Chapter 18

Managerial Accounting

Concepts and Principles

QUESTIONS

1. The managerial accountant plays an important role in preparing the information

necessary for effective planning and control decisions. One example is the budget,

2.

Financial Accounting

Managerial Accounting

(a) Users and decision

makers

Investors, creditors, and

other users external to the

organization

Managers, employees, and

decision makers internal to

the organization

(b) Purpose of

information

Assist external users in

making investment, credit,

and other decisions

Assist managers in making

planning and control

decisions

(c) Flexibility of practice

Structured and often

controlled by GAAP

Relatively flexible (no

GAAP)

(d) Time dimension

Historical information with

minimum predictions

Many projections and

estimates; historical

information also presented

(e) Focus of information

Emphasis on whole

organization

Emphasis on projects,

processes, and subdivision

of an organization

(f) Nature of

information

Monetary information

Mostly monetary; but also

nonmonetary information

Fundamental Accounting Principles, 21st Edition

1026

3. A customer orientation has led companies to adopt the principles of the lean

business model in response to consumer demands. The essence of customer

4. Direct labor refers to the efforts of employees who physically convert materials to

5. Factory overhead is limited to indirect costs that are incurred in the production

process. That is, it consists of activities that support the production process, such

6. Direct materials are raw materials that physically become part of the product and

can be clearly traced to specific units or batches of product. Indirect materials are

7. Direct labor can be either a prime cost or a conversion cost.

8. Direct costs include: costs of materials such as tires, seats, fuel tanks, tracks and

instruments, as well as the labor of workers who assemble the products.

9. Management should be evaluated on the basis of controllable costs. This is

10. Management usually must be able to predict financial performance to be successful.

11. Product costs are capitalized because they represent a future value (an asset) to the

12. A manufacturing business produces a product, whereas in a merchandising or

service business this is not the case. In making a product, the manufacturing

13. To run a successful business, management must make predictions and estimates

14. A manufacturing firm converts raw materials into finished products. A

manufacturing company would report three types of inventories on its balance

sheet: raw materials, goods in process, and finished goods. The finished goods are

15. Manufacturers’ balance sheets usually include small tools, factory buildings, factory

16. Manufacturing firms have inventories at various states of completion. Manufacturing

a product requires raw materials, which are converted to finished goods.

17. Manufacturing activities of a company are described in the manufacturing

18. The three categories of manufacturing costs are: direct materials, direct labor, and

factory overhead.

19. Examples of factory overhead costs include: indirect materials, indirect labor,

depreciation of the factory equipment and plant, amortization of patents, the cost of

Fundamental Accounting Principles, 21st Edition

1028

20.

Components of Manufacturing Statement

Polaris Examples

Direct material ………………………………………………..……..

Tracks, tires, seats

Direct labor …………………………………………………….…

Wages of production employees

Factory overhead ……………………………………………………..

Factory heat, factory lighting

Computation of cost of goods manufactured ……………..

Computation (see Exhibit 18.16)

21.

Arctic Cat

Manufacturing Statement

For Year Ended December 31, 2011

The date matches the period of the income statement. The “manufacturing

statement” supports the income statement in computing cost of goods available for

sale for the cost of goods sold section.

22. The income statement describes the revenues and expenses for the year. Included

in the calculation of the cost of goods sold is a line item identified as the cost of

23. Raw materials inventory turnover and days’ sales in raw materials inventory can be

used to assess raw materials inventory management. Raw materials inventory

24. Yes. Polaris can use the concepts and measures of cycle time and cycle efficiency

to evaluate performance on its product offerings.

25.

Inventory Components ($ millions)

Dell (February 3, 2012)

Production materials ………………………………………………..

$ 753

Work in process ……………………………………………..………..

239

Finished goods ……………………………………………………….

412

Total inventories …………………………………………….………..

$1,404

QUICK STUDIES

Quick Study 18-1 (5 minutes)

Quick Study 18-2 (10 minutes)

1. Managerial accounting

Quick Study 18-3 (5 minutes)

Quick Study 18-4 (5 minutes)

Quick Study 18-5 (5 minutes)

1. Indirect cost

Quick Study 18-6 (5 minutes)

Fundamental Accounting Principles, 21st Edition

1030

Quick Study 18-7 (10 minutes)

Finished goods inventory, December 31, 2012 ……………………..

