Student Name:

Class:

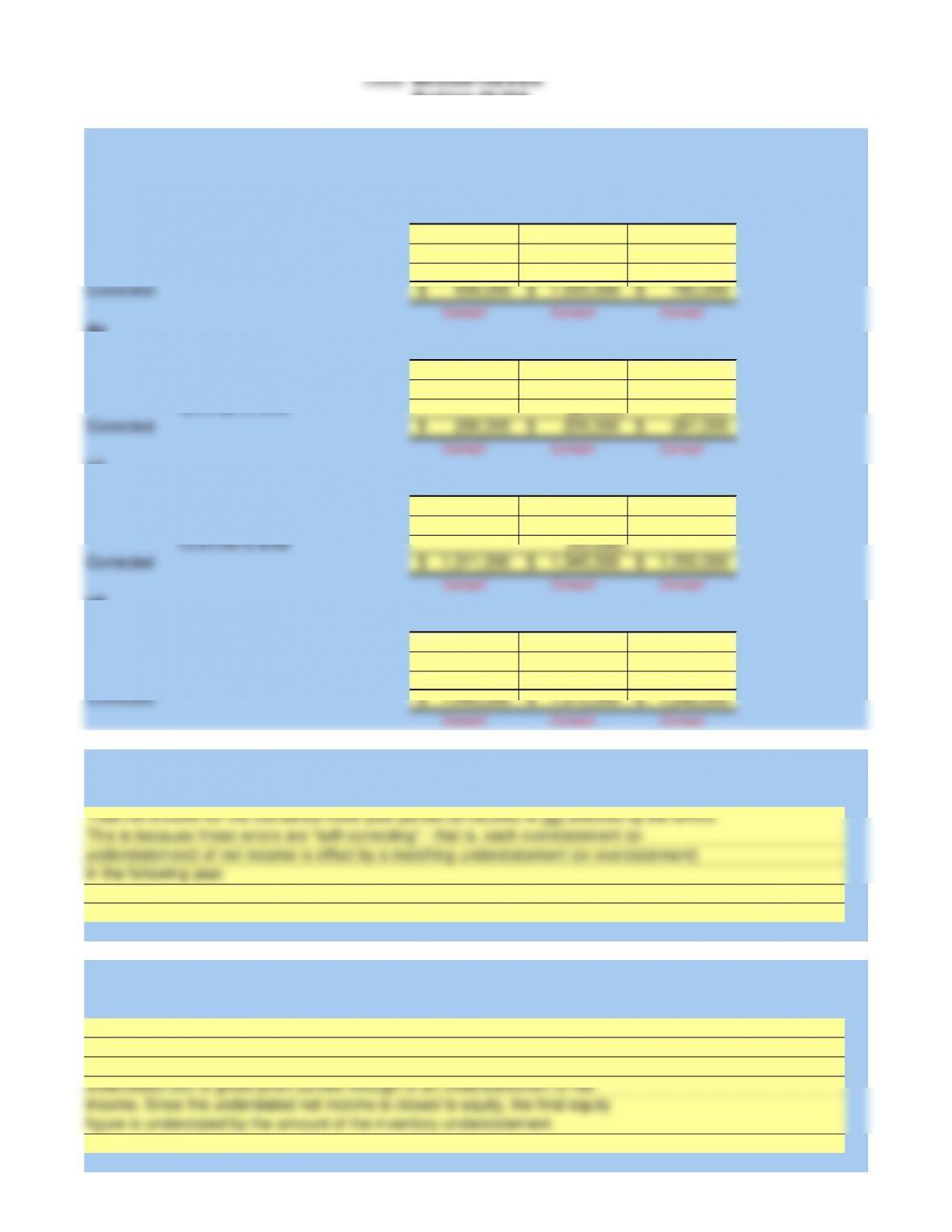

2012 2013 2014

615,000$ 957,000$ 780,000$

(56,000) 56,000

20,000 (20,000)

559,000$ 1,033,000$ 760,000$

Correct! Correct! Correct!

