Title: Problem 13-3A

QA_Ori:

Part 1

Explanations for each of the journal entries

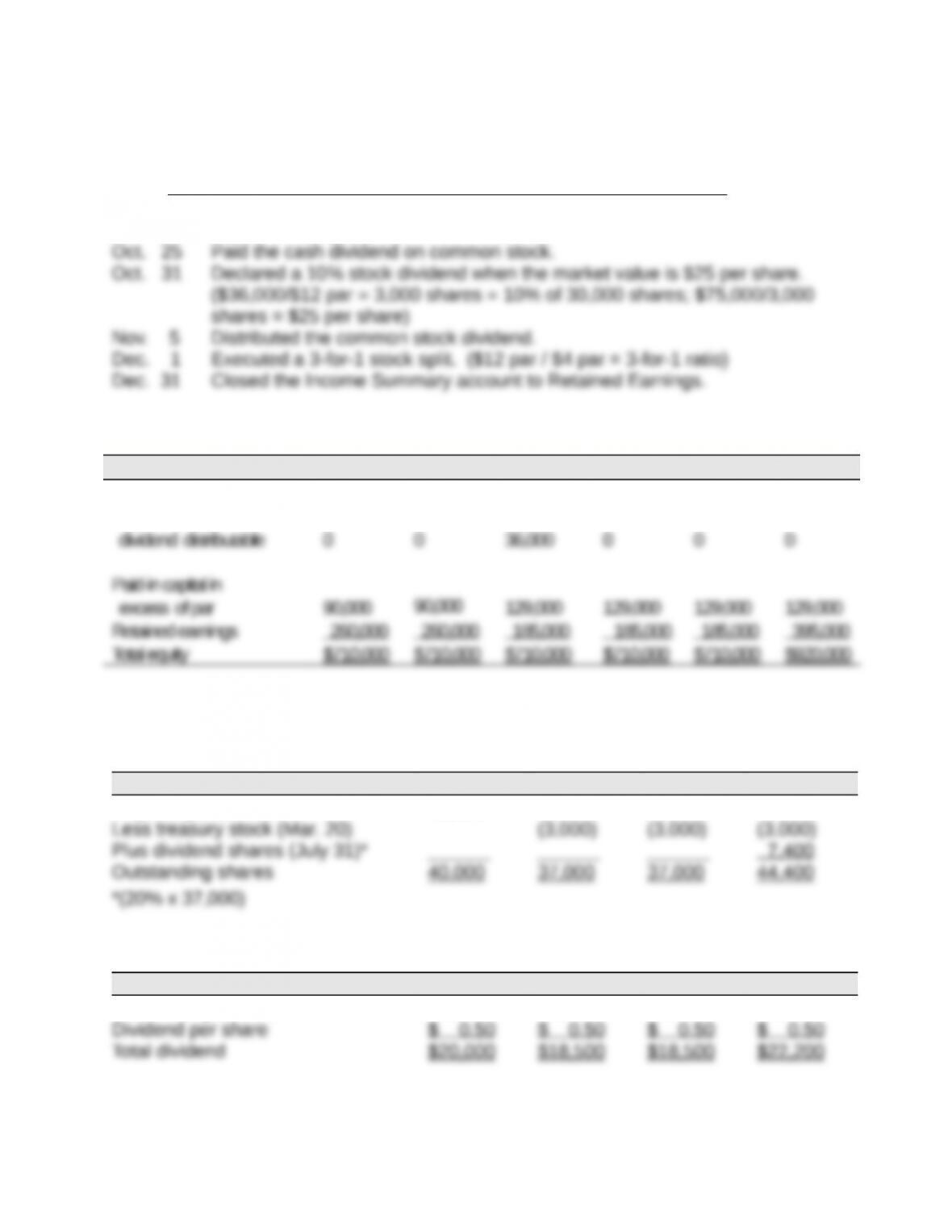

Oct. 2 Declared a cash dividend of $2 per share of common stock. ($60,000 /

30,000 shares)

