Comprehensive Problem (Continued)

Part 3

2013

(a)

Miscellaneous Expenses ……………………………………..

15

Accounts Payable ………………………………………………..

1,287

Interest Revenue …………………………………………….

52

Cash ……………………………………………………………...

1,250

Adjust cash account. (Separate entries are acceptable.)

(b1)

Allowance for Doubtful Accounts ………………………....

679

Accounts Receivable ……………………………………...

679

Wrote off uncollectible accounts.

(b2)

Bad Debts Expense ……………………………………………...

551

Allowance for Doubtful Accounts …………………....

551

Recognize bad debts expense.

(c)

Depreciation Expense—Trucks ……………………………..

6,000

Accumulated Depreciation—Trucks ………………...

6,000

Depreciation on truck.

(d)

Depreciation Expense—Equipment ……………………....

6,100

Accumulated Depreciation—Equipment …………..

6,100

Depreciation on equipment.

(e)

Extermination Services Revenue …………………………..

2,240

Unearned Services Revenue …………………………..

2,240

Adjust for unearned revenues.

(f)

Warranty Expense ………………………………………………..

1,444

Estimated Warranty Liability …………………………..

1,444

Estimate warranty expense.

(g)

No interest accrual required for 2013

Comprehensive Problem (Continued)

Part 4

BUG-OFF EXTERMINATORS

Income Statement

For Year Ended December 31, 2013

Revenues

Extermination services revenue ……………

$57,760

Sales ……………………………………………………

71,026

Interest revenue ………………………………..…

924

Total revenues…………………………………..…

$129,710

Expenses

Cost of goods sold ………………………………

46,300

Depreciation expense—Trucks ………….…

6,000

Depreciation expense—Equipment ………

6,100

Wages expense ……………………………………

35,000

Interest expense………………………………..…

0

Rent expense…………………………………….…

9,000

Bad debts expense ………………………………

551

Miscellaneous expenses ………………………

1,241

Repairs expense ……………………………….…

8,000

Utilities expense………………………………..…

6,800

Warranty expense ……………………………..…

1,444

Total expenses ………………………………….…

120,436

Net income ……………………………………………

$ 9,274

BUG-OFF EXTERMINATORS

Statement of Owner’s Equity

For Year Ended December 31, 2013

D. Buggs, Capital, December 31, 2012 ……………….……

$ 59,700

Add: Investments by owner …………………………….……

0

Net income ……………………………………………..……

9,274

68,974

Less: Withdrawals by owner …………………………….……

(10,000)

D. Buggs, Capital, December 31, 2013 ……………………

$ 58,974

Comprehensive Problem

Part 4 (concluded)

