Fundamental Accounting Principles, 21st Edition

964

Problem 16-7B (35 minutes)

SALT LAKE COMPANY

Cash Flows from Operating Activities—Indirect Method

For Year Ended December 31, 2013

Cash flows from operating activities

Net income ………………………………………………………………….…

$ 20,000

Adjustments to reconcile net income to net cash

provided by operating activities

Depreciation expense ……………………………………………….…

$32,000

Increase in accounts receivable ………………………………..…

(600

)

Decrease in merchandise inventory …………………………..

120

Decrease in accounts payable ………………………………….…

(200

)

Increase in salaries payable ……………………………………..…

300

Increase in utilities payable …………………………………………

200

Decrease in prepaid insurance ………………………………….…

40

Decrease in prepaid rent …………………………………………..…

100

31,960

Net cash provided by operating activities …………………….…

$ 51,960

Problem 16-8BB (35 minutes)

SALT LAKE COMPANY

Cash Flows from Operating Activities—Direct Method

For Year Ended December 31, 2013

Cash flows from operating activities

Cash receipts from customers (1) ………………………………………….…….

$ 155,400

Cash payments to suppliers (2) ……………………………………………..…….

(72,080

)

Cash payments for salaries (3) …………………………………………………….

(19,700

)

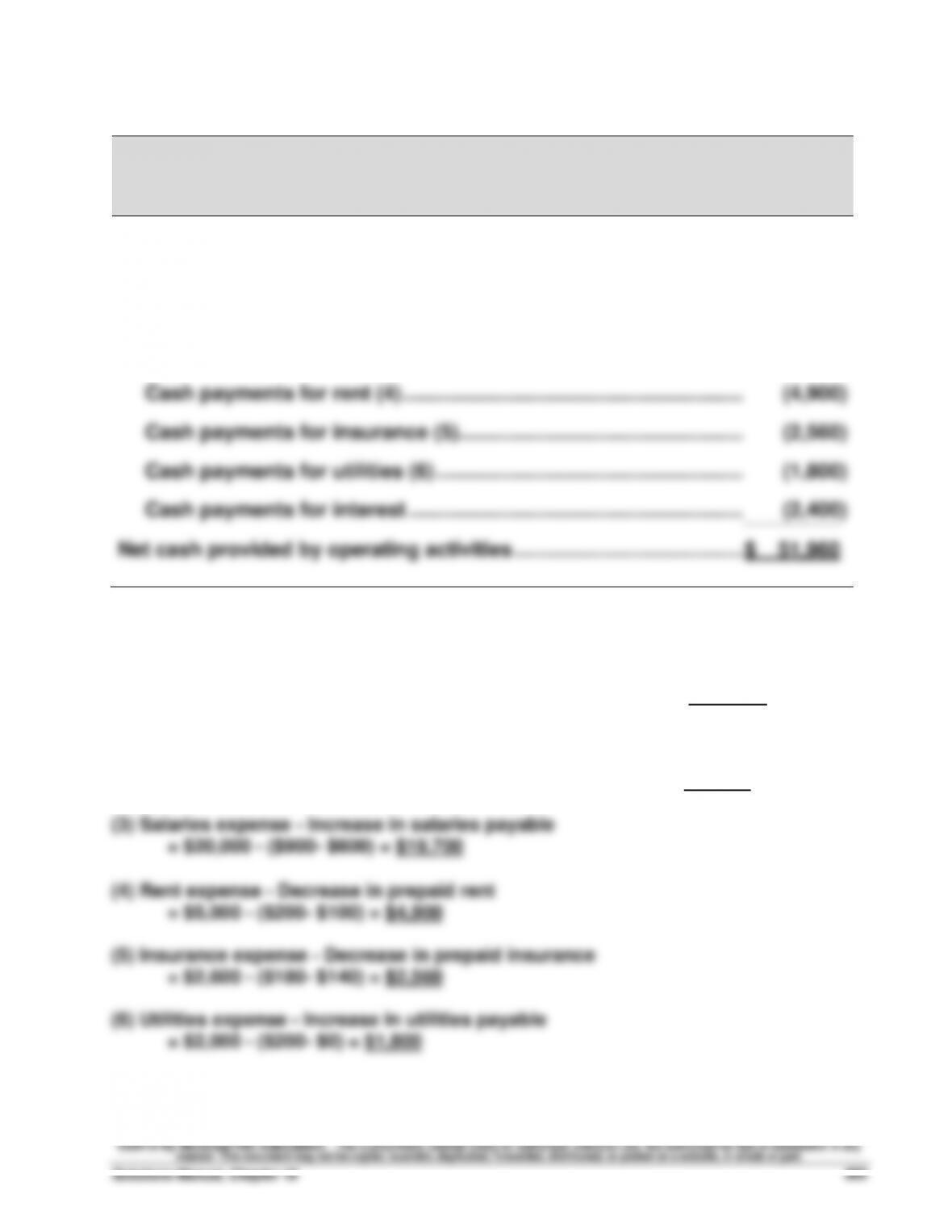

Cash payments for rent (4) …………………………………………………….…

(4,900

)

Cash payments for insurance (5) ………………………………………………….