Part 2

Oct. 2 Oct. 25 Oct. 31 Nov. 5 Dec. 1 Dec. 31

Common stock $360,000 $360,000 $360,000 $396,000 $396,000 $396,000

Common stock

Title: Problem 13-4A

QA_Ori:

Part 1

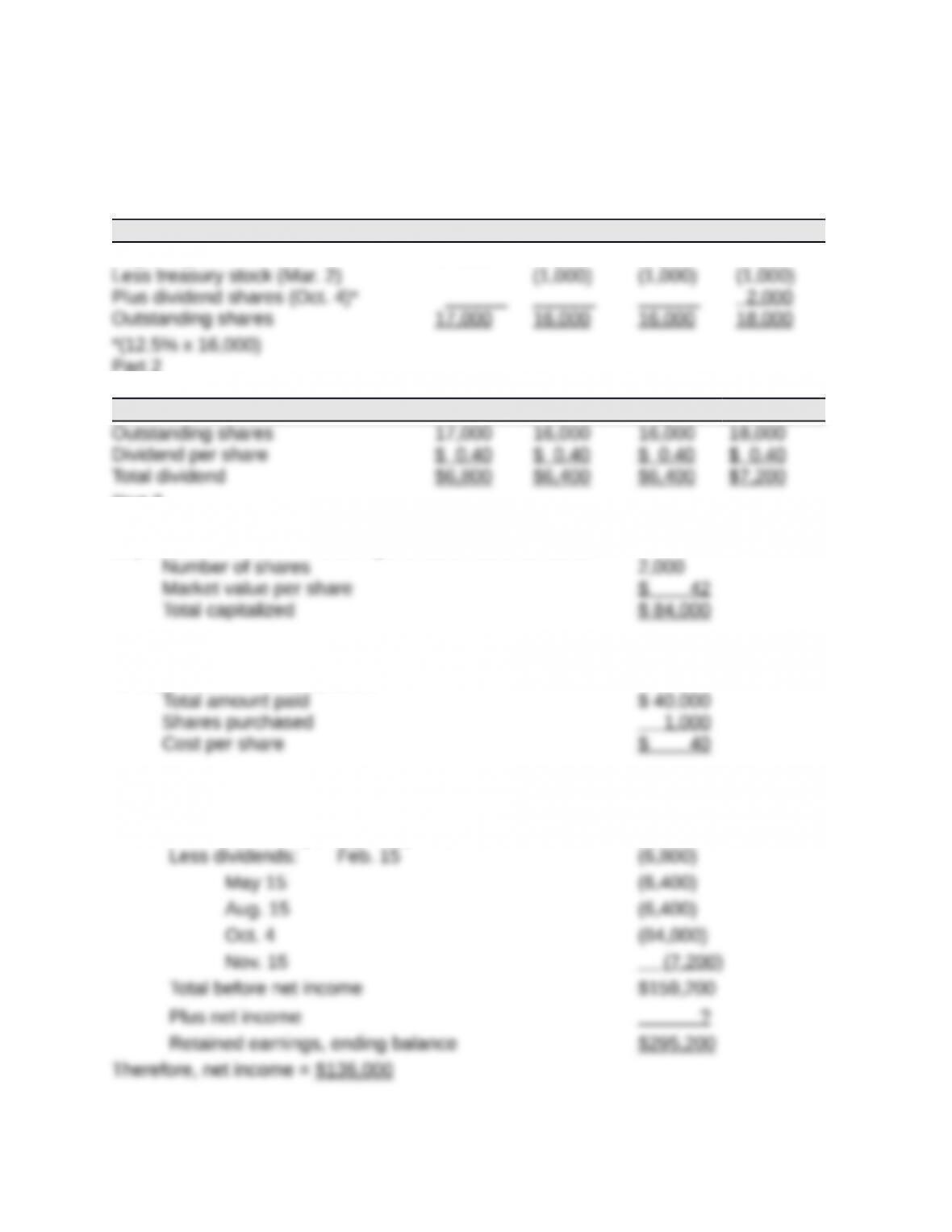

Outstanding common shares

Jan. 5 Apr. 5 July 5 Oct. 5

Beginning balance 40,000 40,000 40,000 40,000

Part 2

Cash dividend amounts

Jan. 5 Apr. 5 July 5 Oct. 5

Outstanding shares 40,000 37,000 37,000 44,400

Part 3

QA_Ori:

