16-1

CHAPTER 16

REPORTING THE STATEMENT OF CASH FLOWS

Related Assignment Materials

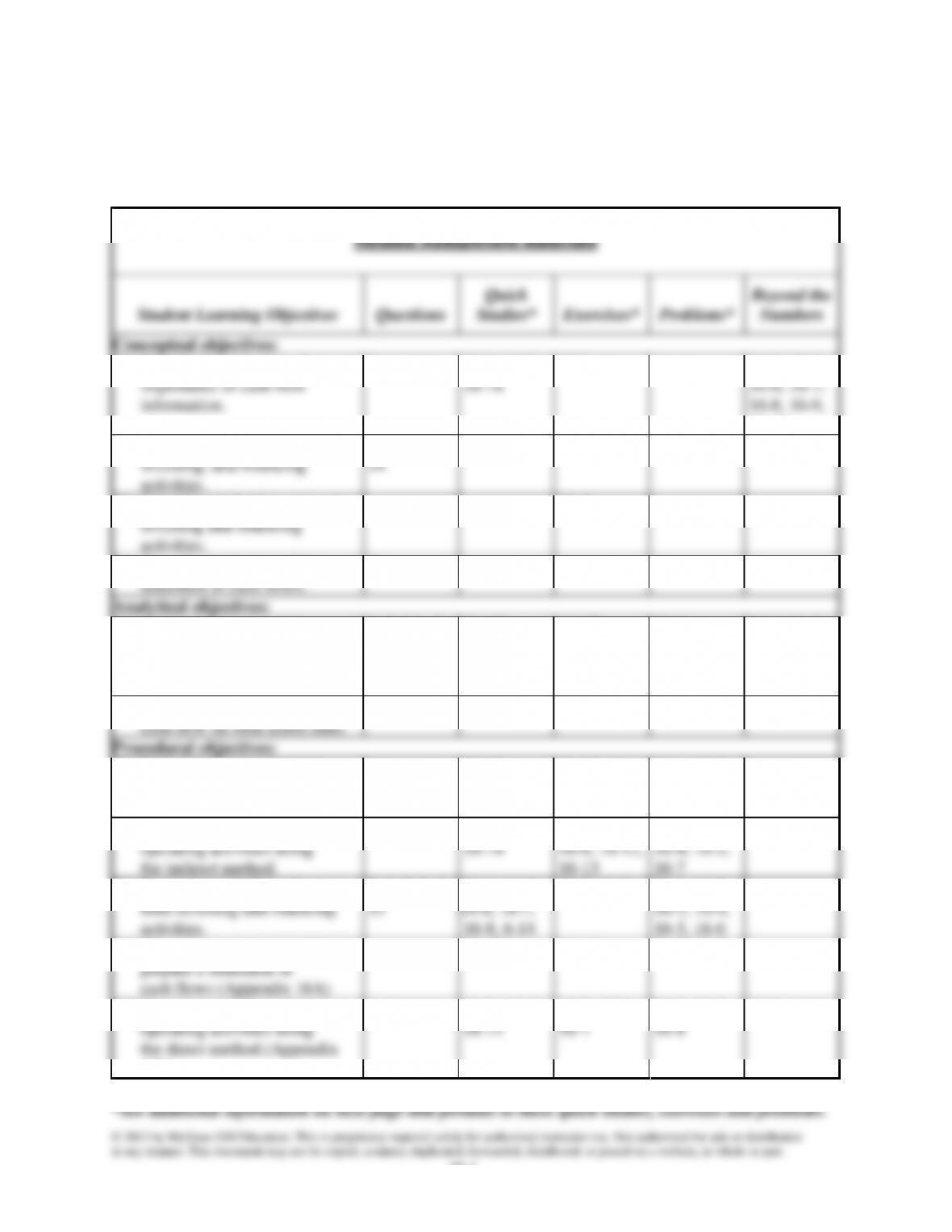

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Explain the purpose and

importance of cash flow

information.

1

16-1, 16-2,

16-18

16-1

16-3, 16-4,

16-6, 16-7,

16-8, 16-9,

16-10

C2. Distinguish between operating,

investing, and financing

activities.

2,3, 7, 8, 9,

14

C3. Identify and disclose noncash

investing and financing

activities.

16-2

C4. Describe the format of the

statement of cash flows.

5

Analytical objectives:

A1. Analyze the statement

of cash flows.

1, 9, 12, 13

16-12

16-17

16-1

16-1, 16-2,

16-3, 16-5,

16-6, 16-7,

16-8

A2. Compute and apply the

cash flow on total assets ratio.

Procedural objectives:

P1. Prepare a statement of cash

flows.

16-17

16-10, 16-

11, 16-15,

16-16, 16-18

16-1, 16-2,

16-3, 16-4,

16-5, 16-6

P2. Compute cash flows from

operating activities using

the indirect method.

6, 10, 11

16-3, 16-6,

16-14

16-3, 16-4,

16-6, 16-12,

16-13

16-1, 16-2,

16-4, 16-5,

16-7

16-6

P3. Determine cash flows from

both investing and financing

activities.

