14-1

Chapter 14

Long-Term Liabilities

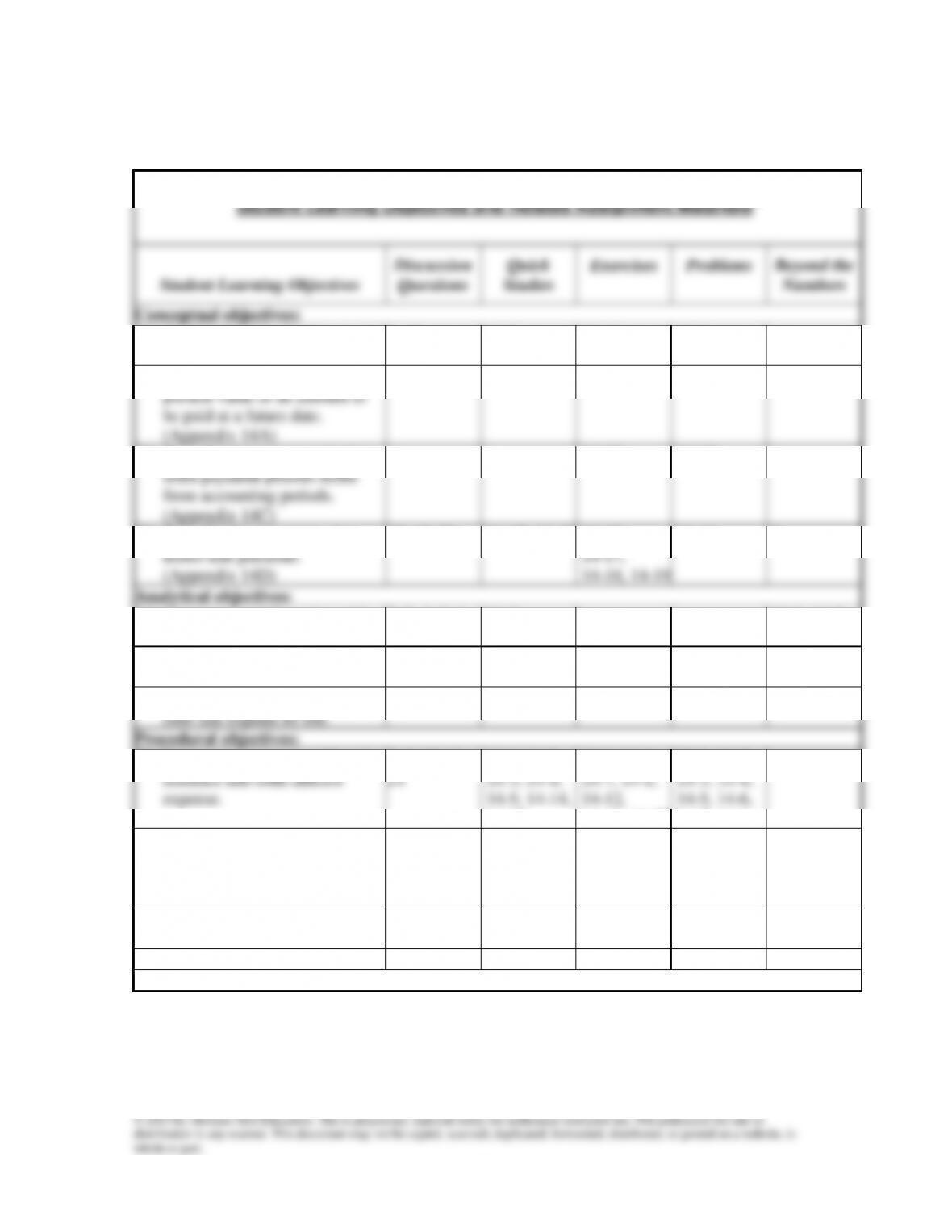

Student Learning Objectives and Related Assignment Materials*

Student Learning Objectives

Discussion

Questions

Quick

Studies

Exercises

Problems

Beyond the

Numbers

Conceptual objectives:

C1. Explain the types and payment

patterns of notes.