Capitalization of retained earnings for small stock dividend

Part 4

Cost per share of treasury stock

Part 5

Net income

Retained earnings, beginning balance $320,000

Less dividends: Jan. 5 (20,000)

Title: Problem 13-5A

QA_Ori:

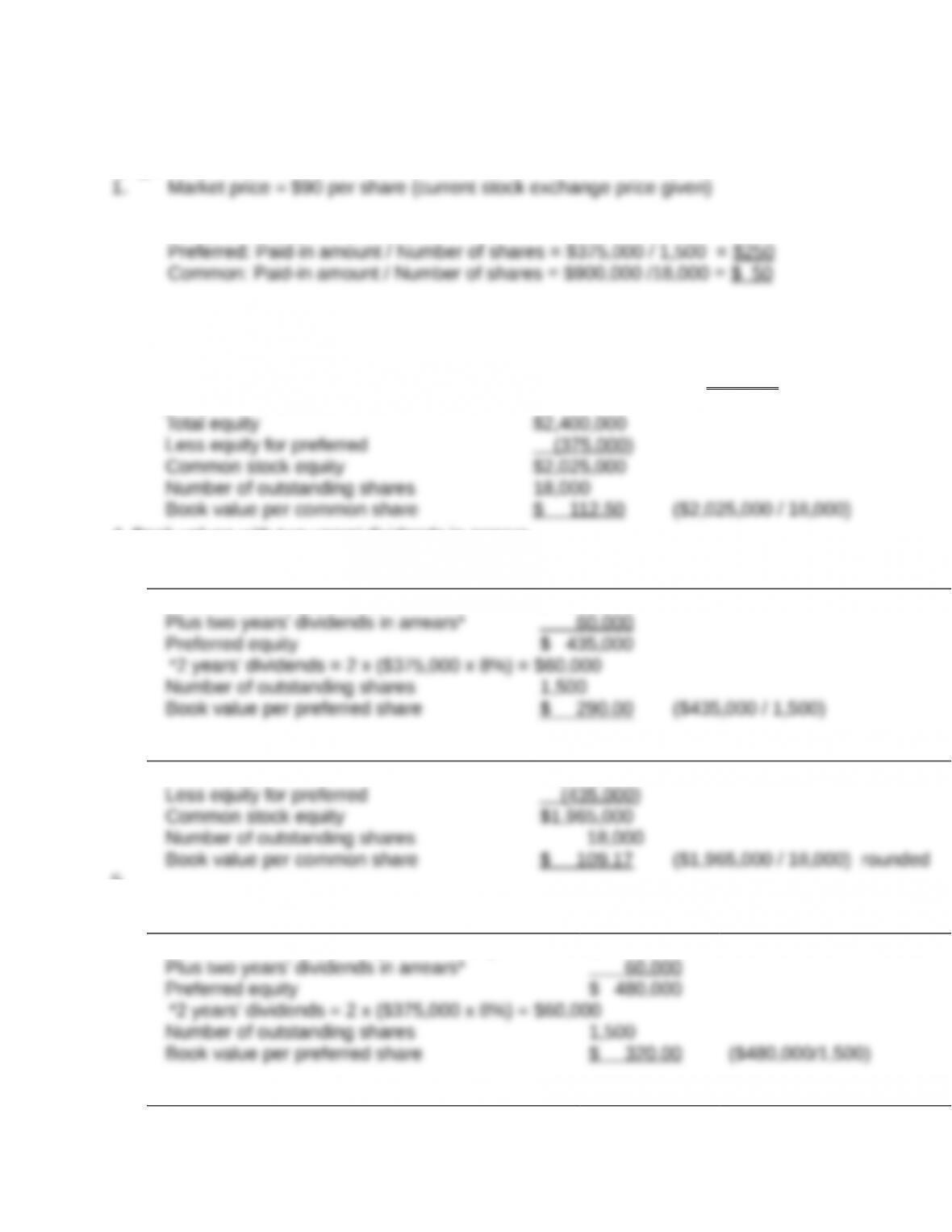

1. Market price = $85 per share (current stock exchange price given)

2. Computation of par values of stock

3. Book values with no dividends in arrears

Book value per preferred share = par value (when not callable) = $50

4. Book values with two years’ dividends in arrears

Preferred stock

shares)

