21–1

CHAPTER 21

COST-VOLUME-PROFIT ANALYSIS

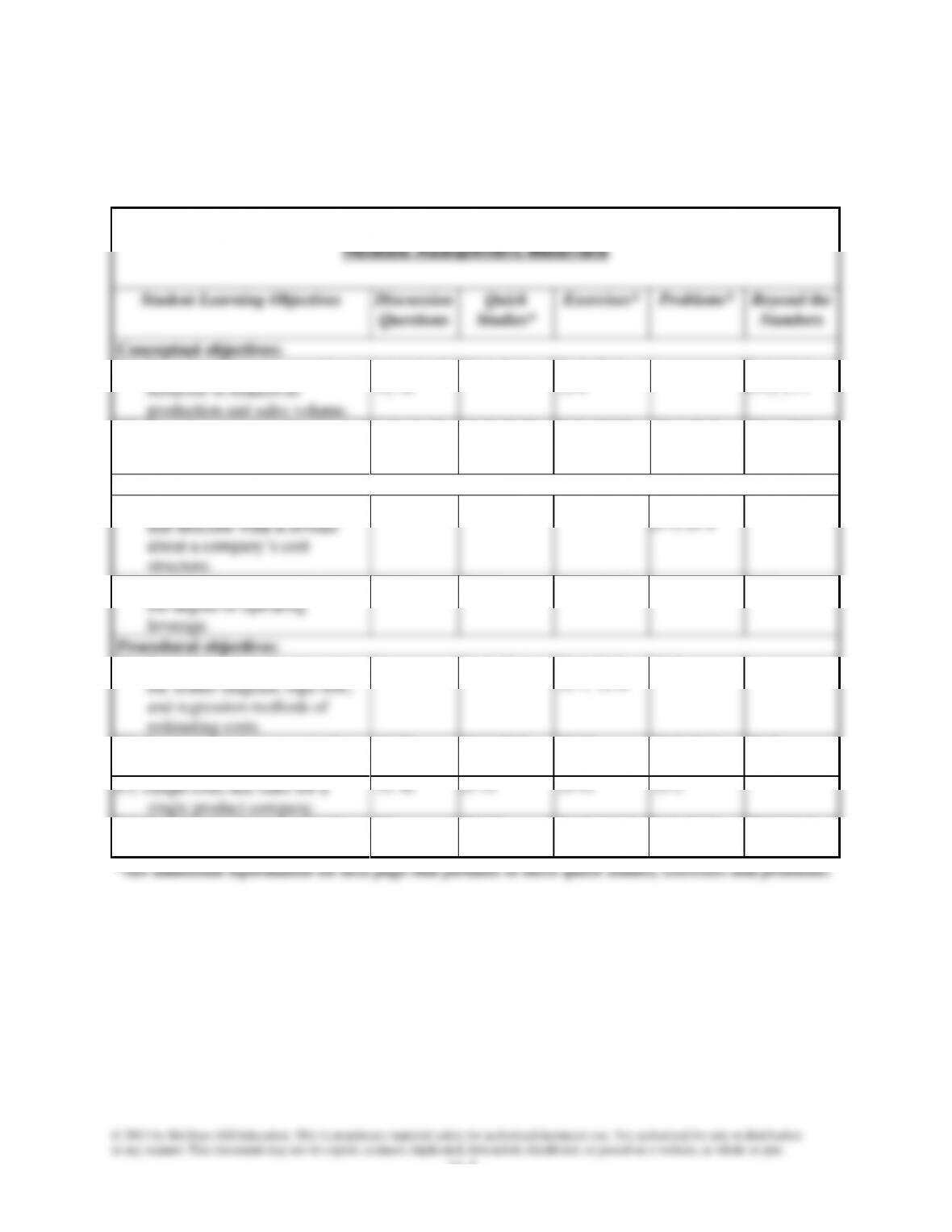

Related Assignment Materials

Student Learning Objectives

Discussion

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Describe different types of cost

behavior in relation to

production and sales volume.

1,2, 3, 5, 10,

12, 19

21-1, 21-2,

21-2, 21-3,

21-4

21-1, 21-3,

21-5, 21-7

C2. Describe several applications of

cost-volume-profit analysis.

4, 9, 11, 21

21-7, 21-10

21-5, 21-12,

21-13, 21-14,

21-15, 21–16

21-4, 21-5,

22–4, 22-6

Analytical objectives:

A1. Compute contribution margin

and describe what it reveals

about a company’s cost

structure.

6, 7, 8

21-5, 21-14

21-1, 21-4,

21-5, 21-6

21-7

A2. Analyze changes in sales using

the degree of operating

leverage.

17, 18

21-11

21-9, 21-21

21-2

Procedural objectives:

P1. Determine cost estimates using

the scatter diagram, high-low,

and regression methods of

estimating costs.

