MATERIALS Step 1: Compute break-even in composite units—Use equation in Exhibit 21.27 Break-even in composite units = Fixed costs/Contribution margin per composite […]

978-0078025587 Chapter 21 Solution Manual Part 5

Title: Problem 21-7B QA_Ori: Part 1 BREAK–EVEN ANALYSIS ASSUMING USE OF SAME MATERIALS Step 1: Compute break-even in composite units—Use equation in Exhibit 21.27 Break-even in composite units = Fixed costs/Contribution margin per composite unit * To compute the contribution […]

978-0078025587 Chapter 22 Excel

Student Name: Class: March April May 25,000 32,000 35,000 30% 30% 30% 7,500 9,600 10,500 15,000 25,000 32,000 22,500 34,600 42,500 (20,000) (7,500) (9,600) 2,500 27,100 32,900 Correct! Correct! Correct! March April May 90,000 95,000 90,000 30% 30% 30% 27,000 […]

978-0078025587 Chapter 22 Lecture Note

22-1 CHAPTER 22 MASTER BUDGETS AND PLANNING © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, […]

978-0078025587 Chapter 22 Solution Manual Part 1

Title: Question 1 QA_Ori: A budget helps managers control and monitor a business by 1) communicating plans to Title: Question 2 QA_Ori: Two common benchmarks used by managers to evaluate performance are: past performance and budgeted performance. Budgeted performance is […]

978-0078025587 Chapter 22 Solution Manual Part 1

Chapter 22 Master Budgets and Planning QUESTIONS 1. A budget helps managers control and monitor a business by 1) communicating plans to employees, 2) coordinating the activities of different parts of the organization, and 3) providing a basis for deciding […]

978-0078025587 Chapter 22 Solution Manual Part 2

Title: Quick Study 22-25 QA_Ori: SCORA INC. Selling Expense Budget For January, February, and March January February March Budgeted sales (from QS 22-23) $60,000 $100,000 $80,000 Title: Quick Study 22-26 QA_Ori: MESSERS COMPANY Cash Budget For Month Ended February 28 […]

978-0078025587 Chapter 22 Solution Manual Part 2

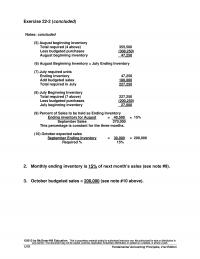

Fundamental Accounting Principles, 21st Edition 1278 Exercise 22-2 (concluded) Notes: concluded (5) August beginning inventory Total required (4 above) 355,500 Less budgeted purchases (308,250) August beginning inventory 47,250 (6) August Beginning Inventory = July Ending Inventory (7) July required units […]

978-0078025587 Chapter 22 Solution Manual Part 3

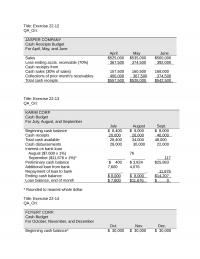

Title: Exercise 22-12 QA_Ori: JASPER COMPANY Cash Receipts Budget For April, May, and June April May June Sales $525,000 $535,000 $560,000 Less ending accts. receivable (70%) 367,500 374,500 392,000 Title: Exercise 22-13 QA_Ori: KARIM CORP. Cash Budget For July, August, […]

978-0078025587 Chapter 22 Solution Manual Part 3

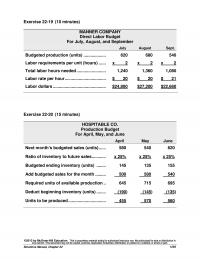

Exercise 22-19 (10 minutes) MANNER COMPANY Direct Labor Budget For July, August, and September July August Sept. Budgeted production (units) ……………….… 620 680 540 Labor requirements per unit (hours) ……… x 2 x 2 x 2 Total labor hours needed […]

978-0078025587 Chapter 22 Solution Manual Part 4

Title: Problem 22-3A QA_Ori: Part 1 Cash collections of credit sales (accounts receivable) From sales in Total % Collected June July April $ 720,000 28% $201,600 Part 2 Budgeted ending inventories (in units) April May June July Next month’s budgeted […]

