Fundamental Accounting Principles, 21st Edition

1040

Exercise 18-11 (25 minutes)

Account

Balance

Sheet

Income

Statement

Manufacturing

Statement

Overhead

Report

Accounts receivable ……………………....

✓

Computer supplies used in office …....

✓

Beginning finished goods inventory

✓

Beginning goods in process

inventory ……………………………………..

✓

Beginning raw materials inventory …..

✓

Cash ……………………………………………...

✓

Depreciation expense—Factory

building………………………………………..

✓

Depreciation expense—Factory

equipment …………………………………...

✓

Depreciation expense—Office

building………………………………………..

✓

Depreciation expense—Office

equipment …………………………………...

✓

Direct labor …………………………………....

✓

Ending finished goods inventory ……..

✓

✓

Ending goods in process inventory....

✓

✓

Ending raw materials inventory ……....

✓

✓

Factory maintenance wages …………....

✓

Computer supplies used in factory ....

✓

Income taxes …………………………………..

✓

Insurance on factory building ………....

✓

Rent cost on office building …………....

✓

Office supplies used ……………………....

✓

Property taxes on factory building …..

✓

Raw materials purchases ………………..

✓

Sales ……………………………………………...

✓

Exercise 18-12 (25 minutes)

SHANTA COMPANY

Manufacturing Statement

For Year Ended December 31, 2013

Direct materials

Raw materials inventory, December 31, 2012 ………………..

$ 37,000

Raw materials purchases ……………………………………..……..

175,600

Raw materials available for use …………………………………..

212,600

Less raw materials inventory, December 31, 2013 ….……..

42,700

Direct materials used …………………………………………..……..

$169,900

Direct labor ……………………………………………………………..……..

225,000

Factory overhead

Factory computer supplies used …………………………..

17,840

Indirect labor ………………………………………………………..……..

47,000

Repairs—Factory equipment ………………………………………..

5,250

Rent cost of factory building ………………………………………..

57,000

Total factory overhead costs ………………………………..……..

127,090

Total manufacturing costs ……………………………………………..

521,990

Goods in process inventory, December 31, 2012 ……………..

53,900

Total cost of goods in process ………………………………..……..

575,890

Less goods in process inventory, December 31, 2013 ………..

41,500

Cost of goods manufactured …………………………………………..

$534,390

Exercise 18-13 (20 minutes)

SHANTA COMPANY

Income Statement

For Year Ended December 31, 2013

Sales ……………………………………………………………………….……..

$1,250,000

Cost of goods sold

Finished goods inventory, December 31, 2012……….……..

$ 62,750

Cost of goods manufactured ………………………………………..

534,390

Cost of goods available for sale …………………………….……..

597,140

Less finished goods inventory, December 31, 2013 …..……..

67,300

Cost of goods sold ……………………………………………….……..

529,840

Gross profit ……………………………………………………….…………..

720,160

Operating expenses

Advertising expense ……………………………………………..……..

94,000

General and administrative expenses …………………………..

129,300

Total operating expenses ……………………………………..……..

223,300

Operating income ……………………………………………………….

$ 496,860

Exercise 18-14 (10 minutes)

Exercise 18-15 (10 minutes)

b. If customers rate any of the factors on the survey as anything other than

“very satisfied,” managers should investigate the reasons for the

Exercise 18-16 (20 minutes)

Cost by Behavior

Cost by Traceability

Cost

Variable

Fixed

Direct

Indirect

1. Advertising ………………………………….….

X

X

2. Beverages and snacks …………………….

X

X

3. Regional VP salary ………………………….

X

X

4. Depreciation on ground equip. …….….

X

X

5. Fuel and oil used in planes …………..….

X

X

6. Flight attendant salaries ………………….

X

X

7. Pilot salaries ………………………………..….

X

X

8. Ground crew wages ……………………..….

X

X

9. Travel agent salaries ……………………….

X

X

Fundamental Accounting Principles, 21st Edition

1044

PROBLEM SET A

Problem 18-1A (20 minutes)

The managerial accounting professional must do more than assign value to

ending inventory and cost of goods sold. S/he must understand the

industry and the current business environment of the company. The

Problem 18-2A (60 minutes)

Instructor note: There can be more than one right answer to this problem. Students can

experience some challenges in completing this assignment. Their reaction is normal and a part of

the process in learning how difficult it is to make estimates of opportunity costs.