$ 345,000

Plus cost of goods manufactured ………………………………………..

918,700

Cost of goods available for sale …………………………………………..

1,263,700

Less finished goods inventory, December 31, 2013 ……………...

283,600

Cost of goods sold ……………………………………………………………...

$ 980,100

Quick Study 18-8 (10 minutes)

Answer is 3.

Cost of goods sold is computed as:

Beginning finished goods inventory ………………………………………….

$ 500

Cost of goods manufactured ……………………………………………………..

4,000

Goods available for sale …………………………………………………………...

4,500

Ending finished goods inventory ……………………………………………….

750

Cost of goods sold …………………………………………………………………...

$3,750

Quick Study 18-9 (5 minutes)

Production activities

2

Sales activities

3

Materials activities

1

Quick Study 18-10 (15 minutes)

Briton Company

Manufacturing Statement

For Year Ended December 31, 2013

Direct materials ………………………………………………………………………….

$190,500

Direct labor ……………………………………………………………………………….

63,150

Factory overhead costs ……………………………………………………………...

24,000

Total manufacturing costs ………………………………………………………...

277,650

Add goods in process, December 31, 2012 ………………………………….

157,600

Total cost of goods in process …………………………..……………………….

435,250

Less goods in process, December 31, 2013 ………………………………...

142,750

Cost of goods manufactured ……………………………………………………...

$292,500

Quick Study 18-11 (10 minutes)

Quick Study 18-12 (5 minutes)

(Amounts in millions of Swiss francs)

Raw materials inventory, beginning …………………………………...

3,243

Plus raw materials purchased …………………………………………….

16,200

Raw materials available for use ………………………………………….

19,443

Less raw materials inventory, ending ………………………………….

3,904

Raw materials used …………………………………………………………...

15,539

Quick Study 18-13 (10 minutes)

(in millions of Swiss francs)

Cost of raw materials used** …………………………………………….

15,539

Beginning raw materials inventory ……………………………………

3,243

Ending raw materials inventory ………………………………………..

3,904

Total beginning plus ending raw materials inventory…………

7,147

Average raw materials inventory (Total / 2) ……………………….

3,574*

Inventory turnover (RM used** / Average inventory) ………….

4.35*

Days’ sales in inventory [(Ending inv./RM used*) x 365] ………..

91.7*

*Rounded

**Beginning RM + Purchased RM – RM used = Ending RM

3,243 + 16,200 – RM used = 3,904

15,539 = RM used

EXERCISES

Exercise 18-1 (15 minutes)

Financial Accounting

Managerial Accounting

1. Time

dimension

Historical information with

minimum predictions.

Many projections and estimates;

historical information also

presented.

2. Users and

decision

makers

Investors, creditors and

other users external to the

organization.

Managers, employees, and

decision makers internal to the

organization.

3. Timeliness of

information

Often available only after

the audit is complete.

Available quickly without the need

to wait for an audit.

4. Purpose of

information

Assist external users in

making investment, credit,

and other decisions.

Assist managers in making

planning and control decisions.

5. Nature of

information

Monetary information.

Mostly monetary; some

nonmonetary information.

6. Flexibility of

practice

Structured and often

controlled by GAAP.

Relatively flexible (no GAAP).

7. Focus of

information

Emphasis on whole

organization.

Emphasis on projects, processes,

and subdivisions of an

organization.

Exercise 18-2 (10 minutes)

1) Short-term planning usually covers a period of one year.

Exercise 18-3 (10 minutes)

Primary Information Source

Business Decision

Managerial

Financial

1. Determine amount of dividends to pay stockholders ...

X

X

2. Evaluate a purchasing department’s performance ….

X

3. Report financial performance to board of directors …...

X

X

4. Estimate product cost for new line of shoes …………..

X

5. Plan the budget for next quarter …………………………….

X

6. Measure profitability of all individual stores …………..

X

X

7. Prepare financial reports according to GAAP ………...

X

8. Determine location and size for a new plant …………..

X

Exercise 18-4 (15 minutes)

1. Five cost classifications are

(a)

Behavior

(c)

Controllability

(e)

Function

(b)

Traceability

(d)

Relevance

2. Two purposes of identifying these separate cost classifications:

(a) Cost classifications provide a standardized framework for using cost

accounting information by management.