978-0078025587 Chapter 22 Solution Manual Part 4

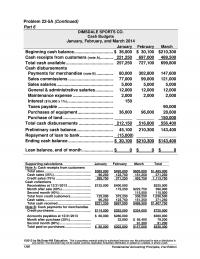

Fundamental Accounting Principles, 21st Edition 1308 Problem 22-5A (Continued) Part 6 DIMSDALE SPORTS CO. Cash Budgets January, February, and March 2014 January February March Beginning cash balance …………………………….…. $ 36,000 $ 30,100 $210,300 Cash receipts from customers (note A)……………. 221,250 […]

978-0078025587 Chapter 22 Solution Manual Part 5

Title: Problem 22-7A QA_Ori: Part 1 ZIGBY MANUFACTURING Sales Budgets April, May, and June 2013 Budgeted Units Budgeted Unit Price Budgeted Total Dollars April 2013 20,500 $23.85 $ 488,925 Part 2 ZIGBY MANUFACTURING Production Budget April, May, and June 2013 […]

978-0078025587 Chapter 22 Solution Manual Part 5

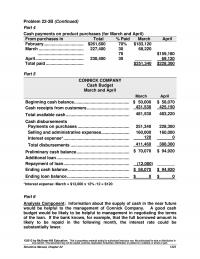

Problem 22-3B (Continued) Part 4 Cash payments on product purchases (for March and April) From purchases in Total % Paid March April February ……………………………..…. $261,600 70% $183,120 March ……………………………………. 227,400 30 68,220 ………………………………….…. 70 $159,180 April ………………………………………. 230,400 30 _______ […]

978-0078025587 Chapter 22 Solution Manual Part 6

Title: Problem 22-4B QA_Ori: Part 1 COMP-MEDIA Budgeted Income Statement For Months of July, August, and September, 2013 July August September Sales* $1,265,000 $1,391,500 $1,530,650 Cost of goods sold* 660,000 726,000 798,600 Gross profit 605,000 665,500 732,050 * Volume for […]

978-0078025587 Chapter 22 Solution Manual Part 6

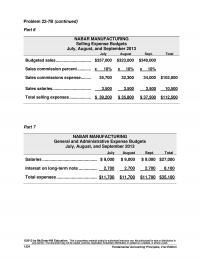

Fundamental Accounting Principles, 21st Edition 1334 Problem 22-7B (continued) Part 6 NABAR MANUFACTURING Selling Expense Budgets July, August, and September 2013 July August Sept. Total Budgeted sales ………………………….. $357,000 $323,000 $340,000 Sales commission percent ………….….. x 10% x 10% x […]

978-0078025587 Chapter 22 Solution Manual Part 7

Title: Problem 22-7B QA_Ori: Part 1 NABAR MANUFACTURING Sales Budgets July, August, and September 2013 Budgeted Units Budgeted Unit Price Budgeted Total Dollars July 2013 21,000 $17.00 $ 357,000 Part 2 NABAR MANUFACTURING Production Budget July, August, and September 2013 […]

978-0078025587 Chapter 23 Excel

Student Name: Class: Units Cost Total 1,615,000 $4.10 $6,621,500 1,620,000 $4.00 6,480,000 $141,500 U Correct! Yes! Units Price Total 1,615,000 $4.10 $6,621,500 1,615,000 $4.00 6,460,000 $161,500 U Correct! Yes! 1,615,000 $4.00 $6,460,000 1,620,000 $4.00 6,480,000 $20,000 F Correct! Yes! $161,500 […]

978-0078025587 Chapter 23 Lecture Note Part 1

23-1 CHAPTER 23 FLEXIBLE BUDGETS AND STANDARD COSTS Related Assignment Materials Student Learning Objectives Discussion Questions Quick Studies* Exercises* Problems* Beyond the Numbers Conceptual objectives: C1. Define standard costs and explain how standard cost information is useful for management by […]

978-0078025587 Chapter 23 Lecture Note Part 2

23–10 Chapter Outline Appendix 23A I. Expanded Overhead Variances A. Computing Overhead Cost Variances⎯assume predetermined rate is based on relation between standard overhead and standard labor hours. 1. Framework uses classifications of overhead costs as either variable or fixed 2. […]

