1120 Fundamental Accounting Principles, 21st Edition

Problem 19-4B (35 minutes)

Part 1

a. Predetermined overhead rate

b. Overhead costs charged to jobs

Direct

Applied

Job No.

Labor

Overhead (50%)

625 ……………………………………………………....

$ 354,000

$177,000

626 ……………………………………………………....

330,000

165,000

627 ……………………………………………………....

175,000

87,500

628 ……………………………………………………....

420,000

210,000

629 ……………………………………………………....

184,000

92,000

630 ……………………………………………………....

10,000

5,000

Total …………………………………………………..…..

$1,473,000

$736,500

c. Overapplied or underapplied overhead determination

Actual overhead cost………………………………………………………

$725,000

Less applied overhead cost ………………………………………….…

736,500

Overapplied overhead ………………………………………………….…

$ (11,500)

Part 2

Dec. 31

Factory Overhead …………………………………………….…….

11,500

Cost of Goods Sold …………………………………….…….

11,500

To assign overapplied overhead.

Estimated direct labor cost

[50 x 2,000 x $15] $1,500,000

Problem 19-5B (90 minutes)

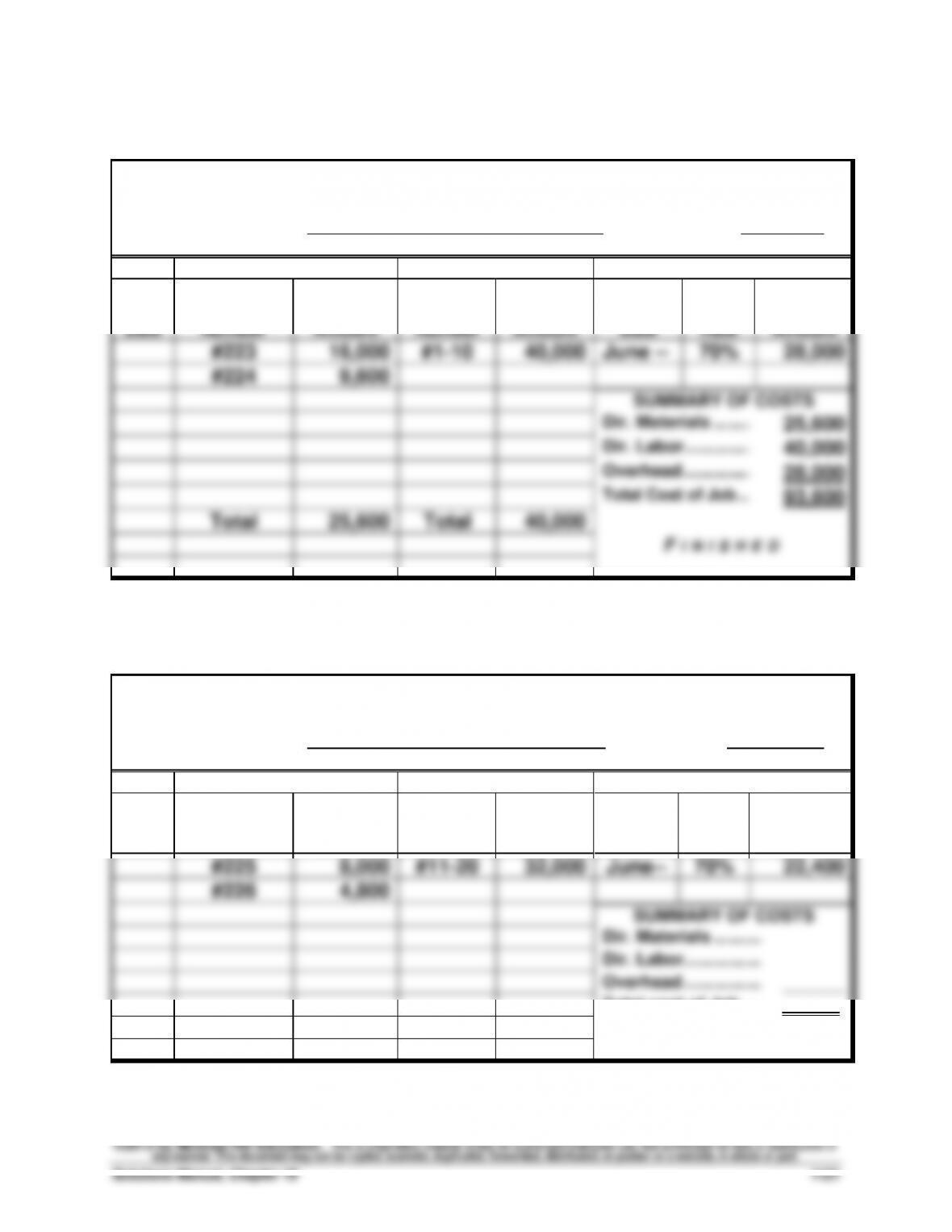

JOB COST SHEET

Customer’s Name

Encinita Company

Job No.

450

Direct Materials

Direct Labor

Overhead Costs Applied

Date

Requisition

Number

Amount

Time

Ticket

Number

Amount

Date

Rate

Amount

#223

16,000

#1–10

40,000

June —

70%

28,000

#224

9,600

SUMMARY OF COSTS

Dir. Materials ……..……………………

25,600

Dir. Labor …………..………………

40,000

Overhead …………..………………

28,000

Total Cost of Job …………………………..

93,600

Total

25,600

Total

40,000

FI N I S H E D

JOB COST SHEET

Customer’s Name

Fargo, Inc.

Job No.

451

Direct Materials

Direct Labor

Overhead Costs Applied

Date

Requisition

Number

Amount

Time

Ticket

Number

Amount

Date

Rate

Amount

#225

8,000

#11–20

32,000

June—

70%

22,400

#226

4,800

SUMMARY OF COSTS

Dir. Materials ………..…………………

Dir. Labor ……………..……………

Overhead ……………..……………

______

Total cost of Job …..………………………

.

Total

Total

1122 Fundamental Accounting Principles, 21st Edition

Problem 19-5B (Continued)

