Title: Question 1

QA_Ori:

The four-step closing entry process is: (i) close the revenue (and gain) accounts to the

Title: Question 2

QA_Ori:

Closing entries affect temporary accounts: revenues, expenses, withdrawals, and income

summary. Specifically, closing entries at the end of an accounting period prepare the

Title: Question 3

QA_Ori:

(i) Closing entries prepare the temporary accounts—revenue and expense (and gain and

Title: Question 4

QA_Ori:

The Income Summary account is used to summarize the period’s revenues and expenses.

Title: Question 5

QA_Ori:

Yes, an error would have occurred because a post-closing trial balance should only

Title: Question 6

QA_Ori:

A work sheet can be used to collect and organize data for preparing (i) adjusting entries,

Title: Question 7

QA_Ori:

The adjustments in the Adjustments columns of a work sheet are identified by letters to

Title: Question 8

QA_Ori:

A company’s operating cycle is the normal time between paying cash for merchandise

Title: Question 9

QA_Ori:

Assets on a typical classified balance sheet include current assets and noncurrent assets—

Title: Question 10

QA_Ori:

Title: Question 11

QA_Ori:

Title: Question 12

QA_Ori:

Reversing entries simplify subsequent entries for accrued expenses and accrued revenues

Title: Question 13

QA_Ori:

The following reversing entry could be made as of the first day of the next accounting

Title: Question 14

QA_Ori:

The five main categories of noncurrent assets on Polaris’s balance sheet are: Property and

Title: Question 15

QA_Ori:

KTM’s current assets are: Liquid assets; Accounts receivable – trade to third parties;

Title: Question 16

QA_Ori:

Title: Question 17

QA_Ori:

The closing entry likely recorded on December 31, 2011, to transfer the company’s net

income to its Retained Earnings account would likely have been (in thousands of Euro):

Title: Quick Study 4-1

QA_Ori:

1. Permanent accounts report on activities related to one or more future

accounting periods, and they carry their ending balances into the next period.

Title: Quick Study 4-2

QA_Ori:

1. (e) Analyzing transactions and events.

2. (h) Journalizing transactions and events.

3. (a) Posting the journal entries.

Title: Quick Study 4-3

QA_Ori:

1. B

2. F

Title: Quick Study 4-4

QA_Ori:

Current assets

Cash……………………………………………………. $ 7,000

Accounts receivable………………………………. 18,000

Current liabilities

Title: Quick Study 4-5

QA_Ori:

a. 5 d. 3

Title: Quick Study 4-6

QA_Ori:

a. BS d. IS

Title: Quick Study 4-7

QA_Ori:

CLAUDELL COMPANY

Work Sheet

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

Income

Statement

Balance Sheet

Account Title Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

Prepaid Rent………………. 1,000 (a) 200 800

Services Revenue………… 55,60

0

(b) 900 56,50

0

56,500

Title: Quick Study 4-8

QA_Ori:

Computation of B. Warton, Capital for the Dec. 31, 2013, balance sheet

Title: Quick Study 4-9

QA_Ori:

Dec. 31 Services Revenue 13,000

Income Summary

13,00

0

To close the revenue account.

Title: Quick Study 4-10

QA_Ori:

The only account from QS 4-9 that would appear in post-closing trial balance is

D. Mai, Capital.

Title: Quick Study 4-11A

QA_Ori:

2013

Jan. 1 Management Fees Earned

12,00

0

12,00

Title: Quick Study 4-12

QA_Ori:

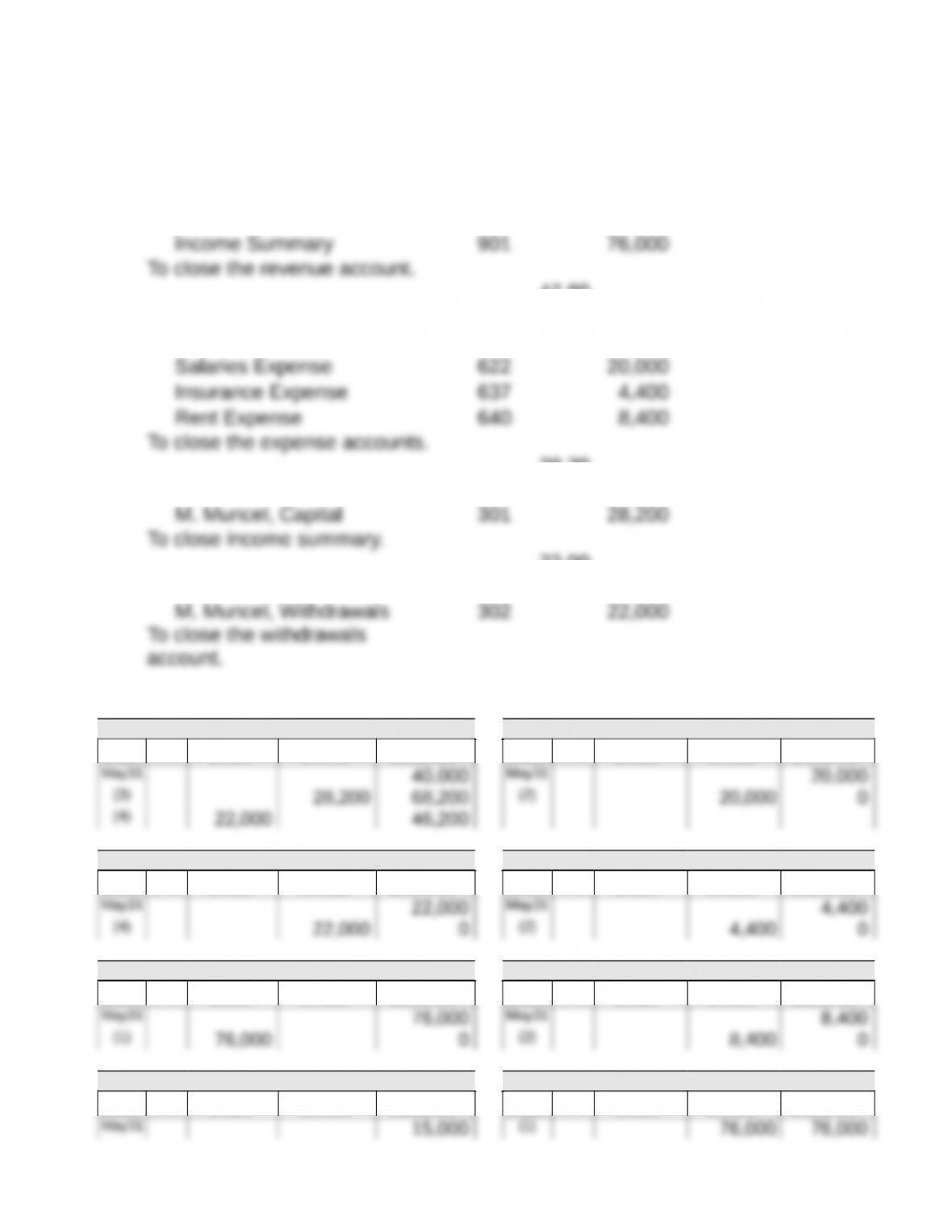

Title: Exercise 4-1

QA_Ori:

Closing entries

1 Services Revenue 401

76,00

0

2 Income Summary 901

47,80

0

Depreciation Expense 603 15,000

3 Income Summary 901

28,20

0

4 M. Muncel, Capital 301

22,00

0

Posted ledger accounts

M. Muncel, Capital No. 301 Salaries Expense No. 622

Date PR Debit Credit Balance Date PR Debit Credit Balance

M. Muncel, Withdrawals No. 302 Insurance Expense No. 637

Date PR Debit Credit Balance Date PR Debit Credit Balance

Services Revenue No. 401 Rent Expense No. 640

Date PR Debit Credit Balance Date PR Debit Credit Balance

Depreciation Expense No. 603 Income Summary No. 901

Date PR Debit Credit Balance Date PR Debit Credit Balance

Posted ledger accounts