978-0078025587 Chapter 23 Solution Manual Part 1

Title: Question 1 QA_Ori: Fixed budget performance reports have limited usefulness because they do not Title: Question 2 QA_Ori: The primary purpose of a flexible budget is to help managers better evaluate past performance, which can improve their abilities to […]

978-0078025587 Chapter 23 Solution Manual Part 1

Chapter 23 Flexible Budgets and Standard Costs QUESTIONS 1. Fixed budget performance reports have limited usefulness because they do not reflect differences in revenues and variable costs that can occur simply because actual volume is different from budgeted volume. This […]

978-0078025587 Chapter 23 Solution Manual Part 2

Title: Exercise 23-1 QA_Ori: Item Cost a. Bike frames Variable b. Screws for assembly Variable c. Repair expense for tools (If these costs are only remotely related to volume, they may be better classified as fixed) Variable * Incoming shipping […]

978-0078025587 Chapter 23 Solution Manual Part 2

Fundamental Accounting Principles, 21st Edition 1360 Exercise 23-6 (20 minutes) 1. Predetermined overhead rate computations Expected volume ……………………………………………………………. 75% Expected total overhead …………………………………………………. $2,100,000 Expected hours ……………………………………………………………… 375,000 hrs. Variable cost per hour ($1,500,000/ 375,000) ……………………. $4.00 Fixed cost per […]

978-0078025587 Chapter 23 Solution Manual Part 3

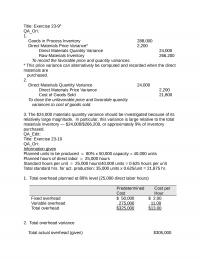

Title: Exercise 23-9A QA_Ori: 1. Goods in Process Inventory 288,000 To record the favorable price and quantity variances. * This price variance can alternatively be computed and recorded when the direct materials are purchased. 2. Direct Materials Quantity Variance 24,000 […]

978-0078025587 Chapter 23 Solution Manual Part 3

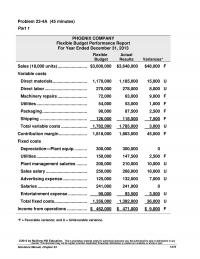

Problem 23-4A (45 minutes) Part 1 PHOENIX COMPANY Flexible Budget Performance Report For Year Ended December 31, 2013 Flexible Actual Budget Results Variances* Sales (18,000 units) …………………….. $3,600,000 $3,648,000 $48,000 F Variable costs Direct materials ………………………… 1,170,000 1,185,000 15,000 U […]

978-0078025587 Chapter 23 Solution Manual Part 4

Title: Problem 23-5A QA_Ori: Part 1 Variable or Fixed Classification Per unit Amount Variable costs (total divided by 15,000 units) Indirect materials $ 3.00 Fixed costs (per month) Depreciation—Building $ 24,000 Depreciation—Machinery 80,000 Taxes and insurance 12,000 Supervision 79,000 Total […]

978-0078025587 Chapter 23 Solution Manual Part 4

Fundamental Accounting Principles, 21st Edition 1390 $50,000 F (Spending variance) $10,000 F (Efficiency variance) $60,000 F (Total variable overhead variance) (b) Fixed Overhead Spending and Volume Variances Actual Overhead Budgeted Overhead Applied Overhead 252,000 x $7 $1,960,000 $2,016,000 $1,764,000 $56,000 […]

978-0078025587 Chapter 23 Solution Manual Part 5

Title: Problem 23-1B QA_Ori: Part 1 Direct Materials Variances Direct materials cost variances Actual units at actual cost [1,000,000 lbs. @ $4.25] $4,250,000 Direct Materials Price and Quantity Variances Actual Cost AQ x AP AQ x SP Standard Cost SQ […]

978-0078025587 Chapter 23 Solution Manual Part 5

Problem 23-6BA (Continued) Part 3 Overhead Variances (a) Variable overhead Preliminary computations Actual variable overhead (given): Indirect materials ……………………………………………….. $10,000 Indirect labor …………………………………………………….. 16,000 Power …………………………………………………………..….. 4,500 Maintenance ………………………………………………….….. 3,000 Total …………………………………………………………….….. $33,500 Actual hours: 37,600 (given) Standard hours: 36,000 […]