13

21-3, 21-4

21-1, 21-6

21-7, 21-8

21-3

P2. Compute break-even point for a

single product company.

14, 20

21-6, 21-8,

21-9

21-10

21-2, 21-4,

21-6

21-2

P3. Graph costs and sales for a

single product company.

15, 16

21-13

21-11

21-2

P4. Compute break-even point for a

multiproduct company.

20

21-12

21-17, 21-18,

21-19, 21-20

21-5, 21-7

22-8, 21-9

21–2

Additional Information on Related Assignment Material

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode.

Corresponding problems in set B also relate to learning objectives identified in grid on previous page.

Problems 21-2A and 21-6A can be completed using EXCEL. The Serial Problem for Success Systems

starts in this chapter and continues throughout many chapters of the text. It is most readily solved

manually if you use the working papers that accompany text.

Narrated PowerPoint Correlation Guide

Learning Objective

Slides

C1

3-7

P1

8-13

A1

14-16

P2

17-19

P3

20-22

C2

23-30

P4

31-37

A2

39-40

Synopsis of Chapter Revision

• Leather Head Sports: NEW opener with new entrepreneurial assignment

• Was Chapter 22 in prior edition

Chapter Outline

I. Identifying Cost Behavior (CVP analysis) ⎯Cost-volume-profit

analysis is a tool to predict how changes in costs and sales levels affect

income; conventional CVP analysis requires that all costs must be

classified as either fixed or variable with respect to production or sales

volume before CVP analysis can be used.

A. Fixed Costs

1. A total fixed cost remains unchanged in amount when volume

product are usually plotted on the horizontal axis and dollars

of cost are plotted on the vertical axis. (Exhibit 21.1)

(cost remains constant at all levels of volume within the

relevant range).

b. Intersection point of line on cost (vertical) axis is at fixed

cost amount.

4. Likely that amount of fixed cost will change when outside of

variable cost changes with the level of production. (Exhibit

21-1)

a. Variable cost is represented by a straight line starting at

the zero cost level.

b. The straight line is upward (positive) sloping. The line

rises as volume increases.

C. Mixed Costs

1. Include both fixed and variable cost components.

2. When volume and cost are graphed, (Exhibit 21-1)

level increases, mixed cost line increases at an amount

equal to the variable cost per unit.

3. Mixed costs are often separated into fixed and variable

components when included in a CVP analysis.

Notes

Chapter Outline

D. Step-wise Costs

1. Fixed within a relevant range of the current production

volume. If production volume expands significantly, total

costs go up by a lump-sum amount (stair-step cost).

2. Treated as either fixed or variable cost in conventional CVP

E. Curvilinear (or Nonlinear) Costs

1. Increase at a non-constant rate as volume increases.

as a curved line that starts at intersection point of cost axis and

volume axis (total cost is zero when volume is zero) and

II. Measuring Cost Behavior⎯After establishing that cost data are

reliable and useful in predicting future costs, three methods are

commonly used to analyze past cost behavior.

“fits” the points visually.

a. Intersection point of line on cost axis is at fixed cost

amount.

b. The variable cost per unit of volume equals the slope of

the line.

i. Select any two points on horizontal axis.

ii. Draw a vertical line from each of these points to

intersect the estimated line of cost behavior.

iii. The slope of the line, or variable cost per unit is

Notes

21–5

Chapter Outline

B. High-low Method

1. Estimate the cost equation by graphically connecting the two

cost amounts at the highest and lowest unit volumes.

(Exhibit 21-5)

b. Variable cost per unit is the slope of the line⎯is computed

as the change in cost divided by the change in units:

Variable cost = high volume costs – low volume costs

the highest and lowest resulting in less precision.

C. Least-Squares Regression⎯computation details covered in

advanced cost accounting courses.

5. Statistical method of identifying cost behavior.

6. Cost equation readily calculated using most spreadsheet

due to use of all data points available.

III. Break-Even Analysis⎯special case of CVP analysis.

A. Contribution Margin

1. Requires separating costs and expenses by behavior (fixed or

per unit basis).

3. Contribution margin per unit (CM per unit) is computed as:

Selling price per unit minus Variable cost per unit

4. Contribution margin ratio—the proportion of a unit’s selling

unit variable costs).

5. Contribution margin ratio (CM %) is computed as:

contribution margin per unit divided by sales price per unit.

Notes

Chapter Outline

B. Computing Break-Even Point

a loss.

b. Can be expressed either in units or dollars of sales.

CM per unit

b. Break-even sales dollars = Fixed costs

CM%

c. Contribution Margin Income Statement

Margin of safety (units) Margin of Safety (dollars)

D. Preparing a Cost-Volume-Profit Chart (also called a break-even graph

or chart)

3. Three steps:

a. Plot fixed costs on vertical axis; draw horizontal line at this

level to show that FC remains unchanged regardless of output

volume.

b. Draw line reflecting total costs (variable costs plus fixed

costs) for a relevant range of volume levels.

i. Line starts at fixed costs on vertical axis.

