Title: Problem 14-8A

QA_Ori:

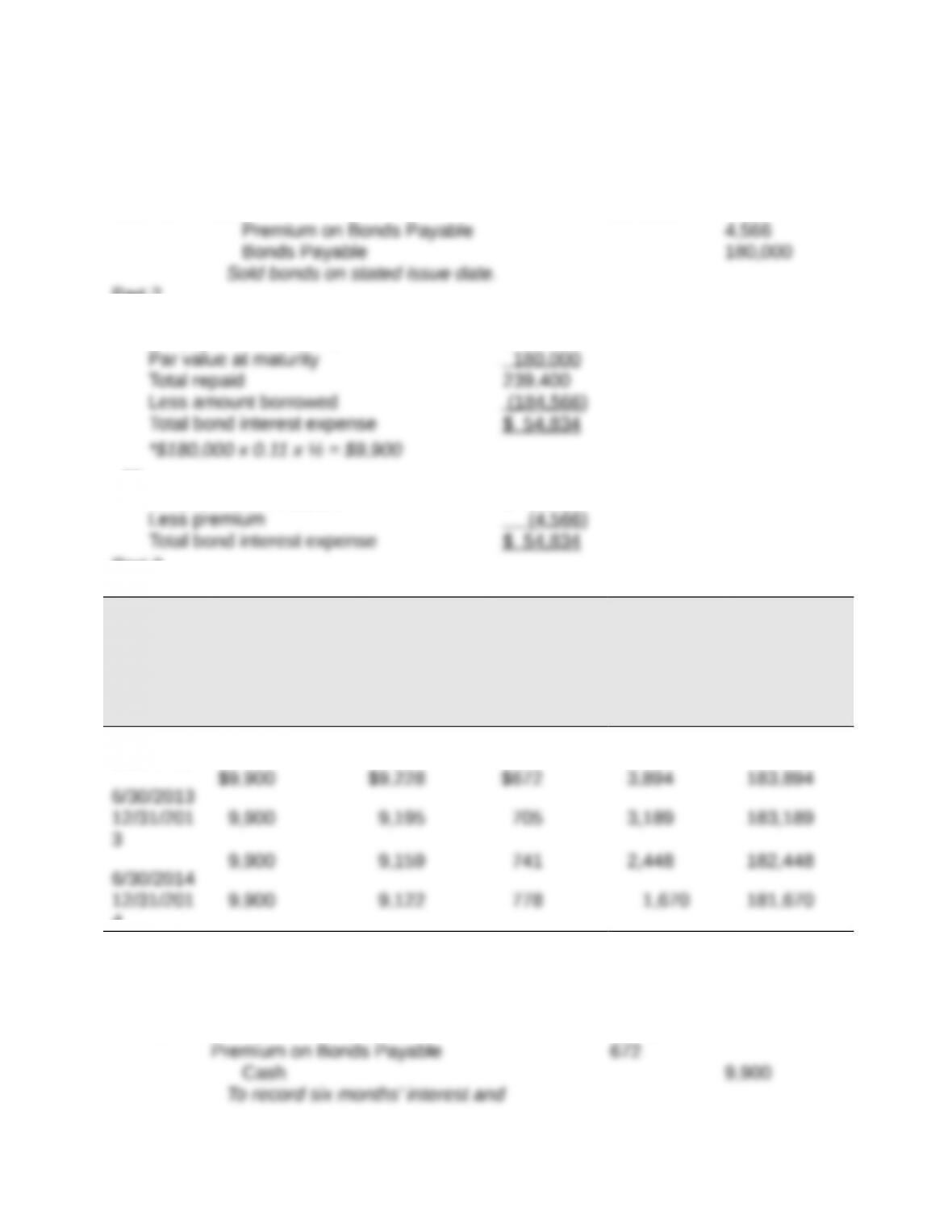

Part 1

2013

Jan. 1 Cash 184,566

Part 2

Six payments of $9,900 $ 59,400

or:

Six payments of $9,900 $ 59,400

Part 3

Semiannu

al

Interest

Period-En

d

(A)

Cash Interest

Paid

[5.5% x

$180,000]

(B)

Bond Interest

Expense

[5% x Prior

(E)]

(C)

Premium

Amortizatio

n

[(A) – (B)]

(D)

Unamortize

d

Premium

[Prior (D) –

(C)]

(E)

Carrying

Value

[$180,000 +

(D)]