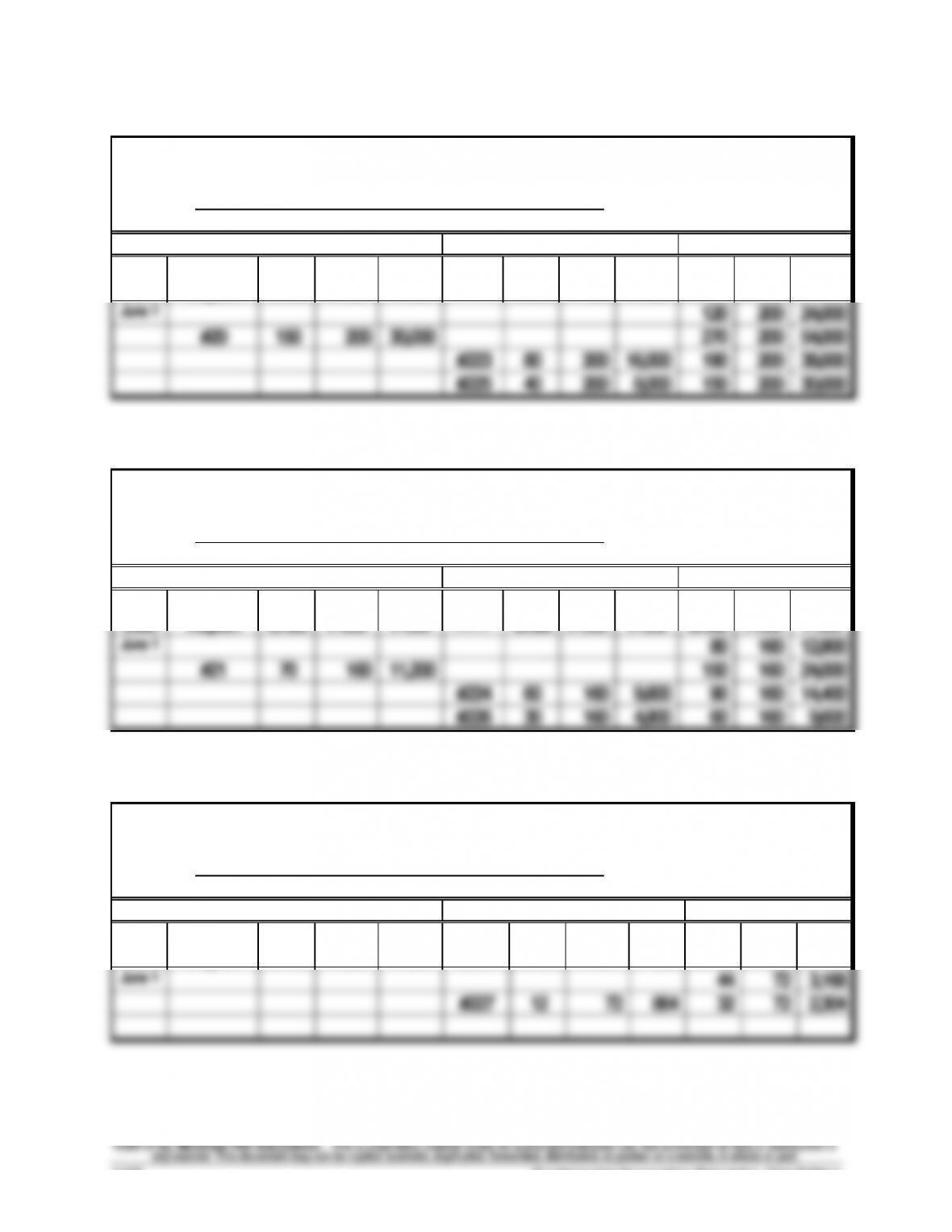

MATERIALS LEDGER CARD

Item

Material M

Received

Issued

Balance

Date

Receiving

Report

Units

Unit

Price

Total

Price

Requi–

sition

Units

Unit

Price

Total

Price

Units

Unit

Price

Total

Price

June 1

120

200

24,000

#20

150

200

30,000

270

200

54,000

#223

80

200

16,000

190

200

38,000

#225

40

200

8,000

150

200

30,000

MATERIALS LEDGER CARD

Item

Material R

Received

Issued

Balance

Date

Receiving

Report

Units

Unit

Price

Total

Price

Requi–

sition

Units

Unit

Price

Total

Price

Units

Unit

Price

Total

Price

June 1

80

160

12,800

#21

70

160

11,200

150

160

24,000

#224

60

160

9,600

90

160

14,400

#226

30

160

4,800

60

160

9,600

MATERIALS LEDGER CARD

Item

Paint

Received

Issued

Balance

Date

Receiving

Report

Units

Unit

Price

Total

Price

Requi–

sition

Units

Unit

Price

Total

Price

Units

Unit

Price

Total

Price

June 1

44

72

3,168

#227

12

72

864

32

72

2,304

Problem 19-5B (Continued)

GENERAL JOURNAL

a.

Raw Materials Inventory ……………………………………..….

41,200

Accounts Payable …………………………………………….

41,200

To record materials purchases ($30,000+$11,200).

d.

Factory Payroll …………………………………………………..….

84,000

Cash …………………………..………………………………..….

84,000

To record factory payroll.

Factory Overhead ………………………………………………….

36,800

Cash …………………………..………………………………..….

36,800

To record other factory overhead.

e.

Finished Goods Inventory ………………………………….….

93,600

Goods in Process …………………………………………….

93,600

To record completion of jobs.

f.

Accounts Receivable ………………………………………….….

290,000

Sales …………………………………………………………….….

290,000

To record sales on account.

Cost of Goods Sold ……………………………………………….

