Chapter 25

Capital Budgeting and Managerial

Decisions

QUESTIONS

1. Capital budgeting decisions require careful analysis because they are generally

the most difficult and risky decisions that management faces.

2. Capital budgeting is the process of planning the acquisition or sale of plant

assets.

3. Capital budgeting decisions are risky because: (1) the outcomes are uncertain,

4. The payback period ignores both the present value of cash flows and all cash

flows after the payback period.

5. A shorter payback period is desirable because management prefers to reduce

the risk that the investment might not be profitable over the long run. As a result

6. If net income is earned evenly throughout each year and straight-line

7. When the present value of expected net cash flows, discounted at 10%, exceeds

the amount invested it indicates that the expected rate of return on the

Fundamental Accounting Principles, 21st Edition

1464

8. Receiving $100 one year from today is worth less than $100 today because a

0.8929 = $89.29 (the present value factor is taken from Table B.1). This means

9. The return on an investment must cover the interest and provide an additional

profit to reward the company for risk. For example, if money can be borrowed at

companies with average risk projects.

10. Accelerated depreciation produces larger tax deductions and lower tax

payments in the early years of an asset’s life compared with straight-line

11. An out-of-pocket cost requires a current outlay of cash. An opportunity cost is

12. Sunk costs are irrelevant because they remain the same whether the product is

sold in its present condition or processed further.

13. There are virtually no incremental costs associated with shipping the additional

iPod. The company’s employees would not receive any additional compensation

14. KTM management could use one of the following common methods to evaluate

15. The company might be willing to sell the units internationally if (a) the company

has excess capacity, (b) the incremental costs of manufacturing and selling the

QUICK STUDIES

Quick Study 25-1 (10 minutes)

Quick Study 25-2 (10 minutes)

1. If all else is equal, Investment A would be preferred over Investment B

because of A’s shorter payback period.

2. However, if the investments are different, then there are at least four

reasons why Investment B might be preferred over Investment A:

Quick Study 25-3 (10 minutes)

Quick Study 25-4 (15 minutes)

Net present value of investment*

Present value of seven $10,000 cash inflows (10,000 x 4.8684) ……..……

$48,684

Present value of $6,000 at end of seven years (6,000 x 0.5132) ……..……

3,079

Present value of cash inflows ……………………………………………………….

51,763

Less immediate cash outflow ……………………………………………………….

50,000

Net present value ………………………………………………………………………..……

$ 1,763

*Present value factors from tables at the end of Appendix B:

4.8684 = Present value of an annuity of 1, where n = 7, i = 10% (from Table B.3)

0.5132 = Present value of 1, where n = 7, i = 10% (from Table B.1)

Fundamental Accounting Principles, 21st Edition

1466

Quick Study 25-5 (10 minutes)

Project A: Profitability index = $1,100,000 / 400,000 = 2.75

Quick Study 25-6 (10 minutes)

Present value factor = Amount invested = $47,946 = 2.2831

Net cash flows $21,000

Quick Study 25-7 (5 minutes)

Quick Study 25-8 (15 minutes)

Incremental cost analysis

Costs of purchasing

Cost to purchase Product B …………………………………………………………..…

$5.00

Revenue loss from reduced price ($13.50 – $12.00) …………………………..

1.50

Total cost …………………………………………………………………………………………

6.50

Savings of purchasing

Costs eliminated if Product B purchased ($5 of $9) …………………………..

5.00

Net incremental cost of purchasing Product B ……………………………….…

$1.50

Analysis: Kando Co. should continue to manufacture and sell Product A.

Quick Study 25-9 (15 minutes)