(b) Cost classifications are useful in different types of management

analysis. For example, cost accounting is used to evaluate

Fundamental Accounting Principles, 21st Edition

1034

Exercise 18-5 (20 minutes)

1.

Cost by Behavior

Cost by Traceability

Product Cost

Variable

Fixed

Direct

Indirect

1. Leather cover for soccer balls ……..….

X

X

2. Annual flat fee paid for office

security …………………………………….….

X

X

3. Coolants for machinery………………..….

X

X

4. Wages of assembly workers ………..….

X

X

5. Lace to hold the leather together ….….

X

X

6. Taxes on factory …………………………..

X

X

7. Machinery depreciation ……………….….

X

X

2. Most fixed costs are indirect. Fixed costs normally are resources

acquired to support the production process rather than being traceable

to individual products or batches of product. However, not all indirect

costs are fixed. Some, like indirect materials, are variable.

Exercise 18-6 (20 minutes)

Product Cost

Period

Cost

Direct

Cost

Indirect

Cost

Prime

Conversion

Direct

Materials

Direct

Labor

Direct

Labor

Over-

head

1. Factory utilities

X

X

2. Advertising

X

3. Amortization of patents on

factory machine

X

X

4. State and federal income tax

X

5. Office supplies used

X

6. Bad debts expense

X

7. Small tools used

X

X

8. Payroll taxes for production

supervisor

X

X

9. Accident insurance on

factory workers*

X

X

X

10. Depreciation—Factory bldg

X

X

11. Wages to assembly

workers**

X

X

X

12. Direct materials used

X

X

* There are certain costs that can be classified as direct for one company and indirect

for another. The specific classification depends on the materiality and cost benefit of

Exercise 18-7 (20 minutes)

Part 1

Company 1, Sun Fresh Foods, is a merchandising firm with only one

inventory item, merchandise inventory. Company 2, Salomon Skis Mfg., is

a manufacturing company with three inventory categories (raw materials,

goods in process, and finished goods).

Part 2

Company 1

Sun Fresh Foods

Current Asset Section

December 31, 2013

Cash …………………………..……………………………………………………………………

$ 7,000

Accounts receivable …………………………………………………………………………

62,000

Merchandise inventory ……………………………………………………….….…………

45,000

Prepaid expenses ………………………………………………………………….…………

1,500

Total current assets ……………………………………………………………….…………

$115,500

Company 2

Salomon Skis Mfg.

Current Asset Section

December 31, 2013

Cash …………………………..……………………………………………………………………

$ 5,000

Accounts receivable …………………………………………………………………………

75,000

Raw materials inventory ………………………………………………………..…………

42,000

Goods in process inventory …………………………………………………..…..

30,000

Finished goods inventory ……………………………………………………….

50,000

Prepaid expenses ………………………………………………………………….…………

900

Total current assets ……………………………………………………………….…………

$202,900

Discussion: The current asset section of the balance sheet for these two

companies differs because one is a merchandiser and one is a

Exercise 18-8 (30 minutes)