A good answer to this problem should show estimates for:

A good answer would also show that purchasing a lower-quality product at

a lower cost will result, under the conditions specified in this case, in

losing money in the long-run. Specifically, the answer should appear

similar to the following:

Fundamental Accounting Principles, 21st Edition

1046

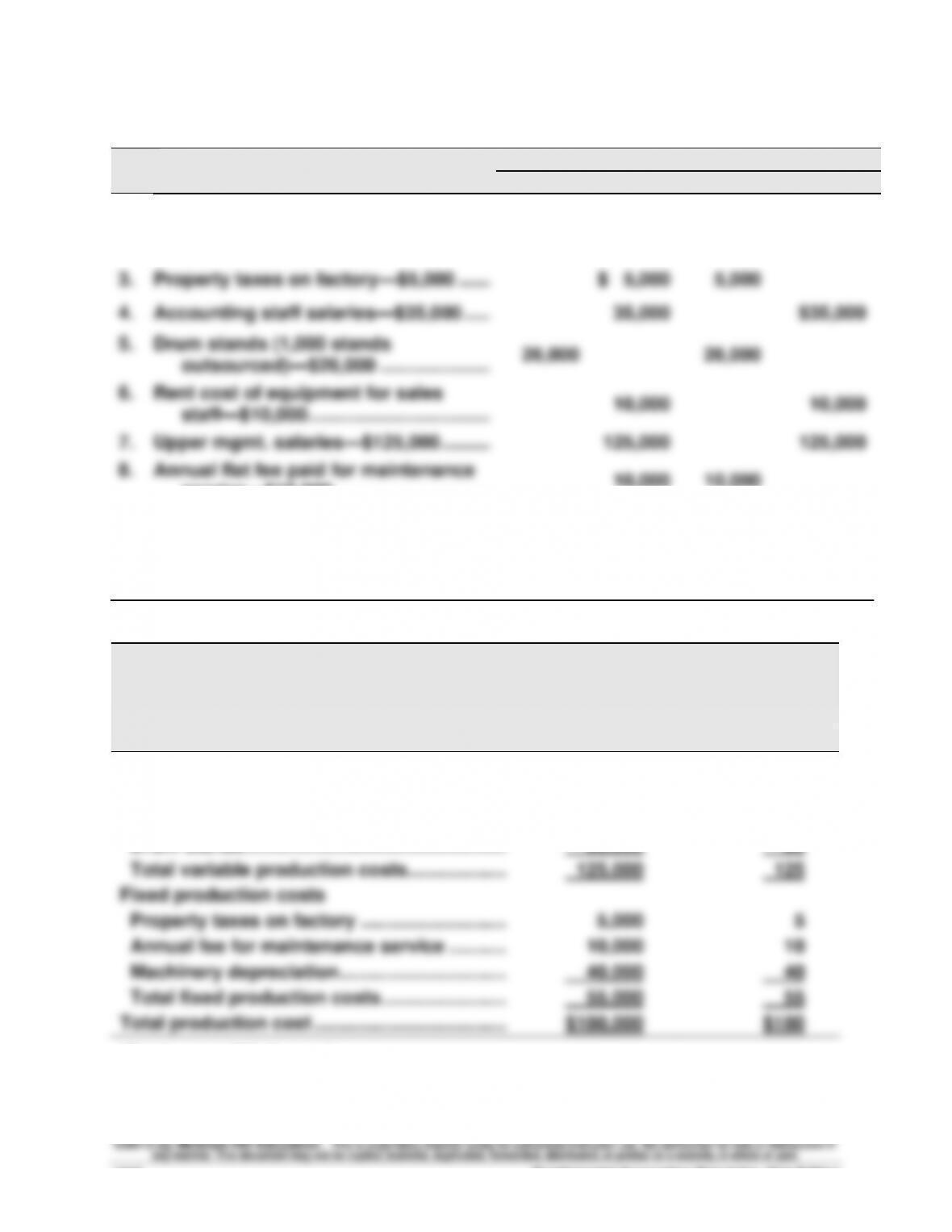

Problem 18-3A (45 minutes)

Part 1 Cost classification and amounts

Cost by Behavior

Cost by Function

Costs

Variable

Fixed

Product

Period

1.

