Exercise 3-6 (15 minutes)

a. Supplies expense for current year: $2,550

Proof:

(a)

(b)

(c)

(d)

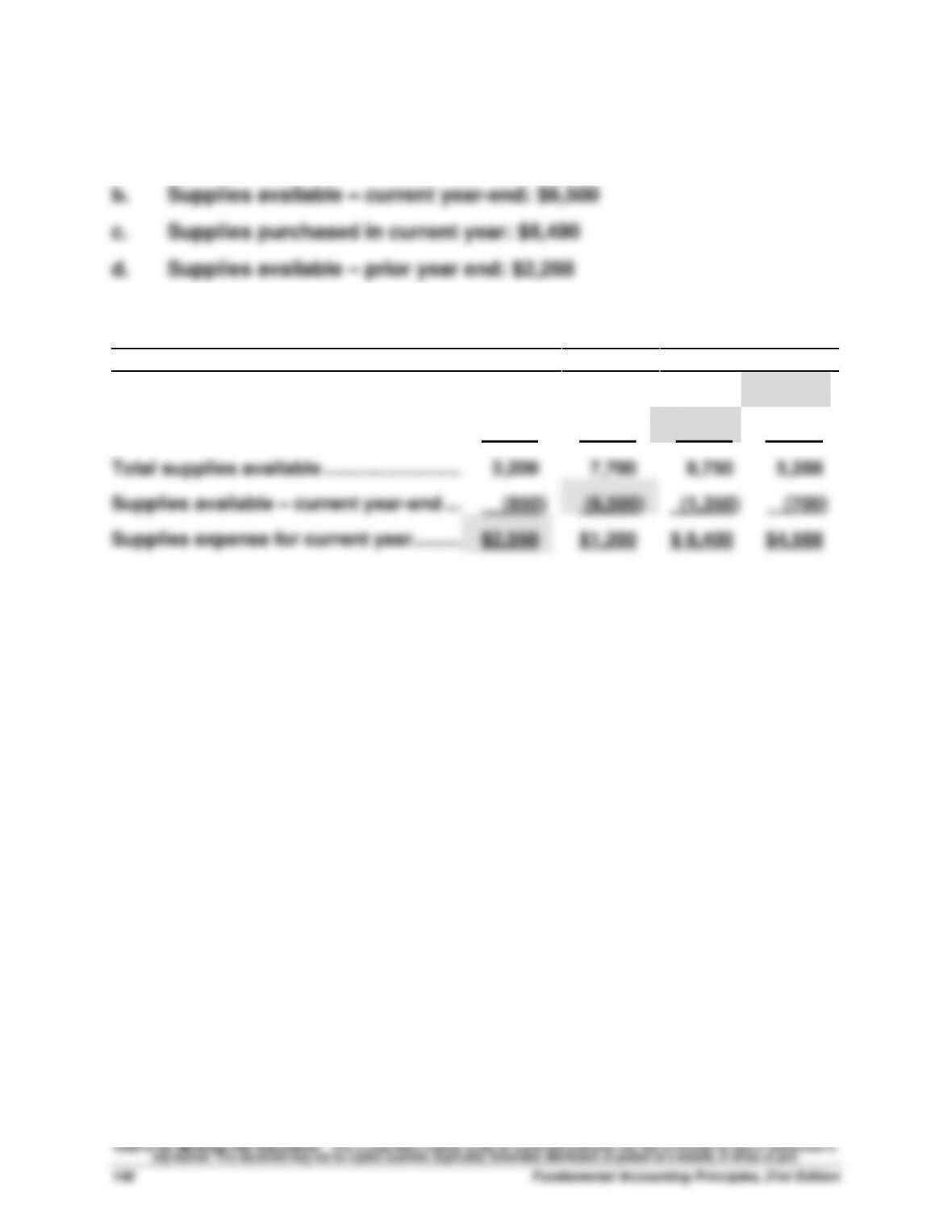

Supplies available – prior year-end ……...