(2,560

)

Cash payments for utilities (6) ……………………………………………….…….

(1,800

)

Cash payments for interest ……………………………………………………….

(2,400

)

Net cash provided by operating activities …………………………………..…….

$ 51,960

Supporting calculations

(1) Sales – Increase in receivables = $156,000 – ($3,600 – $3,000) = $155,400

(2) Cost of Decrease in Decrease in

goods sold inventory accounts payable =

$72,000 – ($980 – $860) + ($2,600 – $2,400) = $72,080

–

+

Fundamental Accounting Principles, 21st Edition

966

SERIAL PROBLEM — SP 16

Serial Problem — SP 16, Success Systems (45 minutes)

SUCCESS SYSTEMS

Statement of Cash Flows (Indirect)

For Quarter Ended March 31, 2014

Cash flows from operating activities

Net income ………………………………………………………………………………

$ 18,686

Adjustments to reconcile net income to net

cash provided by operating activities

Increase in accounts receivable ($22,720 – $5,668) ………….……

(17,052)

Increase in inventory ($704 – $0) ……………………………………..……

(704)

Increase in computer supplies ($2,005 – $580) ………………..……

(1,425)

Decrease in prepaid insurance ($1,665 – $1,110) ……………..……

555

Decrease in accounts payable ($1,100 – $0) …………………….……

(1,100)

Increase in wages payable ($875 – $500) ………………………..…

375

Decrease in unearned computer service revenue ………………

(1,500)

Depreciation expense–Office Equipment …………………………..

400

Depreciation expense–Computer Equipment ……………….……

1,250

Net cash used by operating activities ……………………………….……

$ (515)

Cash flows from investing activities

Net cash used in investing activities ………………………………………

0

Cash flows from financing activities

Cash received from stock issuance ………………………………….……

25,000

Cash paid for dividends …………………………………………………….…

(4,800)

Net cash provided by financing activities …………………………..

20,200

Net increase in cash ……………………………………………………………..……

$ 19,685

Cash balance at December 31, 2013 …………………………………….……

58,160

Cash balance at March 31, 2014 …………………………………………..……

$ 77,845

Reporting in Action — BTN 16-1

1. Polaris uses the indirect method of reporting operating cash flows. We

2. In all three years, Polaris’s cash flows from operating activities markedly

exceed the cash dividends paid, as can be seen from the table below:

($ thousands)

2011

2010

2009

Cash provided by operating activities ..….

$302,530

$297,619

$193,201

Cash dividends paid …………………………..

(61,585)

(53,043)

(50,177)

3. In 2011, the largest item in reconciling the difference between net income

and cash flow from operations was the change (increase) in accrued

expenses of $80,668 thousand.

4. In 2011, the largest cash inflow from investing activities was $11,950

In 2011, the largest cash inflow from financing activities was $100,000

thousand from borrowings under credit agreement/senior notes. The

In 2010, the largest cash inflow from financing activities was $68,105

5. Answer depends on the financial statement information obtained.

Fundamental Accounting Principles, 21st Edition

968

Comparative Analysis — BTN 16-2

1. Polaris’s cash flow on total assets ratio ($ thousands)

Current Year = Operating cash flows/Average total assets

= $302,530 / [($1,228,024 + $1,061,647)/2]

= $302,530 / $1,144,836 = 26.4%

Arctic Cat’s cash flow on total assets ratio ($ thousands)

2. The cash flow on total assets ratio reflects the return on average assets by

using actual operating cash flows instead of net income. This return

3. For both years, Polaris has a higher cash flow on total assets ratio than

Arctic Cat.

4. Many business decision makers (such as analysts) feel that the cash flow

Ethics Challenge — BTN 16-3

1. The business actions available include

a. Encourage early collection of receivables to reduce the accounts

receivable balance.

2. As a business owner, Katie Murphy certainly can exercise discretion over

business actions. However, the underlying economic realities should

Fundamental Accounting Principles, 21st Edition

970

Communicating in Practice — BTN 16-4

Here is a sample of what the body of the memorandum might include:

TO: Diana Wood

FROM: (Your Name)

SUBJECT: Statement of Cash Flows

DATE: _________________

I am pleased to hear your business is more profitable this year than last.

However, I have been thinking about what you said regarding the statement of

cash flows and have some thoughts as to why you found it confusing.