Plastic for casing—$17,000 ……………...

$17,000

$17,000

2.

Wages of assembly workers—$82,000 …

82,000

82,000

3.

Property taxes on factory—$5,000 …….

$ 5,000

5,000

4.

Accounting staff salaries—$35,000 …...

35,000

$35,000

5.

Drum stands (1,000 stands

outsourced)—$26,000 ………………...

26,000

26,000

6.

Rent cost of equipment for sales

staff—$10,000 …………………………….

10,000

10,000

7.

Upper mgmt. salaries—$125,000 ……….

125,000

125,000

8.

Annual flat fee paid for maintenance

service—$10,000 ………………………..

10,000

10,000

9.

Sales commissions—$15 per unit ……..

$15 x units

sold

$15 x units

sold

10.

Machinery depreciation, straight-

line—$40,000 ……………………………..

40,000

40,000

Part 2

DrumBeat

Calculation of Manufacturing Cost per Drum Set

For Year Ended December 31, 2013

Item

Total cost

(at 1,000 units)

Per unit cost*

Variable production costs

Plastic for casing ……………………………………

$ 17,000

$ 17

Wages of assembly workers ……………………

82,000

82

Drum stands …………………………………………..

26,000

26

Total variable production costs……………….

125,000

125

Fixed production costs

Property taxes on factory ……………………….

5,000

5

Annual fee for maintenance service ………..

10,000

10

Machinery depreciation …………………………..

40,000

40

Total fixed production costs ……………………

55,000

55

Total production cost ……………………………….

$180,000

$180

*Total cost / 1,000 drum sets

Problem 18-3A (continued)

Part 3

If 1,200 drum sets are produced, we would expect the cost of the plastic for

Part 4

If 1,200 drum sets are produced, we would expect the cost of the property

Problem 18-4A (30 minutes)

MEMORANDUM

TO:

FROM:

DATE:

SUBJECT:

The memorandum content should include the following points:

Product and period costs are different. Product costs are defined as

direct material, direct labor, and factory overhead. Moreover, product

costs are capitalized and expensed as goods are sold. All other costs,

such as administrative and selling expenses, are reported and expensed

in the period incurred and are called period costs. Period costs are the

types of expenses usually identified as operating expenses.

Product costs can be further understood by thinking about what takes

place in the production process. Direct material and direct labor are

primary components to the production process, thus these costs are

labeled prime costs. Direct labor and factory overhead are key resources

merchandising business does not have to be concerned with prime and

conversion costs. Purchases are the only product cost category for a

merchandiser.

Problem 18-5A (40 minutes)

Part 1

Units and dollar amounts of raw materials inventory in heels

Beginning inventory, December 31, 2012 (1,200 units x $8) …..….

$ 9,600

Purchases during 2013 (35,000 units x $8) ……………………………….

280,000

Inventory available for production ………………………………………….

289,600

Ending inventory, December 31, 2013

([1,200 + 35,000 – 33,200*] units x $8) ………………………………..….

24,000

Inventory transferred into production …………………………………..….

$265,600

**

*Note: 16,600 pairs of boots manufactured require 33,200 heels.

** (33,200 heels x $8)

Part 2 Analysis Component

Topics of discussion for this memorandum include:

• Description (general) of the JIT inventory system and how it operates.

• Cutting the heel inventory in half would free up $12,000 of working

capital (3,000 units x ½ x $8 cost).