1/01/2013

$4,566 $184,566

4

Part 4

2013

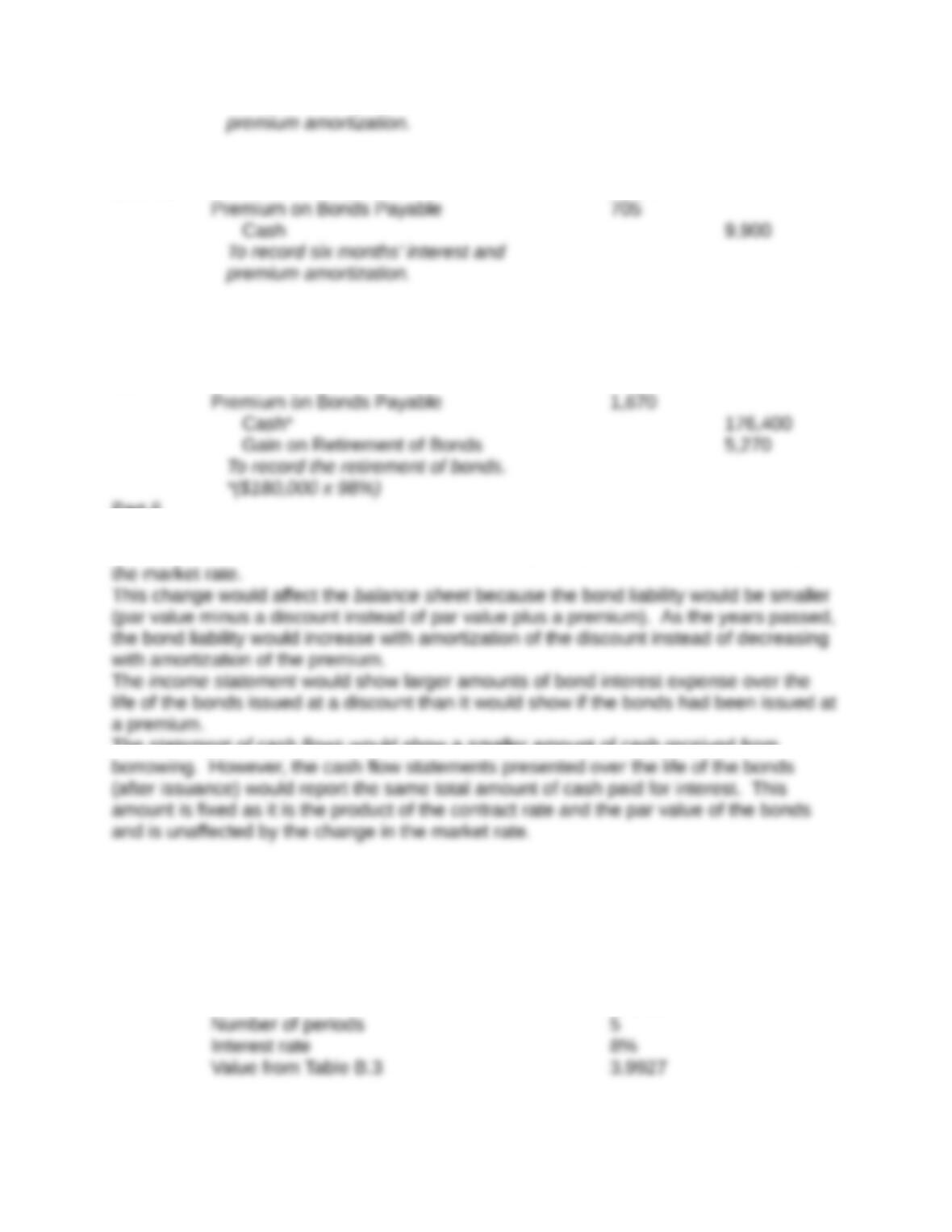

June 30 Bond Interest Expense 9,228

2013

Dec. 31 Bond Interest Expense 9,195

Part 5

2015

Jan. 1 Bonds Payable 180,000

Part 6

If the market rate on the issue date had been 12% instead of 10%, the bonds would

have sold at a discount because the contract rate of 11% would have been lower than

The statement of cash flows would show a smaller amount of cash received from

Title: Problem 14-9A

QA_Ori:

Part 1

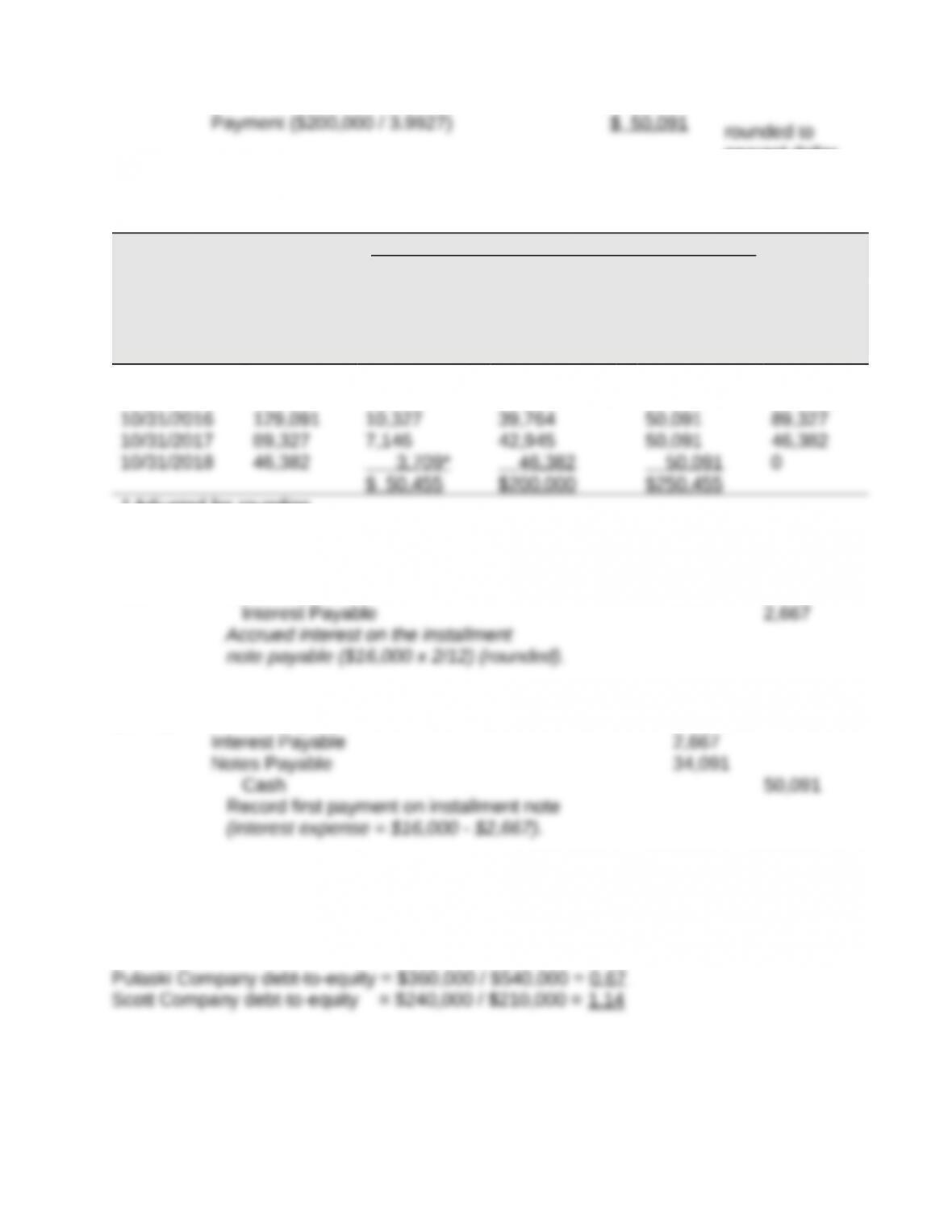

Amount of Payment

Note balance $200,000

nearest dollar

Part 2

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[8% x (A)]

+

(C)

Debit Notes

Payable [(D)

– (B)] =

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

10/31/2014 $200,000 $ 16,000 $ 34,091 $ 50,091 $165,909

10/31/2015 165,909 13,273 36,818 50,091 129,091

* Adjusted for rounding

Part 3

2013

Dec. 31 Interest Expense 2,667

2014

Oct. 31 Interest Expense 13,333

Title: Problem 14-10A

QA_Ori:

Part 1

Part 2

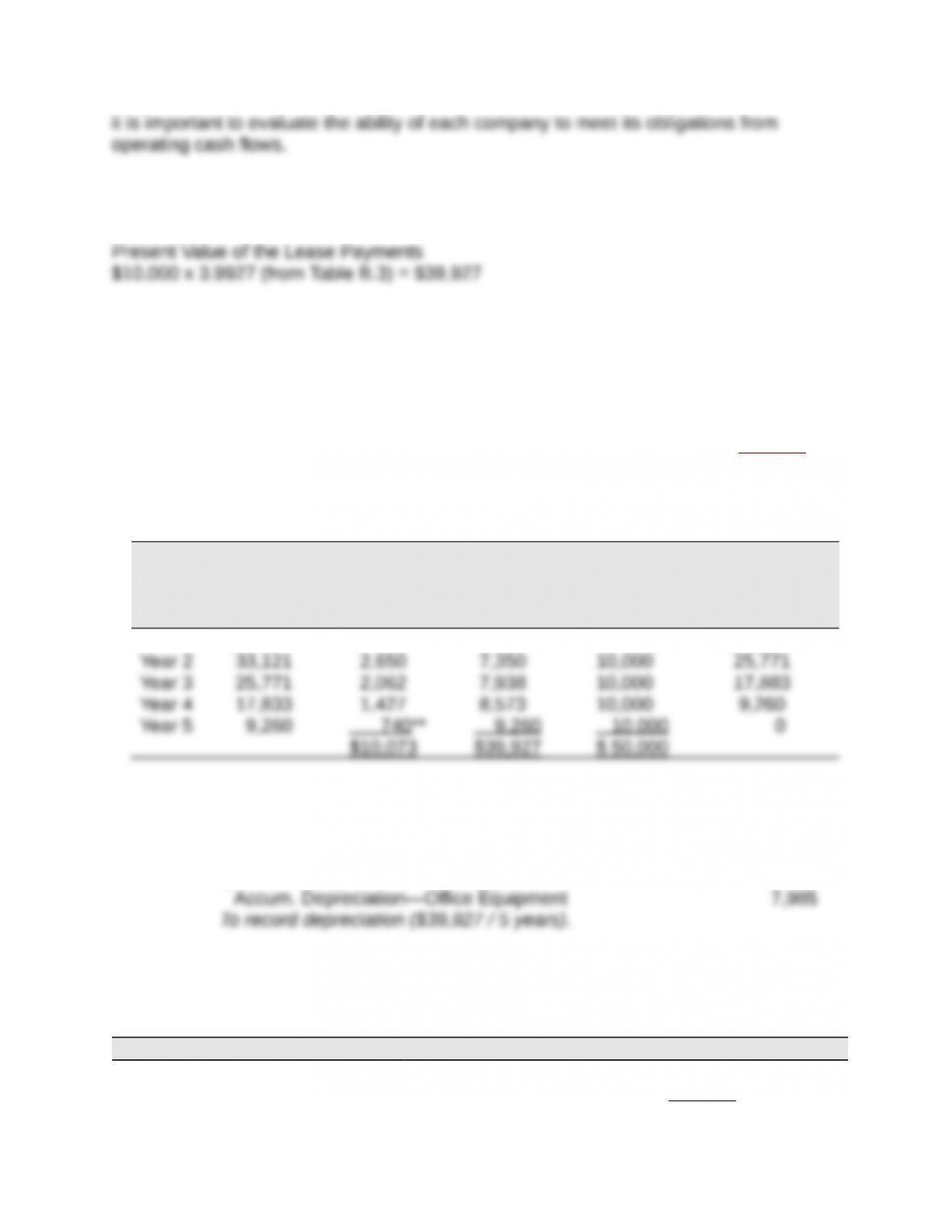

Scott’s debt-to-equity ratio is higher than Pulaski’s. This implies that Scott is more risky.

However, before deciding if either company’s debt-to-equity ratio is too high (or too low),

Title: Problem 14-11A

QA_Ori:

Part 1

Part 2

Leased Asset—Office Equipment 39,927

Lease Liability 39,927

To record capital lease of office equipment.

Part 3

Instructor note: A first printing of the textbook erroneously read that the beginning

balance of the lease liability was $79,854, which should correctly have read $39,927.

Capital Lease Liability Payment (Amortization) Schedule

Period

Ending

Date

Beginning

Balance of

Lease

Liability

Interest on

Lease

Liability (8%)

Reduction

of Lease

Liability

Cash

Lease

Payment

Ending

Balance of

Lease

Liability

Year 1 $39,927 $ 3,194* $ 6,806 $ 10,000 $33,121

* Rounded to nearest dollar.

