Title: Problem 9-2B

QA_Ori:

2013

e. Accounts Receivable………………………………………. 870,220

Sales………………………………………………………. 870,220

f. Cash…………………………………………………………….. 990,800

g. Allowance for Doubtful Accounts……………………… 11,090

h. Bad Debts Expense……………………………………….. 9,773

*Beginning receivables…..…………………….. $ 193,670

Credit sales…..………….……………….……….. 870,220

Collections….……………….…………………….. (990,800)

Title: Problem 9-3B

QA_Ori:

Part 1

a. Expense is 2.5% of credit sales

Dec. 31 Bad Debts Expense……………………………………….. 33,550

b. Expense is 1.5% of total sales

Dec. 31 Bad Debts Expense………………………………………. 35,505

c. Allowance is 6% of accounts receivable

Dec. 31 Bad Debts Expense……………………………………….. 27,000

Part 2

Current assets

Part 3

Current assets

** See computations in Part 1c.

Title: Problem 9-4B

QA_Ori:

Part 1

Calculation of the estimated balance of the allowance

Not due: $396,400 x .020 = $ 7,928

1 to 30: 277,800 x .040 = 11,112

Part 2

Dec. 31 Bad Debts Expense……………………………………… 31,390

*.Unadjusted balance……….….….………..$ 3,400 debit

Part 3

Writing off the account receivable in 2014 will not directly affect Year 2014 net

income. The entry to write off an account involves a debit to Allowance for

Title: Problem 9-5B

Part 1

QA_Ori:

Nov. 1 Notes Receivable—S. Julian………………………………. 4,800

Dec. 31 Interest Receivable……………………………………………. 64

2013

Jan. 30 Cash………………………………………………………………… 4,896

Feb. 28 Notes Receivable—King Co……………………………….. 12,600

Mar. 1 Notes Receivable—M. Shelley……………………………. 6,200

30 Accounts Receivable—King Co…………………………… 12,684

Interest Revenue………………………………………….. 84

Apr. 30 Cash………………………………………………………………… 6,324

Interest Revenue………………………………………….. 124

Title: Problem 9-5B

QA_Ori:

Part 1

June 15 Notes Receivable—R. Solon…………………………….. 2,000

June 21 Notes Receivable—J. Felton…………………………….. 9,500

Aug. 14 Cash……………………………………………………………… 2,034

Interest Revenue*………………………………………. 34

Sept. 19 Cash……………………………………………………………… 9,690

Interest Revenue*………………………………………. 190

Nov. 30 Allowance for Doubtful Accounts……………………….. 12,684

Part 2

Analysis Component: When a business pledges its receivables as security for a

loan and the loan is still outstanding at period-end, the business must disclose

this information in notes to its financial statements. This is a requirement

Title: Serial Problem — SP 9, Success Systems

QA_Ori:

1. a. Bad debts expense is recorded as 1% of total revenues:

2014

1. b. Bad debts expense is recorded as 2% of accounts receivable:

2014

Instructor note: It might help to stress that the beginning balance for the Allowance for Doubtful

Accounts is zero, which is unusual and exists because this is the first period that the company applies

the allowance method.