Fundamental Accounting Principles, 21st Edition

Problem 18-6A (40 minutes)

Part 1

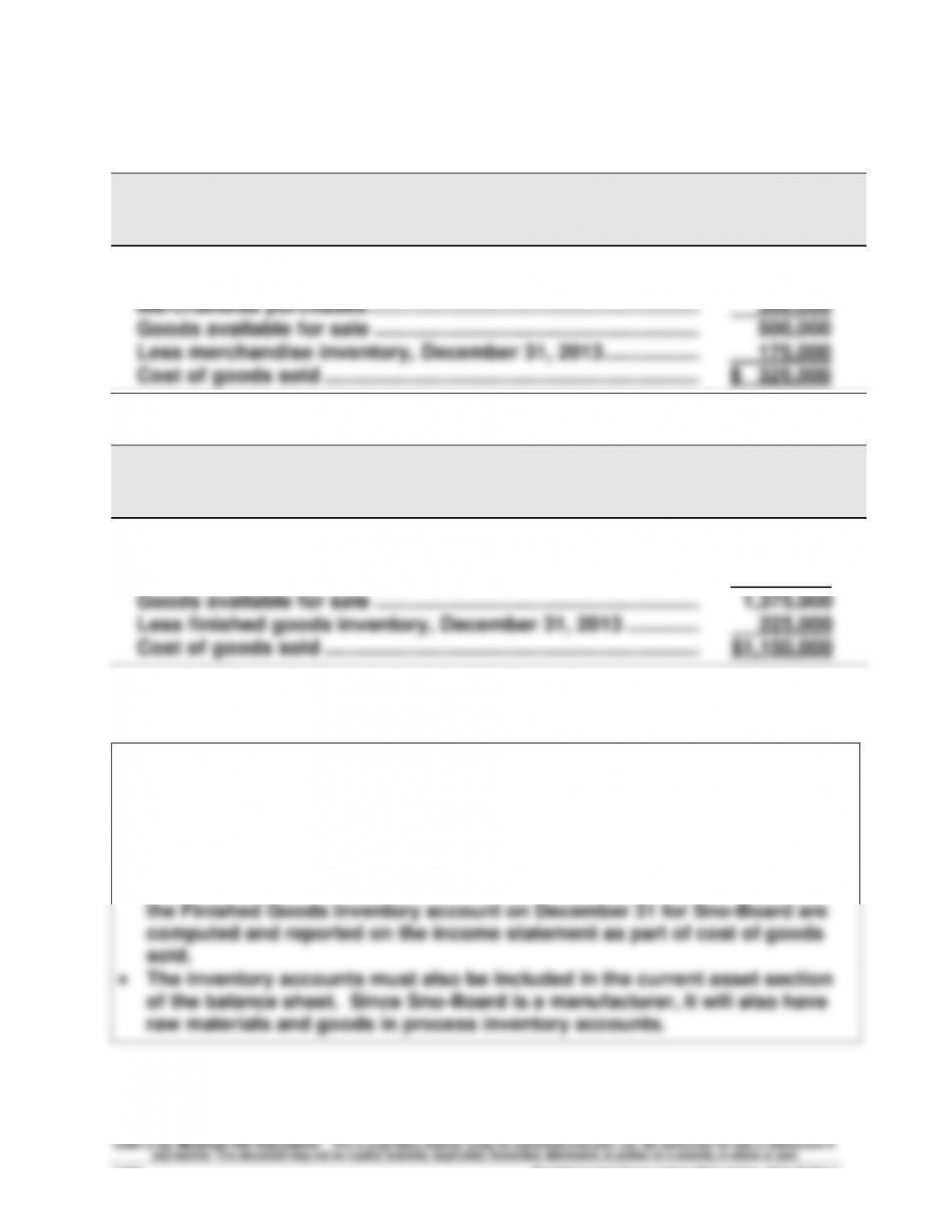

MERCHANDISING BUSINESS

SPORTS WORLD RETAIL

Partial Income Statement

For Year Ended December 31, 2013

Cost of goods sold

Merchandise inventory, December 31, 2012 ……………………..……

$ 200,000

Merchandise purchases …………………………………………………..…..

300,000

Goods available for sale ………………………………………………….……

500,000

Less merchandise inventory, December 31, 2013 ……………..……

175,000

Cost of goods sold ………………………………………………………….……

$ 325,000

MANUFACTURING BUSINESS

SNO–BOARD MFG.