X

Y

Contribution margin per unit ………………………………………..…

$ 5.00

$ 4.00

Production hours per unit …………………………………………….…

1/2

1/3

Contribution margin per production hour ……………………..…

$10.00

$12.00

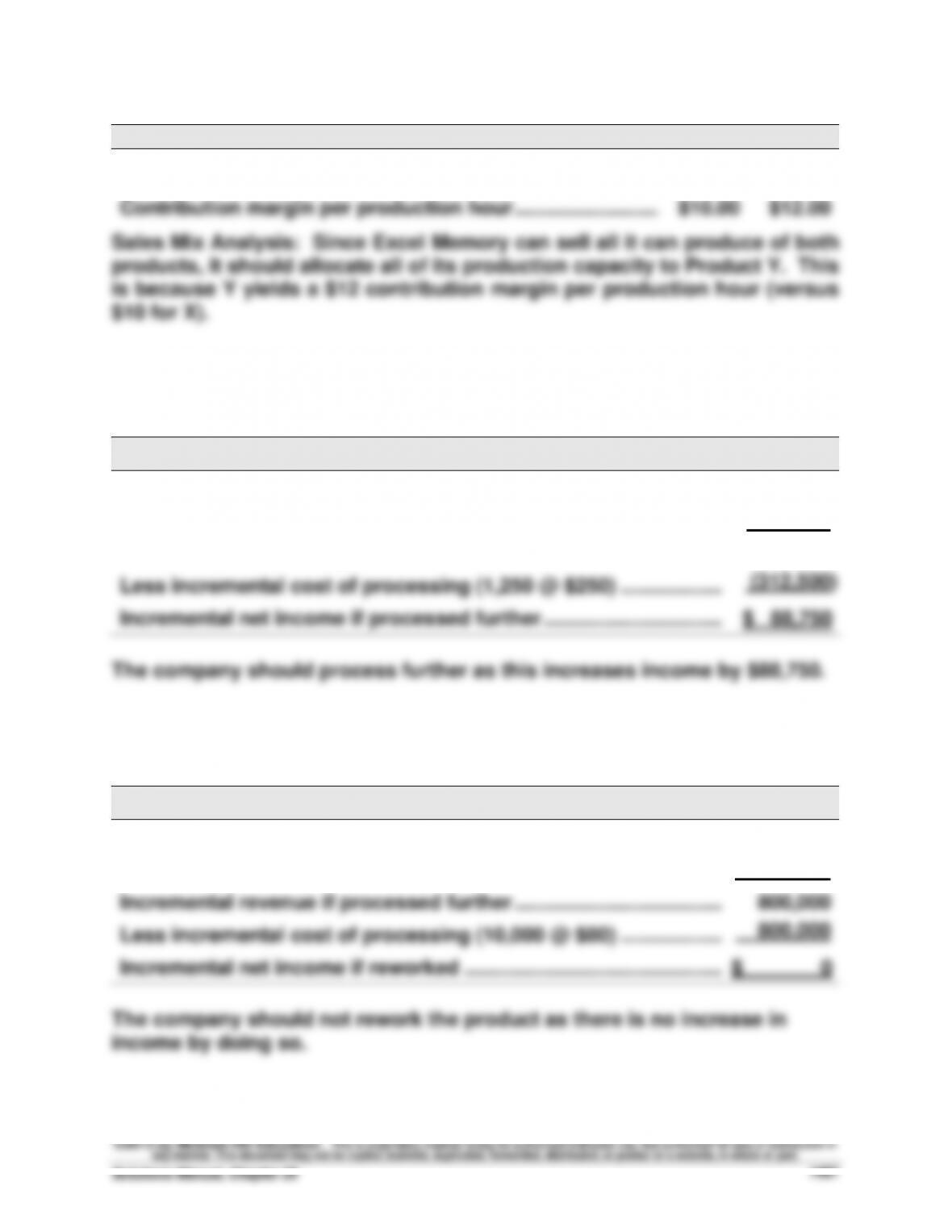

Sales Mix Analysis: Since Excel Memory can sell all it can produce of both

products, it should allocate all of its production capacity to Product Y. This

is because Y yields a $12 contribution margin per production hour (versus

$10 for X).

Quick Study 25-10 (15 minutes)

INCREMENTAL REVENUE AND COST OF ADDITIONAL PROCESSING

Revenue if processed further (1,250 @ $375) …………………………..

$468,750

Revenue if sold as is …………………………………………………………….…

67,500

Incremental revenue if processed further ……………………………….…

401,250

Less incremental cost of processing (1,250 @ $250) …………………

(312,500)

Incremental net income if processed further …………………………..

$ 88,750

The company should process further as this increases income by $88,750.