BUG-OFF EXTERMINATORS

Balance Sheet

December 31, 2013

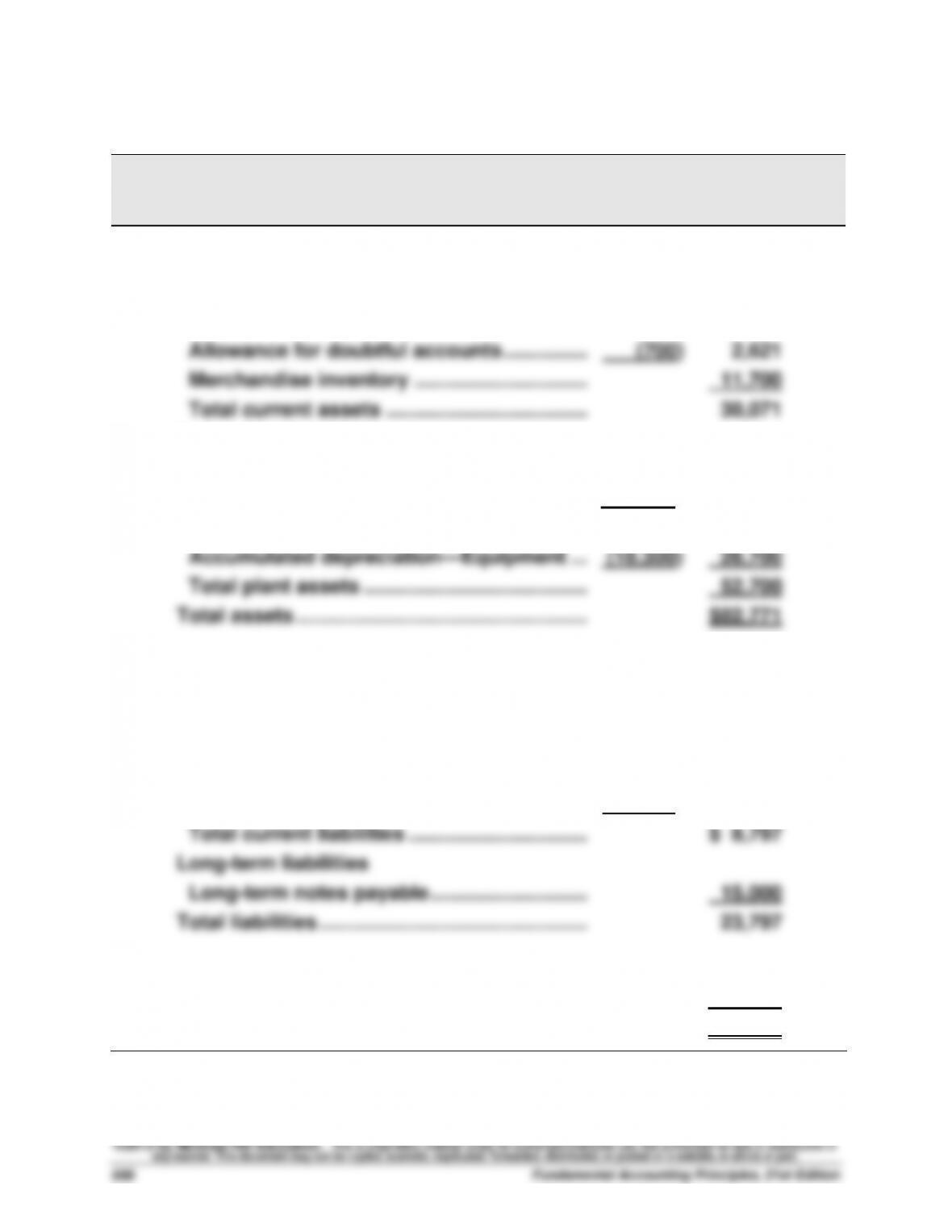

Assets

Current assets

Cash ……………………………………………………....

$15,750

Accounts receivable ………………………………..

$ 3,321

Allowance for doubtful accounts ……………..

(700)

2,621

Merchandise inventory …………………………..

11,700

Total current assets ………………………………..

30,071

Plant assets

Trucks …………………………………………………....

32,000

Accumulated depreciation—Trucks ………...

(6,000)

26,000

Equipment ……………………………………………...

45,000

Accumulated depreciation—Equipment …..

(18,300)

26,700

Total plant assets …………………………………...

52,700

Total assets ……………………………………………...

$82,771

Liabilities

Current liabilities

Accounts payable …………………………………...

$ 3,713

Estimated warranty liability ……………………..

2,844

Unearned services revenue ……………………..

2,240

Total current liabilities …………………………..

$ 8,797

Long-term liabilities

Long-term notes payable ………………………...

15,000

Total liabilities …………………………………………..

23,797

Equity

D. Buggs, Capital ……………………………………...

58,974

Total liabilities and equity ………………………....

$82,771

Reporting in Action — BTN 11-1

1. Times interest earned

($ thousands)

2011

2010

2009

Net income …………………………………..………

$227,575

$147,138

$101,017

Add income taxes ………………………..…

119,051

71,403

50,157

Add interest expense …………………..………

3,987

2,680

4,111

Income before taxes and interest ….………

$350,613

$221,221

$155,285

Times interest earned ratio …………..…..