978-0078025587 Chapter 23 Solution Manual Part 6

Part 3 Direct Materials Variances Preliminary computations Actual material used: 69,000 lbs. (given) Direct material cost variances Actual units at actual cost [69,000 lbs. @ $6.10] $420,900 Standard units at standard cost [67,500 lbs. @ $6.00] 405,000 Direct material cost […]

978-0078025587 Chapter 23 Solution Manual Part 7

Part 4 GUADELUPE COMPANY Overhead Variance Report For Month Ended March 31 Volume Variance Expected production level 80% of capacity Production level achieved 90% of capacity Volume variance $6,000 (favorable) Flexible Actual Controllable Variance Budget Results Variances* Variable overhead costs […]

978-0078025587 Chapter 24 Excel

Student Name: Class: Square Footage Rate Total 1,000 8.25$ 8,250$ «- Correct! 1,800 8.25 14,850$ «- Correct! Value- Usage Total Based Based Costs Costs Costs 18,000$ 18,000$ 27,000 27,000 9,000 9,000 3,000 3,000$ 3,000 3,000 6,000 6,000 66,000$ 54,000$ 12,000$ […]

978-0078025587 Chapter 24 Lecture Note

24-1 CHAPTER 24 PERFORMANCE MEASUREMENT AND RESPONSIBILITY ACCOUNTING © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025587 Chapter 24 Solution Manual Part 1

Title: Question 1 QA_Ori: Many companies are divided into departments when they become too large to be Title: Question 2 QA_Ori: Operating departments are directly involved in manufacturing or selling the products or services of a business. Service departments support […]

978-0078025587 Chapter 24 Solution Manual Part 1

Chapter 24 Performance Measurement and Responsibility Accounting QUESTIONS 1. Many companies are divided into departments when they become too large to be effectively managed as single units. This division into departments is often needed so that the responsibilities for the […]

978-0078025587 Chapter 24 Solution Manual Part 2

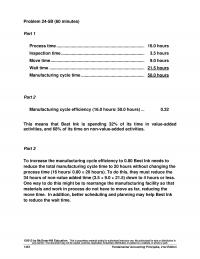

Title: Quick Study 24-15 QA_Ori: Average invested assets = (€12,888 + €13,099) / 2 Title: Quick Study 24-16 QA_Ori: a. Process time 15.0 minutes Inspection time 2.0 minutes Move time 6.4 minutes Wait time 36.6 minutes Manufacturing cycle time 60.0 […]

978-0078025587 Chapter 24 Solution Manual Part 2

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

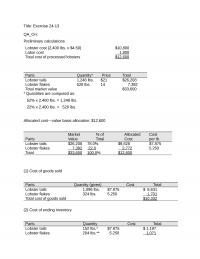

978-0078025587 Chapter 24 Solution Manual Part 3

Title: Exercise 24-13 QA_Ori: Preliminary calculations Lobster cost (2,400 lbs. x $4.50) $10,800 Labor cost 1,800 Total cost of processed lobsters $12,600 Parts Quantity* Price Total Lobster tails 1,248 lbs. $21 $26,208 Lobster flakes 528 lbs. 14 7,392 Total market […]

978-0078025587 Chapter 24 Solution Manual Part 3

©2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or […]

978-0078025587 Chapter 24 Solution Manual Part 4

Title: Problem 24-4A QA_Ori: Part 1 Allocations of joint costs on the basis of sales values Tree pruning and care: $405,000 Grade Sales Value Percent of Total Allocated Cost No. 1 $450,000 48.0% $194,400 No. 2 300,000 32.0 129,600 No. […]

978-0078025587 Chapter 24 Solution Manual Part 4

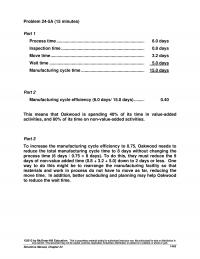

Fundamental Accounting Principles, 21st Edition 1454 Problem 24-5B (60 minutes) Part 1 Process time …………………………………………………………………… 16.0 hours Inspection time ……………………………………………………………..… 3.5 hours Move time ……………………………………………………………………..… 9.0 hours Wait time ………………………………………………………………………… 21.5 hours Manufacturing cycle time ………………………………………………… 50.0 hours Part 2 […]