Quick Study 25-11 (15 minutes)

INCREMENTAL REVENUE AND COST OF REWORK

Revenue if processed further (10,000 @ $110) ………………………..…

$1,100,000

Revenue if sold as is (10,000 @ $30) …………………………………………

300,000

Incremental revenue if processed further ……………………………….…

800,000

Less incremental cost of processing (10,000 @ $80) …………………

800,000

Incremental net income if reworked ……………………………………….…

$ 0

The company should not rework the product as there is no increase in

income by doing so.

Fundamental Accounting Principles, 21st Edition

1468

Quick Study 25-12 (15 minutes)

INCREMENTAL INCOME FROM NEW BUSINESS

Sales (750 units @ $250) ……………………………………………………….

$ 187,500

Incremental variable costs (750 units @ $150) ……………………….….

(112,500)

Incremental fixed costs …………………………………………………………………….

Incremental income from new business ………………………………..………….

(50,000)

$ 25,000

The company should accept the offer for new business as it increases

income by $25,000.

Quick Study 25-13 (15 minutes)

Avoidable

Unavoidable

Expenses

Expenses

Cost of goods sold ………………………………….……

$56,000

—-

Direct expenses ……………………………………………

9,250

$1,250

Indirect expenses…………………………………….……

470

1,600

Service department costs ………………………..…

6,000

1,430

Total ……………………………………………………….

$71,720

$4,280

The division should not be eliminated because its sales of $72,000 are

greater than its avoidable expenses of $71,720.

Quick Study 25-14 (10 minutes)

INCREMENTAL INCOME FROM REPLACING MACHINE

Cost to buy new machine ……………………………………………………....

$(112,500)

Cash received to trade in old machine …………………………………..………….

60,000

Reduction in variable manufacturing costs ……………………………………….

Incremental income ………………………………………………………………………….

60,000

$ 7,500

The company should replace the machine as this increases income by

$7,500.

Quick Study 25-15 (15 minutes)

Year

Cash flows

Present value

of 1 at 10%

Present value of

cash flows

Cumulative

present value of

cash flows

0

$(90,000)

1.0000

$(90,000)

$(90,000)

1

35,000

0.9091

31,819

(58,181)

2

35,000

0.8264

28,924

(29,257)

3

35,000

0.7513

26,296

(2,961)