** Difference due to rounding.

Part 4

Depreciation Expense—Office Equipment 7,985

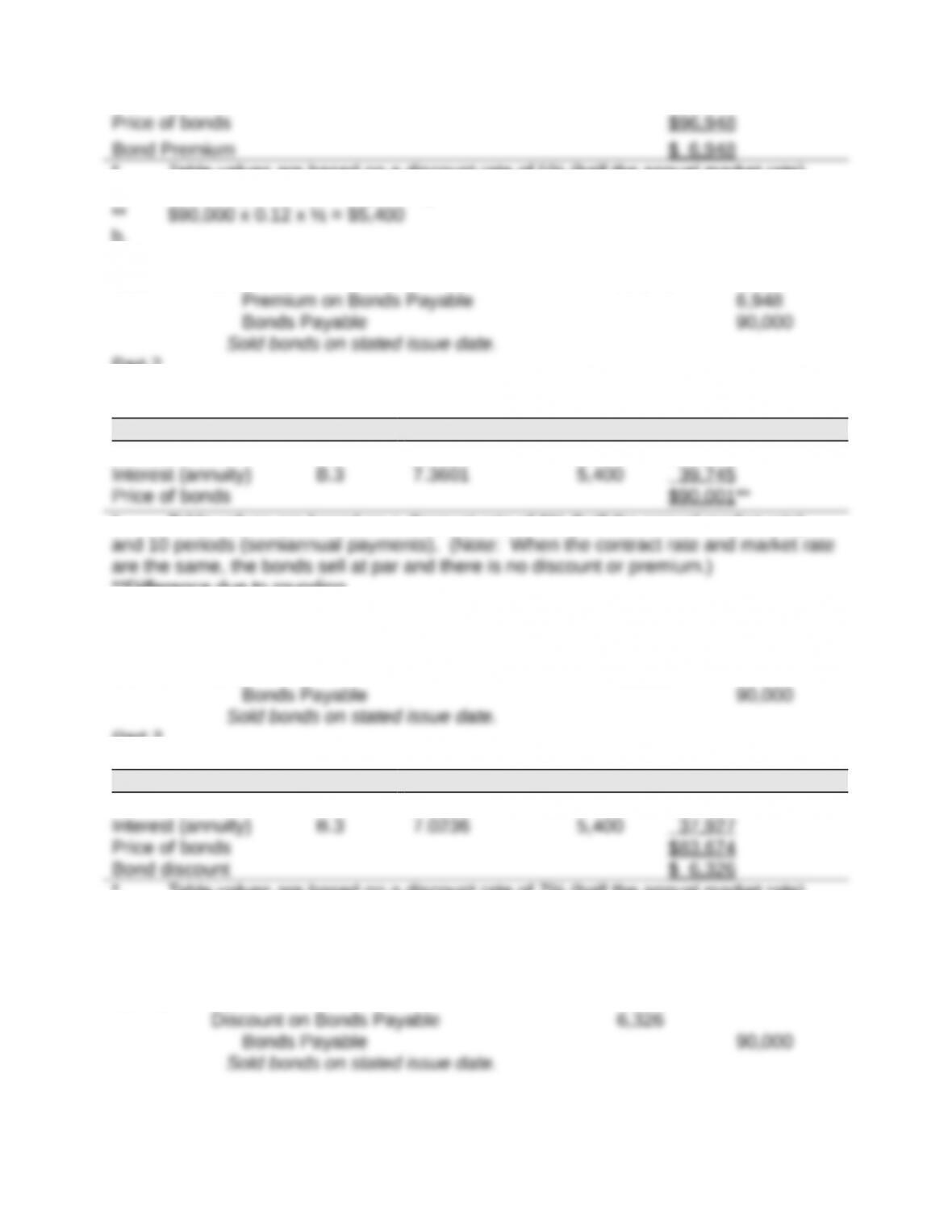

Title: Problem 14-1

QA_Ori:

Part 1

a.

Cash Flow Table Table Value* Amount Present Value

Par value B.1 0.6139 $90,000 $55,251

Interest (annuity) B.3 7.7217 5,400** 41,697

* Table values are based on a discount rate of 5% (half the annual market rate)

and 10 periods (semiannual payments).

b.

2013

Jan. 1 Cash 96,948

Part 2

a.

Cash Flow Table Table Value* Amount Present Value

Par value B.1 0.5584 $90,000 $50,256

* Table values are based on a discount rate of 6% (half the annual market rate)

**Difference due to rounding

b.

2013

Jan. 1 Cash 90,000

Part 3

a.

Cash Flow Table Table Value* Amount Present Value

Par value B.1 0.5083 $90,000 $45,747

* Table values are based on a discount rate of 7% (half the annual market rate)

and 10 periods (semiannual payments).

b.

