Problem 6-3A (Continued)

3d. Specific Identification

Cost of goods available for sale ……………….

$77,200

Less: Cost of Goods Sold

600 @ $45.00 ……………………………….

$27,000

300 @ $42.00 ……………………………….

12,600

200 @ $27.00 ……………………………….

5,400

50 @ $50.00 ……………………………….

2,500

250 @ $46.00 ……………………………….

11,500

Total cost of goods sold …………………………..

59,000

Ending Inventory ……………………………………..

$18,200

Proof of Ending Inventory

100 @ $42

$ 4,200

50 @ $50

$ 2,500

250 @ $46

11,500

Ending Inventory….

400 units

$18,200

4.

FIFO

LIFO

Specific

Identifi-

cation

Weighted

Average

Sales (1,400 x $75) ……………..

$105,000

$105,000

$105,000

$105,000

Less: Cost of goods sold …...

58,800

59,200

59,000

59,440

Gross profit ………………………..

$ 46,200

$ 45,800

$ 46,000

$ 45,560

5. Montoure’s manager would likely prefer the FIFO method since this

Problem 6-4A (40 minutes)

1. Calculate cost of goods available for sale and units available for sale

Beginning inventory ……………………...

600 units @ $45.00

$27,000

Feb. 10 ………………………………………….

400 units @ $42.00

16,800

Mar. 13 ………………………………………….

200 units @ $27.00

5,400

Aug. 21 ………………………………………….

100 units @ $50.00

5,000

Sept. 5 ………………………………………….

500 units @ $46.00

23,000

Units available ……………………………….

1,800 units

Cost of goods available for sale

$77,200

2. Units in ending inventory

Units available (from part 1) …………..…………..

1,800

Less: Units sold (800+600) …………….…………..

1,400

Ending Inventory (units) ………………..…………

400

Problem 6-4A (Concluded)

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(400 x $46.00)…………………………………………………….

$18,400.00

(600x$45.00) + (400x$42.00) + (200x$27.00) +

(100x$50.00) + (100x$46.00) ……………………………….

$58,800.00

b. LIFO

(400 x $45.00)……………………………………………………

$18,000.00

(500 x $46.00) + (100 x $50.00) + (200 x $27.00) +

(400 x $42.00) + (200 x $45.00) …………………………..

$59,200.00

c. Weighted average ($77,200/1,800 = $42.89 [rounded])

(400 x $42.89)…………………………………………………….

$17,156.00

$77,200 [Goods Available] – $17,156.00 [Ending Inventory] ………

$60,044.00

d. Specific identification

(100 x $42.00) + (50 x $50.00) + (250 x $46.00) …….

$18,200.00

$77,200 [Goods Available] – $18,200.00 [Ending Inventory] ………

$59,000.00

4.

FIFO

LIFO

Specific

Identifi-

cation

Weighted

Average

Sales (1,400 x $75) ……………..

$105,000

$105,000

$105,000

$105,000

Less: Cost of goods sold …...

58,800

59,200

59,000

60,044

Gross profit ………………………..

$ 46,200

$ 45,800

$ 46,000

$ 44,956

5. The manager would likely prefer the FIFO method since this methods’

Problem 6-5A (50 minutes)