4

35,000

0.6830

23,905

20, 944

5

35,000

0.6209

21,732

42,676

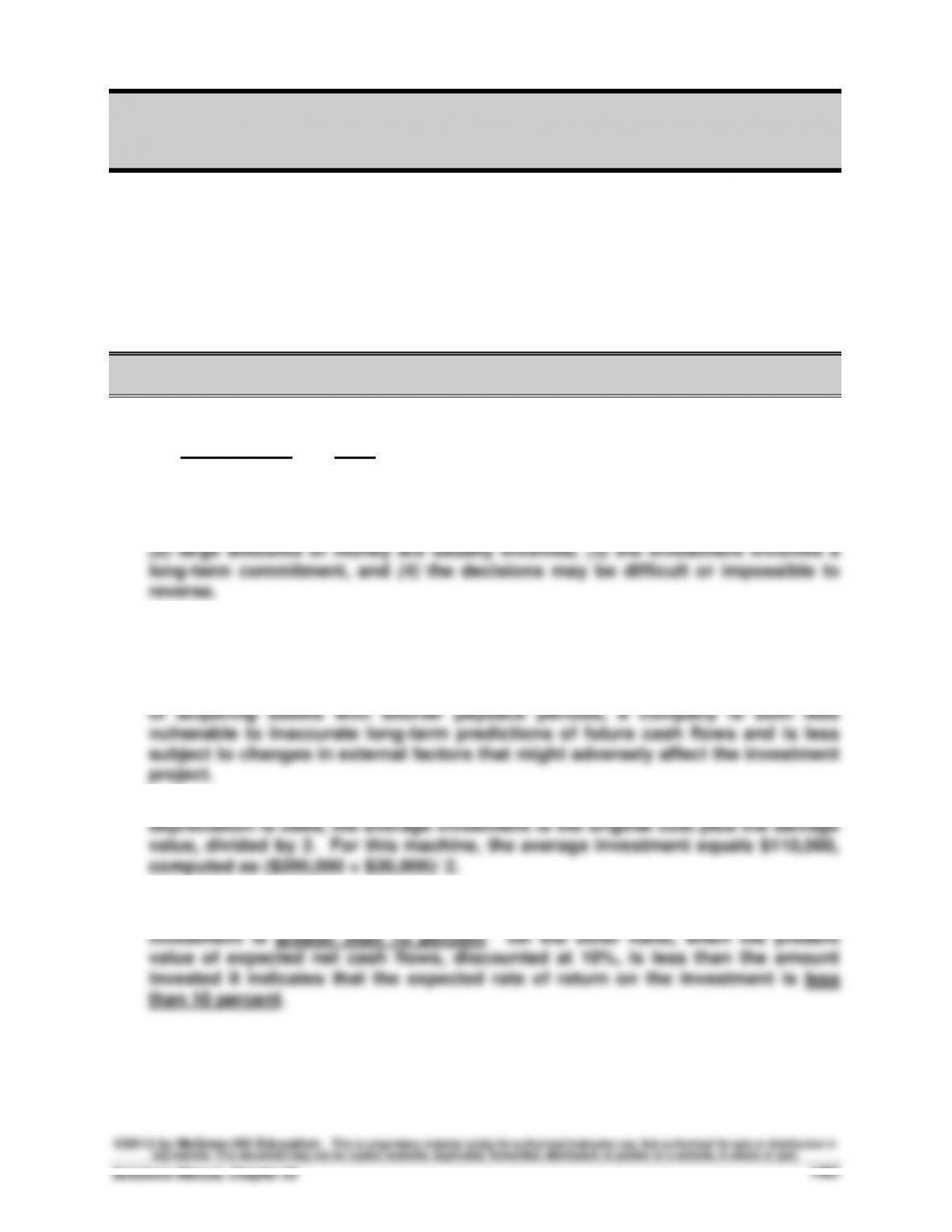

The break-even time point occurs in the 2nd month of the 4th year

[computed as ($2,961 / $23,905) x 12 = 1.5 months]. Therefore, a

reasonable estimate would be approximately 3.2 years (or 3 years, 2

months) for break-even time.

Quick Study 25-16 (15 minutes)

1. Payback period of investment = €80,000,000 / €16,000,000 = 5 years

2.

Fundamental Accounting Principles, 21st Edition

1470

EXERCISES

Exercise 25-1 (20 minutes)

