Fundamental Accounting Principles, 21st Edition

1204

Comprehensive Problem (Continued)

(Using FIFO)

Cost per EUP

Direct

Materials

Direct Labor

Factory

Overhead

Costs incurred this period ……………...

$ 52,440

$ 202,250

$ 101,125

÷ EUP …………………………………………….

÷ 14,000

÷ 10,450

÷ 10,450

Cost per EUP (rounded) ………………….

$3.75 per

EUP

$19.35 per

EUP

$ 9.68 per

EUP

Cost assignment and reconciliation

Costs transferred out

Cost of beginning goods in process ……………………….….

$ 8,135

Cost to complete beginning goods in process

Direct materials (0 EUP x $3.75 per EUP) ……………………….

$ 0

Direct labor (1,250 EUP x $19.35 per EUP) …………….……….

24,188

Factory overhead (1,250 EUP x $9.68 per EUP) ……..……….

12,100

36,288

Costs of units started and completed this period

Direct materials (6,000 EUP x $3.75 per EUP) ………..……….

22,500

Direct labor (6,000 EUP x $19.35 per EUP) …………….……….

116,100

Factory overhead (6,000 EUP x $9.68 per EUP) ……..……….

58,080

196,680

Total cost of goods finished this period ………………….……….

241,103

Costs of ending goods in process

Direct materials (8,000 EUP x $3.75 per EUP) ………..……….

30,000

Direct labor (3,200 EUP x $19.35 per EUP) …………….……….

61,920

Factory overhead (3,200 EUP x $9.68 per EUP) ……..……….

30,976

122,896

Total costs accounted for ……………………………………….……….

$363,999*

*Equals $363,950 costs to account for with $49 rounding difference

Part 3 — Journal entries (Using FIFO)

g.

Finished Goods Inventory ………………………………..………….

241,103

Goods in Process Inventory ………………………..…

241,103

Transferred goods to Finished Goods.

h.

Cash ………………………………………………………………..………….

625,000

Sales ………………………………………………………….………….

625,000

Sold finished goods for cash.

Cost of Goods Sold …………………………………………………….

265,700

Finished Goods Inventory ……………………………………….

265,700

Transferred costs to COGS.

Comprehensive Problem (Continued)

Part 4 (Using FIFO)