1, 12

14-8

14-14

14-9

C2. Explain and compute the

present value of an amount to

be paid at a future date.

(Appendix 14A)

14-19

C3. Describe interest accrual when

bond payment periods differ

from accounting periods.

(Appendix 14C)

14-19

14-10

C4. Describe the accounting for

leases and pensions.

(Appendix 14D)

18, 19, 20

14-12, 14-13

14-12,

14-17,

14-18, 14-19

14-11

3

Analytical objectives:

A1. Compare bond financing with

stock financing.

2, 3, 4, 5, 6,

7, 13, 17

14-8

14-1, 14-3,

14-7, 14-8

A2. Assess debt features and their

implications.

16

14-10

14-1, 14-5

A3. Compute the debt-to-equity

ratio and explain its use.

12

14-16

14-10

14-2, 14-9

Procedural objectives:

P1. Prepare entries to record bond

issuance and bond interest

expense.

8, 9, 10, 11,

14

14-1, 14-2,

14-3, 14-4,

14-5, 14-14,

14-15

14-1, 14-6,

14-7, 14-8,

14-12,

14-13, 14-20

14-1, 14-2,

14-3, 14-4,

14-5, 14-6,

14-7, 14-8

P2. Compute and record

amortization of bond discount.

14-1, 14-5,

14-2, 14-6

14-7, 14-9,

14-11,

14-13

14-2, 14-5,

14-6

14-6

P3. Compute and record

amortization of bond premium.

14-5

14-4, 14-8,

14-10

14-2, 14-3,

14-4, 14-6

14-4, 14-6

P4. Record the retirement of bonds.