Annual Net

Cumulative

Cash Flows

Cash Flows

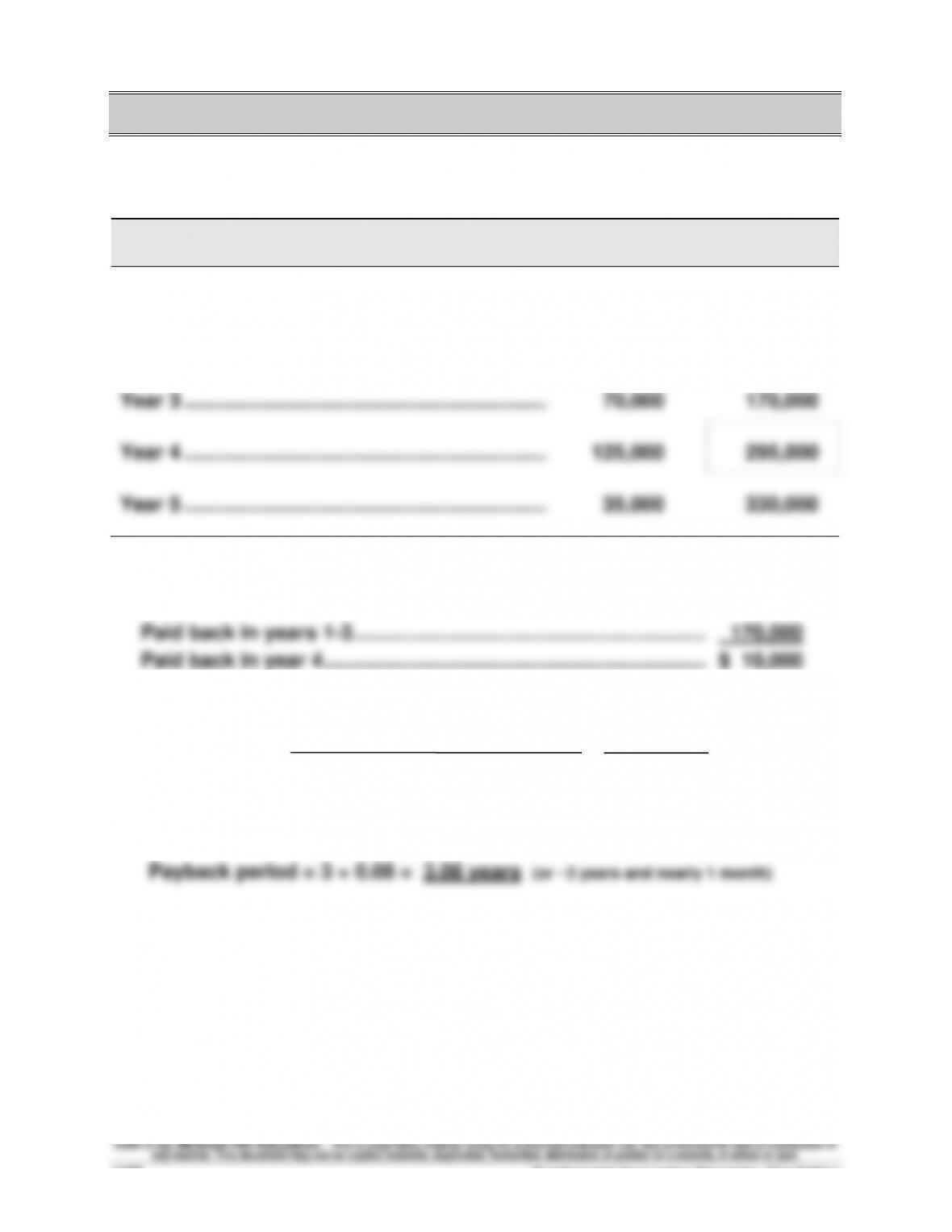

Year 1 ………………………………………………………..…

$ 60,000

$ 60,000

Year 2 ………………………………………………………..…

40,000

100,000

Year 3 ………………………………………………………..…

70,000

170,000

Year 4 ………………………………………………………..…

125,000

295,000

Year 5 ………………………………………………………..…

35,000

330,000

Cost of investment …………………………………………………………………..

$180,000

Paid back in years 1-3 ……………………………………………………….

170,000

Paid back in year 4 …………………………………………………………………..