978-0078025587 Chapter 24 Solution Manual Part 5

Title: Problem 24-4B QA_Ori: Part 1 Allocations of joint cost on the basis of sales values Land preparation, seeding, and cultivating: $700,000 Grade Sales Value Percent of Total Allocated Cost No. 1 $ 900,000 62.5% $437,500 Harvesting, sorting, and grading: […]

978-0078025587 Chapter 25 Excel

Student Name: Class: 115,000$ Correct! Net Net Cash Income Flow 1,840,000$ 1,840,000$ (480,000) (480,000) (672,000) (672,000) (336,000) (336,000) (115,000) (160,000) (160,000) 77,000 (23,100) (23,100) 53,900$ Correct! 168,900$ Correct! 2.84 years Correct! Income taxes Net income Net cash flow Part 3 […]

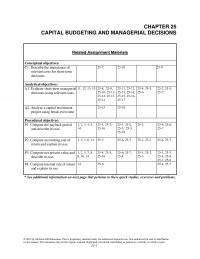

978-0078025587 Chapter 25 Lecture Note

25-1 CAPITAL BUDGETING AND MANAGERIAL DECISIONS Related Assignment Materials Conceptual objectives: C1. Describe the importance of relevant costs for short-term decisions. 25-7 25–10 25-9 Analytical objectives: A1. Evaluate short-term managerial decisions using relevant costs. 11, 12, 13, 15 25-8, 25-9, […]

978-0078025587 Chapter 25 Solution Manual Part 1

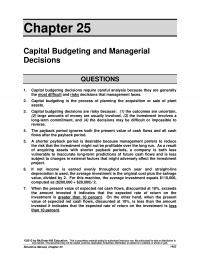

Title: Question 1 QA_Ori: Capital budgeting decisions require careful analysis because they are generally the Title: Question 2 QA_Ori: Capital budgeting is the process of planning the acquisition or sale of plant assets. Title: Question 3 QA_Ori: Capital budgeting decisions […]

978-0078025587 Chapter 25 Solution Manual Part 1

Chapter 25 Capital Budgeting and Managerial Decisions QUESTIONS 1. Capital budgeting decisions require careful analysis because they are generally the most difficult and risky decisions that management faces. 2. Capital budgeting is the process of planning the acquisition or sale […]

978-0078025587 Chapter 25 Solution Manual Part 2

Title: Exercise 25-7 QA_Ori: 1. PROJECT C1 Net Cash Flows Present Value of 1 at 12% Present Value of Net Cash Flows Year 1 $ 12,000 0.8929 $ 10,715 PROJECT C2 Net Cash Flows Present Value of 1 at 12% […]

978-0078025587 Chapter 25 Solution Manual Part 2

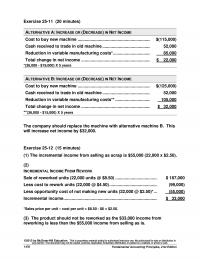

Fundamental Accounting Principles, 21st Edition 1478 Exercise 25-11 (20 minutes) ALTERNATIVE A: INCREASE OR (DECREASE) IN NET INCOME Cost to buy new machine ………………………………………………………. $(115,000) Cash received to trade in old machine …………………………………..…………. 52,000 Reduction in variable manufacturing costs* ………………………….. […]

978-0078025587 Chapter 25 Solution Manual Part 3

Title: Problem 25-2A QA_Ori: Part 1 PROJECT Y Net income $ 56,000 PROJECT Z Part 2 PROJECT Y PROJECT Z 4 years 3 years $350,000 $143,500 $350,000 $153,067 Net income $ 36,400 Depreciation expense* 116,667 Net cash flow $153,067 *Annual […]

978-0078025587 Chapter 25 Solution Manual Part 3

Problem 25-5A (55 minutes) Part 1 Product G Product B Selling price per unit …………………………………………..… $120 $160 Variable costs per unit ………………………………………..… 40 90 Contribution margin per unit ……………………………….… $ 80 $ 70 Machine hours to produce 1 unit ………………………….. […]