14-6, 14-7

14-11

This grid is continued on next page

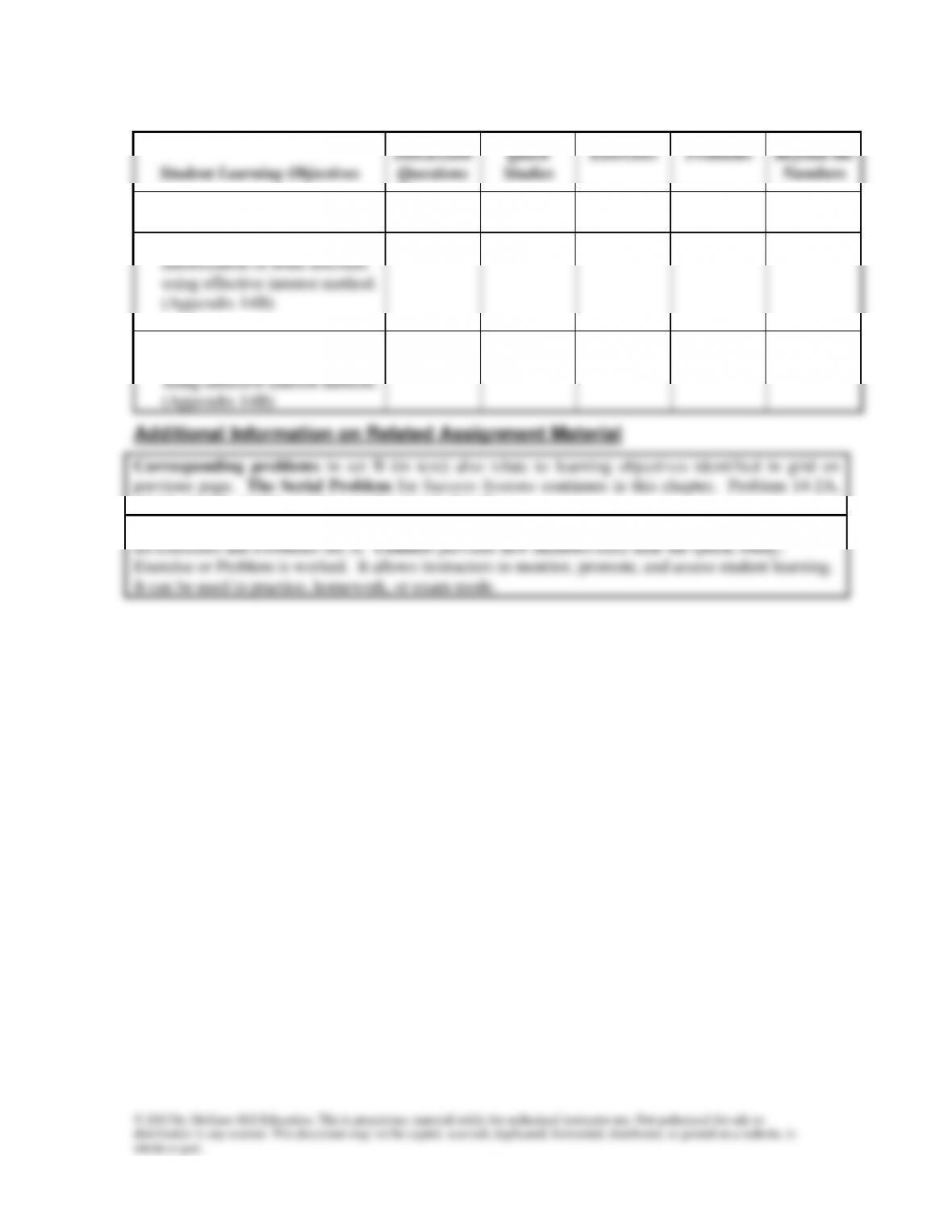

Student Learning Objectives

Discussion

Questions

Quick

Studies

Exercises

Problems

Beyond the

Numbers

P5. Prepare entries to account for

notes.

16

14-14, 14-15

14-8

P6. Compute and record

amortization of bond discount

using effective interest method.

(Appendix 14B)

14-3

14-7, 14-8

P7. Compute and record

amortization of bond premium

using effective interest method.

(Appendix 14B)

14-7

14-5

14-5, 14-8

Synopsis of Chapter Revisions

• barley & birch: NEW opener with new entrepreneurial assignment

• New explanation on why debt (credit) financing is less costly than equity financing

Chapter Outline

Notes

I. Basics of Bonds

Projects that demand large amounts of money often are funded from

bond issuances.

A. Bond Financing

1. A bond is its issuer’s written promise to pay an amount

identified as the par value of the bond with interest.

a. Most bonds require the issuer to make periodic interest

payments.

b. The par value of a bond, also called the face amount or

face value, is paid at a specified future date known as the

maturity date.

2. Advantages of bonds

a. Bonds do not affect owner control.

b. Interest on bonds is tax deductible.

c. Bonds can increase return on equity. A company that earns

a higher return with borrowed funds than it pays in interest

on those funds increases its return on equity. This process is

called financial leverage or trading on the equity.

3. Disadvantages of bonds

a. Bonds can decrease return on equity. A company that earns

a lower return with borrowed funds than it pays in interest

on those funds decreases its return on equity.

b. Bonds require payment of both periodic interest and par

value at maturity. Equity financing, by contrast, does not

require any payments because cash withdrawals (dividends)

are paid at the discretion of the owner (board).

B. Bond Trading

1. Bonds can be traded on exchanges including both the New York

Stock Exchange and the American Stock Exchange.

2. A bond issue consists of a large number of bonds

(denominations of $1,000 or $5,000, etc.) that are sold to many

different lenders.

3. Market value (price) is expressed as a percentage of par (face)

value. Examples: bonds issued at 103 ½ means that they are sold

for 103.5% of their par value. Bonds issued at 95 means that

they are sold for 95% of their par value.

C. Bond-Issuing Procedures

Governed by state and federal laws. Bond issuers also insure they do

not violate any existing contractual agreements.