$ 10,000

Part of year = = = 0.08

Amount paid back in year 4

Net cash flow in year 4

$10,000

$125,000

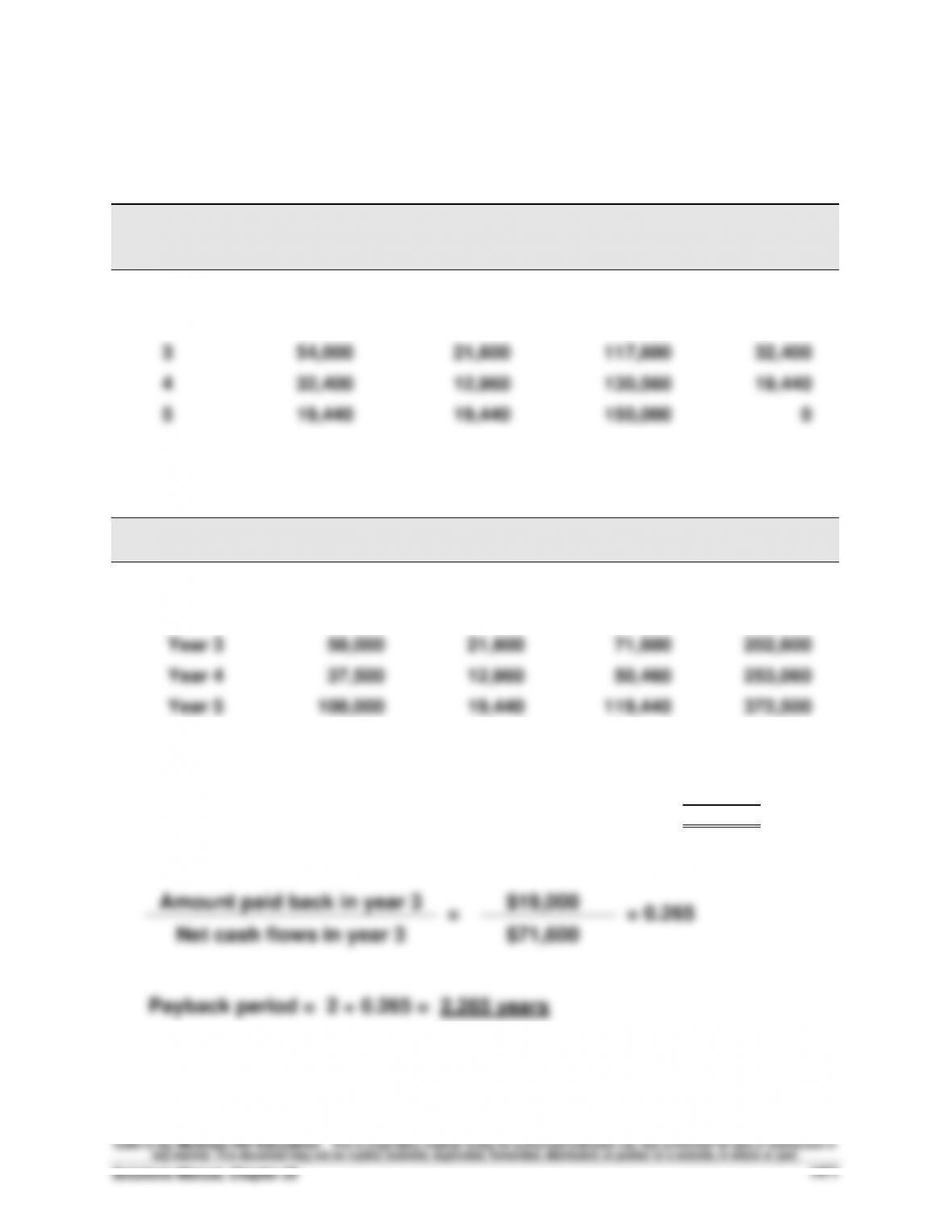

Exercise 25-2 (30 minutes)

COMPUTATION OF ANNUAL DEPRECIATION EXPENSE

Double-declining balance rate = (100% / 5) x 2 = 40%

Annual Depr.

Beginning

(40% of

Accum. Depr.

Ending

Year

Book Value

Book Value)

at Year-End

Book Value

1

$150,000

$60,000

$ 60,000

$90,000

2

90,000

36,000

96,000

54,000

3

54,000

21,600

117,600

32,400

4

32,400

12,960

130,560

19,440

5

19,440

19,440

150,000

0

ANNUAL CASH FLOWS

Net

Income

Depreciation

Net Cash

Flow

Cumulative

Cash Flow

Year 1

$ 10,000

$60,000

$ 70,000

$ 70,000

Year 2

25,000

36,000

61,000

131,000

Year 3

50,000

21,600

71,600

202,600

Year 4

37,500

12,960

50,460

253,060

Year 5

100,000

19,440

119,440

372,500

Cost of machine ……………………………………………………………..…….

$150,000

Paid back in years 1 and 2 …………………………..…………………..…….

131,000

Paid back in year 3 ………………………………………………………….…….

$ 19,000

Fundamental Accounting Principles, 21st Edition

1472

Exercise 25-3 (20 minutes)

a.

Payback period = = = 2.21 years

where

Annual after-tax income ……………………………………………………….

$150,000

Plus depreciation* …………………………………………………………….…..

85,000

Annual net cash flow ………………………………………………………..…..

$235,000

*Annual depreciation = = $85,000

b.

Annual after-tax income ……………………………………………………….

$ 60,000

Plus depreciation* …………………………………………………………….…..

45,000

Annual net cash flow ………………………………………………………..…..