87.9a

82.5b

37.8c

a$350,613/$3,987

b$221,221/$2,680

c$155,285/$4,111

Analysis comment: For each of these fiscal years, it is obvious that

2. Loyalty reward liabilities arise when a customer makes a purchase

under a frequent purchase program. It is an estimated liability as the

3. Yes. Polaris has both commitments and contingencies (see its Note

4. The solution depends on the financial statement information accessed.

Comparative Analysis — BTN 11-2

1. Polaris—Times interest earned

($ thousands)

Current

Year

One Year

Prior

Two Years

Prior

Net income …………………………………..………

$227,575

$147,138

$101,017

Add income taxes ………………………..…

119,051

71,403

50,157

Add interest expense …………………..………

3,987

2,680

4,111

Income before taxes and interest ….………

$350,613

$221,221

$155,285

Times interest earned ratio …………..…..

87.9a

82.5b

37.8c

a$350,613/$3,987

b$221,221/$2,680

c$155,285/$4,111

Arctic Cat—Times interest earned

($ thousands)

Current

Year

One Year

Prior

Two Years

Prior

Net income (loss) …………………………..

$ 13,007

$1,875

$ (9,508)

Add income taxes (benefit) …………..………

5,224

(777)

(6,247)

Add interest expense …………………..………

11

250

1,015

Income before taxes and interest ….………

$ 18,242

$1,348

$(14,740)

Times interest earned ratio …………..…..

1,658.4a

5.4b

(14.5)c

a$18,242/$11

b$ 1,348/$250

2. Polaris and Arctic Cat both are in very strong positions in their ability to

make any interest payments should their income decline based on the

Ethics Challenge — BTN 11-3

1. It is in Bly’s self-interest to maximize the amount of revenues less

warranty expenses so as to maximize his personal bonus. Since Bly

2. Although Bly might be able to affect the amount of revenues less

warranty expenses via the warranty expense accrual in the short run,

over several years the amounts should even out. The dealership

Communicating in Practice — BTN 11-4

MEMORANDUM

To:

Tom Pretti, General Manager

From:

Dusty Johnson, Manager⎯Accounting and Finance

Date:

Subject:

Reporting warranties in financial statements

This memorandum is in response to your comment on my proposal for the

treatment of a contingency in our financial statements. You specifically

object to the proposed recognition of an expense and liability for

warranties. The purpose of this memorandum is to respond to your

objection.

Both the conservatism and matching principles apply to accounting for

warranties. Conservatism requires us to include an expense in this year’s

financial statements for costs that we may or may not pay in the future.

income measure would be incomplete if it did not match the cost of

fulfilling the warranty against revenues generated by offering the warranty.

This treatment would be in compliance with the matching principle.

Your comment also raised the objection that we don’t know what costs

reasonableness of repair costs. If the product is different from others, we

may have a basis for going with only a note disclosure. However, financial

statement recognition is a more effective way to get the information into

users’ hands. As a result, it is usually preferred, even if we are uncertain

about the amount.

Taking It to the Net — BTN 11-5

1. McDonald’s 2011 current liabilities include the following:

• Accounts payable

• Income taxes

• Current maturities of long-term debt

2. The portion of long-term debt maturing in the next 12 months ($

millions) is:

3. Times interest earned for McDonald’s as of 12/31/2011

($ millions)

12/31/2011

Net Income ……………………………………………………...

$ 5,503.1

Plus income taxes …………………………………………...

2,509.1

Plus interest expense ……………………………………….

492.8

Income before interest and taxes ……………………..

$ 8,505.0

Times interest earned ……………………………………...

17.26

times

Teamwork in Action — BTN 11-6

1. Option A: Interest Expense = $6,000 x 10% x 90/360 = $150

The interest expense in option B does exceed option A. If interest cost

is the only consideration, then Option A is the preferred loan. However,

2. Entries:

2a. Issue date, Option A

June 1

Cash …………………………..………………………………..….