$ 400

$1,200

$ 1,260

$2,288

Supplies purchased in current year ……..

2,800

6,500

8,490

3,000

Total supplies available ……………………….

3,200

7,700

9,750

5,288

Supplies available – current year-end …..

(650)

(6,500)

(1,350)

(700)

Supplies expense for current year………..

$2,550

$1,200

$ 8,400

$4,588

Exercise 3-7 (25 minutes)

Dec. 31 Accounts Receivable ……………………………………… 2,100

Fees Earned …………………………………………….. 2,100

To record earned but unbilled fees (30% x $7,000).

31 Salaries Expense ……………………………………………. 2,250

Salaries Payable………………………………………. 2,250

To record accrued salaries.

31 Insurance Expense ………………………………………….. 1,400

Prepaid Insurance ……………………………………. 1,400

To record expired prepaid insurance.

Exercise 3-8 (20 minutes)

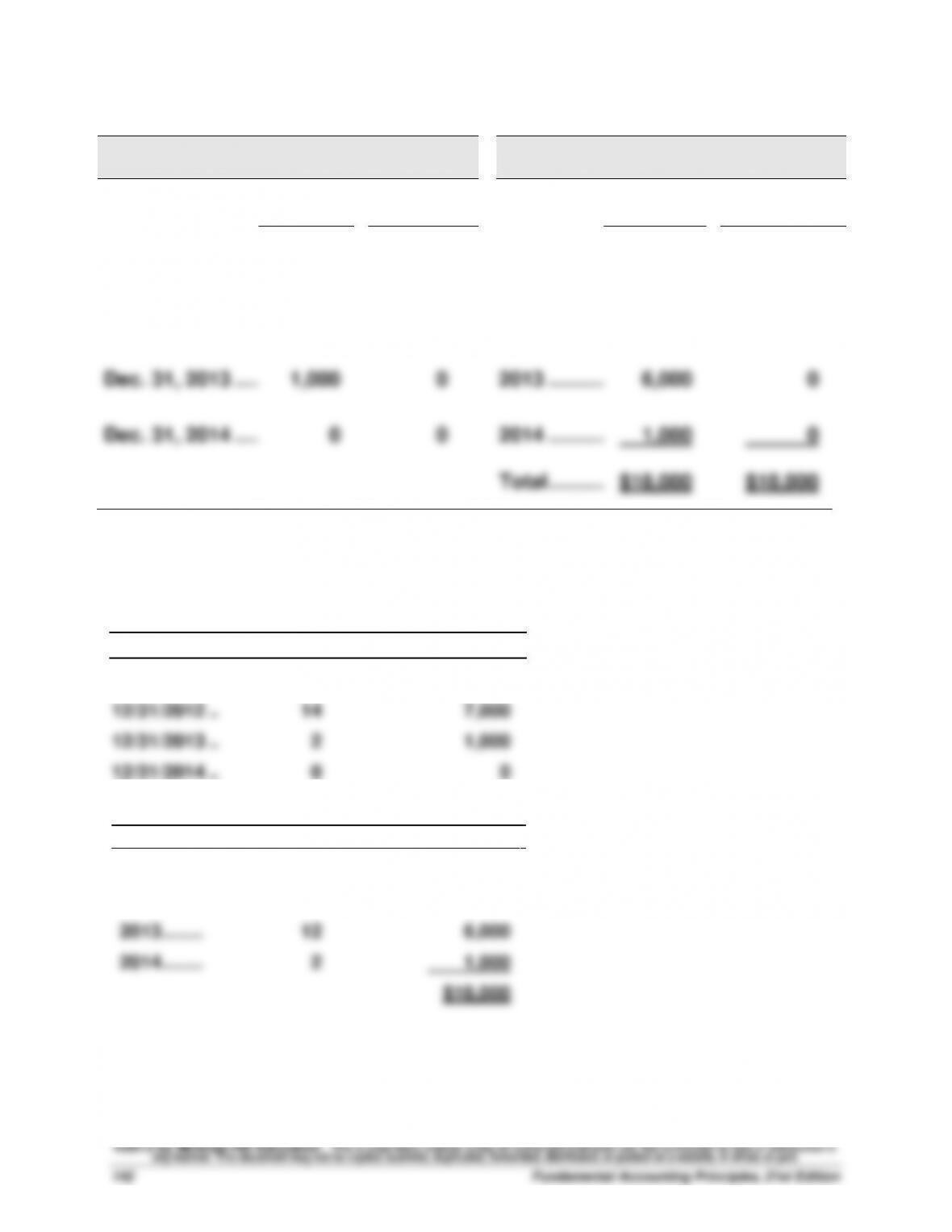

Balance Sheet Insurance Asset using

Insurance Expense using

Accrual

Basis*

Cash

Basis

Accrual

Basis**

Cash

Basis

Dec. 31, 2011 …..………..

$13,000

$0

2011 ……….…………………

$ 5,000

$18,000

Dec. 31, 2012 …..………..

7,000

0

2012 ……….…………………

6,000

0

Dec. 31, 2013 …..………..

1,000

0

2013 ……….…………………

6,000

0

Dec. 31, 2014 …..………..

0

0

2014 ……….…………………

1,000

0

Total ……….…………………

$18,000

$18,000

Explanations:

*Accrual asset balance equals months left in the policy x $500 per month (monthly

cost is computed as $18,000 / 36 months).

Months Left Balance

12/31/2011 .. 26 $13,000

**Accrual insurance expense equals months covered in the year x $500 per month.

Months Covered

Expense

2011 ……..……………………

10

$ 5,000

2012 ……..……………………

12

6,000

2013 ……..……………………

12

6,000

2014 ……..……………………

2

1,000

$18,000

Exercise 3-9 (10 minutes)

a. $ 4,361 / $ 44,500 = 9.8%

b. $ 97,706 / $ 398,800 = 24.5%

Analysis and Interpretation: Company c has the highest profitability

Exercise 3-10A (30 minutes)

a.

Dec. 1 Supplies Expense …………………………………………… 2,000