Common stock

Total equity $280,000

shares)

5. Book values with call price and two years’ dividends in arrears

Preferred stock

Common stock

Total equity $280,000

sh.)

6. Dividend allocation in total

Preferred Common Total

2 years’ dividends in arrears $ 5,000 $ 0 $ 5,000

$4,000 / 4,000 shares = $1.00

7. Equity represents the residual interest of owners in the assets of the business

Title: Problem 13-1B

QA_Ori:

Part 1

a. To record sale of 3,000 ($3,000/$1 per share) shares of $1 par value common

b. To record issuance of 1,000 ($1,000/$1 per share) shares of $1 par value

c. To record acquisition of assets and liabilities by issuing 800 ($800/$1 per share)

Part 2

Number of outstanding shares

Issued in (a) 3,000

Part 3

Minimum legal capital = Outstanding shares x Par value per share

Part 4

Total paid-in capital from common stockholders

From transaction (a) $120,000

Part 5

Book value per common share

Title: Problem 13-2B

QA_Ori:

Part 1

Jan. 10 Treasury Stock, Common 480,000

Mar. 2 Retained Earnings 240,000

Mar. 31 Common Dividend Payable 240,000

Nov. 11 Cash* 312,000

Treasury Stock, Common** 288,000

Nov. 25 Cash* 152,000

Paid-In Capital, Treasury Stock 24,000

Dec. 1 Retained Earnings 500,000

Dec. 31 Income Summary 1,072,000

Part 2

BALTHUS CORP.

Statement of Retained Earnings

For Year Ended December 31, 2014

Retained earnings, December 31, 2013 $2,160,000

Part 3

BALTHUS CORP.

Stockholders’ Equity Section of the Balance Sheet

December 31, 2014

Common stock$1 par value, 320,000 shares

Title: Problem 13-3B

QA_Ori:

Part 1

Explanations for each of the journal entries

Jan. 17 Declared a cash dividend of $1 per share of common stock. ($96,000 /

96,000 shares)

Feb. 5 Paid the cash dividend on common stock.

Part 2

Jan. 17 Feb. 5 Feb. 28 Mar. 14 Mar. 25 Mar. 31

Common stock $

960,000

$ 960,000 $ 960,000 $1,080,000 $1,080,000 $1,080,000

0

Title: Problem 13-4B

QA_Ori:

Part 1

Outstanding common shares

Feb. 15 May 15 Aug. 15 Nov. 15

Beginning balance 17,000 17,000 17,000 17,000

Part 2

Cash dividend amounts

Feb. 15 May 15 Aug. 15 Nov. 15

Part 3

Capitalization of retained earnings for small stock dividend

Part 4

Cost per share of treasury stock

Part 5

Net income

Retained earnings, beginning balance $270,000

Title: Problem 13-5B

QA_Ori:

2. Computation of stock par values

3.

Book values with no dividends in arrears

Book value per preferred share = par value (when not callable) = $ 250

Common stock

4. Book values with two years’ dividends in arrears

Preferred stock

Preferred stock par value $ 375,000

Common stock

Total equity $2,400,000

5.

Book values with call price and two years’ dividends in arrears

Preferred stock

Preferred stock call price (1,500 x $280) $ 420,000

Common stock

Total equity $2,400,000

6.

Dividend allocation in total

Preferred Common Total

2 years’ dividends in arrears $ 60,000 $ 0 $ 60,000

Dividends per share for the common stock

7. Equity represents the residual interest of owners in the assets of the business after

subtracting claims of creditors. With few exceptions, these assets and liabilities are