93,600

Finished Goods Inventory …………………………….….

93,600

To record cost of sales.

h.

Goods in Process Inventory* ………………………………….

38,400

Factory Overhead ………………………………………………….

864

Raw Materials Inventory ………………………………..….

39,264

To record direct & indirect materials.

*($16,000 + $8,000 + $9,600 + $4,800)

i.

Goods in Process Inventory* ………………………………….

72,000

Factory Overhead ………………………………………………….

12,000

Factory Payroll ……………………………………………..….

84,000

To record direct & indirect labor.

*($40,000 + $32,000)

j.

Goods in Process Inventory …………………………..…..….

50,400

Factory Overhead …………………………………………….

50,400

To apply overhead ($28,000 + $22,400).

1124 Fundamental Accounting Principles, 21st Edition

Problem 19-5B (Continued)

k. The ending balance in Factory Overhead is computed as:

Actual Factory Overhead

Miscellaneous overhead …………..

$36,800

Indirect materials ……………………..

864

Indirect labor …………………………...

12,000

Total actual factory overhead ……

49,664

Factory overhead applied ……………

50,400

Overapplied overhead …………………

$ (736)

SERIAL PROBLEM— SP 19

Serial Problem—SP 19, Success Systems (40 minutes)

1. The cost of direct materials requisitioned in the month equals the total

direct materials costs accumulated on the three jobs less the amount of

direct materials cost assigned to Job 6.02 in May:

Job 6.02 ………………………………………………………………..

$1,500

Less prior costs ……………………………………………..……..

(600)

$ 900

Job 6.03 ………………………………………………………………..

3,300

Job 6.04 ………………………………………………………………..

2,700

Total materials used (requisitioned) ………………..……..

$6,900

2. Direct labor cost incurred in the month equals the total direct labor

costs accumulated on the three jobs less the amount of direct labor cost

assigned to Job 6.02 in May:

Job 6.02 …………………………..…………………………….……..

$ 800

Less prior costs ……………………………………………..……..

(180)

$ 620

Job 6.03 …………………………..…………………………….……..

1,420

Job 6.04 …………………………..…………………………….……..

2,100

Total direct labor …………………………………………….……..

$4,140

3. The predetermined overhead rate equals the ratio between the amount

of overhead assigned to the jobs divided by the amount of direct labor

cost assigned to them. Since the rate is assumed constant during the

year in this problem, and the same rate is used for all jobs within a

month, the ratio for any one of them equals the rate that was applied.

This table shows the ratio for jobs 6.02 and 6.04:

Job 6.02

Job 6.04

Overhead ………………………………………………..……

$ 400

$1,050

Direct labor …………………………..………………………

800

2,100

Predetermined overhead rate …………………..……

50%

50%

4. The cost transferred to finished goods in June equals the total costs of

the two completed jobs for the month, which are Jobs 6.02 and 6.03:

Job 6.02

Job 6.03

Total

Direct materials ………………………..…

$1,500

$3,300

$4,800

Direct labor …………………………..….…….

800

1,420

2,220

Overhead …………………………..……..…….

400

710

1,110

Total transferred cost ……………….…….

$2,700

$5,430

$8,130

1126 Fundamental Accounting Principles, 21st Edition

Reporting in Action — BTN 19-1

1. We would anticipate that at least two types of costs will increase as a

percent of sales with Polaris’s growth in domestic sales. The first type

is broadly classed into variable costs. Variable costs are the usual

2. Both types of costs identified in part 1 are likely to increase as Polaris

expands into more markets. Examples of specific items include

communication, advertising, training, travel, and management costs. In

3. Solution depends on the annual report information obtained.

Comparative Analysis — BTN 19-2

1. Actual inventory changes and operating cash flow effects as found on

the cash flow statement (amounts are in $thousands)