Cash ……………………………………………………….. 2,000

Purchased supplies.

d.

Dec. 28 Cash ………………………………………………………………. 3,700

Remodeling Fees Earned …………………………. 3,700

Received fees for work to be done.

e.

Dec. 31 Supplies ………………………………………………………… 1,840

Supplies Expense ……………………………………. 1,840

Adjust expenses for unused supplies.

f.

Exercise 3-11A (25 minutes)

a. Initial credit recorded in the Unearned Fees account

July 1 Cash …………………………………………………………….. 3,000

Unearned Fees ………………………………………. 3,000

Received fees for work to be done for Solana.

18 Cash …………………………………………………………….. 8,500

Unearned Fees ………………………………………. 8,500

Received fees for work to be done for Jordan.

b. Initial credit recorded in the Fees Earned account

July 1 Cash …………………………………………………………….. 3,000

Fees Earned …………………………………………… 3,000

Received fees for work to be done for Solana.

12 No entry required.

18 Cash …………………………………………………………….. 8,500

Fees Earned …………………………………………… 8,500

Received fees for work to be done for Jordan.

27 No entry required.

Exercise 3-11A –concluded

c. Under the first method (and using entries from a)

Unearned Fees = $3,000 + $7,500 – $3,000 + $8,500 – $7,500 = $8,500

Under the second method (and using entries from b)

Unearned Fees = $8,500

Exercise 3-12 (20 minutes)

adidas AG

Balance Sheet

December 31, 2011

(Euros in millions)

Assets

Noncurrent assets

Intangible assets …………………………………………… € 154

Tangible and other assets ……………………………… 255

Other noncurrent assets ………………………………… 3,429

Total noncurrent assets …………………………………. 3,838

Current assets

Total assets …………………………………………………….. € 6,046

Equity

Total equity …………………………………………………….. € 2,322

Liabilities

Total noncurrent liabilities ………………………………. 3,379

PROBLEM SET A

Problem 3-1A (10 minutes)

1. E 5. C 9. D

Problem 3-2A (35 minutes)

Part 1

Adjustment (a)

Dec. 31 Office Supplies Expense ………………………….. 14,846

($4,000 + $13,400 – $2,554).