2, 3, 7, 8, 9,

15

16-4, 16-5,

16-6, 16-7,

16-8, 6-14

16-8, 16-9

16-1, 16-2,

16-3, 16-4,

16-5, 16-6

P4A.Illustrate use of a spreadsheet to

prepare a statement of

cash flows (Appendix 16A)

16-13

16-14

16-2, 16-5

P5B.Compute cash flows from

operating activities using

the direct method.(Appendix

16B)

4, 5

16-9, 16-10,

16-11

16-2, 16-5,

16-7

16-3, 16-6,

16-8

16-6

Chapter Outline

Notes

I. Basics of Cash Flow Reporting

A. Purpose of a Statement of Cash Flows

To report all major cash receipts (inflows) and cash payments

(outflows) during a period. This report classifies cash flows into

operating, investing, and financing activities. It answers important

questions such as:

1. How does a company obtain its cash?

2. Where does a company spend its cash?

3. What explains the change in the cash balance?

B. Importance of Cash Flows

Information about cash flows, and its sources and uses, can

influence decision makers in important ways.

C. Measurement of Cash Flows

The phrase, cash flows refers to both cash and cash equivalents. A

cash equivalent must satisfy two criteria:

1. Be readily convertible to a known amount of cash.

2. Be sufficiently close to its maturity date so its market value is

unaffected by interest rate changes.

D. Classifications of Cash Flows

Cash receipts and cash payments are classified and reported in one

of three categories:

1. Operating activities include transactions and events that

determine net income (with some exceptions such as unusual

gains and losses). Specific examples:

a. Cash inflows from cash sales, collections on credit sales,

receipts of dividends and interest, sale of trading

securities, and settlements of lawsuits.

b. Cash outflows for payments to suppliers for goods and

services, to employees for wages, to lenders for interest, to

government for taxes, to charities, and to purchase trading

securities.

2. Investing activities include transactions and events that affect

long-term assets, namely the purchase or sale of these assets.

Specific examples:

a. Cash inflows from selling long-term productive assets,

selling available-for-sale securities, notes and held-to–

maturity securities, and collecting principal on loans to

others.

b. Cash outflows from purchasing long-term productive

assets, purchasing available for sale securities and held-to–

maturity securities, and making loans to others.

Chapter Outline

Notes

3. Financing activities include transactions and events that affect

long-term liabilities and equity:

a. Cash inflows from owner contributions, from issuing

company’s own stock, from issuing bonds and notes and

from issuing short and long-term debt.

b. Cash outflows from repaying cash loans, owner’s

withdrawals, paying shareholder’s cash dividend and

purchasing treasury stock.

E. Noncash Investing and Financing Activities

Activities that do not affect cash receipts or payments but because

of their importance and the full disclosure principle they are

disclosed at the bottom of the statement of cash flows or in a note

to the statement.

F. Format of the Statement of Cash Flows

1. Lists cash flows by categories (operating, financing and

investing) and identifies the net cash inflow or outflow in each

category.

2. Combines the net cash flow in each of the three categories and

identifies the net change in cash for the period.

3. Combines the net change in cash with the prior period ending

cash to prove the current period ending cash.

4. Contains a separate schedule or note disclosure of any noncash

financing and investing activities.

G. Preparing the Statement of Cash Flow

1. Five steps:

a. Compute the net increase or decrease in cash (bottom line

or target number).

b. Compute and report net cash provided (used) by operating

activities (using either the direct or indirect method).

c. Compute and report net cash provided (used) by investing

activities.

d. Compute and report net cash provided (used) by financing

activities.

e. Compute net cash flow by combining net cash provided

by operating, investing, and financing activities and then

prove it by adding it to the beginning cash balance to

show that it equals the ending cash balance.

Note: Noncash investing and financing activities are disclosed

in either a note or in a separate schedule to the statement.

Chapter Outline

Notes

2. Sources of information for preparing the statement of cash

flows

a. Comparative balance sheets.

b. The current income statement.

c. Other information—generally derived from analyzing

noncash balance sheet accounts.

3. Alternative approaches to preparing the statement:

a. Analyzing the cash account.

b. Analyzing noncash accounts.

II. Cash Flows from Operating Activities

A. Indirect and Direct Methods of Reporting—Two ways of reporting

that apply only to the operating activities section.

1. Direct Method—separately lists each major item of operating

cash receipts and each major item of operating cash payments.

Cash payments are subtracted from cash receipts to determine

the net cash provided (used) by operating activities.

2. Indirect Method—reports net income and then adjusts it for

items necessary to obtain net cash provided (used) by

operating activities.

3. Note that the net cash provided (used) by operating activities

is identical under both the direct and indirect method.

B. Application of the Indirect Method of Reporting

1. Reports net income and then adjusts it for three types of items

necessary to obtain net cash provided (used) by operating

activities.

2. The three types of adjustments are:

a. to reflect changes in noncash current assets and current

liabilities.

b. to income statement items involving operating activities

that do not affect cash inflows or outflows.

c. to eliminate gains and losses resulting from investing and

financing activities (not part of operating activities).