General ledger accounts

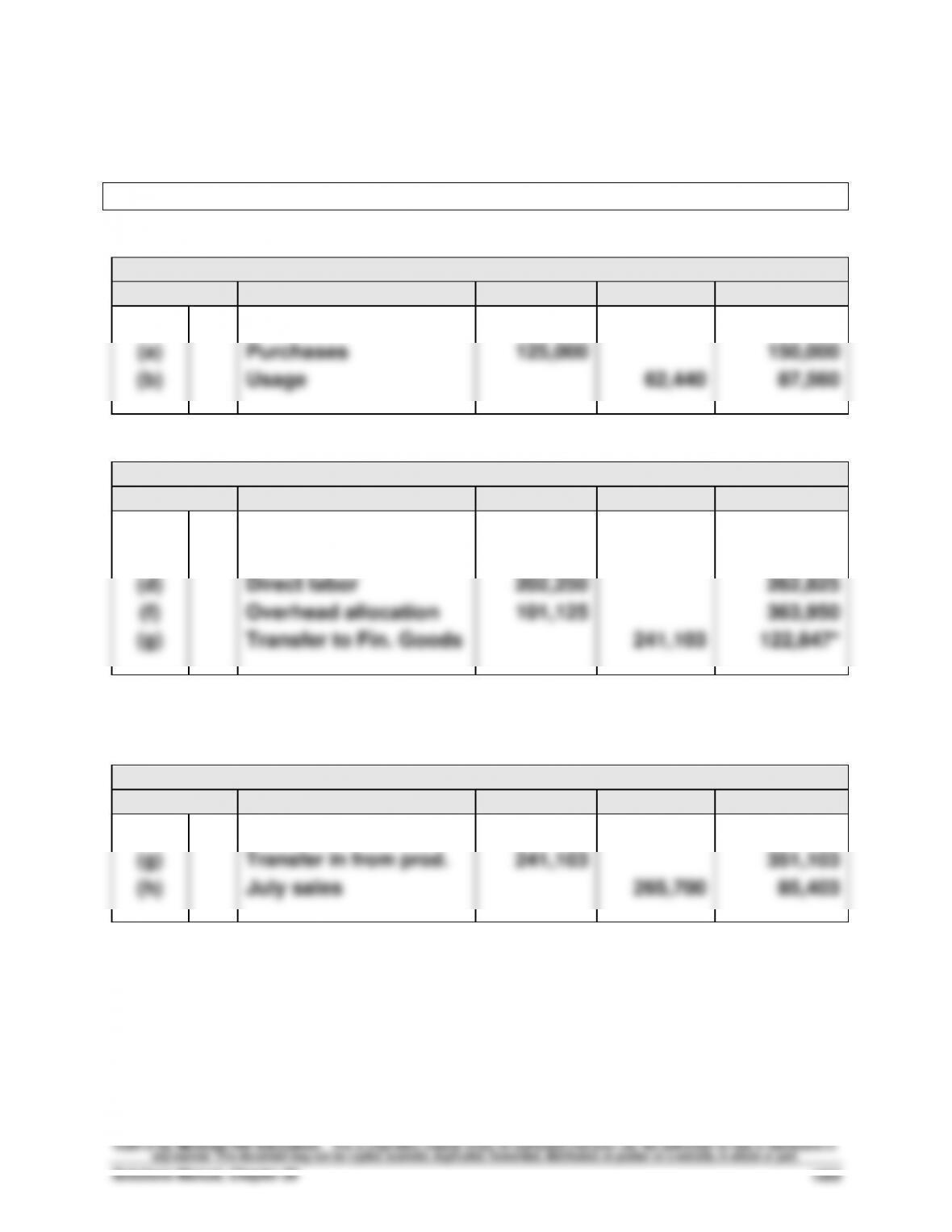

Raw Materials Inventory

Acct. No. 132

Date

Explanation

Debit

Credit

Balance

June

30

Balance

25,000

(a)

Purchases

125,000

150,000

(b)

Usage

62,440

87,560

Goods in Process Inventory

Acct. No. 133

Date

Explanation

Debit

Credit

Balance

June

30

Balance

8,135

(b)

Direct materials

52,440

60,575

(d)

Direct labor

202,250

262,825

(f)

Overhead allocation

101,125

363,950

(g)

Transfer to Fin. Goods

241,103

122,847*

*Agrees with $122,896 from process cost summary with $49 rounding difference

Finished Goods Inventory

Acct. No. 135

Date

Explanation

Debit

Credit

Balance

June

30

Balance

110,000

(g)

Transfer in from prod.

241,103

351,103

(h)

July sales

265,700

85,403

Fundamental Accounting Principles, 21st Edition

1206

Comprehensive Problem (Concluded)