Adjustment (b)

31 Insurance Expense …………………………………… 7,120

Policy

Cost per Month

Months Active

in 2013

2013 Cost

A

$600

($14,400/24 mo.)

3

$ 1,800

B

360

($12,960/36 mo.)

12

4,320

C

200

($ 2,400 /12 mo.)

5

1,000

Total

$ 7,120

Instructor note: The first printing of the book had a typo in the marginal check

figure of 11,440 for Insurance Expense instead of the correct 7,120.

Adjustment (c)

31 Salaries Expense ……………………………………… 3,920

Problem 3-2A −concluded

Adjustment (d)

Dec. 31 Depreciation Expense—Building ………………. 30,500

Accumulated Depreciation—Building … 30,500

To record annual depreciation expense

[($960,000 -$45,000) / 30 years = $30,500]

Adjustment (e)

To record earned but unpaid Dec. rent.

Adjustment (f)

Part 2

Cash Payment for (c)

Jan. 6 Salaries Payable …………………………..……….. 3,920

Salaries Expense* …………………………………. 5,880

Cash ………………………………………………. 9,800

To record payment of accrued and

current salaries. *(3 days x $1,960)

Cash Payment for (e)

Problem 3-3A (90 minutes)

Parts 1 and 2

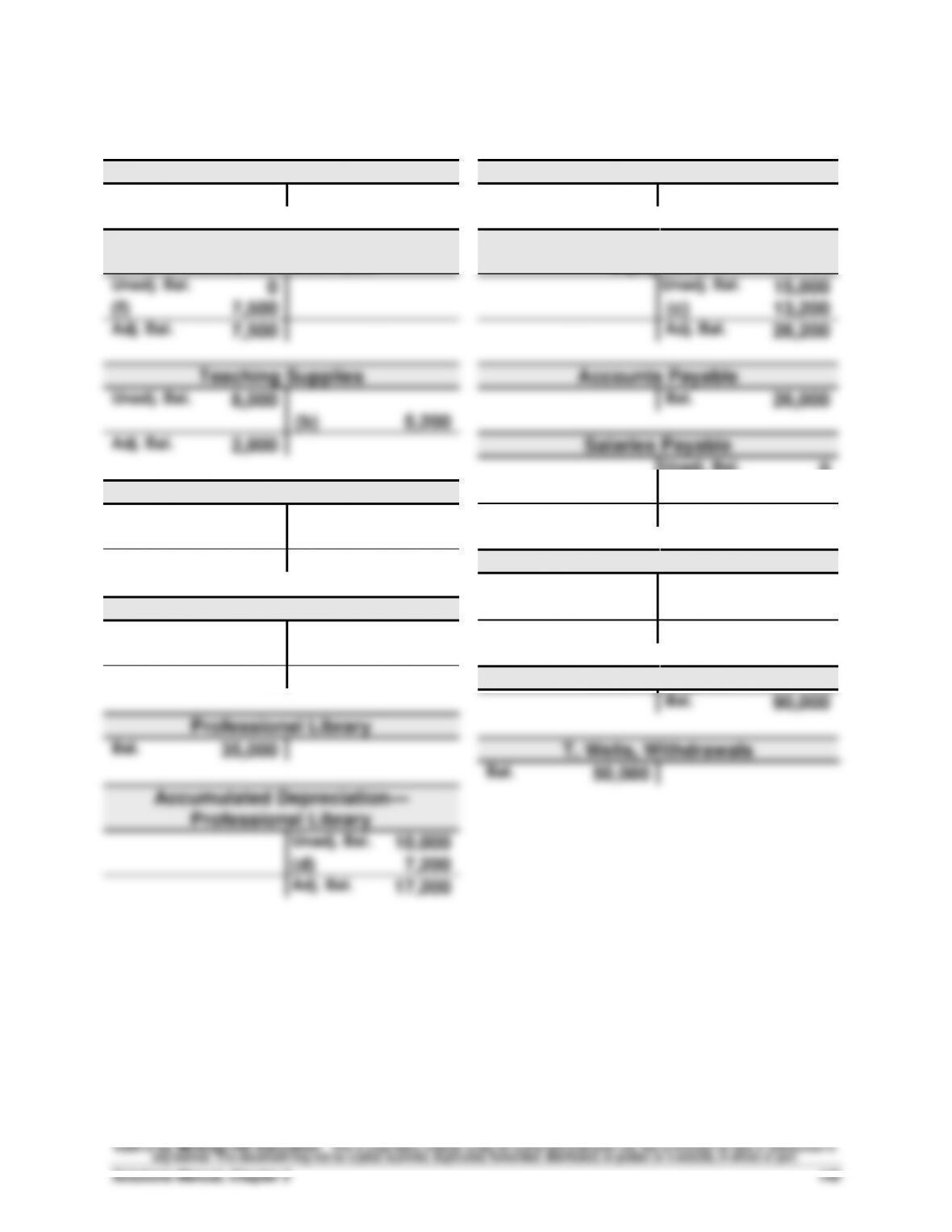

Cash

Equipment

Unadj. Bal.

34,000

Unadj. Bal.

80,000

Accounts Receivable

Accumulated Depreciation—

Equipment

Unadj. Bal.

0

Unadj. Bal.

15,000

(f)

7,500

(c)

13,200

Adj. Bal.

7,500

Adj. Bal.

28,200

Teaching Supplies

Accounts Payable

Unadj. Bal.

8,000

Bal.

26,000

(b)

5,200

Adj. Bal.

2,800

Salaries Payable

Unadj. Bal.

0

Prepaid Insurance

(g)

400

Unadj. Bal.

12,000

Adj. Bal.

400

(a)

2,400

Adj. Bal.

9,600

Unearned Training Fees

Unadj. Bal.

12,500

Prepaid Rent

(e)

5,000

Unadj. Bal.

3,000

Adj. Bal.

7,500

(h)

3,000

Adj. Bal.

0

T. Wells, Capital

Bal.

90,000

Professional Library

Bal.

35,000

T. Wells, Withdrawals

Bal.

50,000

Accumulated Depreciation—

Professional Library

Unadj. Bal.

10,000

(d)

7,200

Adj. Bal.