978-0078025587 Chapter 25 Solution Manual Part 4

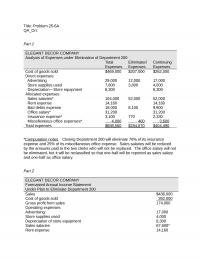

Title: Problem 25-6A QA_Ori: Part 1 ELEGANT DECOR COMPANY Analysis of Expenses under Elimination of Department 200 Total Eliminated Continuing Expenses Expenses Expenses Cost of goods sold $469,000 $207,000 $262,000 Direct expenses *Computation notes. Closing Department 200 will eliminate 70% […]

978-0078025587 Chapter 25 Solution Manual Part 4

Problem 25-5B (55 minutes) Part 1 Product R Product T Selling price per unit …………………………………………….. $ 60 $ 80 Variable costs per unit ………………………………………….. 20 45 Contribution margin per unit …………………………………. $ 40 $ 35 Machine hours to produce 1 […]

978-0078025587 Chapter 25 Solution Manual Part 5

Title: Problem 25-4B QA_Ori: WINDMIRE COMPANY COMPARATIVE INCOME STATEMENTS (1) (2) (3) Normal New Volume Business Combined Supporting computations Normal direct material cost $384,000 Units of output 300,000 Cost per unit $ 1.28 New business volume 50,000 New business direct […]

978-0078025587 Chapter 3 Excel

Student Name: Class: Parts 1 and 2 Unadj. Bal. 34,000 Unadj. Bal. 80,000 Bal. 34,000 Bal. 80,000 Correct! Correct! Unadj. Bal. 0 Unadj. Bal. 15,000 (f) 7,500 ( c) 13,200 Adj. Bal. 7,500 Adj. Bal. 28,200 Correct! Correct! Unadj. Bal. […]

978-0078025587 Chapter 3 Lecture Note

3-1 STATEMENTS Related Assignment Materials Student Learning Objectives Questions Quick Studies* Exercises* Problems* Beyond the Numbers Conceptual objectives: C1. Explain the importance of periodic reporting and the time period principle. 3 3-4, 3-6 3-2 3-1, 3-3, 3-4, 3-5, 3-8, 3- […]

978-0078025587 Chapter 3 Solution Manual Part 1

Title: Question 1 QA_Ori: The cash basis of accounting reports revenues when cash is received while the Title: Question 2 QA_Ori: The accrual basis of accounting generally provides a better indication of company performance and financial condition than does the […]

978-0078025587 Chapter 3 Solution Manual Part 1

Chapter 3 Adjusting Accounts and Preparing Financial Statements QUESTIONS 1. The cash basis of accounting reports revenues when cash is received while the accrual basis reports revenues when they are earned. The cash basis reports expenses when cash is paid […]

978-0078025587 Chapter 3 Solution Manual Part 10

Part 2 JKL CoMPANY Income Statement For Year Ended July 31, 2013 Revenues Consulting fees earned $134,24 0 Expenses Depreciation expense—Office equipment $6,00 0 74,00 JKL CoMPANY Statement of Owner’s Equity For Year Ended July 31, 2013 J. Logan, Capital, […]

978-0078025587 Chapter 3 Solution Manual Part 12

Title: Problem 3-5B Part 1 QA_Ori: SPEEDY COURIER Income Statement For Year Ended December 31, 2013 Revenues Delivery fees earned $611,80 0 Interest earned 34,000 Total revenues $645,80 0 SPEEDY COURIER Statement of Owner’s Equity For Year Ended December 31, […]

978-0078025587 Chapter 3 Solution Manual Part 2

Title: Quick Study 3-18 QA_Ori: a. Step 1: Salaries Payable equals $0 Step 2: Salaries Payable should equal $15,500 (not yet recorded) Step 3: Adjusting entry to get from Step 1 to Step 2 Salaries Expense……………………………………………………. 15,500 Salaries Payable…………………………………………………. 15,500 […]