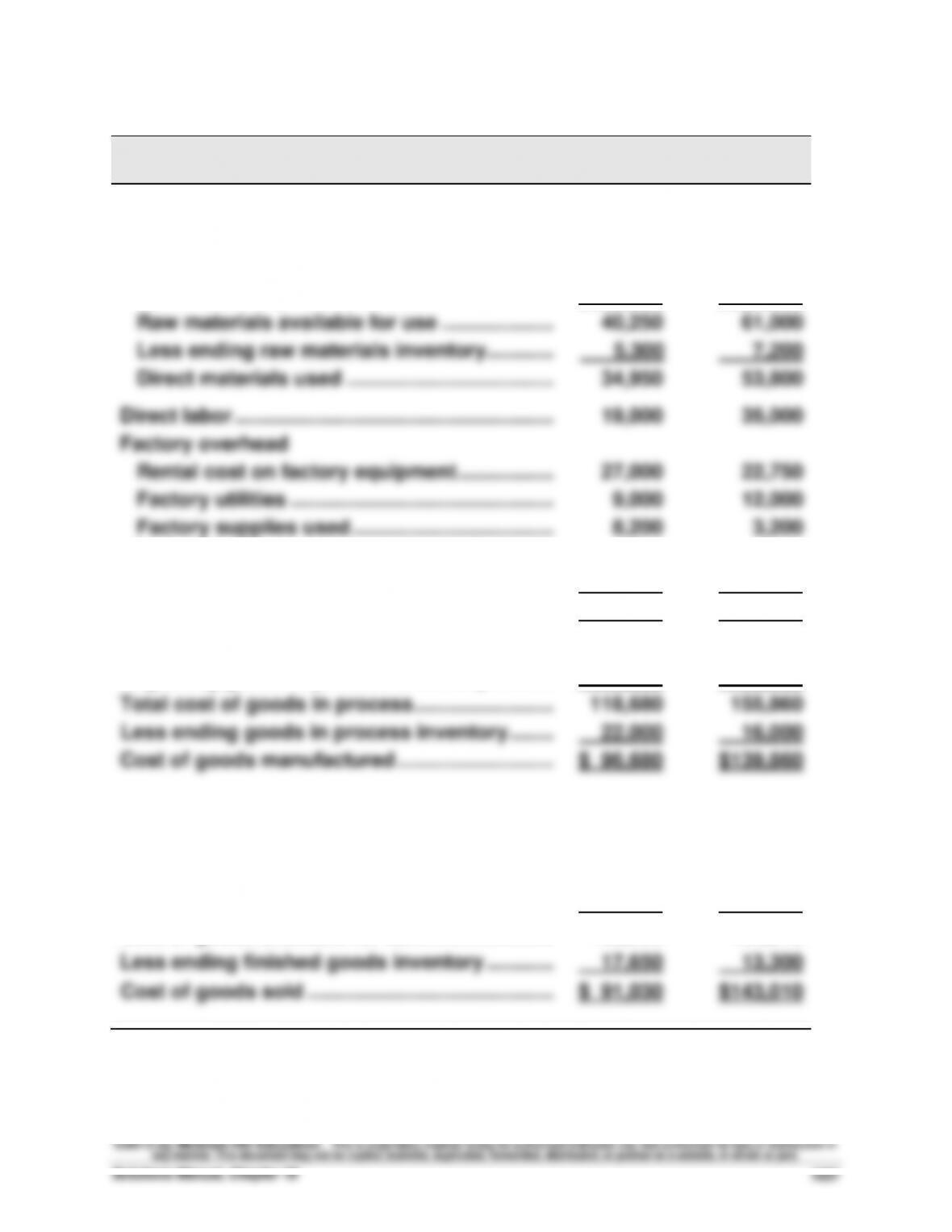

Garcia

Company

Culpepper

Company

1. COST OF GOODS MANUFACTURED

Direct materials

Beginning raw materials inventory ……………..

$ 7,250

$ 9,000

Raw materials purchases …………………………..

33,000

52,000

Raw materials available for use ………………....

40,250

61,000

Less ending raw materials inventory …………..

5,300

7,200

Direct materials used ………………………………...

34,950

53,800

Direct labor …………………………………………………..

19,000

35,000

Factory overhead

Rental cost on factory equipment ……………....

27,000

22,750

Factory utilities ………………………………………....

9,000

12,000

Factory supplies used ………………………………..

8,200

3,200

Indirect labor ……………………………………………..

1,250

7,660

Repairs—Factory equipment ……………………...

4,780

1,500

Total factory overhead ……………………………....

50,230

47,110

Total manufacturing costs …………………………..

104,180

135,910

Beginning goods in process inventory ………....

14,500

19,950

Total cost of goods in process ……………………...

118,680

155,860

Less ending goods in process inventory ……....

22,000

16,000

Cost of goods manufactured ………………………...

$ 96,680

$139,860

2. COST OF GOODS SOLD

Beginning finished goods inventory ……………..

$ 12,000

$ 16,450

Cost of goods manufactured ………………………...

96,680

139,860

Cost of goods available for sale …………………....

108,680

156,310

Less ending finished goods inventory …………..

17,650

13,300

Cost of goods sold ……………………………………....