The statement of cash flows (operating section) can be prepared using either

of two methods—the direct or the indirect method. From what you describe,

your statement is probably prepared using the indirect method. This method

shows a determination of net cash flows in the operating (first) section by

listing the net income number and applying a series of accounting

adjustments. These adjustments often do not make sense to those that do

not have an accounting or finance background.

I recommend that you request your accountant to provide you with a

statement of cash flows that is prepared using the direct method. This will

identify exactly how much cash came in from operating activities like sales. It

will also identify exactly how much cash went out for operating expenses like

merchandise, wages, interest, and taxes. It will determine your net operating

cash flow by directly subtracting the total of these operating outflows from the

inflows. You should find this format more understandable.

Note that good cash management is essential to business success and

growth. The statement of cash flows will provide you with a lot more

information regarding your cash than a balance sheet can offer. It will allow

you to see exactly where your cash came from, where it went, and how much

it changed. It organizes these amounts into categories of operating,

financing, and investing. This organization of cash information will allow you

to better project and plan for the future.

Please reconsider the value of the statement of cash flows for your business

decisions. If you wish to discuss this further, please call me.

Taking It to the Net — BTN 16-5

1. Mendocino Brewing Company uses the indirect method to construct the

consolidated statement of cash flows.

3. The following table shows the net income (or net loss) and the cash flows

from operations for Mendocino Brewing for 2010 and 2011. Over this two–

2010

2011

Net income (loss) …………………..………

$ 49,400

$(1,078,500)

Cash flows from operations …………….

1,412,600

1,011,700

4. For the recent period, the largest cash outflow for investing was $1,025,900

for purchases of property, equipment and leasehold improvements.

5. In the recent period, for supplementary cash flow information, the company

reports cash flows related to: Interest paid, and Income taxes paid.

Fundamental Accounting Principles, 21st Edition

972

Teamwork in Action — BTN 16-6

Part 1

a. The reporting objective of the statement of cash flows is to provide

information about important cash inflows and outflows for business

decision makers. It answers specific questions such as:

b. The statement can be prepared using the direct method or the indirect

method for reporting cash flows from operating activities.

Similarities

• Both methods report the same net cash flow from operating activities.

Differences

• Cash flow from operating activities is determined differently. The direct

method determines all operating cash inflows and outflows, and then

Teamwork in Action (Continued)

c. Steps to prepare the statement of cash flows:

(i) Compute the net increase or decrease in cash using comparative

balance sheet data. This is the target number or the number the

statement will explain and prove.

d. Common analyses made from information in the statement of cash flows

include assessing a company’s:

• Ability to generate future cash flows.

• Ability to pay dividends.

Part 2

Adjusting Net Income to Cash Flow from Operating Activities

Items to Add

Items to Subtract

a.

Noncash expenses

Noncash revenues

b.

Losses

Gains

c.

Decreases in current assets

Increases in current assets

d.

Increases in current liabilities

Decreases in current liabilities

Fundamental Accounting Principles, 21st Edition

974

Teamwork in Action (Concluded)

Part 3

a. Cash receipts from customers = Sales – Increase in Accounts Receivable,

or, + Decrease in Accounts Receivable.

Explanation: Sales reflects what is earned during the period. If Accounts

Receivable increases, that increase represents earnings not yet collected,

so we subtract it. If Accounts Receivable decreases, the entity collected

that much more than the period’s sales, so we add it.

the entity paid for less than the period’s purchases, so we subtract it.

c. Cash paid for wages and operating expenses = Wages and other operating

expenses [+ Increase in prepaid expenses, or, – Decrease in prepaid

expenses] and [+ Decrease in accrued liabilities, or, – Increase in accrued

liabilities].

d. Cash paid for interest and taxes = Interest and tax expense + Decrease in

related payable, or, – Increase in related payable.