17,200

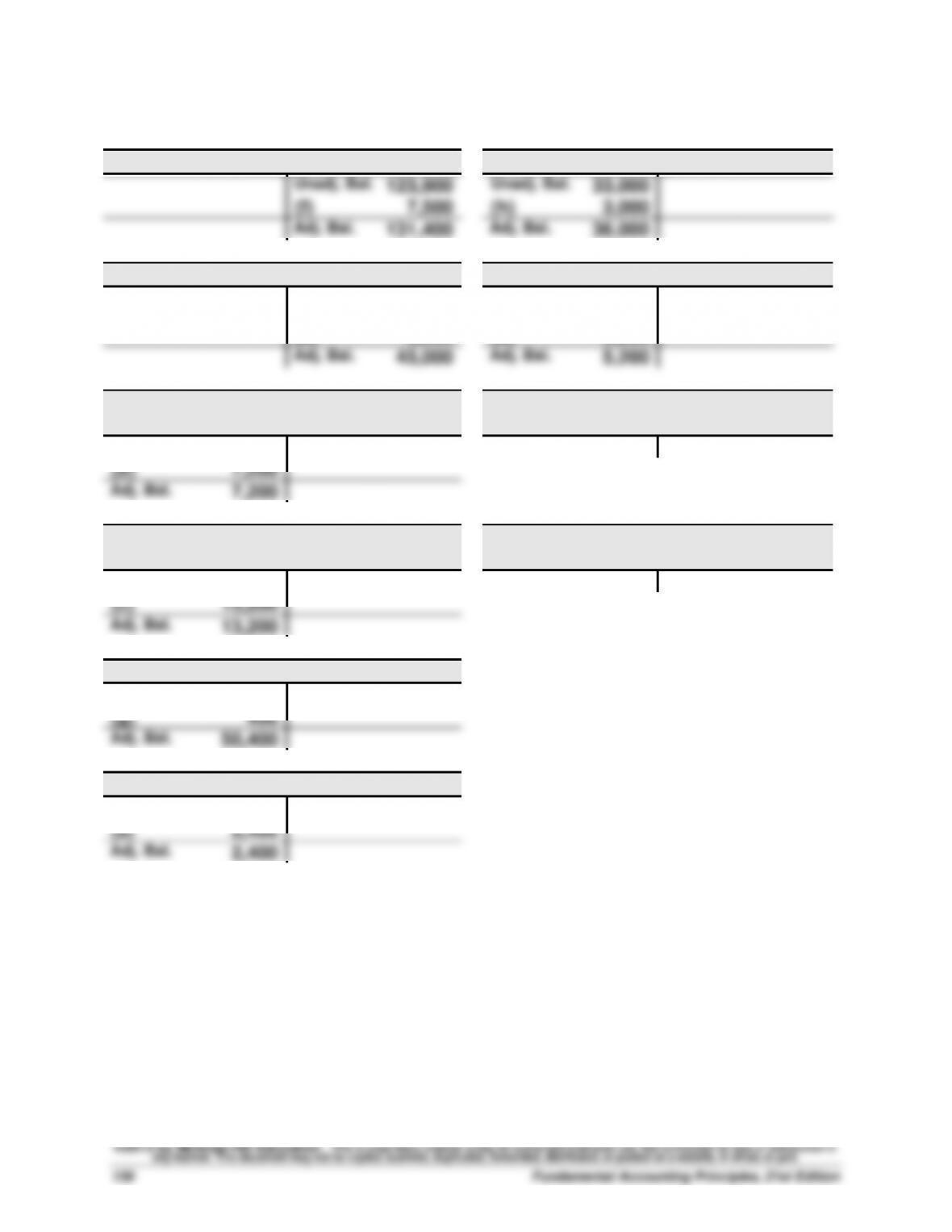

Problem 3-3A (Continued)

Tuition Fees Earned

Rent Expense

Unadj. Bal.

123,900

Unadj. Bal.

33,000

(f)

7,500

(h)

3,000

Adj. Bal.

131,400

Adj. Bal.

36,000

Training Fees Earned

Teaching Supplies Expense

Unadj. Bal.

40,000

Unadj.

Bal.

0

(e)

5,000

(b)

5,200

Adj. Bal.

45,000

Adj. Bal.

5,200

Depreciation Expense—

Professional Library

Advertising Expense

Unadj. Bal.

0

Bal.

6,000

(d)

7,200

Adj. Bal.

7,200

Depreciation Expense—

Equipment

Utilities Expense

Unadj. Bal.

0

Bal.

6,400

(c)

13,200

Adj. Bal.

13,200

Salaries Expense

Unadj. Bal.

50,000

(g)

400

Adj. Bal.

50,400

Insurance Expense

Unadj. Bal.

0

(a)

2,400

Adj. Bal.

2,400

Problem 3-3A (Continued)

Part 2

Adjustment (a)

Dec. 31

Insurance Expense …………………………………….………..