Polaris

Current Year

One Year

Prior

Two Years

Prior

Inventory change ………..………………

Increase

Increase

Decrease

Operating cash

flow effect from

inventory change ………..………………

Decrease of

$49,973

Decrease of

$56,612

Increase of

$42,997

Arctic Cat

Current Year

One Year

Prior

Two Years

Prior

Inventory change ………..………………

Decrease

Decrease

Decrease

Operating cash

flow effect from

inventory change ………..………………

Increase of

$20,587

Increase of

$40,003

Increase of

$2,798

2. A successful JIT system should reduce inventory levels. This reduction

in inventory should increase operating cash flows. In the solution of

part 1, notice that decreases in inventory yield increases in operating

3. This is a one-time occurrence of a release of cash. However, this one–

time adjustment can yield a recurring impact on returns if such freed up

1128 Fundamental Accounting Principles, 21st Edition

Ethics Challenge — BTN 19-3

Instructor note: This problem is designed to illustrate why the accounting professional

must be aware of management’s and employees’ biases when working with and relying

on accounting estimates and data.

MEMORANDUM

TO:

FROM:

DATE:

SUBJECT:

Suggested content outline

The obvious concern is that management is allocating more overhead to

government jobs compared to open market bid contracts. There is no

obvious reason for such behavior other than a profit motive.

Specifically, by allocating more overhead to government jobs, profits on

government jobs will increase in relation to cost. Conversely, private

market jobs will show greater profits because more overhead is allocated

to government jobs and less to private jobs.

This type of abuse in overhead allocation is a real problem in practice.

This is why we hear of “$500 hammers” sold to the U.S. Government.

Communicating in Practice — BTN 19-4

Student notes should include but not be limited to the following points:

1. You recommend replacing the general accounting (periodic inventory)

system with a cost accounting (perpetual inventory) system—

specifically a job order cost accounting system. Cost accounting

systems provide product cost information as products are

2. This new system would require use of many different documents to

control the acquisition, use, and availability of materials. It also requires

documents for allocation of labor and overhead costs, and for finished

3. The focal point of the new system is the job cost sheet, which is used to

1130 Fundamental Accounting Principles, 21st Edition

Taking It to the Net — BTN 19-5

Instructor note: There is no single solution to this assignment.

The Website [amsi.com] provides details about what its job costing

software can provide to users. After careful examination, students can

write a report to the CEO, which may include the following points:

Teamwork in Action — BTN 19-6

1. A medical clinic can be considered as appropriate for a job order cost

accounting system. This is because each patient is unique in many

ways, such as the type/location of the illness (skin, heart, lung, etc.),

2. In light of the differences identified in part 1, the doctors will consider

the individual characteristics of every patient in determining the type

Entrepreneurial Decision — BTN 19-7

1. A job cost sheet for a service company would likely not have any costs

2. Examples of direct labor and overhead costs for Astor and Black

include:

Hitting the Road — BTN 19-8

1. The framework for the job cost sheet should follow that in the second

exhibit in the chapter. This includes the descriptions for: company

2. Results of the comparison of job cost sheets to a builder’s actual job

Global Decision — BTN 19-9

1. Actual inventory amounts and changes. KTM’s amounts are in Australian

dollars (thousands) and Piaggio’s amounts are in euros (thousands).

KTM ($ ‘000’s)

Balance,

Current Year

Balance,

Prior Year

Change in

Inventory

Inventory …………………….…….

$113,979

$108,910

$5,069

Increase

Operating cash

flow effect from

inventory change ………..………………

Decrease of

$5,069

Piaggio (€ ‘000’s)

Balance,

Current Year

Balance,

Prior Year

Change in

Inventory

Inventory …………………….…….

€236,998

€240,066

€3,068

Decrease

Operating cash

flow effect from

inventory change ………..………………

Increase of

€3,068

2. A successful JIT system should reduce inventory levels. This reduction

in inventory should increase operating cash flows. In the solution of

part 1, notice that decreases in inventory yield increases in operating

3. We cannot definitively determine which company of the two would

benefit the most from JIT implementation. The benefit of JIT would