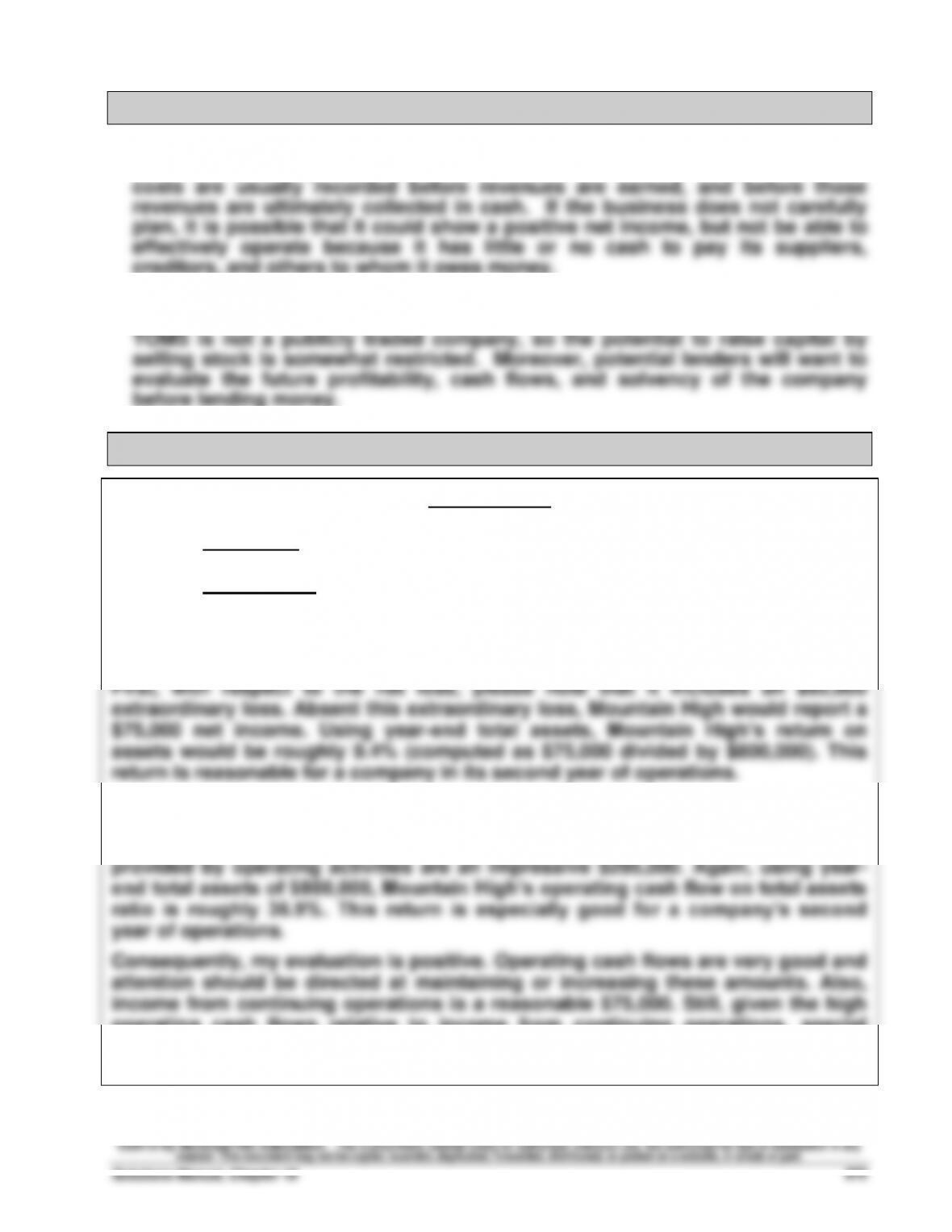

Entrepreneurial Decision — BTN 16-7

1. It is common that small businesses must pay cash in advance for items such

as rent, advertising, supplies, and facilities expansion. Consequently, those

creditors, and others to whom it owes money.

2. As a privately held corporation, TOMS can potentially raise cash financing for

expansion by selling shares in the company or by borrowing the monies.

Entrepreneurial Decision — BTN 16-8

Memorandum

To: Jenna and Matt Wilder

From: Your name

Subject: Performance evaluation of Mountain High

Date: Current Date

I have completed my evaluation of your company, Mountain High. My conclusion

is that Mountain High is performing well. This is in spite of its reported net loss

and its negative net cash flow, which I explain in this memorandum.

Second, with respect to its net cash outflow of $(5,000), please note that this is

mainly due to Mountain High’s renovation and expansion activities. This is

reflected in its summarized statement of cash flows. Specifically, its cash flows

operating cash flows relative to income from continuing operations, special

scrutiny should be directed at identifying and assessing differences between

cash flow and accrual amounts for important individual operating activities.

Fundamental Accounting Principles, 21st Edition

976

Hitting the Road — BTN 16-9

1. The Motley Fool’s Website defines cash flow as earnings before interest,

taxes, depreciation, and amortization (EBITDA). The school’s justification

for this definition includes: “Interest income and expense, as well as taxes, are

all tossed aside because cash flow is designed to focus on the operating business

2. Some analysts tend to focus on this particular earnings definition

(earnings before interest and taxes or EBIT) as it purportedly allows a

3. Answer depends on the links visited and chosen for the report.

Global Decision — BTN 16-10

1. Piaggio’s cash flow on total assets ratio follows (in Euro thousands):

Current Year = Operating cash flows / Average total assets

= €155,624 / [(€1,520,184 + €1,545,722)/2]

= €155,624 / €1,532,593 = 10.2%

2. For the current year, Piaggio’s ratio (10.2%) is lower than Polaris’s (26.4%)