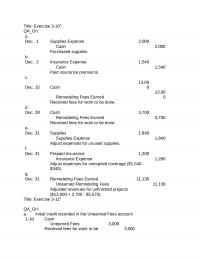

978-0078025587 Chapter 3 Solution Manual Part 2

Exercise 3-6 (15 minutes) a. Supplies expense for current year: $2,550 b. Supplies available – current year-end: $6,500 c. Supplies purchased in current year: $8,490 d. Supplies available – prior year end: $2,288 Proof: (a) (b) (c) (d) Supplies available […]

978-0078025587 Chapter 3 Solution Manual Part 3

Title: Exercise 3-10A QA_Ori: a. Dec. 1 Supplies Expense 2,000 b. Dec. 2 Insurance Expense 1,540 Cash 1,540 Paid insurance premiums. c. Dec. 15 Cash 13,00 0 Remodeling Fees Earned 0 Received fees for work to be done. 13,00 d. […]

978-0078025587 Chapter 3 Solution Manual Part 3

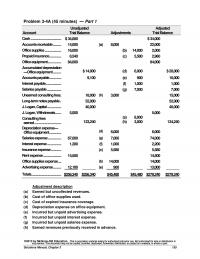

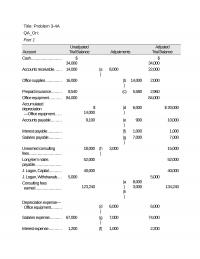

Problem 3-4A (45 minutes) — Part 1 Account Unadjusted Trial Balance Adjustments Adjusted Trial Balance Cash ………………………………….. $ 34,000 $ 34,000 Accounts receivable ……….. 14,000 (a) 8,000 22,000 Office supplies …………………. 16,000 (b) 14,000 2,000 Prepaid insurance ……………. 8,540 (c) […]

978-0078025587 Chapter 3 Solution Manual Part 4

Title: Problem 3-4A QA_Ori: Part 1 Account Unadjusted Trial Balance Adjustments Adjusted Trial Balance Cash…………………….. $ 34,000 $ 34,000 Accounts receivable…… 14,000 (a ) 8,000 22,000 Office supplies………….. 16,000 (b ) 14,000 2,000 Prepaid insurance……… 8,540 (c) 5,580 2,960 Office […]

978-0078025587 Chapter 3 Solution Manual Part 4

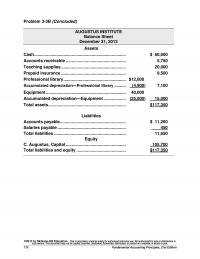

Problem 3-3B (Concluded) AUGUSTUS INSTITUTE Balance Sheet December 31, 2013 Assets Cash …………………………………………………………………… $ 60,000 Accounts receivable …………………………………………… 5,750 Teaching supplies ………………………………………………. 20,000 Prepaid insurance ………………………………………………. 9,500 Professional library …………………………………………….. $12,000 Accumulated depreciation—Professional library ………. (4,900) 7,100 Equipment ………………………………………………………….. 40,000 […]

978-0078025587 Chapter 3 Solution Manual Part 5

Title: Problem 3-3B Parts 1 and 2 QA_Ori: Cash Accounts Payable Accounts Receivable Salaries Payable Unadj. Bal. 0 Unadj. Bal. 0 (f) 5,750 (g) 450 Adj. Bal. 5,750 Adj. Bal. 450 Teaching Supplies Unearned Training Fees Unadj. Bal. 70,000 Unadj. […]

978-0078025587 Chapter 3 Solution Manual Part 5

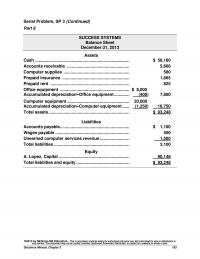

Serial Problem, SP 3 (Continued) Part 6 SUCCESS SYSTEMS Balance Sheet December 31, 2013 Assets Cash …………………………………………………………………….. $ 58,160 Accounts receivable …………………………………………….. 5,668 Computer supplies ……………………………………………….. 580 Prepaid insurance ………………………………………………… 1,665 Prepaid rent …………………………………………………………. 825 Office equipment ………………………………………………….. $ 8,000 […]

978-0078025587 Chapter 3 Solution Manual Part 6