Chapter Outline

Notes

1. Bond indenture is the contract between the bond issuer and the

bondholders; it identifies the obligations and rights of each

party. A bondholder may also receive a bond certificate that

includes specifics such as the issuer’s name, the par value, the

contract interest rate, and the maturity date.

2. Issuing corporation normally sells its bonds to an investment

firm (the underwriter), which resells the bonds to the public.

3. A trustee (usually a bank or trust company) monitors the issuer

to ensure it complies with the obligations in the indenture.

II. Bond Issuances

A. Issuing Bonds at Par—bonds are sold for face amount.

Entries are:

1. Issue date: debit Cash, credit Bonds Payable (face amount).

2. Interest date: debit Interest Expense, credit Cash (face times

bond interest rate times interest period).

3. Maturity date: debit Bonds Payable, credit Cash (face amount).

B. Bond Discount or Premium—bonds are sold for an amount different

than the face amount.

1. Contract rate—(also called coupon rate, stated rate, or nominal

rate) annual interest rate paid by the issuer of bonds (applied to

par value).

2. Market rate—annual rate borrowers are willing to pay and

lenders are willing to accept for a particular bond and its risk

level.

3. When contract rate and market rate are equal, bonds sell at par

value; when contract rate is above market rate, bonds sell at a

premium (above par); when the contract rate is below market

rate, bonds sell at a discount (below par).

C. Issuing Bonds at a Discount—sell bonds for less than par value.

1. The discount on bonds payable is the difference between the

par (face) value of a bond and its lower issuance price.

2. Entry to record issuance at a discount: debit Cash (issue price),

debit Discount on Bonds Payable (amount of discount), credit

Bonds Payable (par value).

3. Discount on Bonds Payable is a contra liability account; it is

deducted from par value to yield the carrying (book) value of

the bonds payable.

Chapter Outline

Notes

4. Amortizing a Bond Discount

a. Total bond interest expense is the sum of the interest

payments and bond discount (or can be computed by

comparing total amount borrowed to total amount repaid

over life).

b. Discount must be systematically reduced (amortized) over

the life of the bond to report periodic interest expense

incurred.

c. Requires crediting Discount on Bonds Payable when bond

interest expense is recorded (payment and/or accruals) and

increasing Interest Expense by the amortized amount.

d. Amortizing the discount increases book value; at maturity,

the unamortized discount equals zero and the carrying value

equals par value.

5. Straight-line method—allocates an equal portion of the total

discount to bond interest expense in each of the six-month

interest periods.

D. Issuing Bonds at a Premium—sell bonds for more than par value.

1. The premium on bonds payable is the difference between the

par value of a bond and its higher issuance price.

2. Entry to record issuance at a premium: debit Cash (issue price),

credit Premium on Bonds Payable (amount of premium), credit

Bonds Payable (par value).

3. Premium on Bonds Payable is an adjunct liability account; it is

added to par value to yield the carrying (or book) value of the

bonds payable.

4. Amortizing a Bond Premium

a. Total bond interest expense incurred is the interest payments

less the bond premium.

b. Premiums must be systematically reduced (amortized) over

the life of the bond to report periodic interest expense

incurred.

c. Requires debiting Premium on Bonds Payable when bond

interest expense is recorded (payment and/or accruals) and

decreasing Interest Expense by the amortized amount.

d. Amortizing the premium decreases book value; at maturity,

book value = face value.

5. Straight-line method allocates an equal portion of the total

premium to bond interest expense in each of the six-month

interest periods.

E. Bond Pricing

Chapter Outline

Notes

be used to compute price, which is the combination of the:

1. Present Value of a Discount Bond. Present value of the maturity

payment is found by using single payment table, the market rate,

and number of periods until maturity.

2. Present Value of a Premium Bond. Present value of the

semiannual interest payments is found by using annuity table,

the market rate, and number of periods until maturity.

3. Present values found in present value tables in Appendix B at the

end of this book.

III. Bond Retirement

A. Bond Retirement at Maturity

1. Carrying value at maturity will always equal par value.

2. Entry to record bond retirement at maturity: debit Bonds

Payable, credit Cash.