2013

Jan. 1 Cash 83,674

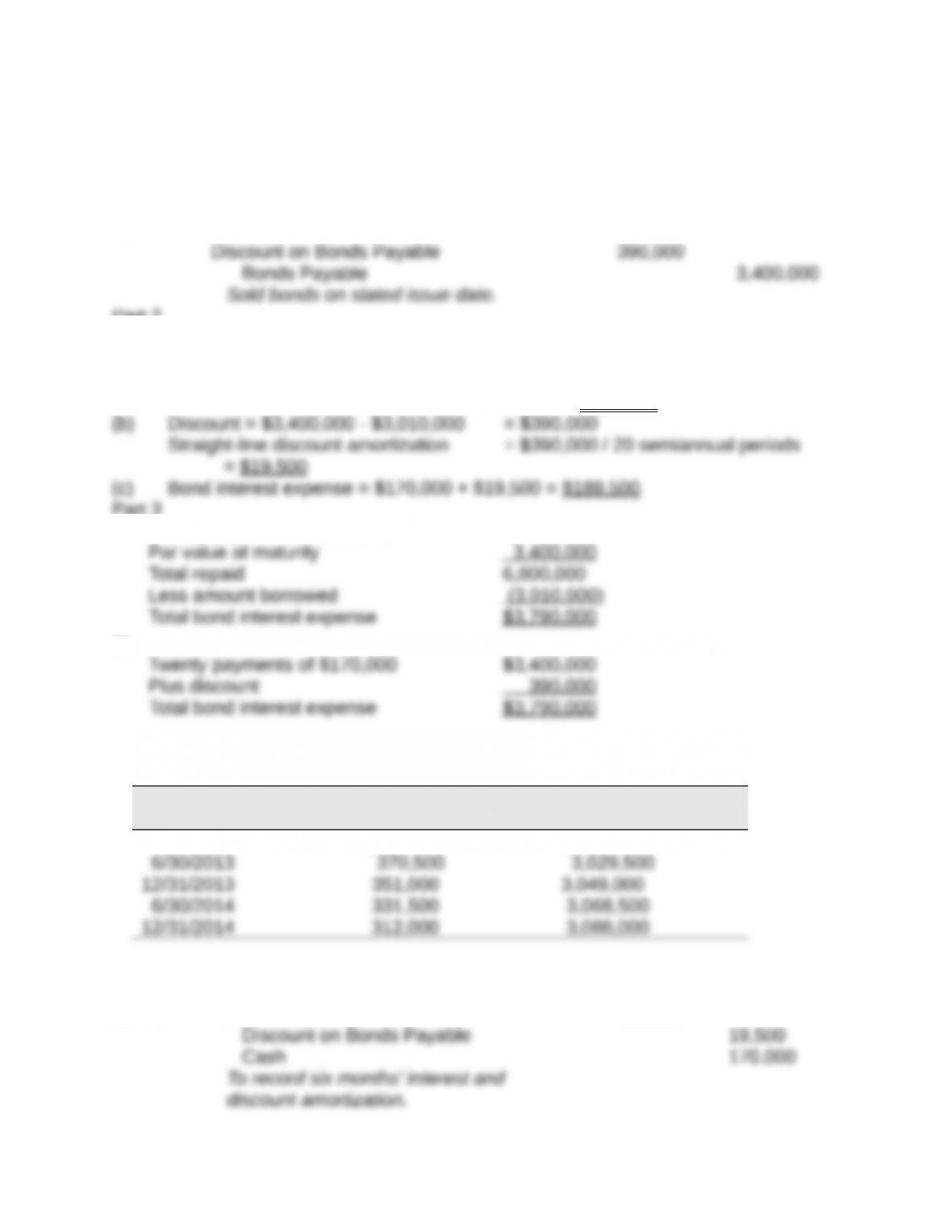

Title: Problem 14-2B

QA_Ori:

Part 1

2013

Jan. 1 Cash 3,010,000

Part 2

[Note: The semiannual amounts for (a), (b), and (c) below are the same

throughout the bonds’ life because the company uses straight-line amortization.]

(a) Cash Payment = $3,400,000 x 10% x 6/12 year = $170,000

Part 3

Twenty payments of $170,000 $3,400,000

or:

Part 4

(Semiannual amortization: $390,000/20 = $19,500)