$ 91,030

$143,010

Exercise 18-9 (20 minutes)

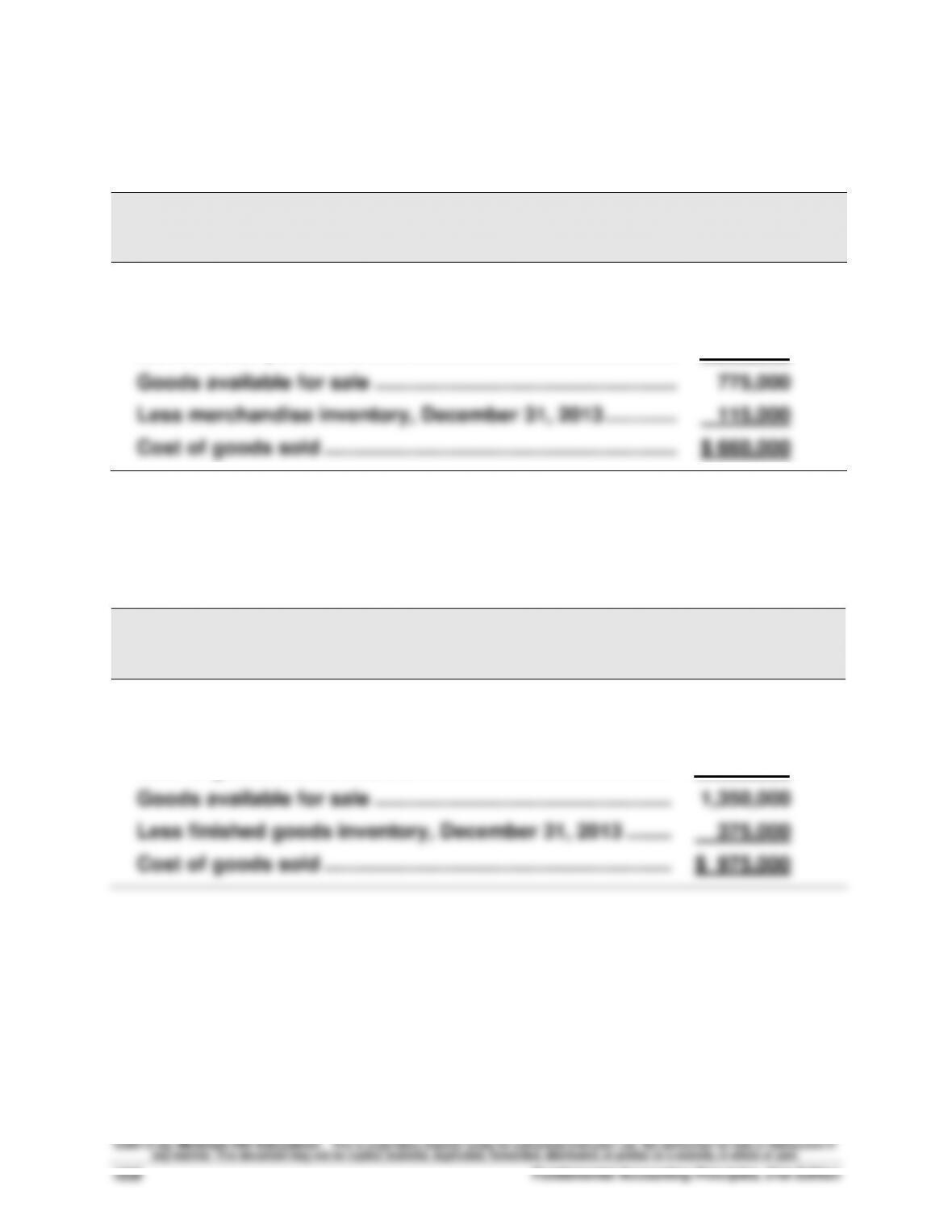

Merchandising Business

VIKING RETAIL

Partial Income Statement

For Year Ended December 31, 2013

Cost of goods sold

Merchandise inventory, December 31, 2012 …………………..…..

$ 275,000

Merchandise purchases ………………………………………………..…..

500,000

Goods available for sale ……………………………………………….…..

775,000

Less merchandise inventory, December 31, 2013 …………..…..

115,000

Cost of goods sold ……………………………………………………….

$ 660,000

Manufacturing Business

LOG HOMES MANUFACTURING

Partial Income Statement

For Year Ended December 31, 2013

Cost of goods sold

Finished goods inventory, December 31, 2012……………..…

$ 450,000

Cost of goods manufactured ……………………………………….…

900,000

Goods available for sale ……………………………………………..…

1,350,000

Less finished goods inventory, December 31, 2013 ……..…

375,000

Cost of goods sold ……………………………………………………....