2,400

Prepaid Insurance …………………………………………..

2,400

To record the insurance expired.

Adjustment (b)

31

Teaching Supplies Expense ……………………….….

5,200

Teaching Supplies ………………………………..………..

5,200

To record supplies used ($8,000 – $2,800).

Adjustment (c)

31

Depreciation Expense—Equipment …………….………..

13,200

Accumulated Depreciation—Equipment ……..…………

13,200

To record equipment depreciation.

Adjustment (d)

31

Depreciation Expense—Profess. Library …….………..

7,200

Accumul. Depreciation—Profess. Library …..………..

7,200

To record professional library depreciation.

Adjustment (e)

31

Unearned Training Fees …………………………..…………..

5,000

Training Fees Earned ……………………………………..

5,000

To record 2 months’ training fees earned

that were collected in advance.

Adjustment (f)

31

Accounts Receivable ………………………………….………..

7,500

Tuition Fees Earned………………………………………..

7,500

To record tuition earned

($3,000 x 2 1/2 months).

Adjustment (g)

31

Salaries Expense ……………………………………….………..

400

Salaries Payable……………………………………………..

400

To record accrued salaries

(2 days x $100 x 2 employees).

Adjustment (h)

31

Rent Expense …………………………………………….………..

3,000

Prepaid Rent …………………………………………………..

3,000

To record expiration of prepaid rent.

Problem 3-3A (Continued)

Part 3

WELLS TECHNICAL INSTITUTE

Adjusted Trial Balance

December 31, 2013

Debit

Credit

Cash ………………………………………………………………..

$ 34,000

Accounts receivable …………………………..…………….

7,500

Teaching supplies ……………………………………………

2,800

Prepaid insurance …………………………………………….

9,600

Prepaid rent ……………………………………………………..

0

Professional library ………………………………………….

35,000

Accumulated depreciation—Professional library …

$ 17,200

Equipment …………………………..…………………………..

80,000

Accumulated depreciation—Equipment …………….

28,200

Accounts payable …………………………………………….

26,000

Salaries payable ……………………………………………….

400

Unearned training fees …………………………..…………

7,500

T. Wells, Capital ……………………………………………….

90,000

T. Wells, Withdrawals ……………………………………….

50,000

Tuition fees earned …………………………………………..

131,400

Training fees earned …………………………………………

45,000

Depreciation expense—Professional library ……..

7,200

Depreciation expense—Equipment …………………..

13,200

Salaries expense ……………………………………………..

50,400

Insurance expense …………………………………………..

2,400

Rent expense …………………………..……………………….

36,000

Teaching supplies expense ………………………………

5,200

Advertising expense …………………………………………

6,000

Utilities expense……………………………………………….

6,400

_______

Totals …………………………..………………………………….

$345,700

$345,700

Problem 3-3A (Continued)