Partial Income Statement

For Year Ended December 31, 2013

Cost of goods sold

Finished goods inventory, December 31, 2012………………….……

$ 500,000

Cost of goods manufactured …………………………………………………

875,000

Goods available for sale ………………………………………………….……

1,375,000

Less finished goods inventory, December 31, 2013 ………….……

225,000

Cost of goods sold ………………………………………………………….……

$1,150,000

Part 2

MEMORANDUM

TO:

FROM:

DATE:

SUBJECT:

The answers will vary but should include:

• The Merchandise Inventory account on December 31 for Sports World and

the Finished Goods Inventory account on December 31 for Sno-Board are

computed and reported on the income statement as part of cost of goods

sold.

• The inventory accounts must also be included in the current asset section

of the balance sheet. Since Sno-Board is a manufacturer, it will also have

raw materials and goods in process inventory accounts.

Problem 18-7A (75 minutes)

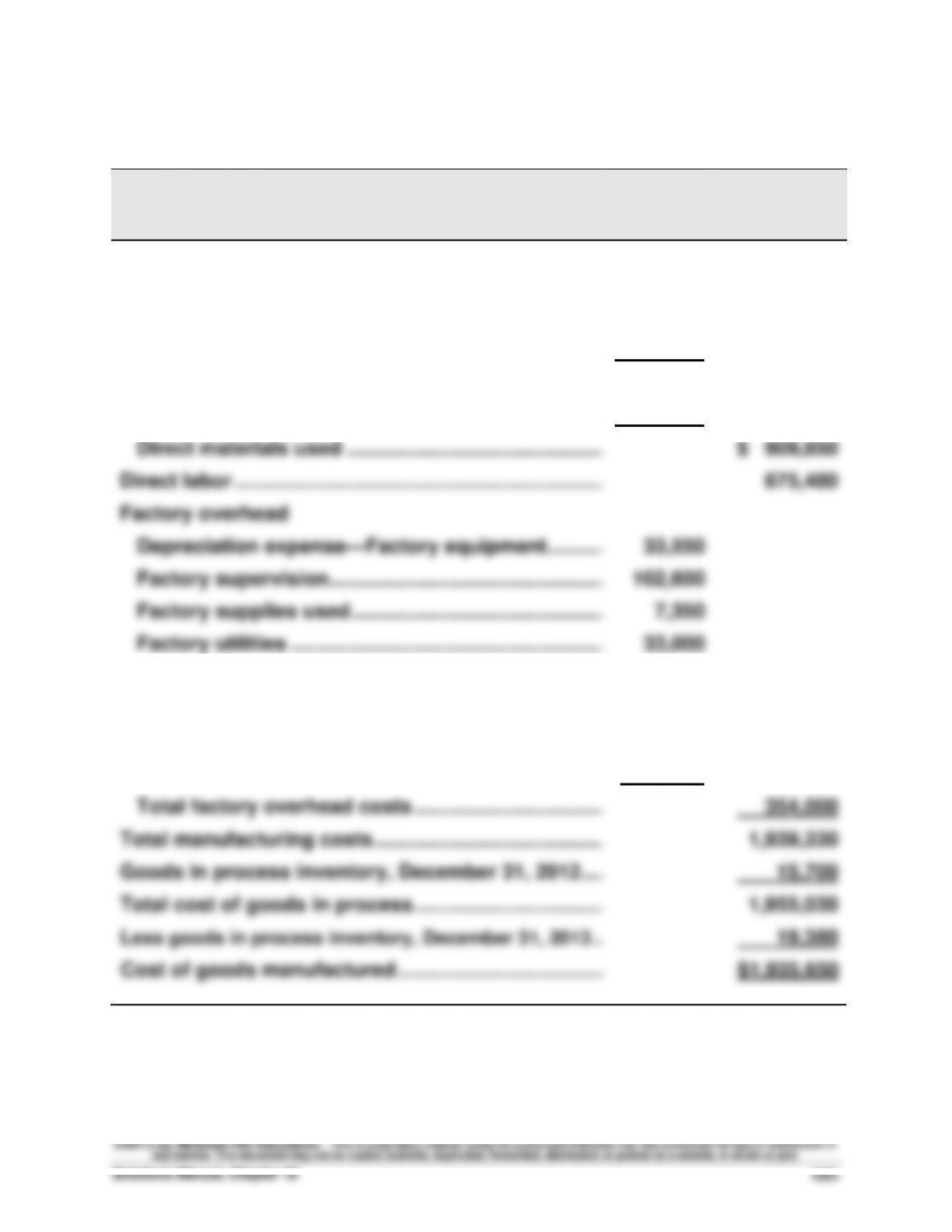

Part 1

DE LEON COMPANY

Manufacturing Statement

For Year Ended December 31, 2013

Direct materials

Raw materials inventory, December 31, 2012 …….…

$

166,850

Raw materials purchases ………………………………….…

925,000

Raw materials available for use ………………………..…

1,091,850

Less raw materials inventory, December 31, 2013 ..…

182,000

Direct materials used ……………………………………….…

$ 909,850

Direct labor ……………………………………………………………

675,480

Factory overhead

Depreciation expense—Factory equipment ……….…

33,550

Factory supervision ………………………………………….…

102,600

Factory supplies used …………………………………………

7,350

Factory utilities ………………………………………………..…

33,000

Indirect labor ………………………………………………………

56,875

Miscellaneous production costs ……………………….…

8,425

Rent expense—Factory building ……………………….…

76,800

Maintenance expense—Factory equipment ……….…

35,400

Total factory overhead costs …………………………….…

354,000

Total manufacturing costs …………………………………..…

1,939,330

Goods in process inventory, December 31, 2012 ….…

15,700

Total cost of goods in process …………………………….…

1,955,030

Less goods in process inventory, December 31, 2013 ..…

19,380

Cost of goods manufactured …………………………..…..…

$1,935,650

Fundamental Accounting Principles, 21st Edition

1052

Problem 18-7A (Continued)

Part 2

DE LEON COMPANY

Income Statement

For Year Ended December 31, 2013

Sales …………………………………………………………………..…

$4,525,000

Less sales discounts …………………………………………..…