Part 4—concluded

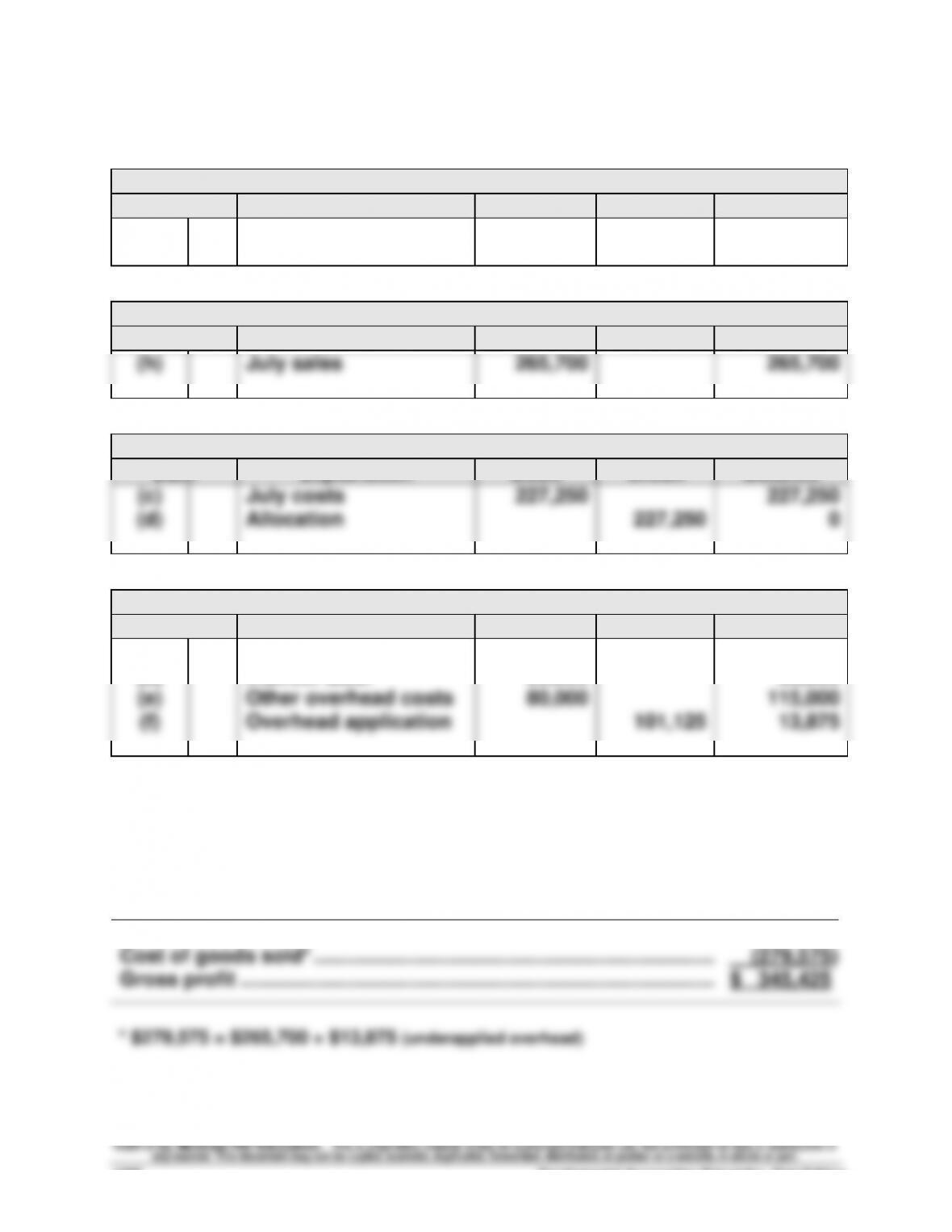

Sales

Acct. No. 413

Date

Explanation

Debit

Credit

Balance

(h)

July sales

625,000

625,000

Cost of Goods Sold

Acct. No. 502

Date

Explanation

Debit

Credit

Balance

(h)

July sales

265,700

265,700

Factory Payroll

Acct. No. 530

Date

Explanation

Debit

Credit

Balance

(c)

July costs

227,250

227,250

(d)

Allocation

227,250

0

Factory Overhead

Acct. No. 540

Date

Explanation

Debit

Credit

Balance

(b)

Indirect materials

10,000

10,000

(d)

Indirect labor

25,000

35,000

(e)

Other overhead costs

80,000

115,000

(f)

Overhead application

101,125

13,875

Part 5 (Using weighted-average)

Computation of gross profit for July

Sales ……………………………………………………….………………………………

$ 625,000

Cost of goods sold* …………………………………………………………………

(279,575)

Gross profit ………………………………………………………………………….…

$ 345,425

* $279,575 = $265,700 + $13,875 (underapplied overhead)

Reporting in Action — BTN 20-1

1. These costs are part of getting the products that Polaris sells to its

customers, costs to fulfill warranties to its customers, and

2. These costs would either be expensed as cost of sales or as selling

and administrative expenses. Thus, net income will not be affected.