Part 4

WELLS TECHNICAL INSTITUTE

Income Statement

For Year Ended December 31, 2013

Revenues

Tuition fees earned …………………………………….. $131,400

Training fees earned …………………………………… 45,000

Total revenues ……………………………………………. $176,400

Expenses

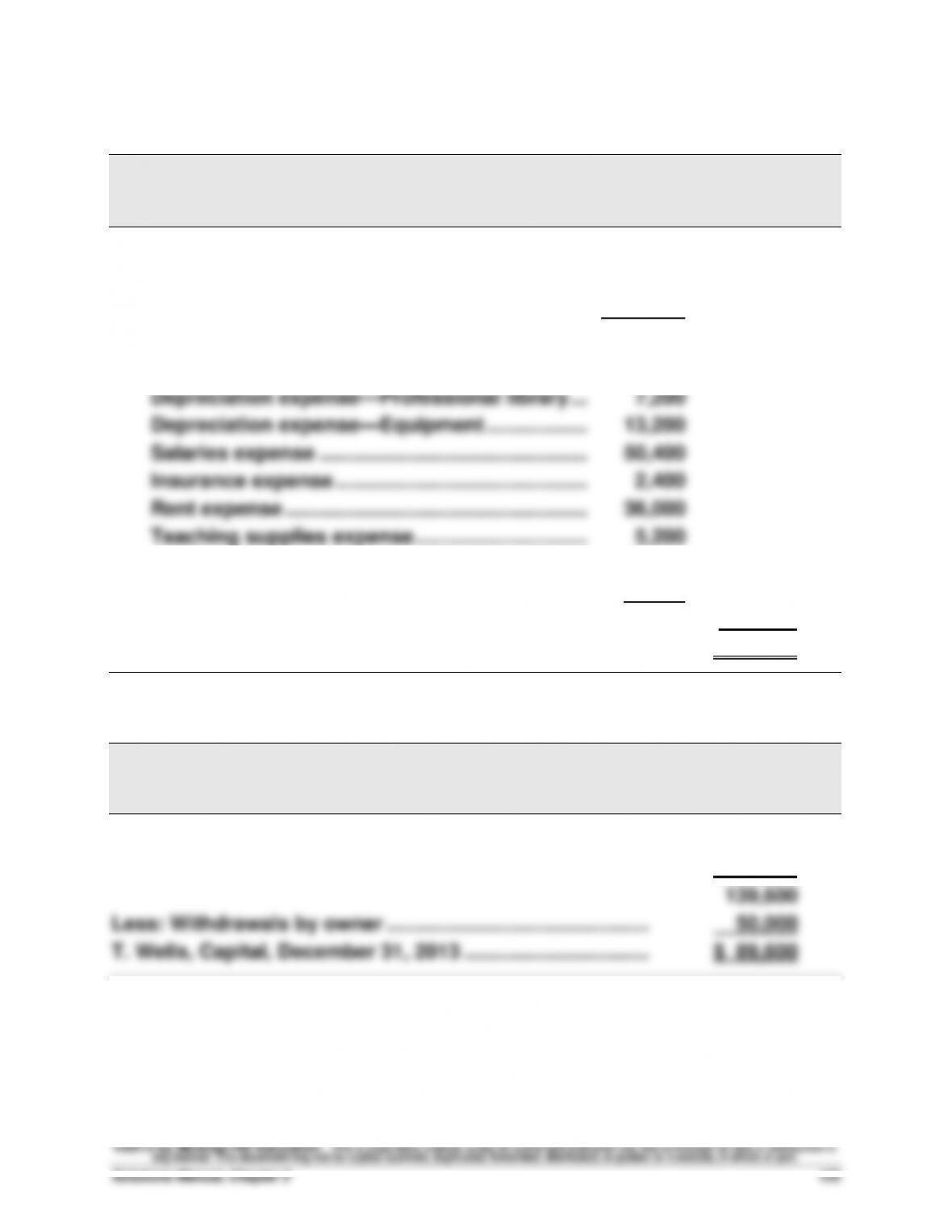

Advertising expense …………………………………… 6,000

Utilities expense …………………………………………. 6,400

Total expenses …………………………………………… 126,800

Net income …………………………..………………………. $ 49,600

WELLS TECHNICAL INSTITUTE

Statement of Owner’s Equity

For Year Ended December 31, 2013

T. Wells, Capital, December 31, 2012 …………………………... $ 90,000

Plus: Net income ………………………………………………………… 49,600

Problem 3-3A (Concluded)

WELLS TECHNICAL INSTITUTE

Balance Sheet

December 31, 2013

Assets

Cash ……………………………………………………………………… $ 34,000

Accounts receivable ……………………………………………… 7,500

Teaching supplies …………………………………………………. 2,800

Prepaid insurance …………………………..…………………….. 9,600

Liabilities

Total liabilities ………………………………………………………. 33,900

Equity

T. Wells, Capital …………………………………………………….. 89,600

Total liabilities and equity ……………………………………… $123,500