Notes

Chapter Outline

c. Draw sales line.

i. Line starts at origin (zero units and zero dollars of sales).

ii. Slope of line is equal to selling price per unit; compute

total revenues for any volume level, and connect this

point with the origin.

a. Volume levels to left of break-even point⎯vertical distance

is amount of loss expected because the total costs line is

above the total sales line.

b. Volume levels to right of break-even point⎯vertical distance

is amount of profit expected because the total sales line is

above the total costs line.

2. If expected cost and revenue behavior is different from three

assumptions stated above, CVP analysis may still be useful.

can offset each other. The same can be said for fixed costs.

b. Relevant range of operations⎯Assumes a specific cost is

variable or fixed is more likely valid when operations are

within the relevant range. (If normal range of activity

changes, some costs may need reclassification.)

Notes

Chapter Outline

IV. Applying Cost-Volume-Profit Analysis ⎯Useful in helping managers

evaluate likely effects of strategies considered in planning business

– Variable Costs (# units sold x unit variable cost)

Contribution Margin

– Fixed Costs

fixed costs + target pretax income

CM%

fixed costs + target pretax income

CM

compute sales for a target income (exhibit 21.24)

C. Sensitivity Analysis⎯Knowing the effects of changing some

estimates used in CVP analysis by substituting new estimated

amounts (in total or per unit as appropriate) in the related formula can

known and remains constant.

2. Sales mix is the ratio (proportion) of the sales volumes for

various products.

3. To apply multiproduct CVP analysis, estimate break-even point

by using a composite unit.

a. Determine sales mix of various products.

b. Composite Unit—a specific number of units of each product

in proportion to their expected sales mix. Multi-product CVP

treats this composite unit as a single product

Notes

Chapter Outline

e. Determine the CM per composite unit by subtracting the total

variable price from the total selling price of the composite

unit

f. In break-even analysis, a composite unit is treated as a unit

of a single product.

g. Break-even point in composite units is computed as:

Fixed Costs _

CM per composite unit

c. Compute the contribution margin per unit of each product.

(sales price per unit less variable cost per unit).

d. Multiply the contribution margin per unit for each unit x the

f. Divide fixed costs by the weighted average contribution

margin to compute the break-even point in units.

V. Decision Analysis—Degree of Operating Leverage⎯Useful tool in assessing

the effect of changes in the level of sales on income.

Notes

21–10

Alternate Demo Problem Twenty-One

Trimble Company sells an electronic toy for $40. The variable cost is $24

per unit and the fixed cost is $32,000 per year. Management is considering

the following changes:

Alternative #1

Lease a new packaging machine for $4,000 per year, which will reduce

variable cost by $1 per unit.

Alternative #2

Increase selling price 10 percent to counteract an expected 25 percent

increase in fixed cost.

Alternative #3

Reduce fixed cost by 25 percent by moving to a lower rent location. This

would have the effect of increasing variable costs by 10 percent.

Required:

Consider and answer each of the following questions independently:

Round calculations to the nearest unit

(a) Determine the current break-even point in units and dollars.

(b) Determine the expected profit assuming alternative #1 and sales of

3,200 units.

(c) Determine the break-even point in units and dollars assuming

alternative #2.

(d) Determine the break-even point required in units and dollars

assuming alternative #3.

(e) Determine the volume of sales required to earn $23,600 assuming

alternative #3.

21–11

Solution: Alternate Demo Problem Twenty-One

(a)

Break-even point (in units) = Fixed costs/CM per unit

$32,000/($40 per unit – $24 per unit) = 2,000 units

2,000 units x $40 per unit = $80,000 dollars

(or)

Break-even point (in dollars) = Fixed costs/CM ratio

$32,000/[($40 per unit –$16 per unit)/$40 per unit] = $80,000

$80,000 dollars/$40 per unit = 2,000 units

(b)

Net income = (CM per unit x number of units sold) – Fixed costs

New fixed costs = $32,000 + $4,000 = $36,000

New CM = $40 per unit – $23 per unit = $17 per unit

($17 per unit x 3,200 units) – $36,000 = $18,400

(c)

Break-even point (in units) = Fixed costs/CM per unit

New fixed costs = $32,000 + $8,000 = $40,000

New CM = $44 per unit – $24 per unit = $20 per unit

$40,000/$20 per unit = 2,000 units

2,000 units x $44 per unit = $88,000

(d)

Break–even point (in units) = Fixed costs/CM per unit

New fixed costs = $32,000 – $8,000 = $24,000

New CM = $40 per unit – $26.40 per unit = $13.60 per unit

$24,000/$13.60 per unit = 1,765 units

1,765 units x $40 per unit = $70,600

(e)

Required sales (in units) = (Fixed costs + Target NI)/CM per unit

($24,000 + $23,600)/$13.60 per unit = 3,500 units