Per Unit

Total

Total

LCM Applied

to Items

Inventory Items

Units

Cost

Market

Cost

Market

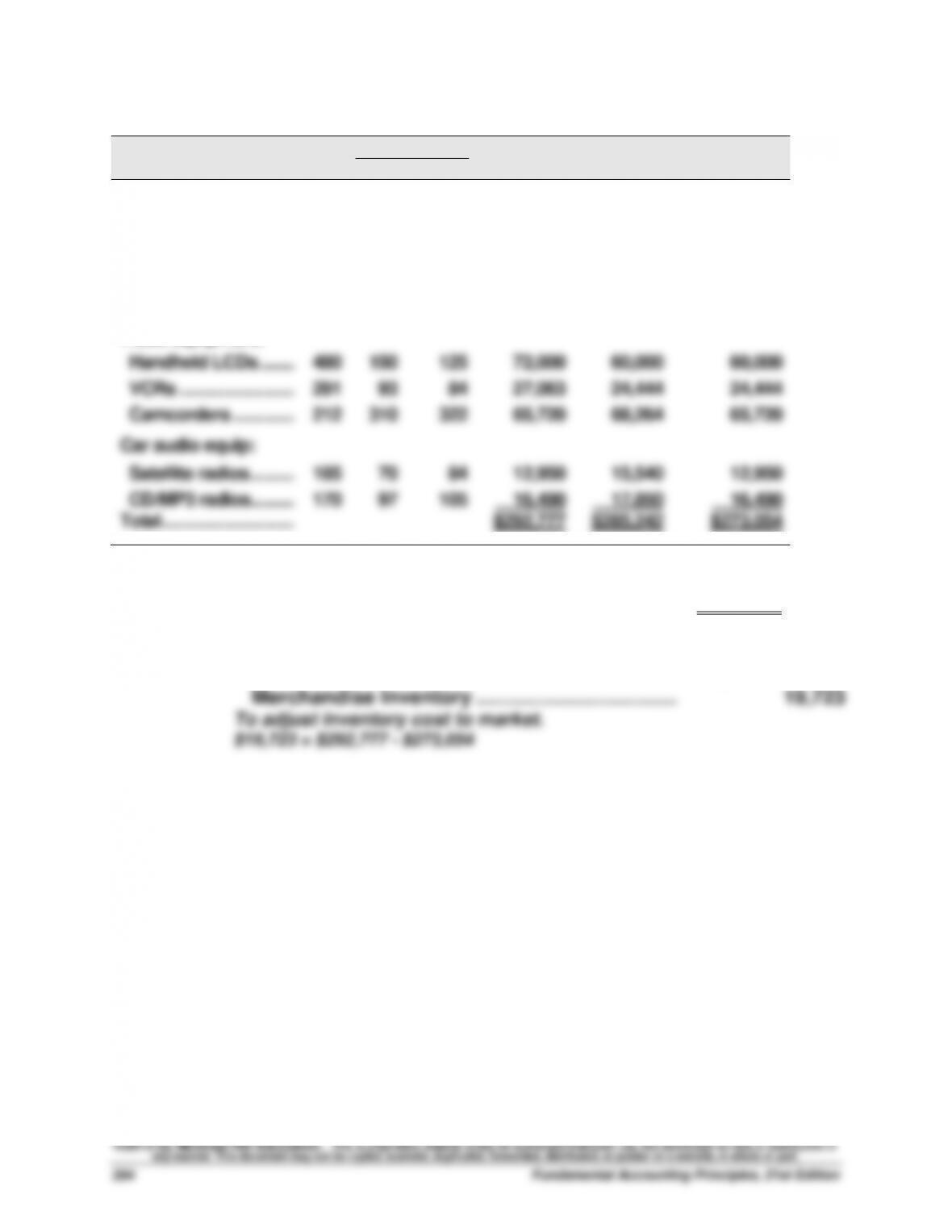

Audio equipment:

Receivers ………………..

345

$ 90

$ 98

$ 31,050

$ 33,810

$ 31,050

CD players ……………...

260

111

100

28,860

26,000

26,000

MP3 players …………...

326

86

95

28,036

30,970

28,036

Speakers………………...

204

52

41

10,608

8,364

8,364

Video equipment:

Handheld LCDs ……...

480

150

125

72,000

60,000

60,000

VCRs ……………………...

291

93

84

27,063

24,444

24,444

Camcorders …………...

212

310

322

65,720

68,264

65,720

Car audio equip:

Satellite radios ………..

185

70

84

12,950

15,540

12,950

CD/MP3 radios………..

170

97

105

16,490

17,850

16,490

Total ………………………….

$292,777

$285,242

$273,054

1. Lower of cost or market for inventory applied separately = $273,054

2.

Dec 31

Cost of Goods Sold ………………………………………….….

19,723

Merchandise Inventory ……………………………….….

19,723

To adjust inventory cost to market.