Comparative Analysis — BTN 20-2

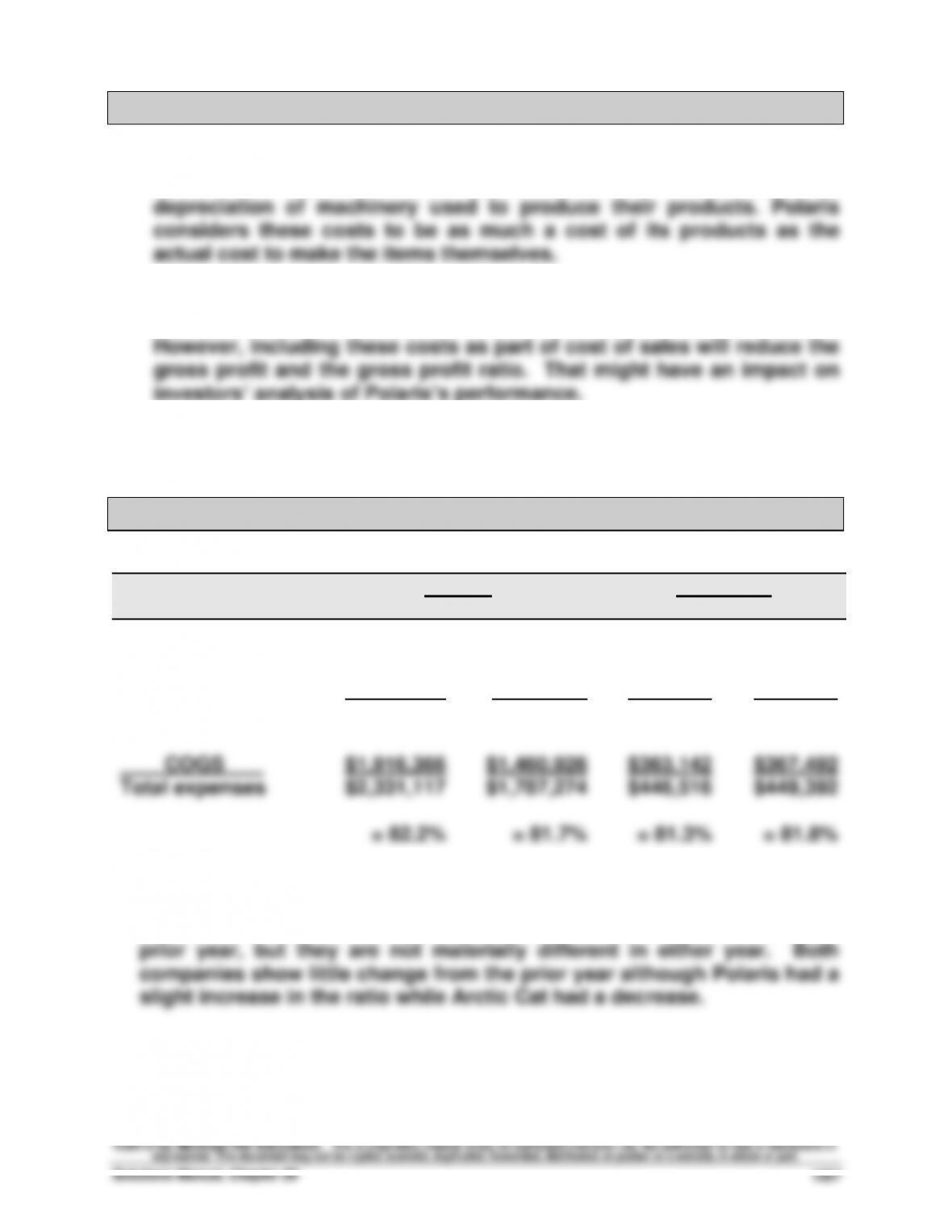

1.

Polaris

Arctic Cat

($ thousands)

Current Year

Prior Year

Current Year

Prior Year

Expenses

Cost of goods sold ……

$1,916,366

$1,460,926

$363,142

$367,492

Operating expenses .…

414,751

326,348

83,374

81,900

Total expenses ……….…

$2,331,117

$1,787,274

$446,516

$449,392

COGS .

Total expenses

$1,916,366

$2,331,117

= 82.2%

$1,460,926

$1,787,274

= 81.7%

$363,142

$446,516

= 81.3%

$367,492

$449,392

= 81.8%

2. Polaris and Arctic Cat have similar ratios for both years. Polaris has a

higher ratio in the current year and Arctic Cat has a higher ratio in the

Ethics Challenge — BTN 20-3

MEMORANDUM

TO:

FROM:

DATE:

SUBJECT:

Instructor note: The student’s solution will vary depending on the industry, product, and process

chosen. It will also depend on the sources obtained.

The memorandum should initially identify an industry (say, steel), a

product (say, cans), and a process (say, forming).

Generally, there are at least three approaches to maintaining and

expanding one’s knowledge about a particular industry, product, and

process—students are likely to have additional insights.

Communicating in Practice — BTN 20-4

MEMORANDUM

TO:

FROM:

DATE:

SUBJECT:

The main focus of this memorandum should be to explain the difference

between determining direct and indirect costs in a job order versus a

process cost accounting system since this appears to be the primary

source of confusion. In addition to the memorandum’s content, the

instructor should look for a student’s ability to be diplomatic in the

communication.

Points the memorandum should make include:

1. The reason for the assistant’s confusion. Given the assistant’s

2. Since your company does not limit production to specific batches of

3. It is important to recognize that the cost object is the process, not the

job. If costs are traceable to the cost object, they are direct costs.