6,000

Notes Payable …………………………………………….

6,000

Borrowed cash by issuing an

interest-bearing note.

6,000

Borrowed cash by issuing an

interest-bearing note.

Notes Payable ………………………………………………….

6,000

6,150

Repaid note plus interest.

Notes Payable ………………………………………………….

6,160

Repaid note plus interest.

Teamwork in Action (Concluded)

4. Entries:

4a. Adjusting entry, Option A (Dec. 31)

Dec. 31

Interest Expense …………………………………………..….

50

Interest Payable ………………………………………….

50

Accrue interest on note

payable [$6,000 x 10% x 30/360].

4b. Adjusting entry, Option B (Dec. 31)

Dec. 31

Interest Expense …………………………………………..….

40

Interest Payable ………………………………………….

40

Accrue interest on note payable

[$6,000 x 8% x 30/360].

4c. Maturity date entry, Option A

March 1

Interest Expense …………………………………………..….

100

Interest Payable ……………………………………………….

50

Notes Payable ………………………………………………….

6,000

Cash ……………………………………………………….

6,150

Repaid note plus interest.

4d. Maturity date entry, Option B

March 31

Interest Expense …………………………………………..….

120

Interest Payable ……………………………………………….

40

Notes Payable ………………………………………………….

6,000

Cash ……………………………………………………….

6,160

Repaid note plus interest.