62,500

Net sales …………………………………………………………….…

4,462,500

Cost of goods sold

Finished goods inventory, December 31, 2012………

$

167,350

Cost of goods manufactured ……………………………..…

1,935,650

Goods available for sale ………………………………………

2,103,000

Less finished goods inventory, December 31, 2013 ….…

136,490

Cost of goods sold ………………………………………………

1,966,510

Gross profit from sales ……………………………………….…

2,495,990

Operating expenses

Selling expenses

Advertising expense ………………………………………..…

28,750

Depreciation expense—Selling equipment ……….…

8,600

Rent expense—Selling space …………………………..

26,100

Sales salaries expense …………………………………….…

392,560

Total selling expenses …………………………………….…

456,010

General and administrative expenses

Depreciation expense—Office equipment ……………

7,250

Office salaries expense ………………………………………

63,000

Rent expense—Office space ………………………………

22,000

Total general and administrative expenses …………

92,250

Total operating expenses ………………………………….…

548,260

Income before state and federal taxes ……………………

1,947,730

Income taxes expense ……………………………………………

233,725

Net income ……………………………………………………………

$1,714,005

Problem 18-7A (Continued)

Part 3

Raw

Materials

Finished

Goods

Cost of raw materials used ……………………………………………..

$909,850

Cost of finished goods sold …………………………………….……..

$1,966,510

Beginning inventory ………………………………………………..……..

$166,850

$ 167,350

Ending inventory……………………………………………………....

182,000

136,490

Total beginning plus ending inventory ……………………..……

$348,850

$ 303,840

Average inventory (Total / 2) …………………………………………..

$174,425

$ 151,920

Inventory turnover (COGS* / Average inventory) ……………..

5.2

12.9

Days’ sales in inventory [(Ending inv./COGS*) x 365] .……..

73.0

25.3

* To calculate the turnover and days’ sales in inventory for raw materials, use raw materials used

rather than cost of goods sold.

Discussion: The inventory turnover ratio for the raw materials inventory is

significantly lower than the turnover ratio for finished goods.

One reason for the difference could be that source of supply for raw materials

is relatively undependable, so that management believes it is necessary to

carry a larger inventory to sustain operations through periods when the

sales by not having enough product on hand.

Similar inferences are drawn from the days’ sales in inventory ratio results. In

Problem 18-8A (10 minutes)