4. In job order cost accounting, materials and labor used exclusively on

specific jobs are charged to the jobs as direct costs. Materials and

5. A process cost accounting system uses the concepts of direct and

6. Some costs classified as manufacturing overhead in a job order system

can be classified as direct costs in process cost accounting. For

Fundamental Accounting Principles, 21st Edition

1210

Taking It to the Net — BTN 20-5

There are several ways that such software is helpful to a business.

• This software allows companies to create process maps so they can

analyze and communicate processes and workflows.

• It provides a calculation of cost per process and activity.

Teamwork in Action — BTN 20-6

Each member of the team should participate in the activity to improve and

reinforce his/her understanding of the entries that correspond to Exhibit

20.4. (Note: The entries below are pro forma entries since information for

amounts are not provided in this activity.)

1.

Raw Materials Inventory …………………………..

#

Accounts Payable …………………………………………….

#

Purchased materials on credit.

2.

Goods in Process Inventory …………………….…….

#

Raw Materials Inventory ……………………..……

#

To assign costs of direct materials

used in production departments.

3.

Factory Overhead …………………………………….…………….

#

Raw Materials Inventory ……………………..……

#

To record indirect materials used.

Teamwork in Action (concluded)

4.

Factory Payroll ……………………………………….…………….

#

Cash ……………………………………………………….

#

To record factory wages incurred.

5.

Goods in Process Inventory …………………….…….

#

Factory Payroll …………………………………..…………….

#

To assign costs of direct labor used

in production.

6.

Factory Overhead …………………………………….…………….

#

Factory Payroll …………………………………..…………….

#

To record indirect labor as overhead.

7.

Factory Overhead ………………………………………………….

#

Prepaid Insurance ……………………………..…………….

#

Accrued Utilities Payable …………………..………

#

Cash ………………………………………………….……

#

Accum. Depreciation—Factory Equip ….…………….

#

To record manufacturing overhead incurred.

8.

Goods in Process Inventory ……………………..……

#

Factory Overhead ………………………………..……………

#

Allocated factory overhead costs

to production.

9.

Finished Goods Inventory …………………………..

#

Goods in Process Inventory ………………..…………

#

To record the transfer of completed

goods from production to finished

goods inventory.

10.

Accounts Receivable ………………………………..……………

#

Sales …………………………………………………..…..

#

To record sale.

Cost of Goods Sold …………………………………..……………

#

Finished Goods Inventory …………………………..

#

To record cost of goods sold.

Fundamental Accounting Principles, 21st Edition

1212

Entrepreneurial Decision — BTN 20-7

1. Neal’s new manufacturing facility enables him to make his own mix for

less than $7 per gallon. Overall, his cost per equivalent unit will be

2. If a business unnecessarily holds materials, it will be less profitable

than a company that maintains appropriate raw materials inventory

levels. First, the inventory requires costs for storage space. Second,

when inventory is perishable, additional costs must be incurred to

3. A hybrid system combines features of both process and job order

operations. Three Twins Ice Cream resembles a process operation in

that each flavor of ice cream goes through the same processing steps.

Hitting The Road — BTN 20-8

Instructor note: This assignment is designed to help students identify

specific costs in a service process costing system. The answers are likely

to be unique for each student. Below are a few suggestions. This problem

is also a review of cost classifications.

Cost

Description

Direct

Material

Direct

Labor

Overhead

Variable

Cost

Fixed

Cost

Manual

sorting

X

X

Heating and

cooling

X

X

Manually

moving mail

– within

department

X

X

If hired on

a temp.

basis

X

Full time

labor under

contract.

Manually

moving mail

– between

departments

X

X

If hired on

a temp.

basis

X

Full time

labor under

contract

Sorting

equipment

X

X

Rentals

X

X

Overhead allocation suggestions:

Not all components should be allocated the same. Some examples:

Heating cost can be allocated on square footage.

Rent cost on the value of floor space occupied.

Fundamental Accounting Principles, 21st Edition

1214

Global Decision — BTN 20-9

1. Ratio of Cost of Goods Sold to Total Expenses

(€ millions)

Current Year

Prior Year

Piaggio …………………..…

€1,061.9 / €1,411=

75.3%

€1,023.1 / €1,374.3=

74.4%

(From BTN 20-2)

($ thousands)

Current Year

Prior Year

Polaris ………………………

$1,916,366/

$2,331,117

= 82.2%

$1,460,926/

$1,787,274

= 81.7%

($ thousands)

Current Year

Prior Year

Arctic Cat ……………….…

$363,142/

$446,516

= 81.3%

$367,492/

$449,392

= 81.8%

2. As a percentage of total expenses, Piaggio spends more on selling and