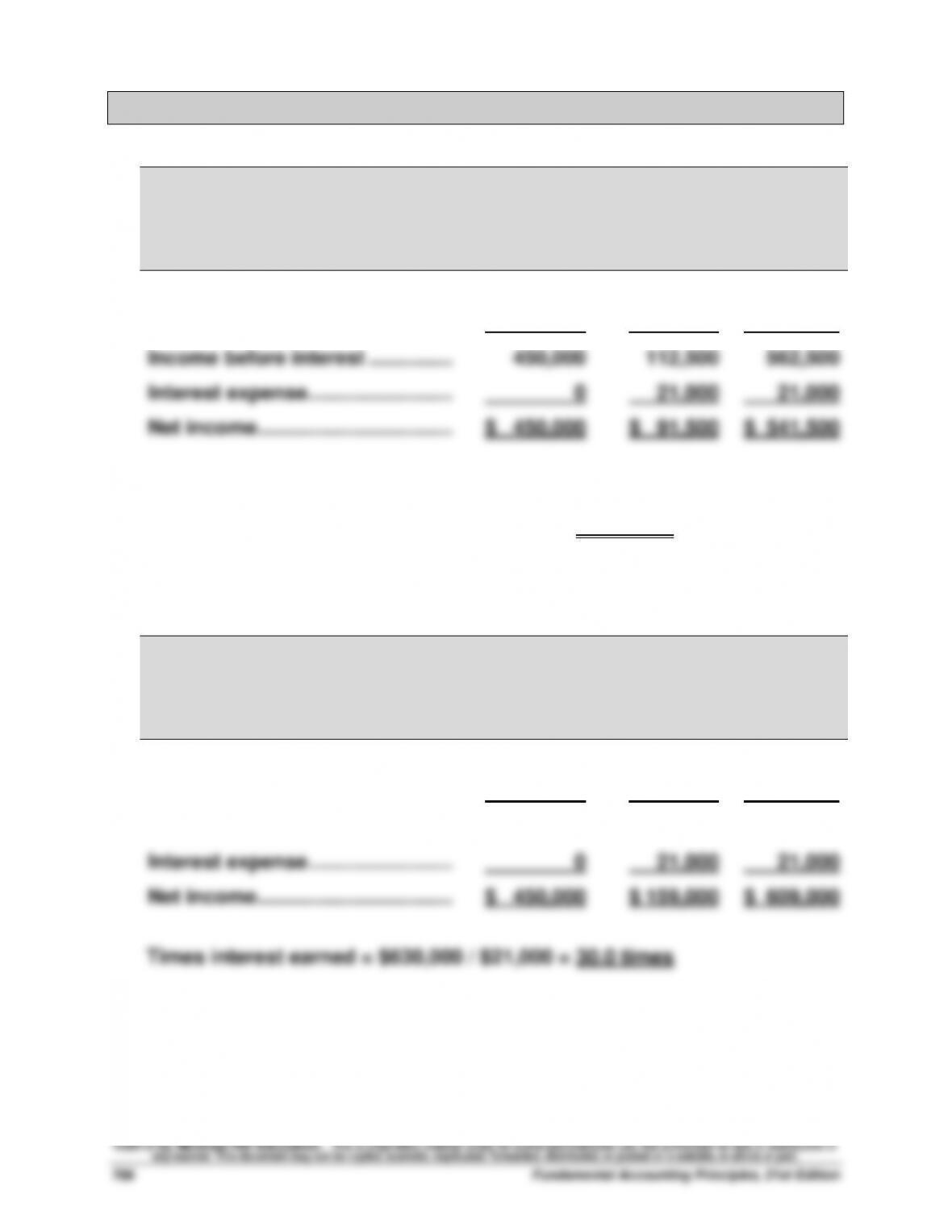

Entrepreneurial Decision — BTN 11-7

1.

SmartIT Staffing

Income Statement (Prospective)

Current

Operations

European

Total

Sales ………………………………………

$1,000,000

$ 250,000

$1,250,000

Operating expenses (55%) ………

550,000

137,500

687,500

Income before interest ……………

450,000

112,500

562,500

Interest expense……………………..

0

21,000

21,000

Net income ……………………………..

$ 450,000

$ 91,500

$ 541,500

2. Times interest earned = $562,500 / $21,000 = 26.8 times

3.

SmartIT Staffing

Income Statement (Prospective)

Current

Operations

European

Total

Sales ………………………………………

$1,000,000

$ 400,000

$1,400,000

Operating expenses (55%) ………

550,000

220,000

770,000

Income before interest ……………

450,000

180,000

630,000

Interest expense……………………..

0

21,000

21,000

Net income ……………………………..

$ 450,000

$ 159,000

$ 609,000

Times interest earned = $630,000 / $21,000 = 30.0 times

Entrepreneurial Decision (concluded)

4.

SmartIT Staffing

Income Statement (Prospective)

Current

Operations

European

Total

Sales ………………………………………

$1,000,000

$ 100,000

$1,100,000

Operating expenses (55%) ………

550,000

55,000

605,000

Income before interest ……………

450,000

45,000

495,000

Interest expense……………………..

0

21,000

21,000

Net income ……………………………..

$ 450,000

$ 24,000

$ 474,000

Times interest earned = $495,000 / $21,000 = 23.6 times

5. In each of these cases, the company’s times interest earned is at least

Hitting the Road — BTN 11-8

There is no formal solution to this problem. A discussion of the

Global Decision — BTN 11-9

1. KTM— Times interest earned

(Euro in thousands)

Current Year

One Year Prior

Net income ………………………………………....

€ 20,818

€ 2,660

Add income taxes ………………………………..

1,709*

(229)

Income before income taxes ………………..

19,109

2,889

Add interest expense …………………………..

9,693

4,256

Income before taxes and interest ………...

€ 28,802

€ 7,145

Times interest earned ratio …………………..

3.0a

1,7b

* Income tax is added for the current year, which is not normal. This is because of a tax loss

carryforward in Austria (which is explained in advanced courses).

a 28,802/ 9,693

b 7,145/ 4,256

2. Of these three companies, Polaris and Arctic Cat both have superior

coverage of interest expense for the current year. Specifically,

Polaris’s times interest earned of 87.9 for the current year and Arctic