B. Bond Retirement Before Maturity

1. Two common approaches to retire bonds before maturity:

a. Exercise a call option—pay par value plus a call premium.

b. Purchase them on the open market.

2. Difference between the purchase price and the bonds’ carrying

value is recorded as a gain (or loss) on retirement of bonds.

C. Bond Retirement by Conversion

Convertible bondholders have the right to convert their bonds to

stock. If converted, the carrying value of bonds is transferred to

equity accounts and no gain or loss is recorded.

IV. Long-Term Notes Payable

Notes are issued to obtain assets, such as cash. Notes are typically

transacted with a single lender, such as a bank.

A. Installment Notes—obligations requiring a series of periodic

payments to the lender.

1. Entry to record issuance of an installment note for cash: debit

Cash, credit to Notes Payable.

2. Payments include interest expense accruing to the date of the

payment plus a portion of the amount borrowed (principal).

a. Equal total payments consist of changing amounts of interest

and principal.

b. Entry to record installment payment: debit Interest Expense

(issue rate times the declining carrying value of note), debit

Notes Payable (for difference between the equal payment

and the interest expense), credit Cash for the amount of the

equal payment.

Chapter Outline

Notes

B. Mortgage Notes and Bonds

A mortgage is a legal agreement that helps protect a lender if a

borrower fails to make required payments. A mortgage contract

describes the mortgage terms.

1. Accounting for mortgage notes and bonds—same as accounting

for unsecured notes and bonds.

2. Mortgage agreements must be disclosed in financial statements.

V. Global View—Compares U.S.GAAP to IFRS

1. Accounting for Bonds and Notes – The definitions and

characteristics of bonds and notes are broadly similar for both

GAAP and IFRS.

a. Both systems allow companies to account for bonds and notes

using the fair value option method. This method is similar to

that applied to measuring and accounting for debt and equity

securities.

b. Fair value is the amount a company would receive if it

settled a liability in an orderly transaction as of the balance

sheet date.

c. Companies can use several sources of inputs to determine fair

value which fall into three classes:

i. Level 1: observable quoted market price in active markets

for identical items

ii. Level 2: observable inputs other than those in Level 1

iii. Level 3: observable inputs reflecting a company’s

assumptions about value.

2. Accounting for Leases and Pensions – Both GAAP and IFRS

require companies to distinguish between operating leases and

capital leases; the latter is referred to as finance leases under

IFRS. Both systems account for leases in a similar manner. The

main difference is the criteria for identifying a lease as a capital

lease are more general under IFRS.

Chapter Outline

2. Term or Serial

a. Term bonds and notes are scheduled for maturity on one

specified date.

b. Serial bonds and notes mature at more than one date (often in

series) and are usually repaid over a number of periods.

3. Registered or Bearer

a. Registered bonds are issued in the names and addresses of

their holders. Bond payments are sent directly to registered

holders.

b. Bearer bonds, also called unregistered bonds, are made

payable to whoever holds them (the bearer). Many bearer bonds

are also coupon bonds; which are interest coupons that are

attached to the bonds.

4. Convertible and/or Callable

a. Convertible bonds and notes can be exchanged for a fixed

number of shares of the issuing company’s common stock.

b. Callable bonds and notes have an option exercisable by the

issuer to retire them at a stated dollar amount before maturity.

B. Debt-to-Equity Ratio

1. Knowing the level of debt helps in assessing the risk of a

company’s financing structure.

2. A company financed mainly with debt is riskier than a company

financed mainly with equity because liabilities must be repaid.

3. Debt-to-equity ratio measures the risk of a company’s financing

structure.

Notes

4. Debt-to-equity ratio is computed by dividing total liabilities by

A. Present Value Concepts

1. Cash paid (or received) in the future has less value now than the

same amount of cash paid (or received) today.

4. Present Value tables can be used to determine the present value

of future cash payments of a single amount or an annuity.

B. Present Value Tables (Complete tables in Appendix B)

single payment.