Title: Reporting in Action 1

QA_Ori:

The revenue items from its income statement must be identified, and those

would be credited to Income Summary as step 1 in the closing entry process.

Title: Reporting in Action 2

QA_Ori:

The total expenses that would be debited to Income Summary as step 2 in the

closing entry process must be computed. Polaris’ total expenses for the year

ended December 31, 2011, are (in thousands):

Cost of sales $1,916,366

Selling and marketing 178,725

Title: Reporting in Action 3

QA_Ori:

The balance of Income Summary before it is closed as of December 31, 2011,

Title: Reporting in Action 4

QA_Ori:

From the cash flow statement, we see that Polaris paid $61,585 ($ in thousands)

in cash dividends.

Title: Reporting in Action 5

QA_Ori:

Solution depends on the financial statements accessed.

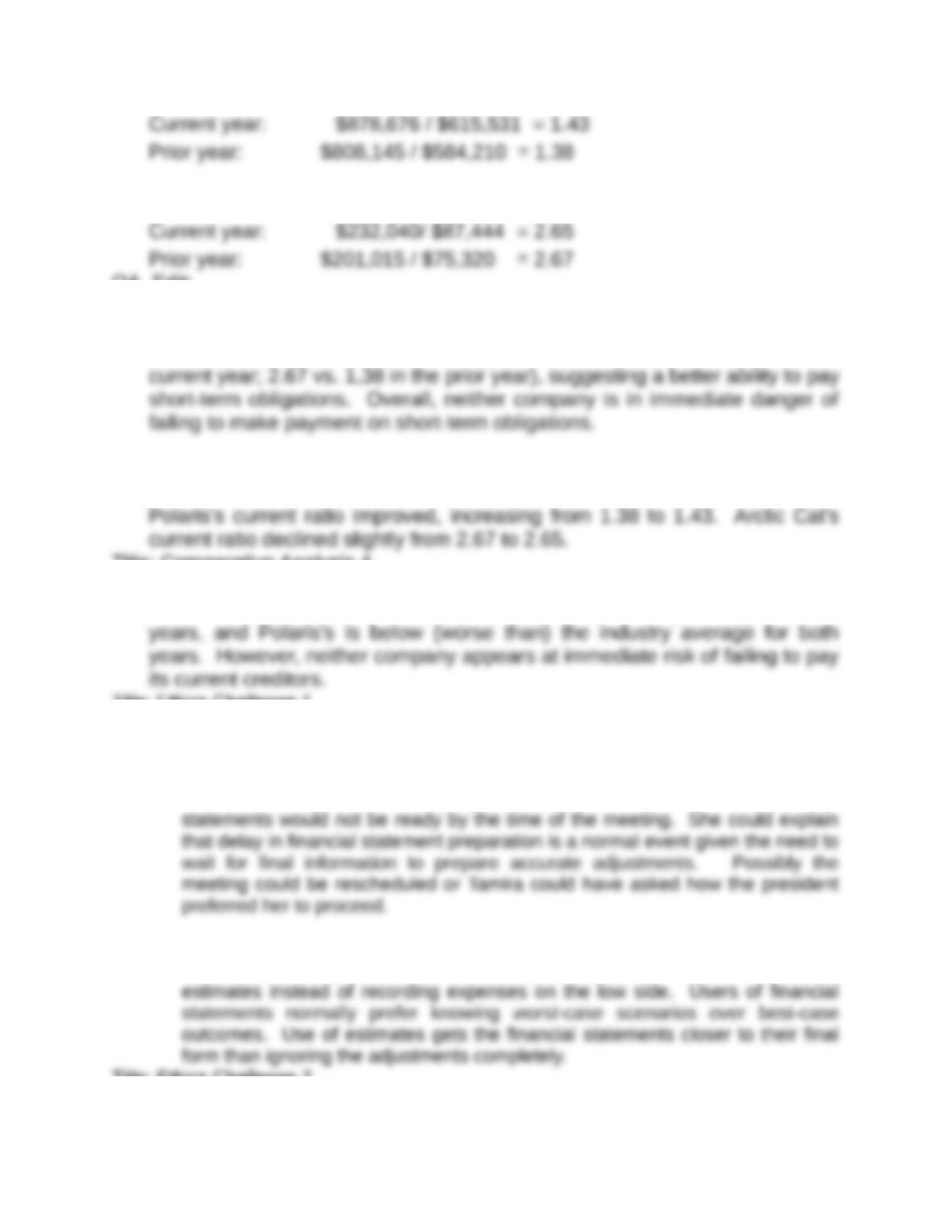

Title: Comparative Analysis 1

QA_Ori:

Polaris’s current ratios: ($ in thousands)

Arctic Cat’s current ratios: ($ in thousands)

QA_Edit:

Title: Comparative Analysis 2

QA_Ori:

In both years, Arctic Cat has the higher current ratio (2.65 vs 1.43 for the

Title: Comparative Analysis 3

QA_Ori:

Title: Comparative Analysis 4

QA_Ori:

Arctic Cat’s current ratio is above (better than) the industry average for both

Title: Ethics Challenge 1

QA_Ori:

There are several courses of action that Tamira could have taken. Two possibilities

follow:

a. She could have consulted with the president and told him that finalized financial

b. The estimation decision was not a bad choice in itself, but she should have

informed the president. Tamira probably should have used less optimistic

Title: Ethics Challenge 2

QA_Ori:

Students may offer one of the above alternatives or another response they may

TO: _____________________

FROM: _____________________

DATE: ______________________

SUBJECT: CLARIFICATIONS—OBJECTIVE OF THE CLOSING PROCESS

[Following is a sample of what the memorandum’s contents might include.]

When we speak of “closing the books” or the closing process we are not talking

Scoreboards are used to temporarily hold information that will allow us to determine

who won or lost in an athletic game or event. When the athletic event is over, the

result of the game is permanently recorded elsewhere–probably in the team’s record

The revenue and expense accounts temporarily hold the information to determine if

the owner(s) won or lost in the game of business. Each fiscal period should be

I hope this memo clarifies the objective of the closing process.

[Note: The memorandum need not discuss the income summary account since the assignment requires

explaining the concept, not the procedure.]

Title: Taking It to the Net 1

QA_Ori:

The Motley Fool states that a benchmark of 1.5 is generally regarded as

sufficient to meet near-term operating needs.

Title: Taking It to the Net 2

QA_Ori:

One should always check a company’s current ratio (as well as any other ratio)

against its main competitors in a given industry. Industries have their own norms

as far as what values of current ratios make sense and which do not.

Title: Taking It to the Net 3

QA_Ori:

A current ratio that is too high can suggest that a company is hoarding assets

instead of using them to effectively grow the business—this is an inefficient use

of resources that can potentially impair long-term returns.

Title: Teamwork in Action 1

QA_Ori:

1. Accounts and adjusted balances to be extended to Balance Sheet columns

Trial Balance Adjustments Balance Sheet

Account Title Debit Credit Debit Credit Debit Credit

Cash……………………………..$16,000 $16,000

Accounts receivable………… (d) 800 800

Supplies…….………………….. 12,000 (c) 7,000 5,000

(Cash + AR + Supplies + Prepaid Ins. + Equipment – Accum. Depreciation)

Adjusted revenue account balance

Trial Balance Adjustments

Income

Statement

Title Debit Credit Debit Credit Debit Credit

Investigation Fees

Closing entry

Account Titles and Explanation Debit Credit

Investigation Fees Earned……….………..……………………………. 33,800

2. Adjusted balances of expense accounts

Title Trial Balance Adjustments

Income

Statement

Debit Credit Debit Credit Debit Credit

Rent Expense……….………….15,000 15,000

Closing entry

Account Titles and Explanation Debit Credit

Income Summary…………………..………..…………………………….. 28,200

Rent Expense…………..…………………..………..……….. 15,000

4.

D. Noseworthy, Capital Income Summary

Third and Fourth closing entries

Account Titles and Explanation Debit Credit

To close Income Summary to Capital.

5. Proving the Accounting Equation

ASSETS = LIABILITIES + OWNER’S EQUITY

Title: Entrepreneurial Decision 1

QA_Ori:

A classified balance sheet classifies liabilities into current and non-current.

The current liabilities are those that are due in the short-term, and must be

Title: Entrepreneurial Decision 2

QA_Ori:

To better understand the company’s operations, she must make sure that all

revenues earned in a particular accounting period are included in that

period’s income statement. In addition, she must match expenses to

revenues. Without closing entries, revenues and expenses would continue to

Title: Entrepreneurial Decision 3

QA_Ori:

Closing procedures will accomplish two objectives for Arynetta. First, the

Title: Hitting the road

QA_Ori:

There is no formal solution to this field activity. The instructor may wish to tally

students’ findings to show results across companies as to use of work sheets,

software preferences, and time it takes to prepare finalized annual financial

statements.

Title: Global Decision 1

QA_Ori:

Current ratio (in thousands Euro)

Title: Global Decision 2

QA_Ori:

Analysis: Piaggio’s current ratio declined (is worse) for the current year. This puts