3. Adjustments for changes in current assets and current

liabilities are made as follows:

a. Decreases in noncash current assets are added to net

income.

b. Increases in noncash current assets are subtracted from net

income.

c. Increases in current liabilities are added to net income.

d. Decreases in current liabilities are subtracted from net

Chapter Outline

Notes

4. Adjustments for operating items not providing or using cash

are made as follows:

a. Expenses with no cash outflows are added back to net

income.

b. Revenues with no cash inflows are subtracted from net

income.

5. Adjustments for nonoperating items are made as follows:

a. Nonoperating losses are added back to net income.

b. Nonoperating gains are subtracted from net income.

C. Summary of Adjustments for the Indirect method—see Exhibit 16-

12, page 644 of text.

III. Cash Flows from Investing—identical under direct and indirect

methods. Three-stage process of analysis to determine cash provided

(used) by investing activities:

A. Identify changes in investing-related accounts (all non-current

assets, and the current accounts for both notes receivable and

investments in securities—excluding trading securities).

B. Explain these changes to identify their cash flows effects using

reconstruction analysis (reconstructed entries—not the actual

entries by the preparer).

C. Report their cash flow effects.

IV. Cash Flows from Financing— identical under direct and indirect

methods. Three-stage process of analysis to determine cash provided

(used) by financing activities:

A. Identify changes in financing-related accounts (all non-current

liabilities—including current portion of any notes and bonds, and

the equity accounts).

B. Explain these changes to identify their cash flows effects using

reconstruction analysis (reconstructed entries—not the actual

entries by the preparer).

C. Report their cash flow effects.

16-7

Chapter Outline

Notes

V. Global View—Compares U.S.GAAP to IFRS

A. Both systems permit the direct or indirect approach to reporting

cash flows from operating activities and the application of both

methods are fairly consistent under both systems. Two basic

differences are:

1. U.S. GAAP requires cash inflows from interest and dividend

revenue is classified as operating activities, whereas IFRS

permits classification under operating or investing provided it

is consistent across periods.

2. U.S.GAAP requires cash outflows for interest expense to be

classified as operating activities, whereas IFRS permits

classification under operating or investing provided it is

consistent across periods.

B. Both systems are fairly similar in reporting cash flows from

investing and financing activities.

VI. Decision Analysis—Cash Flow Analysis

A. Analyzing Cash Sources and Uses

1. Managers stress understanding and predicting cash flows for

business decisions.

2. Creditor and investor decisions are also based on a company’s

cash flow evaluations.

3. Operating cash flows are generally considered to be most

significant because they represent results of ongoing

operations.

B. Cash Flow on Total Assets

1. Similar to return on total assets except the return is analyzed

based on operating cash flows rather than net income.

2. Computed by dividing cash flow from operations by average

total assets.

Chapter Outline

Notes

VII. Spreadsheet Preparation of the Statement of Cash Flows

(Appendix 16A)

A spreadsheet approach may be used to organize and analyze the

information to prepare a statement of cash flows by the indirect

method, including the supplemental disclosures of noncash investing

and financing activities.

A. The spreadsheet has four columns containing dollar amounts.

1. Columns one and four contain the beginning and ending

balances of each balance sheet account.

2. Columns two and three are for reconciling the changes in

each balance sheet account.

B. Separate sections on the working paper present (a) balance

sheet items with debit balances; (b) balance sheet items with

credit balances; (c) cash flows from operating activities,

starting with net income; (d) cash flows from investing

activities; (e) cash flows from financing activities; and (f)

noncash investing and financing activities.

C. Information for sections (c) – (f) is developed in four steps in

the Analysis of Changes columns:

1. By adjusting net income for the changes in all noncash

current asset and current liability account balances. This

reconciles the changes in these accounts.

2. By eliminating from net income the effects of all noncash

revenues and expenses. This begins the reconciliation of

noncurrent assets.

3. By eliminating from net income any gains or losses from

investing and financing activities. This involves the

reconciliation of noncurrent assets and noncurrent

liabilities and perhaps the recording of disclosures in

sections (c) – (g).

4. By entering any remaining items, such as dividend

payments, which are necessary to reconcile the changes in

all balance sheet accounts.

Chapter Outline

Notes

VIII. Direct Method of Reporting Operating Cash Flows (Appendix

16B)

A. Separately list each major item or class of operating cash

receipts and cash payments.

B. Classes of operating cash receipts include cash received from

customers, renters, interest, and dividends.

C. Classes of operating cash payments include cash paid to

suppliers, to employees and other operating expense, interest,

and income taxes.

D. Subtract the cash payments from cash receipts to determine

the net cash provided (used) by operating activities.

E. The items to be listed are determined by adjusting individual

accrual basis income statement items to cash basis items. This

is done by determining the impact from changes in their

related balance sheet accounts.

F. Exhibit 16B.6 (p. 661) summarizes the common adjustments

for the items making up net income to arrive at net cash

provided (used) by operating activities under the direct

method.

G. This is the method recommended (but not required) by the

FASB.

H. When the direct method is used, the FASB requires a

reconciliation of net income to net cash provided (used) by

operating activities. This is operating cash flows computed

using the indirect method.