Title: Problem 3-5B

Part 1

QA_Ori:

SPEEDY COURIER

Income Statement

For Year Ended December 31, 2013

Revenues

Delivery fees earned

$611,80

0

Interest earned 34,000

Total revenues

$645,80

0

SPEEDY COURIER

Statement of Owner’s Equity

For Year Ended December 31, 2013

L. Horace, Capital, December

31, 2012

$125,00

0

SPEEDY COURIER

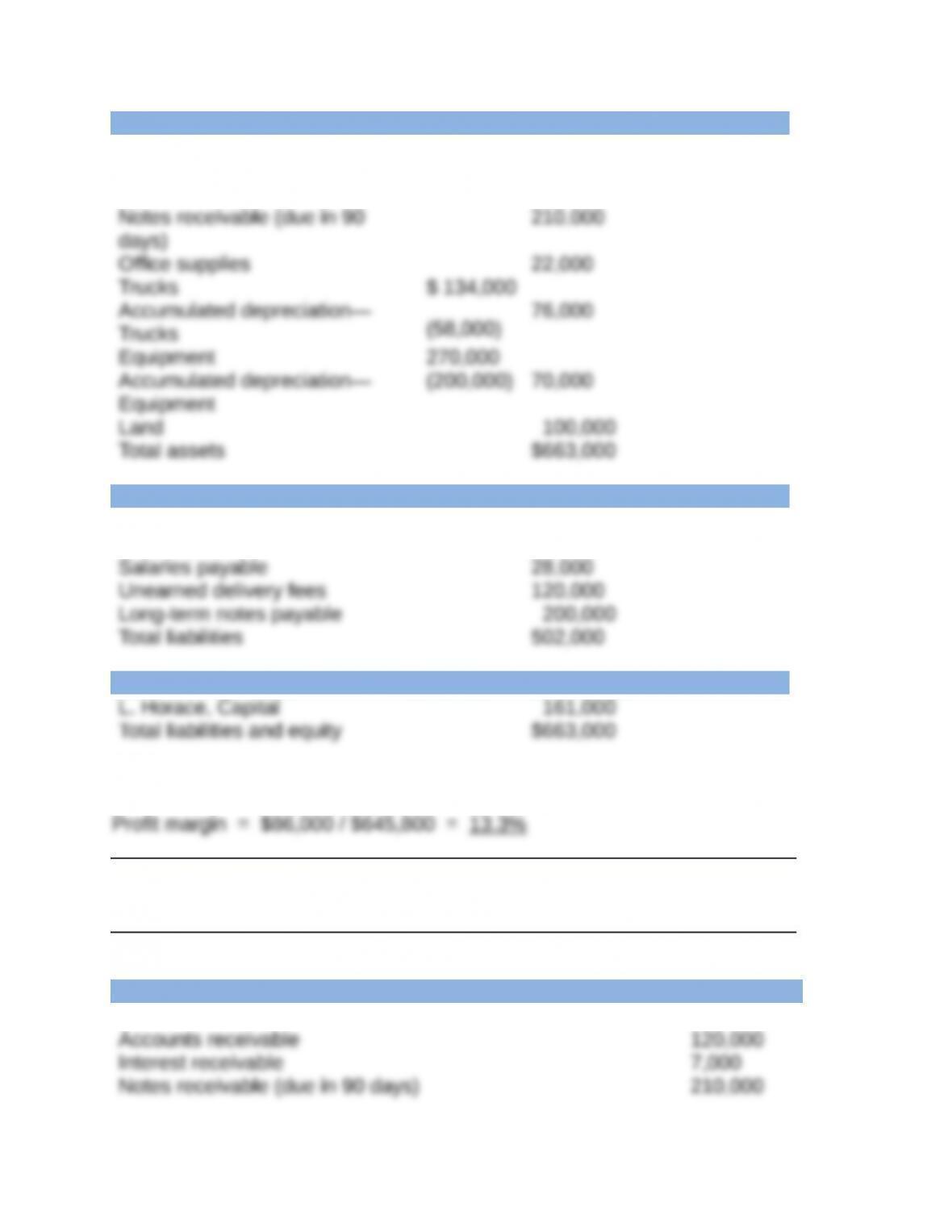

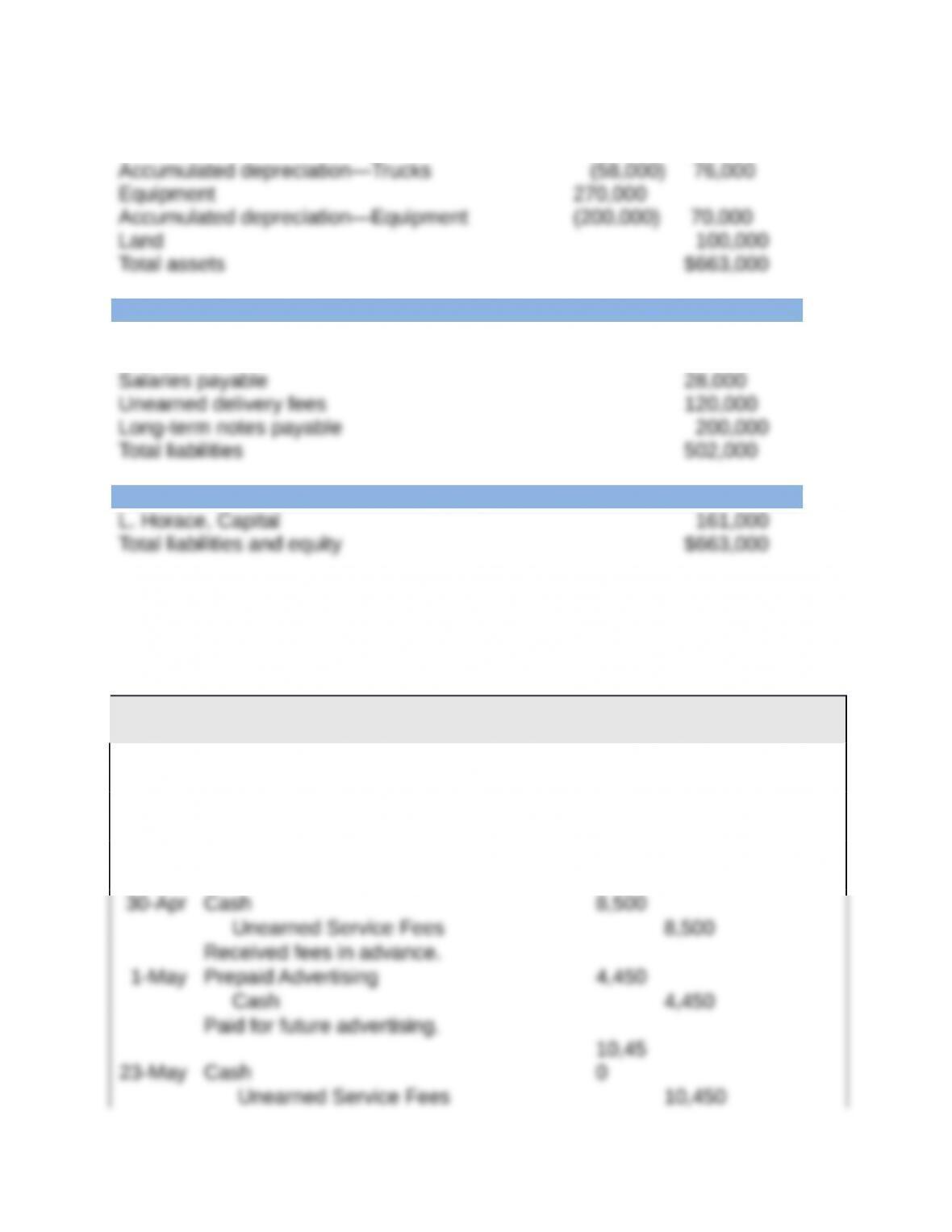

Balance Sheet

December 31, 2013

Assets

Cash $ 58,000

Accounts receivable 120,000

Interest receivable 7,000

Liabilities

Accounts payable $134,000

Interest payable 20,000

Equity

Part 2

SPEEDY COURIER

Balance Sheet

December 31, 2013

Assets

Cash $ 58,000

Office supplies 22,000

Trucks $ 134,000

Liabilities

Accounts payable $134,000

Interest payable 20,000

Equity

Title: Problem 3-6BA

QA_Ori:

Part 1

Method that records prepaid expenses and unearned revenues in balance sheet

accounts

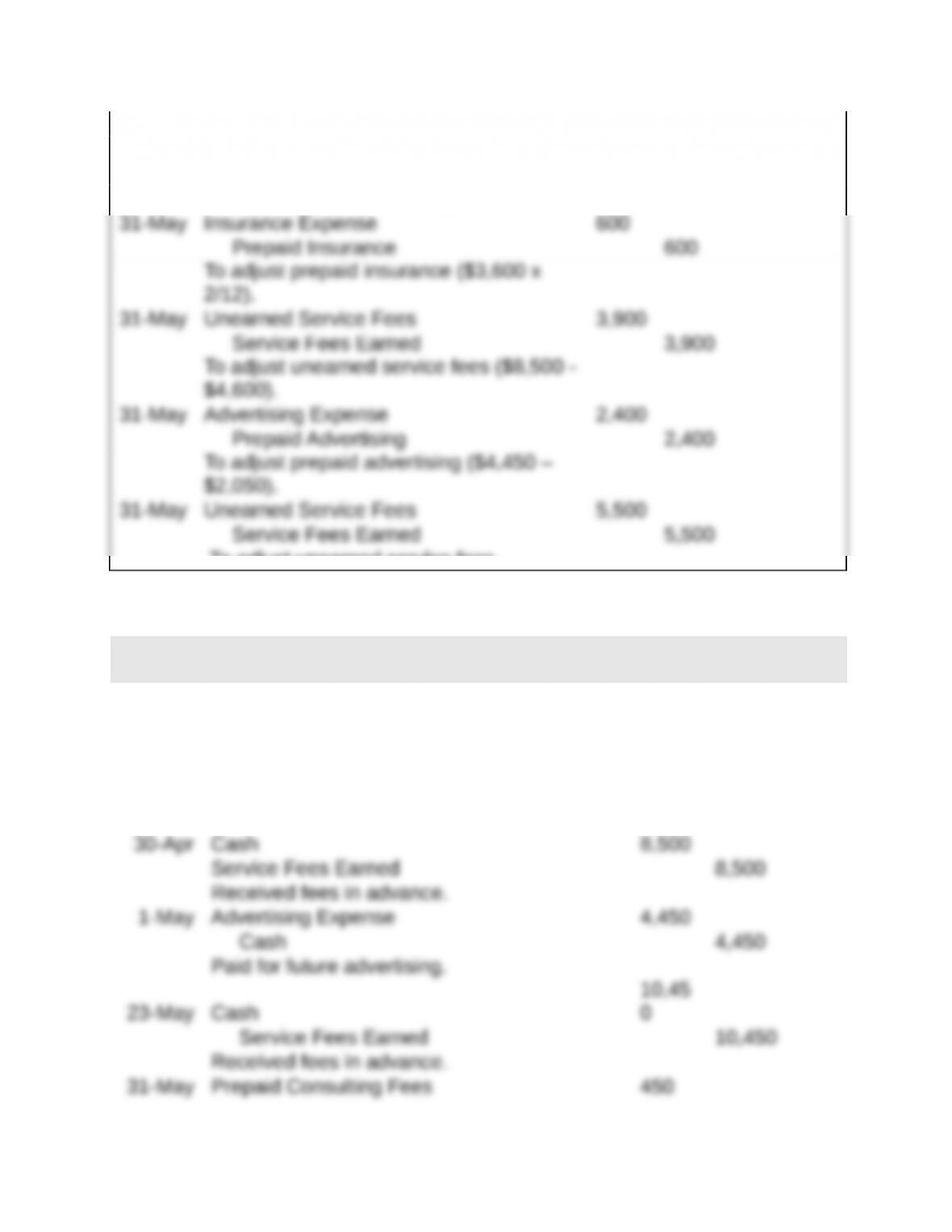

1-Apr Prepaid Consulting Fees 2,450

Cash 2,450

Paid for future consulting services.

1-Apr Prepaid Insurance 3,600

Cash 3,600

Paid insurance for one year.

Received fees in advance.

31-May Consulting Fees Expense 2,000

Prepaid Consulting Fees 2,000

To adjust prepaid consulting fees.

To adjust unearned service fees.

Part 2

Method that records prepaid expenses and unearned revenues in income

statement accounts

1-Apr Consulting Fees Expense 2,450

Cash 2,450

Paid for future consulting services.

1-Apr Insurance Expense 3,600

Cash 3,600

Paid insurance for one year.

Consulting Fees Expense 450

To adjust prepaid consulting fees ($2,450 –

$2,000).

Part 3

There are no differences between the two methods in terms of the amounts that

appear on the financial statements. In both cases, the financial statements

reflect the following:

Prepaid consulting fees as of May 31 $450

When prepaid expenses and unearned revenues are recorded in balance sheet

Title: Serial Problem, Success Systems

QA_Ori:

Part 1

<Note: The general ledger is displayed at the end of Part 6>

Journal entries

2-Dec Advertising Expense 655

1,02

5

Cash 101 1,025

Paid share of mall advertising costs.

3-Dec Repairs Expense–Computer 684 500

Cash 101 500

Repaired the computer.

3,95

Paid cash for owner withdrawal.

Part 2

Adjusting entries

31-De

c Computer Supplies Expense 652

3,06

5

3,06

31-De

c Insurance Expense 637 555

31-De

c Wages Expense 623 500

31-De

Depreciation

1,25

Adjustment for computer equipment

depreciation:

$20,00

31-De

c Depreciation Expense—Office Equip 612 400

Accumulated Depreciation—Office

Equipment 164 400

31-De

c Rent Expense 640

2,47

5

2,47

Part 3

SUCCESS SYSTEMS

Adjusted Trial Balance

December 31, 2013

Debit Credit

Cash $58,160

Accounts receivable 5,668

Computer supplies 580

Prepaid insurance 1,665

Prepaid rent 825

Office equipment 8,000

Totals

4

4

Part 4

SUCCESS SYSTEMS

Income Statement

For Three Months Ended December 31, 2013

Revenue

Computer services revenue $31,284

Expenses

Depreciation expense—Office

equipment $400

Depreciation expense—Computer

Part 5

SUCCESS SYSTEMS

Statement of Owner’s Equity

For Three Months Ended December 31, 2013

A. Lopez, Capital, October 1, 2013

$83,00

0

Plus: Net income 14,248

97,248