$105,000

*Annual depreciation = = $45,000

Exercise 25-4 (15 minutes)

Average investment = = $400,000

$700,000 + $100,000

2

Cost of investment

Annual net cash flow

$520,000

$235,000

$520,000 – $10,000

6

$380,000 – $20,000

8

Exercise 25-5 (20 minutes)

COMPUTING NET CASH FLOWS FROM NET INCOME

Net income

Cash flows

Sales ……………………………………………………………….…….

$225,000

$225,000

Materials, labor & overhead ……………………………..…….

120,000

120,000

Depreciation ……………………………………………………….

30,000

Selling and administrative ……………………………….…….

22,500

22,500

Pretax income ……………………………………………………….

52,500

Income taxes (30%) ……………………………………………….

15,750

15,750

Net income ……………………………………………………….

$ 36,750

Net cash flows ……………………………………………………….

$ 66,750

1. Payback period = = 5.39 years

2. Accounting rate of return = = 20.42%

*Average investment

Cost ………………………………………………….…

$360,000

Salvage …………………………………………….…

0

Sum ………………………………………………….…

$360,000

Average (Sum/2) ……………………………….…

$180,000

Exercise 25-6 (20 minutes)

Annual

Net Cash

Flows

Present

Value of

Annuity

at 8%

Present

Value of

Net Cash

Flows

Years 1 through 6…………………………………..……..

$ 66,750

4.6229

$ 308,579

Amount to be invested …………………………..

(360,000)

Net present value of investment …………….……..

$ (51,421)

Based on this net present value analysis, the investment is not acceptable.

$360,000

$66,750

$36,750

$180,000*

Exercise 25-7 (35 minutes)

1.

PROJECT C1

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 12,000

0.8929

$ 10,715

Year 2 ……………………………………………………….

108,000

0.7972

86,098

Year 3 ……………………………………………………….

168,000

0.7118

119,582

Totals ……………………………………………………….

$288,000

$216,395

Amount invested …………………………………………..

(228,000)

Net present value …………………………………..……..

$ (11,605)

PROJECT C2

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 96,000

0.8929

$ 85,718

Year 2 ……………………………………………………….

96,000

0.7972

76,531

Year 3 ……………………………………………………….

96,000

0.7118

68,333

Totals ……………………………………………………….

$288,000

$230,582

Amount invested …………………………………………..

(228,000)

Net present value …………………………………..……..

$ 2,582

PROJECT C3

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$180,000

0.8929

$160,722

Year 2 ……………………………………………………….

60,000

0.7972

47,832

Year 3 ……………………………………………………….

48,000

0.7118

34,166

Totals ……………………………………………………….

$288,000

$242,720

Amount invested …………………………………………..

(228,000)

Net present value …………………………………..……..

$ 14,720

Exercise 25-7 (Continued)

2. INTERNAL RATE OF RETURN VS. NET PRESENT VALUE FOR C2

3. INTERNAL RATE OF RETURN FOR PROJECT C2

(i) Present value factor = Amount invested / Net cash flows

= $228,000 / $96,000 = 2.375

Fundamental Accounting Principles, 21st Edition

1476

Exercise 25-8 (20 minutes)

PROJECT A

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 40,000

0.9091

$ 36,364

Year 2 ……………………………………………………….

56,000

0.8264

46,278

Year 3 ……………………………………………………….

80,295

0.7513

60,326

Year 4 ……………………………………………………….

90,400

0.6830

61,743

Year 5 ……………………………………………………….

65,000

0.6209

40,359

Totals ……………………………………………………….

$331,695

245,070

Amount invested …………………………………………..

(160,000)

Net present value …………………………………..……..

$ 85,070

PROJECT B

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 32,000

0.9091

$ 29,091

Year 2 ……………………………………………………….

50,000

0.8264

41,320

Year 3 ……………………………………………………….

66,000

0.7513

49,586

Year 4 ……………………………………………………….

72,000

0.6830

49,176

Year 5 ……………………………………………………….

24,000

0.6209

14,902

Totals ……………………………………………………….

$244,000

184,075

Amount invested …………………………………………..

(105,000)

Net present value …………………………………..……..

