23–10

Chapter Outline

Appendix 23A

I. Expanded Overhead Variances

A. Computing Overhead Cost Variances⎯assume predetermined rate is

based on relation between standard overhead and standard labor hours.

1. Framework uses classifications of overhead costs as either variable or

fixed

2. A spending variance results when amount paid to acquire overhead

from actual direct labor hours used; reflects on the cost-effectiveness

in using the overhead allocation base such as direct labor hours.

B. Variable overhead cost variances can be determined by formulas.

Formulas:

Actual Overhead Applied Overhead

AH x AVR AH x SVR SH x SVR

Spending variance Efficiency variance

for the expected production volume.

Notes

23–11

A. Standard cost systems also record standard costs and variances in

accounts.

1. Simplifies recordkeeping

2. Helpful in report preparation.

3. Record standard materials costs incurred:

Goods in Process Inventory SQ x SP

Direct Materials Price Variance

Direct Materials Quantity Variance

Raw Materials Inventory AQ x AP

(the variances are debited if unfavorable or credited if favorable)

4. Record standard labor cost of goods manufactured:

Goods in Process Inventory SQ x SP

Direct Labor Rate Variance

5. Assign standard predetermined overhead to cost of goods

manufactured:

Goods in Process Inventory SQ x SPR

(the variances are debited if unfavorable or credited if favorable)

6. An alternative is to combine the spending and efficiency variances into

one account called “Control Variances”.

7. Accumulate balances in the different variance accounts until end of

GAAP (generally accepted accounting principles).

Notes

23–12

Alternate Demo Problems Twenty-Three

Problem #1

XYZ Company manufactures tables. A standard cost card for the

manufacture of one table shows the following:

Standard Cost per Table:

Direct material: 4 sq. ft. @ $3/sq. ft.

$12

Direct labor: 2 hours @ $8/hr

16

Total prime costs

$28

In November, the company produced 1,000 tables. Actual production costs

and quantities were:

Direct material: 3,900 sq. ft. @ $3.10/sq. ft.

$12

Direct labor: 2,300 hours @ $7.80/hr

16

Required:

Calculate the price and quantity variances for direct material and direct

labor.

23–13

Problem #2

Atlantic Company has the following monthly flexible budget information

based on an expectation of operating at 80% of the factory’s capacity or

10,000 units produced:

Operating Levels

70%

80%

90%

Budgeted output in units

8,000

10,000

12,000

Budgeted labor (standard hours)

16,000

20,000

24,000

Budgeted overhead

Variable overhead

$ 48,000

$60,000

$ 72,000

Fixed overhead

40,000

40,000

40,000

Total overhead

$ 88,000

$100,000

$112,000

During the current month, the company operated at 70% of capacity and

employees worked 16,500 hours and the flowing actual overhead costs

were incurred:

Variable overhead

$ 47,300

Fixed overhead

41,000

Total overhead

$88,300

Required:

1. Compute the predetermined overhead rate per direct labor hour for

variable overhead, fixed overhead, and total overhead.

