Title: Teamwork in Action

QA_Ori:

Concepts and procedures to illustrate in expert presentation:

Specific Identification Expert:

(a) and (b) Concept:

Purchases are always recorded at the actual specific costs. The specific

identification cost flow assumption requires units sold be assigned their actual

cost. Total cost of goods sold is tallied based on these individual cost

assignments. The new inventory balance is perpetually determined to be the

amount after sales at actual cost is deducted.

(a) and (b) Procedures:

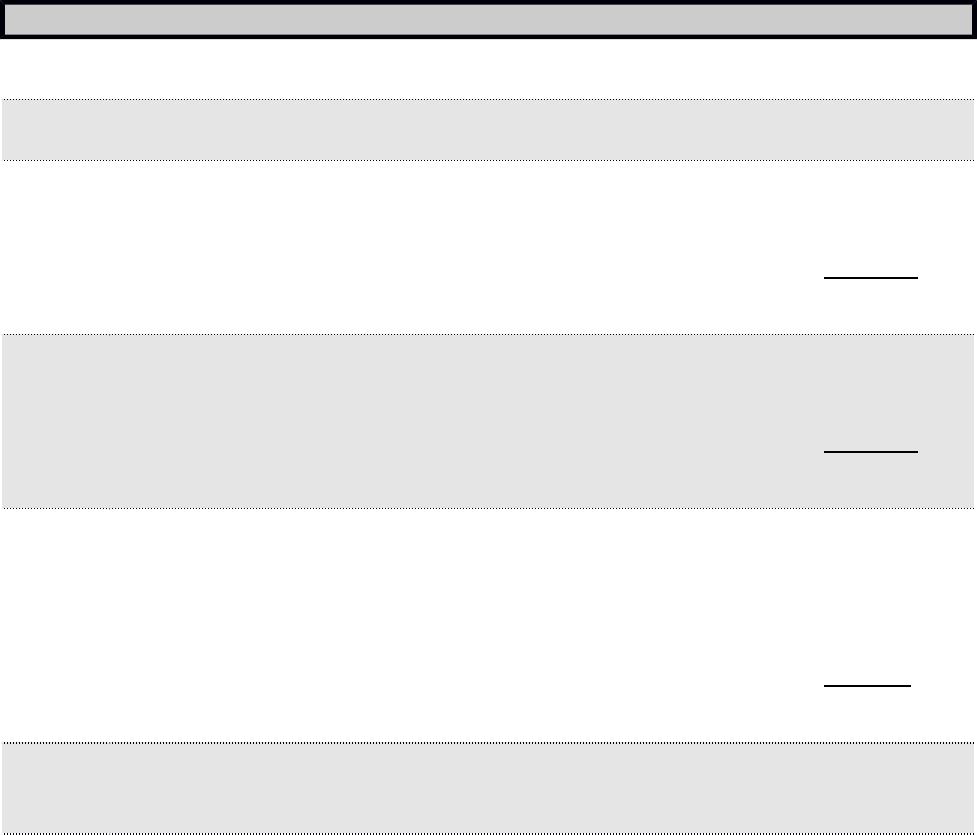

Date Goods Purchased Cost of Goods Sold Inventory Balance

Jan. 1 50 @ $100

= $ 5,000

Jan.10 30 @ $ 100 = $ 3,000 20 @ $100

= $ 2,000

LIFO Expert:

(a) and (b) Concept:

Purchases are always recorded at actual costs. The LIFO cost flow assumption

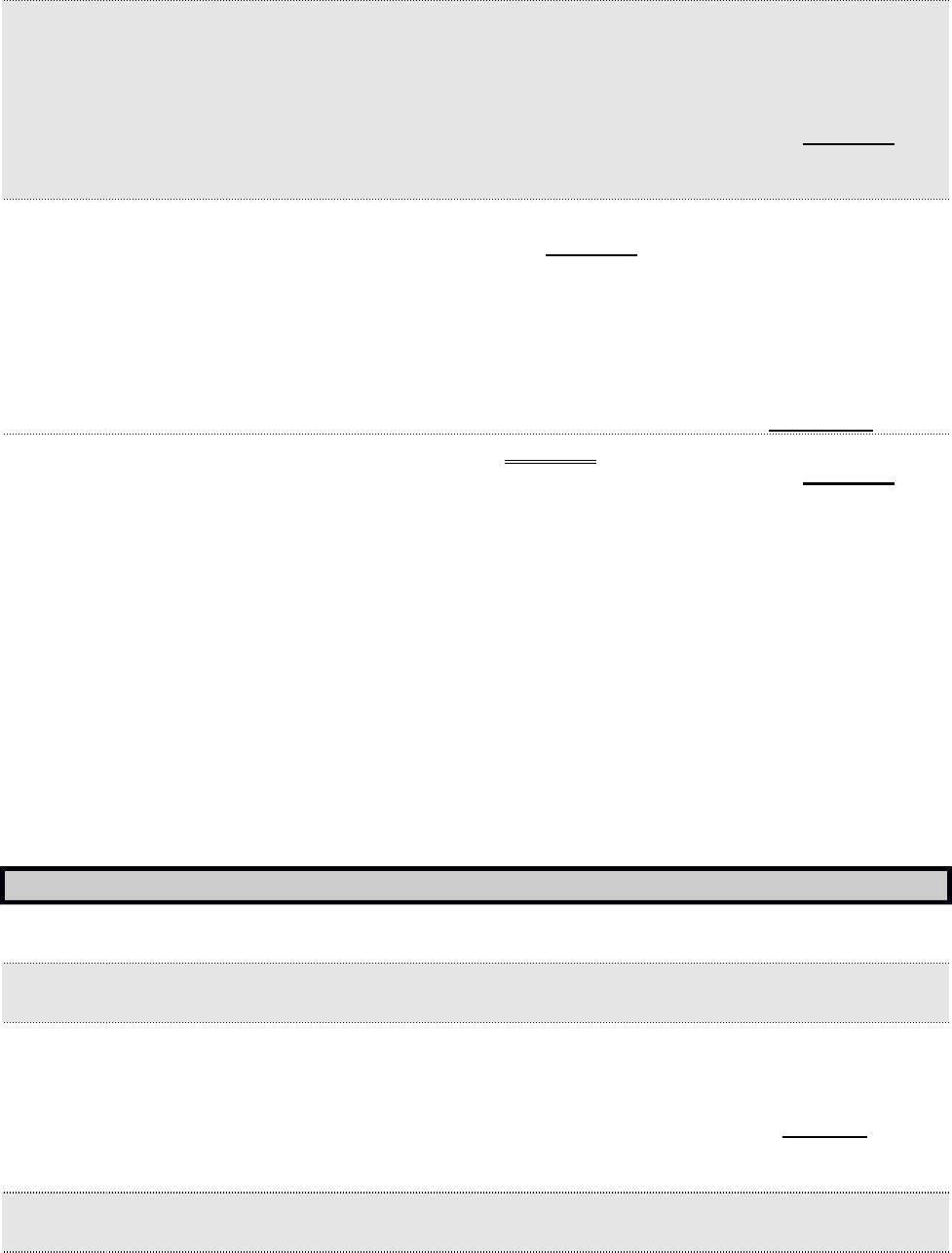

Date Goods Purchased Cost of Goods Sold Inventory Balance

Jan. 1 50 @ $100

= $ 5,000

Jan.10 30 @ $100

= $ 3,000

20 @ $100

= $ 2,000

FIFO Expert:

(a) and (b) Concept:

Purchases are always recorded at actual costs. The FIFO cost flow assumption

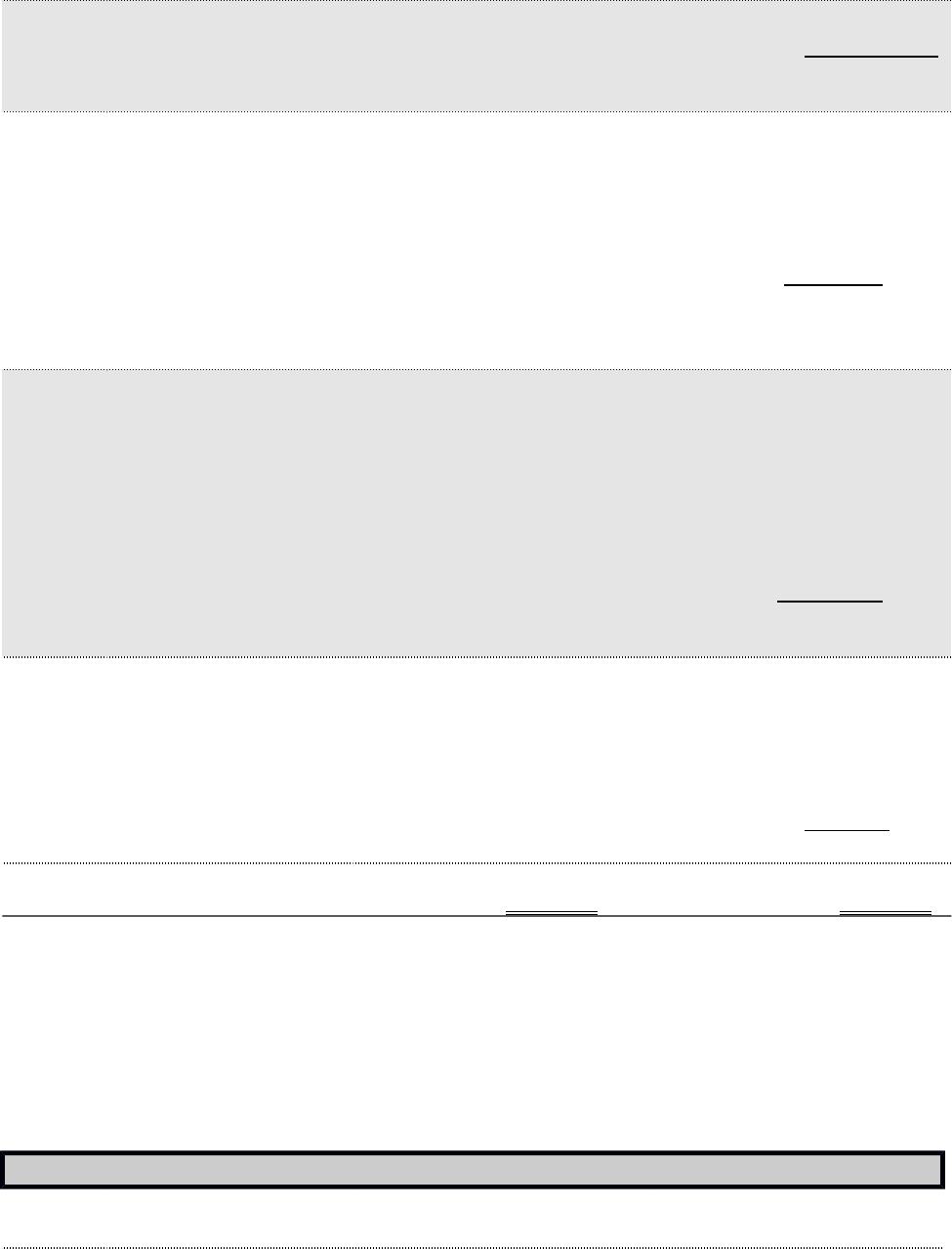

Date Goods Purchased Cost of Goods Sold Inventory Balance

Jan. 1 50 @ $100

= $ 5,000

Jan.10 30 @ $100

= $ 3,000

20 @ $100

= $ 2,000

Jan.14 150 @ $120 =

$18,000

20 @ $100

= $ 2,000

150 @ $120

= 18,000

$

20,000

Weighted Average Expert:

(a) and (b) Concept:

Purchases are always recorded at actual costs. The Weighted Average cost flow

assumption requires units sold be assigned a cost based on running weighted

and (b) Procedures:

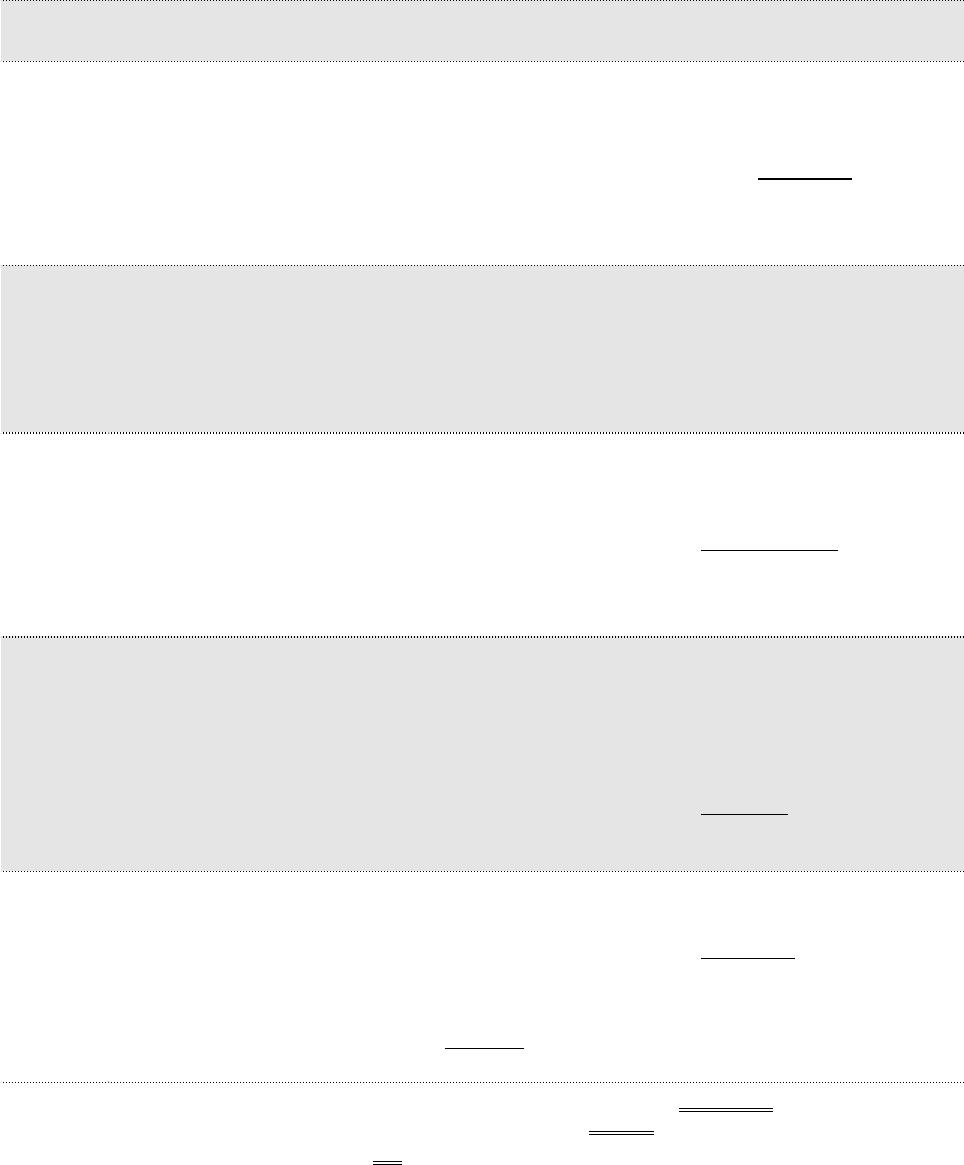

Date Goods Purchased Cost of Goods Sold Inventory Balance

Jan. 1 50 @ $100 = $

5,000

Jan.10 30 @ $100 = $

3,000

20 @ $100 = $

2,000

Jan.14 150 @ $120

= $18,000

170 @ $117.647 =

$20,000

(2,000 +18,000)/

(20+150)

* rounded ** adjusted for rounding

(c) Cost Flow versus Actual Physical Flow

Typical comments experts may express in response to (c):

Physical flow of goods can be affected by the type of products in inventory and/or

the way inventory is stored and/or displayed.