Semiannual

Period-End

Unamortized Discount Carrying

Value

1/01/2013 $390,000 $3,010,000

Part 5

2013

June 30 Bond Interest Expense 189,500

2013

Dec. 31 Bond Interest Expense 189,500

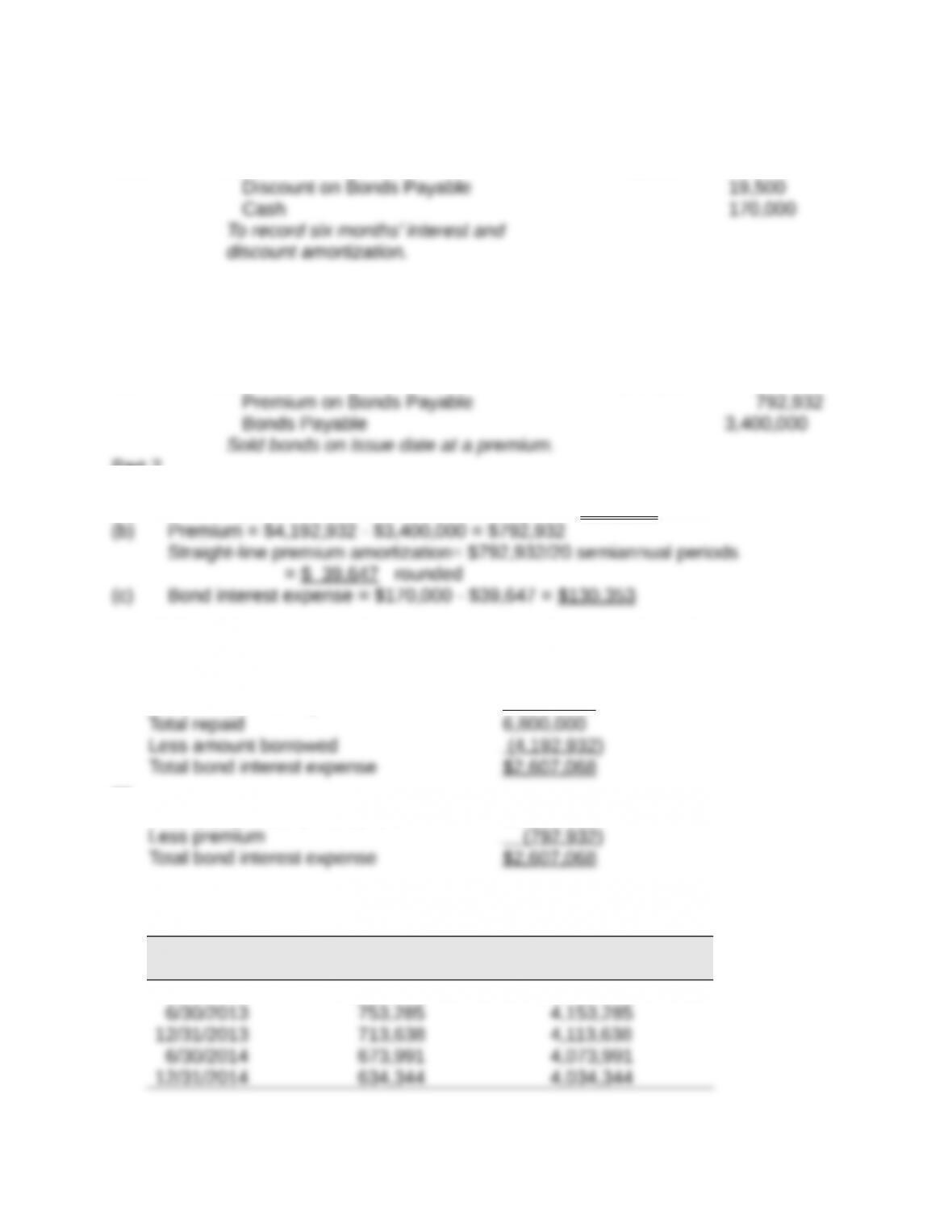

Title: Problem 14-3B

QA_Ori:

Part 1

2013

Jan. 1 Cash 4,192,932

Part 2

(a) Cash Payment = $3,400,000 x 10% x 6/12 year = $170,000

Part 3

Twenty payments of $170,000 $3,400,000

Par value at maturity 3,400,000

or:

Twenty payments of $170,000 $3,400,000

Part 4

Semiannual

Period-End

Unamortized

Premium

Carrying

Value

1/01/2013 $792,932 $4,192,932

Part 5

QA_Ori:

2013

June 30 Bond Interest Expense 130,353

2013

Dec. 31 Bond Interest Expense 130,353

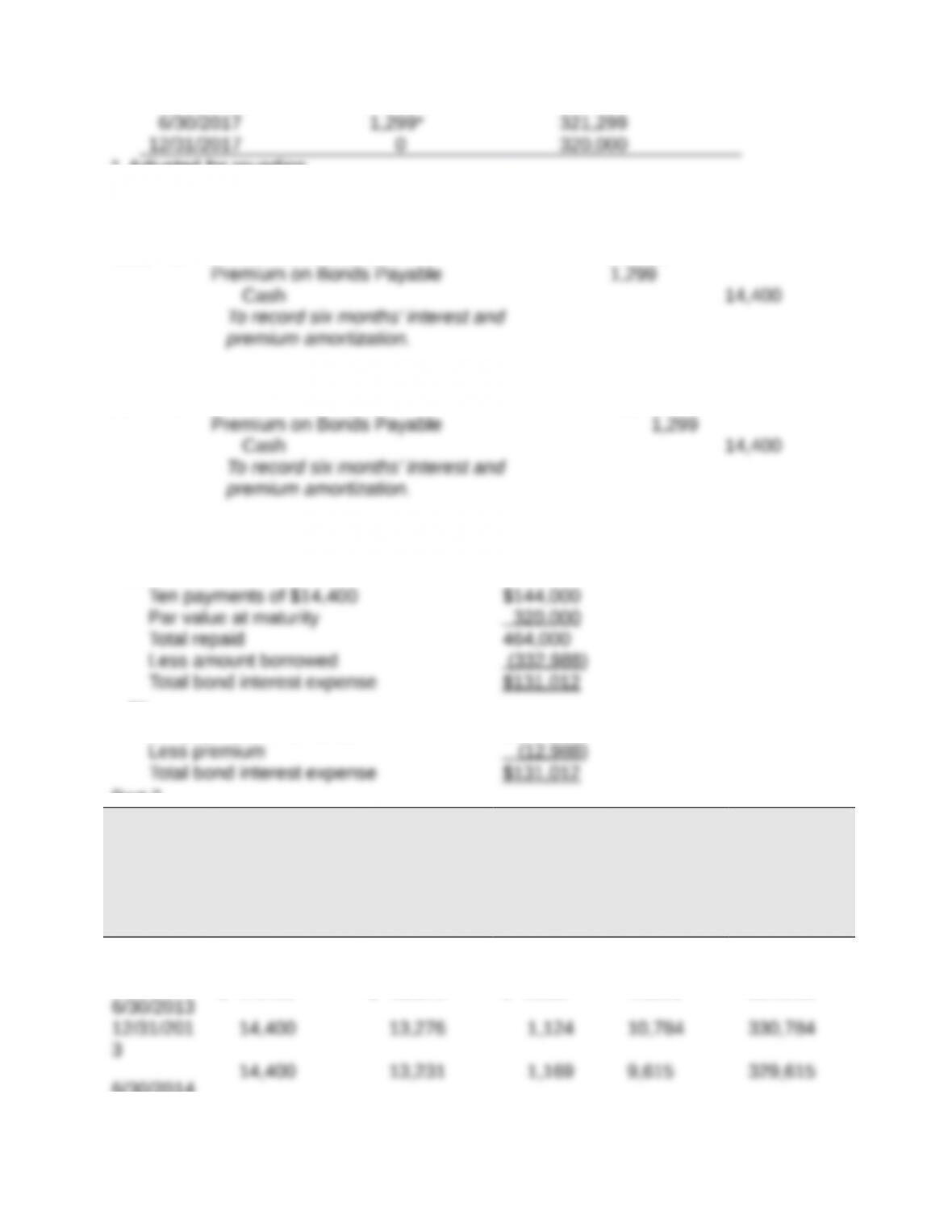

Title: Problem 14-4B

QA_Ori:

Part 1

Ten payments of $14,400* $ 144,000

or:

Ten payments of $14,400 $ 144,000

Part 2

Straight-line amortization table ($12,988/10 = $1,299**)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2013 $12,988 $332,988

6/30/2013 11,689 331,689

* Adjusted for rounding.

**Rounded to nearest dollar.

Part 3

2013

June 30 Bond Interest Expense 13,101

2013

Dec. 31 Bond Interest Expense 13,101

Title: Problem 14-5B

QA_Ori:

Part 1

or:

Ten payments of $14,400 $144,000

Part 2

Semiannu

al

Interest

Period-En

d

(A)

Cash Interest

Paid

[4.5% x

$320,000]

(B)

Bond Interest

Expense

[4% x Prior

(E)]

(C)

Premium

Amortizatio

n

[(A) – (B)]

(D)

Unamortize

d

Premium

[Prior (D) –

(C)]

(E)

Carrying

Value

[$320,000 +

(D)]

1/01/2013

$12,988 $332,988

$ 14,400 $ 13,320 $ 1,080 11,908 331,908

6/30/2014

12/31/201

4

14,400 13,185 1,215 8,400 328,400

14,400 13,136 1,264 7,136 327,136

*Adjusted for rounding.

Part 3

2013

June 30 Bond Interest Expense 13,320

2013

Dec. 31 Bond Interest Expense 13,276

Part 4

As of December 31, 2015

Cash Flow Table Table Value* Amount Present Value

Par value B.1 0.8548 $320,000 $273,536

* Table values are based on a discount rate of 4% (half the annual original market

rate) and 4 periods (semiannual payments).

Comparison to Part 2 Table

Except for a small rounding difference, this present value ($325,807) equals the carrying

Title: Problem 14-6B

QA_Ori:

Part 1

2013

Jan. 1 Cash 198,494

Part 2

Thirty payments of $7,200*$ 216,000

or:

Thirty payments of $7,200* $ 216,000

Part 3

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2013 $41,506 $ 198,494

Part 4

2013

June 30 Bond Interest Expense 8,584

2013

Dec. 31 Bond Interest Expense 8,584

Discount on Bonds Payable 1,384