$ 975,000

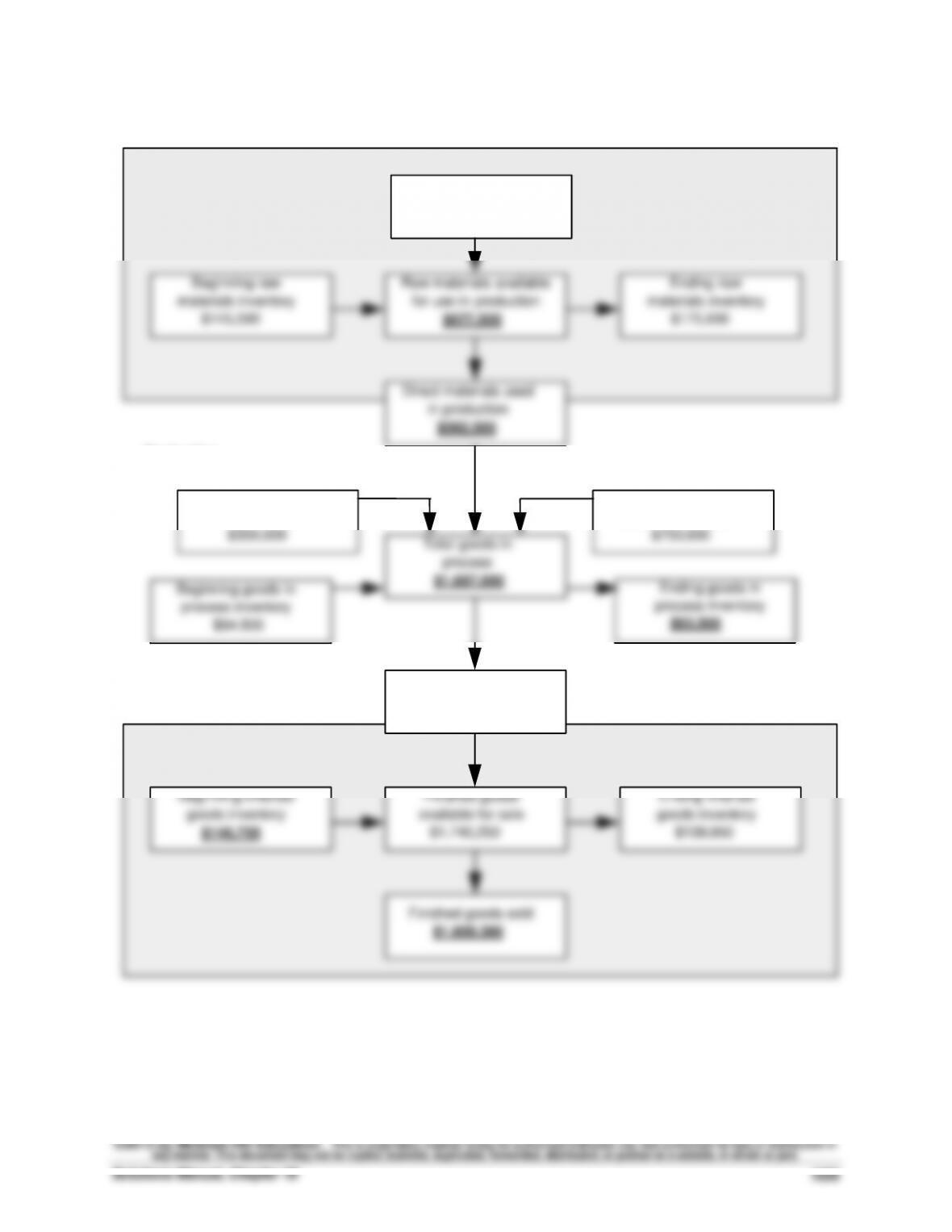

Exercise 18-10 (15 minutes)

Direct materials used

in production

$502,500

Factory overhead

used in production

$750,000

Ending raw

materials inventory

$175,000

Beginning raw

materials inventory

$145,500

Raw materials available

for use in production

$677,500

Raw materials

purchases

$532,000

Production

Activity

Sales

Activity

Materials

Activity

Direct labor used

in production

$350,000

Ending goods in

process inventory

$93,500

Total goods in

process

$1,687,000

Beginning goods in

process inventory

$84,500

Ending finished

goods inventory

$139,950

Finished goods sold

$1,600,300

Beginning finished

goods inventory

$146,750

Finished goods

available for sale

$1,740,250

Finished goods

manufactured

$1,593,500