2. Compute the variable overhead spending and efficiency variances.

3. Compute the fixed overhead spending and volume variance.

23–14

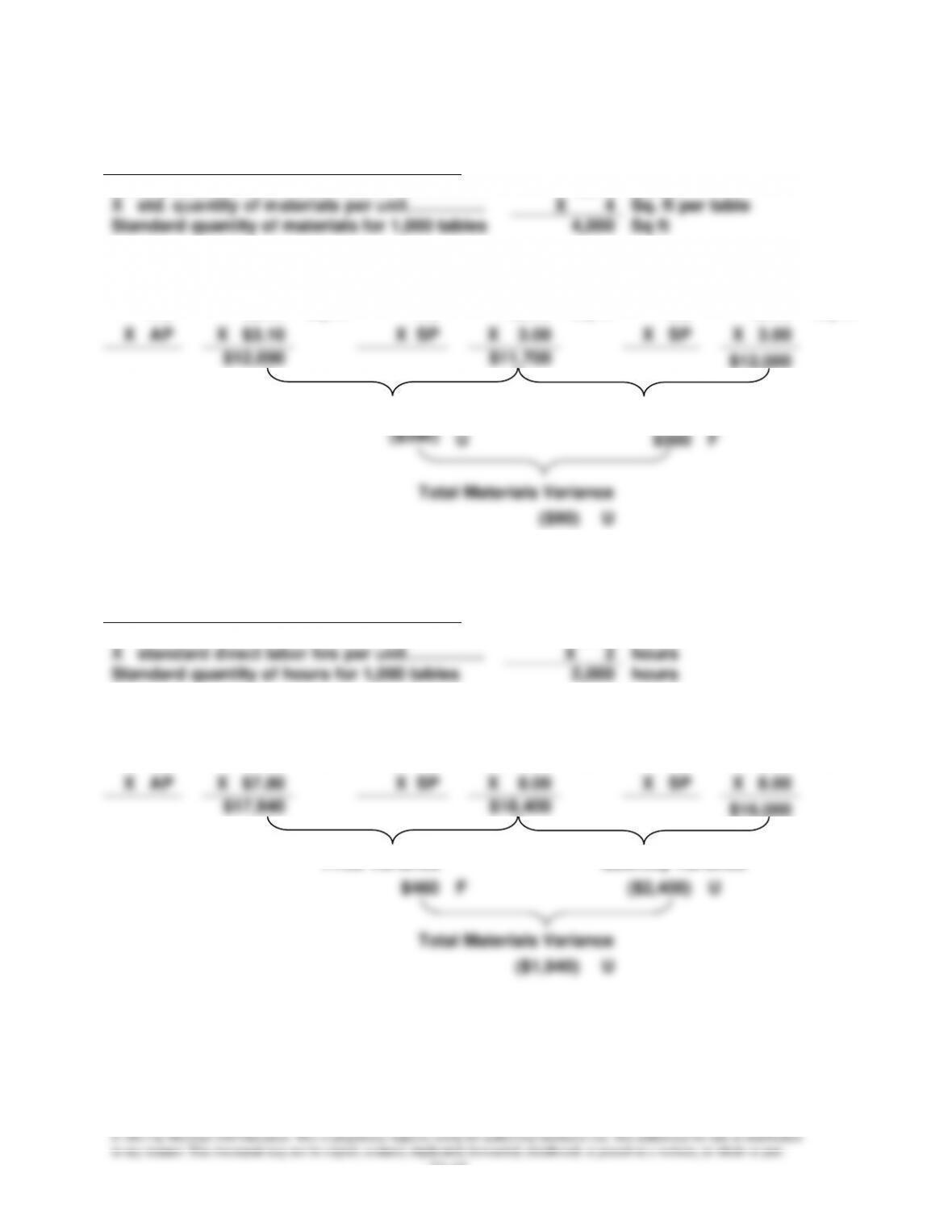

Solution: Problem #1

Materials Variances

Units produced……………………………………..

1,000

tables

X std. quantity of materials per unit…………..

X 4

Sq. ft per table

Standard quantity of materials for 1,000 tables

4,000

Sq ft

AQ

3,900

Sq ft.

AQ

3,900

Sq ft.

SQ

4,000

Sq ft.

X AP

X $3.10

X SP

X 3.00

X SP

X 3.00

$12,090

$11,700

$12,000

Price Variance

Quantity Variance

($390)

U

$300

F

Total Materials Variance

($90)

U

Labor Variances

Units produced……………………………………..

1,000

tables

X standard direct labor hrs per unit…………..

X 2

hours

Standard quantity of hours for 1,000 tables

2,000

hours

AQ

2,300

Hrs.

AQ

2,300

Hrs.

SQ

2,000

Hrs.

X AP

X $7.80

X SP

X 8.00

X SP

X 8.00

$17,940

$18,400

$16,000

Price Variance

Quantity Variance

$460

F

($2,400)

U

Total Materials Variance

($1,940)

U

23–15

Material Variances:

Quantity Variance:

Standard units at standard price

4,000 ft @ $3.00 =

$12,000

Actual units at standard price

3,900 ft @ $3.00 =

11,700

Variance (favorable)

100 ft @ $3.00 =

$ 300

Price Variance:

Actual units at actual price

3,900 ft @ $3.10 =

$12,090

Actual units at standard price

3,900 ft @ $3.00 =

11,700

Variance (unfavorable)

3,900 ft @ $0.10 =

390

Direct material cost variance

(unfavorable)

$ 90

Labor Variances:

Efficiency (Quantity) Variance

Actual hours at standard rate

2,300 hrs. @ $8.00 =

$18,400

Standard hours at standard rate

2,000 hrs. @ $8.00 =

16,000

Variance (unfavorable)

300 hrs. @ $8.00 =

$2,400

Rate (Price) Variance:

Actual hours at standard rate

2,300 hrs. @ $8.00 =

$18,400

Actual hours at actual rate

2,300 hrs. @ $7.80 =

17,940

Variance (favorable)

2,300 hrs. @ $0.20 =

460

Direct labor cost variance

(unfavorable)

$1,940

23–16

Solution: Problem #2

1. Compute the predetermined overhead rates

Overhead at operating level expected (80%) or 10,000 units

Variable Overhead Rate:

Expected Variable Overhead

$ 60,000

=

$ 3.00

per DLH

Expected Direct Labor Hours

20,000

Fixed Overhead Rate:

Expected Fixed Overhead

$ 40,000

=

$ 2.00

per DLH

Expected Direct Labor Hours

20,000

Total Overhead Rate:

Expected Total Overhead

$100,000

=

$ 5.00

per DLH

Expected Direct Labor Hours

20,000

2. Variable Overhead Variance Computations

Actual Variable

Applied Variable

Overhead

Overhead

AH

AH

16,500

SH

16,000

x AVR

x SVR

$ 3.00

x SVR

$ 3.00

total

$47,300

$49,500

$48,000

Variable

Variable

Spending Variance

Efficiency Variance

$ 2,200

F

$(1,500)

U

23–17

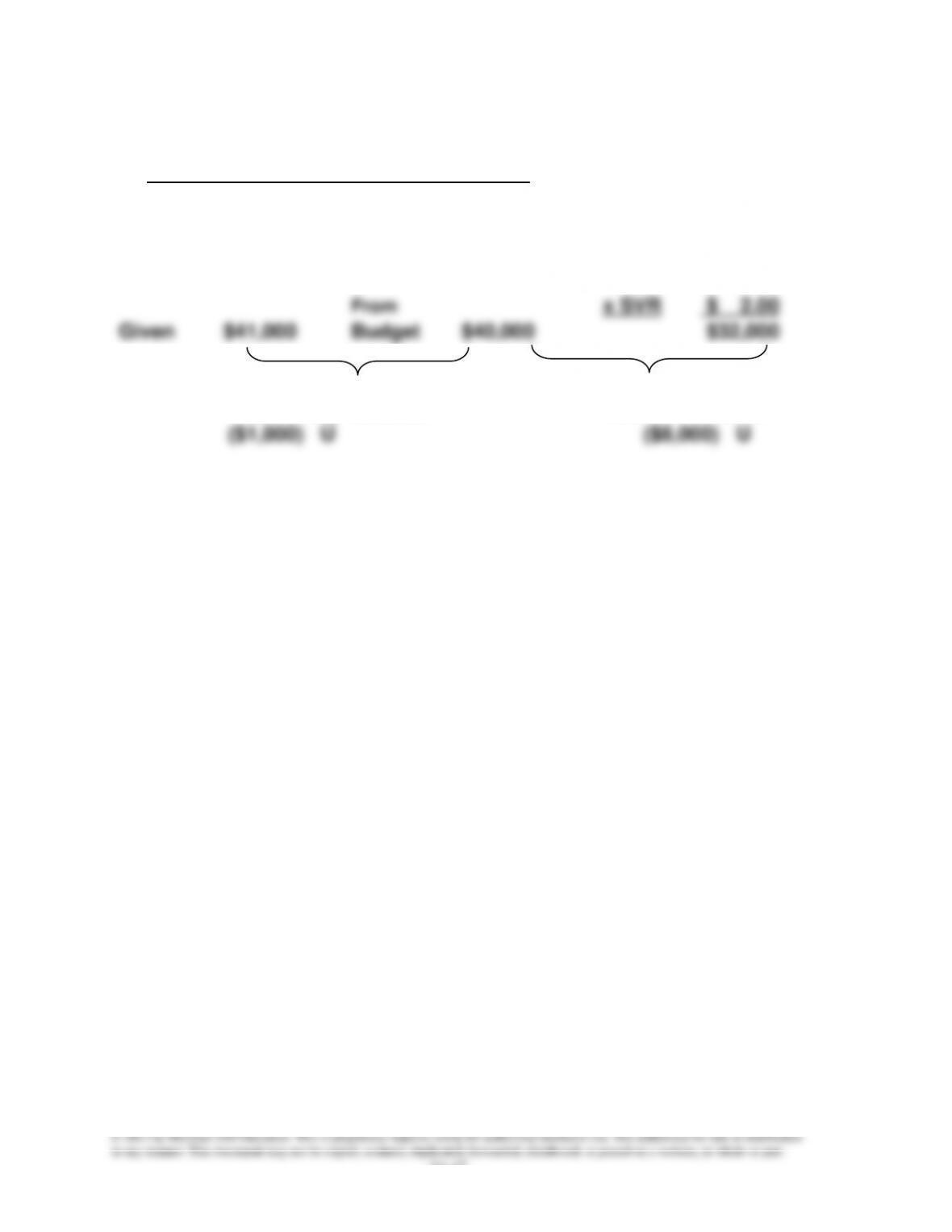

3. Fixed Overhead Variance Computations

Actual Fixed

Applied Fixed

Overhead

Overhead

SH

16,000

From

x SVR

$ 2.00

Given

$41,000

Budget

$40,000

$32,000

Fixed

Fixed

Spending Variance

Volume Variance

($1,000)

U

($8,000)

U