2012 2013 2014

230,000$ 285,000$ 241,000$

56,000 (56,000)

(20,000) 20,000

286,000$ 209,000$ 261,000$

Correct! Correct! Correct!

2012 2013 2014

(c)

Total current assets:

Reported

56,000

(20,000)

1,311,000$ 1,345,000$ 1,200,000$

Correct! Correct! Correct!

2012 2013 2014

(d)

Equity:

Reported

56,000

(20,000)

1,443,000$ 1,510,000$ 1,242,000$

Correct! Correct! Correct!

Instructor

Total net income for the combined three-year period ($756,000) is not affected by the errors.

This is because these errors are “self-correcting” – that is, each overstatement (or

Adjustments to Correct Inventory Errors

NAVAJO COMPANY

from the inventory errors? Explain

2. What is the error in total net income for the combined three-year period resulting

McGraw-Hill/Irwin

Problem 06-06A

The understatement of inventory by $56,000 results in an overstatement of cost of

goods sold by that same amount. The $56,000 overstatement of cost of goods sold

results in an understatement of gross profit by the same amount. This

results in an understatement of equity by the same amount in that year.

3. Explain why the understatement of inventory by $56,000 at the end of 2012

figure is understated by the amount of the inventory understatement.

understatement of gross profit carries through to an understatement of net

understatement) of net income is offset by a matching understatement (or overstatement)

in the following year.

Adjustments: 12/31/2012 error

income. Since the understated net income is closed to equity, the final equity

(a)

Cost of goods sold:

(b)

Net income:

Reported

Adjustments: 12/31/2012 error

12/31/2013 error

Corrected

Reported

Corrected

12/31/2013 error

Corrected

Adjustments: 12/31/2012 error

12/31/2013 error

Corrected

Adjustments: 12/31/2012 error

12/31/2013 error

Key Figures 2012 2013 2014

(a) 615,000$ 957,000$ 780,000$

(b) 230,000 285,000 241,000

(c) 1,255,000 1,365,000 1,200,000

(d) 1,387,000 1,530,000 1,242,000

56,000$

20,000$

286,000$

209,000$

261,000$

NAVAJO COMPANY

For Year Ended December 31

Given Data P06-06A:

Total equity

Total current assets

Net income

Cost of goods sold

Understated December 31, 2012

Inventory errors:

Corrected net income: 2014

Corrected net income: 2013

(1) Corrected net income: 2012

Check figures:

Overstated December 31, 2013

Student Name:

Class:

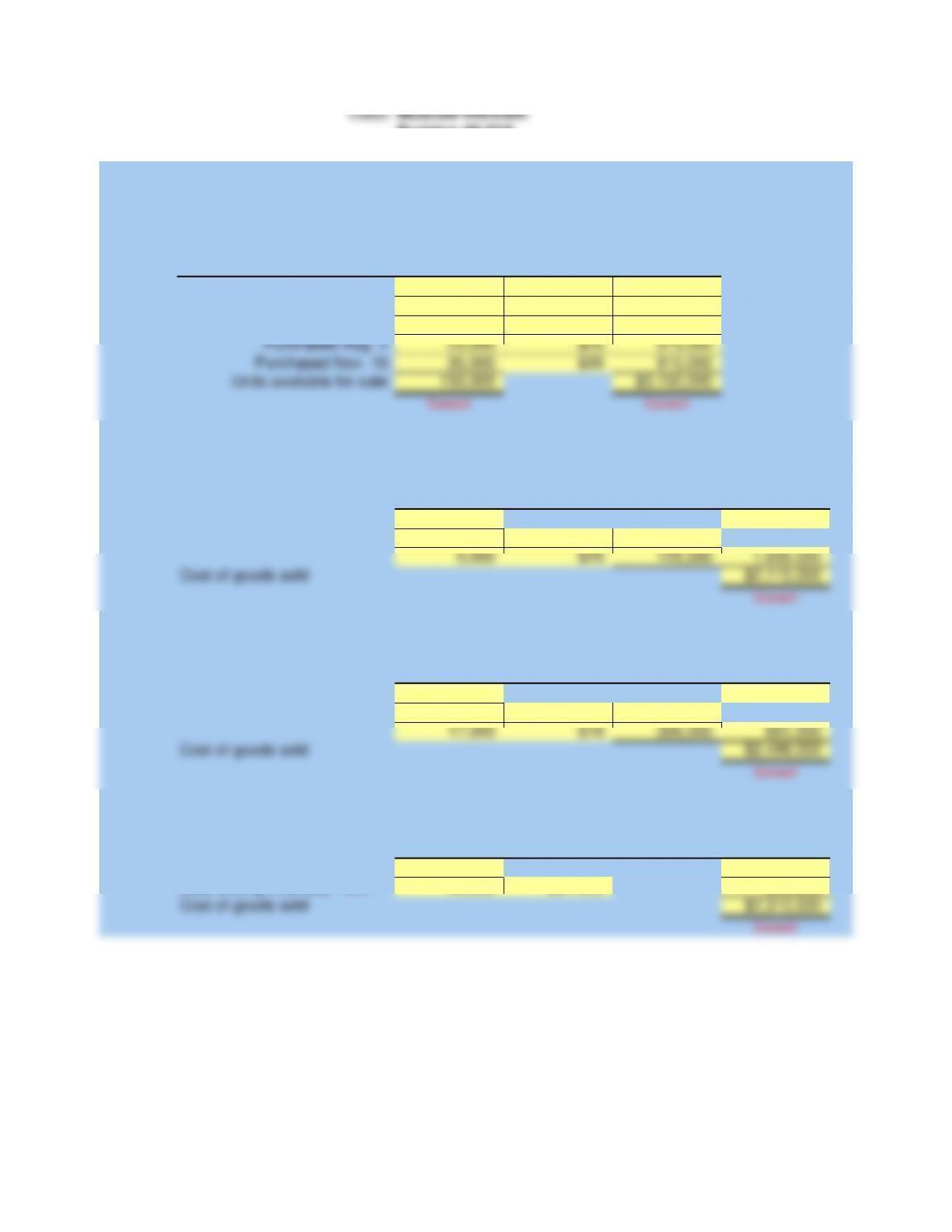

Number and total cost of units available for sale:

Unit Total

Units Cost Cost

23,000 $15 $345,000

30,000 $18 540,000

39,000 $20 780,000

23,000 $25 575,000

35,000 $26 910,000

150,000 $3,150,000

Correct! Correct!

Unit Total

Units Cost Cost

150,000 $3,150,000

35,000 $26 910,000

5,000 $25 125,000 1,035,000

$2,115,000

Correct!

Unit Total

Units Cost Cost

(b) LIFO periodic:

Total cost of units available

23,000 $15 345,000

17,000 $18 306,000 651,000

$2,499,000

Correct!

Unit Total

Units Cost Cost

Total cost of units available

Less ending inventory – WA

$2,310,000

Correct!

Instructor

Inventory

SEMINOLE COMPANY

Problem 06-07A

McGraw-Hill/Irwin

Less ending inventory – LIFO

Beginning inventory:

(a) FIFO periodic:

(c) Weighted-average periodic:

Total cost of units available

Less ending inventory – FIFO

Cost of goods sold

Units available for sale:

Purchased Nov. 10:

Purchased Aug. 1:

Purchased May 25:

Purchased Mar. 7:

Cost of goods sold

Cost of goods sold

23,000

15$

Units Cost

30,000 18$

39,000 20$

23,000 25$

35,000 26$

40,000

2,155,000$

2,499,000$

2,310,000$

SEMINOLE COMPANY

Given Data P06-07A:

Units in beginning inventory

Cost of each unit

Check figures:

(2) Cost of goods sold: FIFO

Cost of goods sold: LIFO

Cost of goods sold: Weighted average

Purchases:

May 25

Aug. 1

Nov. 10

Ending units in inventory, Dec. 31

Mar. 7