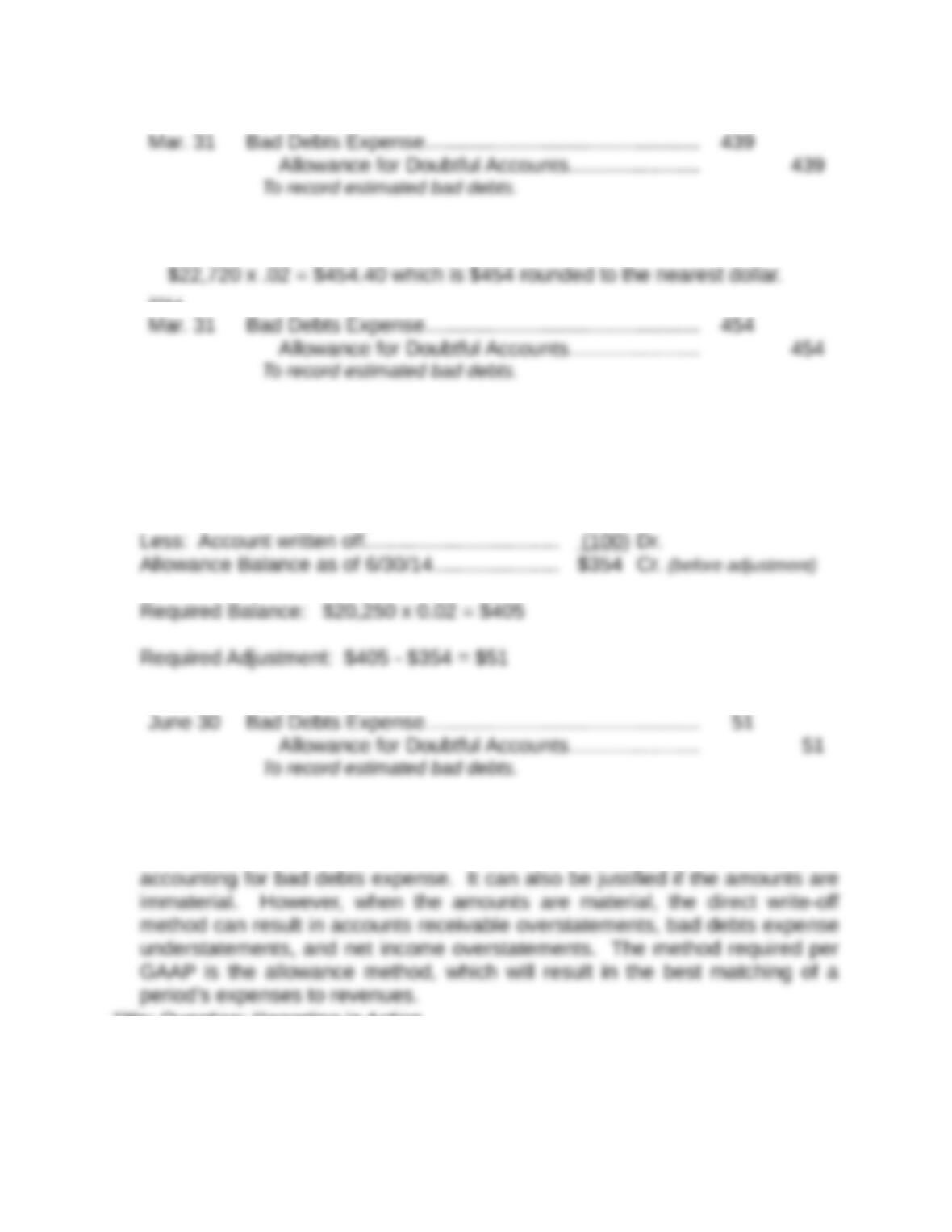

2. Allowance Balance as of 3/31/14…………………. $454 Cr.

2014

3. Many small business owners use the direct write-off method of recording bad

debts expense. The direct method is a simple and straightforward method of

Title: Question: Reporting in Action

Title: Question 1

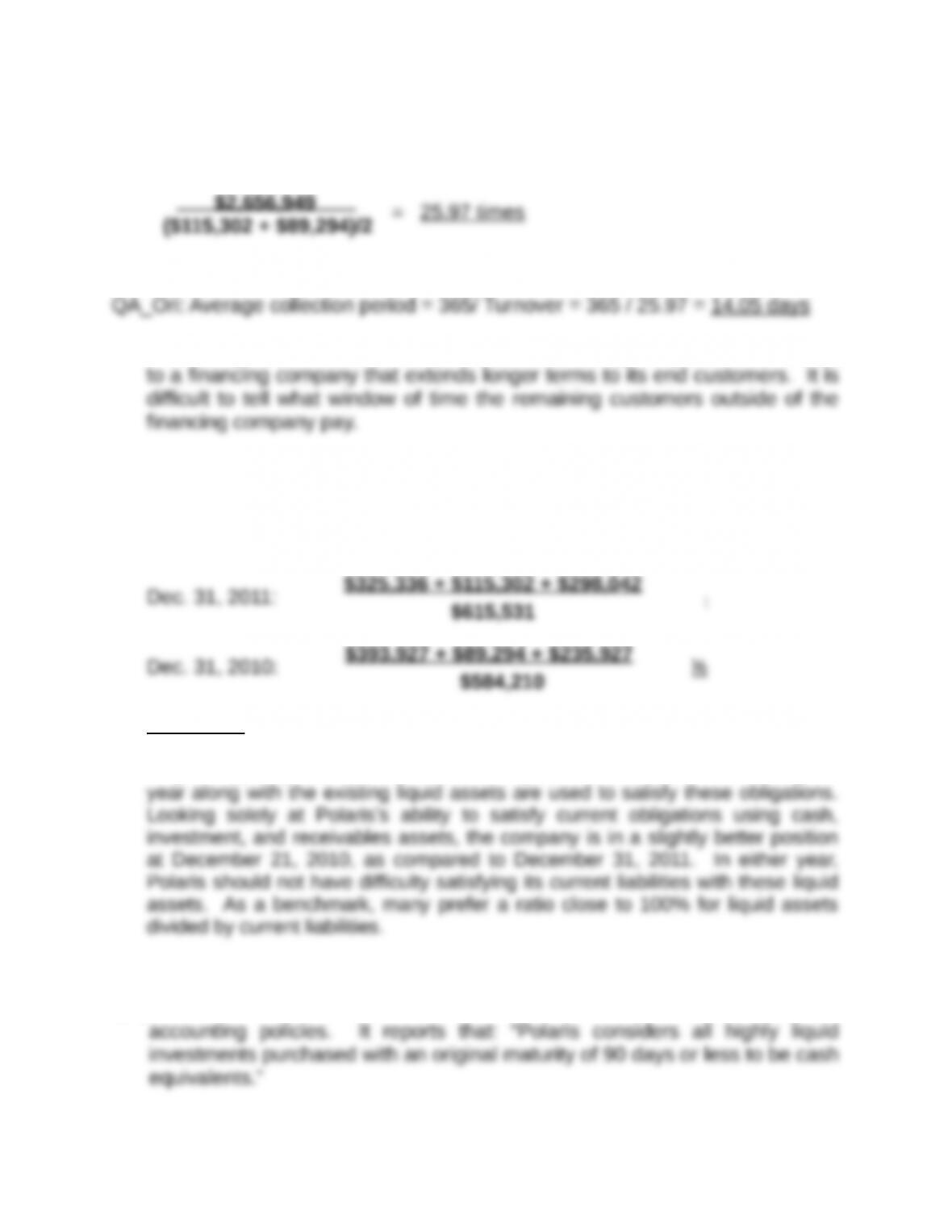

QA_Ori: Polaris’s receivables at December 31, 2011, are $115,302 thousand.

Title: Question 2

QA_Ori:

Accounts receivable turnover for 2011 ($ thousands)

Title: Question 3

This time period is about ~15 days because Polaris typically sells its products

Title: Question 4

QA_Ori:

Liquid assets as a percent of current liabilities ($ thousands)

Comments: Current liabilities are obligations that are due to be paid or

liquidated within one year or one operating cycle of the business, whichever is

longer. Typically, cash provided from the operations of the business during the

Title: Question 5

QA_Ori: Note 1 to Polaris’s financial statements describes its significant

Title: Question 6

QA_Ori: Solution depends on the financial statement information obtained.

Title: Comparative Analysis

Title: Question 1

QA_Ori:

Accounts Receivable Turnover ($ thousands)

Polaris (Current Year):

Polaris (Prior Year):

Arctic Cat (Current Year): = 17.55 times

Arctic Cat (Prior Year): = 13.36 times

Title: Question 2

QA_Ori:

Average Collection Period (or “Average Days’ Sales Uncollected”)

Interpretation: The average collection period for Polaris is shorter than Arctic

1. Both companies appear reasonably efficient in collecting accounts

receivable. Arctic Cat collects them over a longer period of time in both