More Specific Expert Comments to (c):

Specific Identification–Always reflects the actual cost flow. Electronic scanning

FIFO–Most businesses try to move their older or earlier acquired inventory first,

LIFO–Few actually sell their most recently acquired inventory first. This could

Weighted Average–This cost is rarely the actual cost flow. This would require the

(d) Impact of Methods

Typical comments experts may express in response to (d):

In a period of rising prices LIFO will generally result in the highest cost of goods

Specific Identification will result in a cost of goods sold, net income and tax

(e) Valuation

Typical comments experts may express in response to (e):

FIFO tends to value ending inventory closest to replacement cost whereas LIFO

Title: Entrepreneur Decision 1

QA_Ori:

days

Title: Entrepreneur Decision 2

QA_Ori:

The owners’ proposal for their company would yield a much improved inventory

turnover of 8 vis-à-vis the current turnover of 4. On the downside, its days’ sales

We need to recognize that the major concern with this proposal is with the

company’s confidence in both maintaining its current sales level and with not

Title: Hitting the Road

QA_Ori:

There is no formal solution for this field activity. The required solution does allow

Title: Global Decision 1

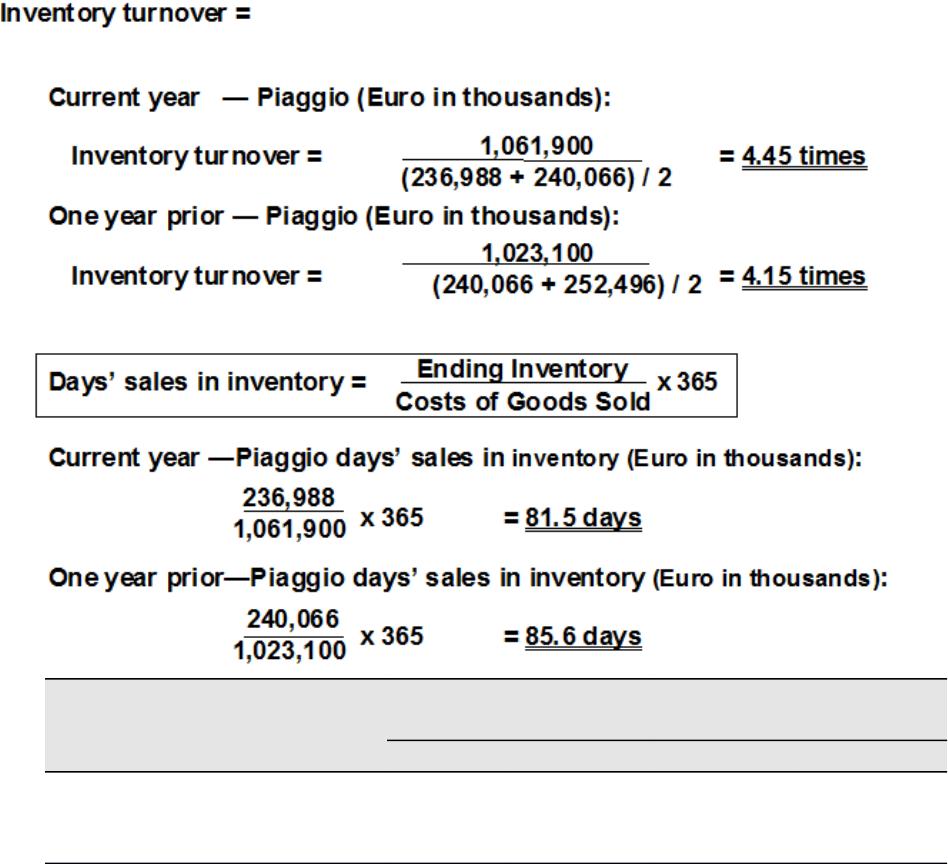

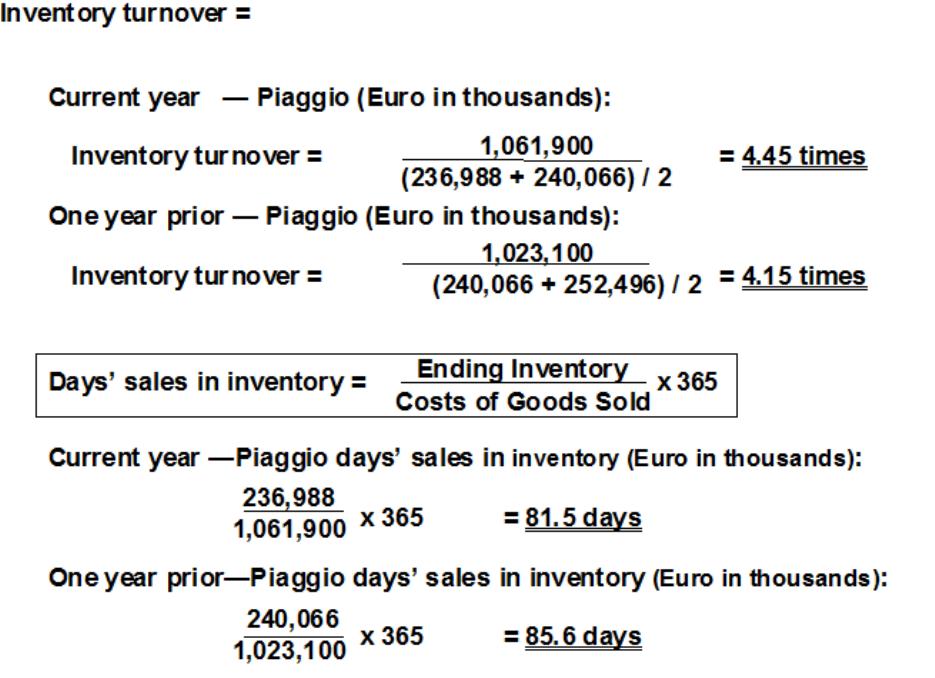

QA_Ori:

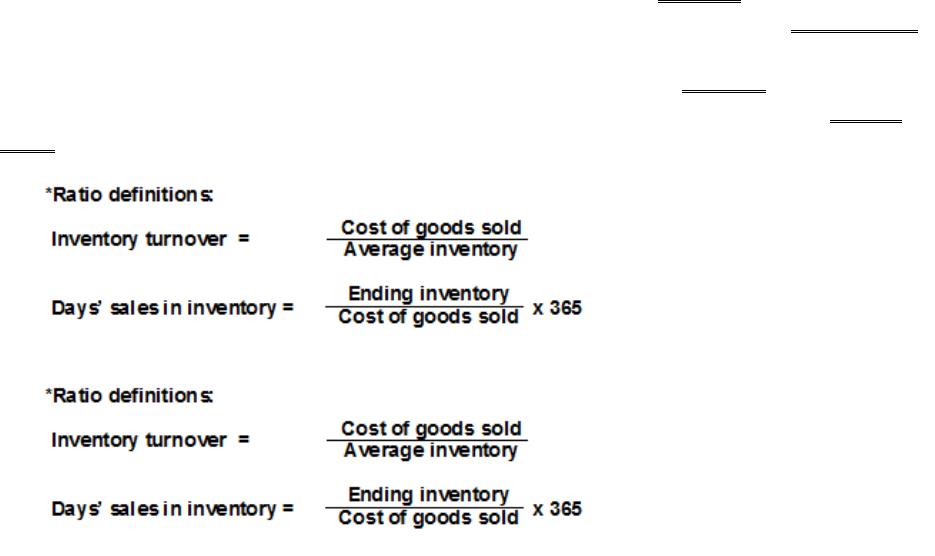

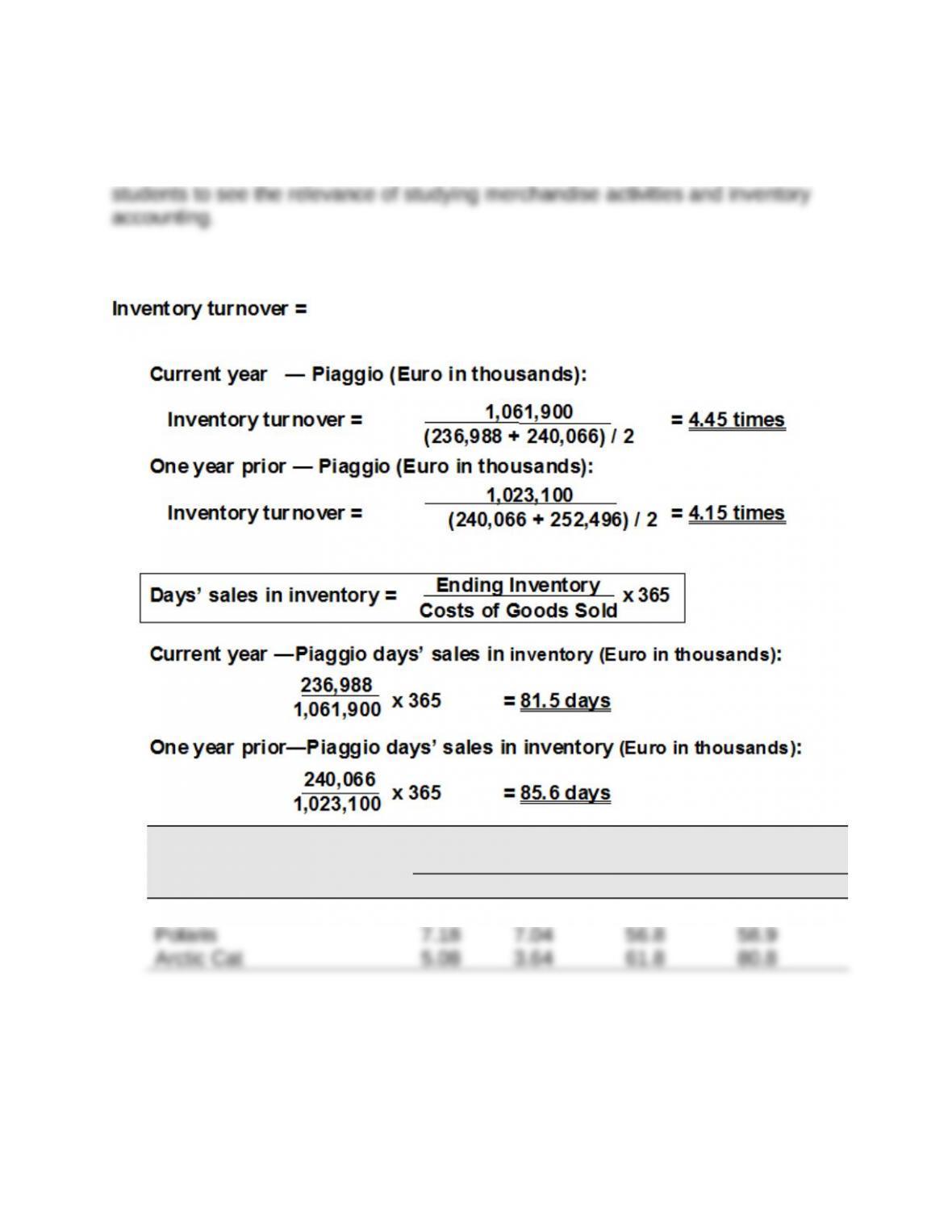

Inventory Turnover Days’ Sales in

Inventory

Company Current Prior Year Current Prior Year

Piaggio 4.45 4.15 81.5 85.6

NOTE: COMPUTATIONS FOR POLARIS AND ARCTIC CAT ARE IN BTN

6-2.

Title: Global Decision 2

QA_Ori:

For the current year and prior years, Polaris has the highest inventory

turnover and the lowest days’ sales in inventory. For the current year, Piaggio