$ 79,075

Project A’s profitability index = $85,070 / 160,000 = 0.5317

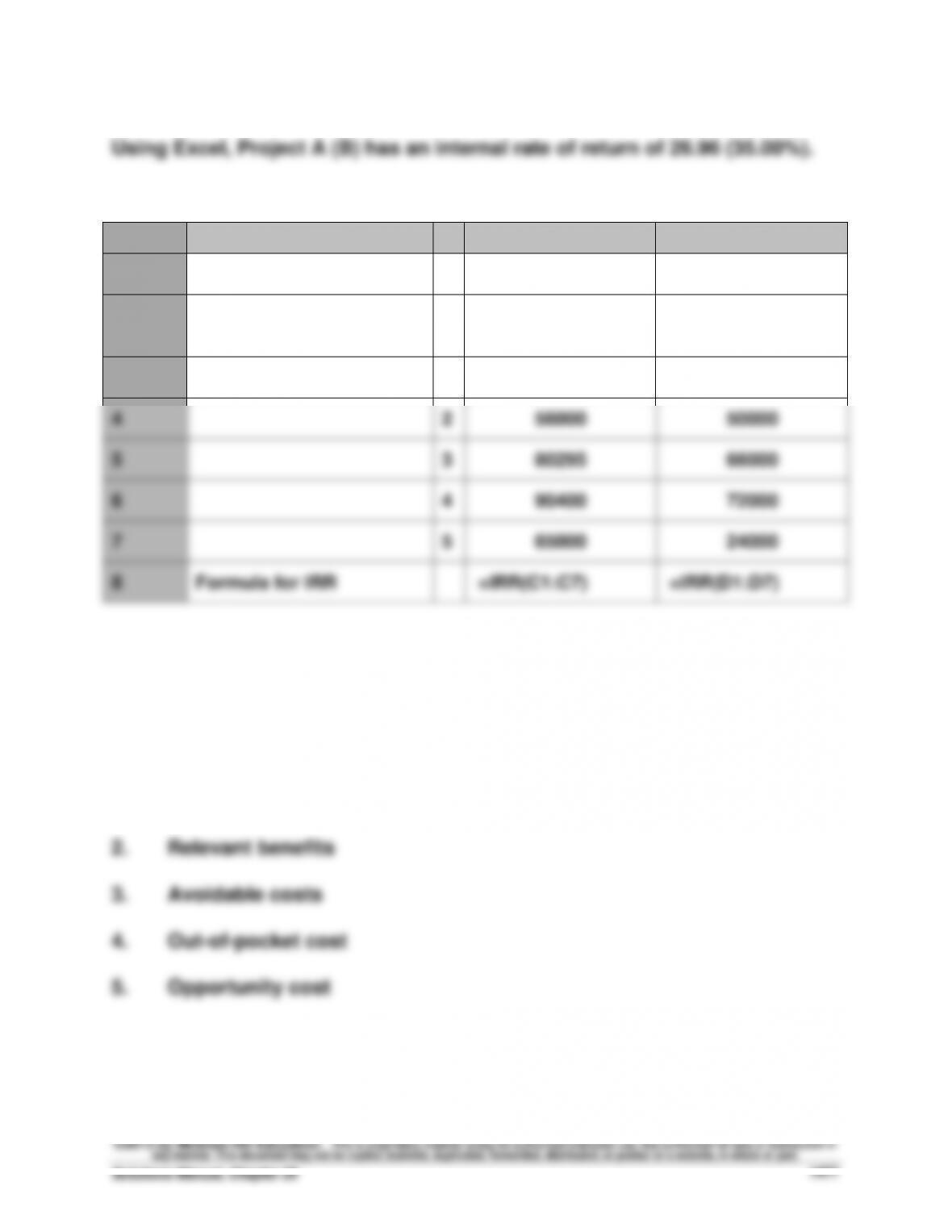

Exercise 25-9A (20 minutes)

Project A Project B

A

B

C

D

1

Initial investment

-160000

-105000

2

Annual cash flows,

end of period

3

1

40000

32000

4

2

56000

50000

5

3

80295

66000

6

4

90400

72000

7

5

65000

24000

8

Formula for IRR

=IRR(C1:C7)

=IRR(D1:D7)

Exercise 25-10 (10 minutes)

1. Sunk cost