$19,723 = $292,777 – $273,054

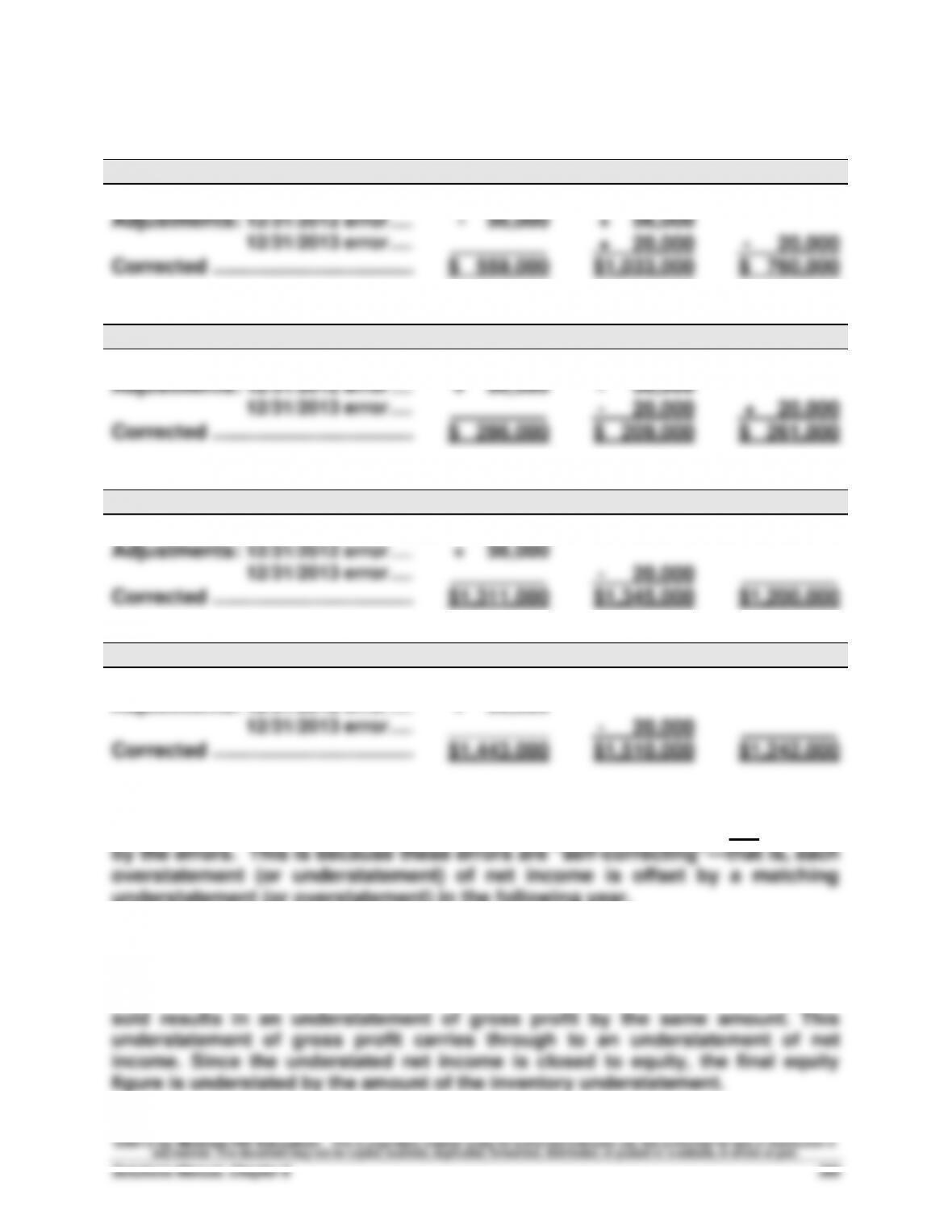

Problem 6-6A (35 minutes)

Part 1

(a)

Cost of goods sold

2012

2013

2014

Reported …………………………..…….

$ 615,000

$ 957,000

$ 780,000

Adjustments: 12/31/2012 error ……

– 56,000

+ 56,000

12/31/2013 error ……

.

+ 20,000

– 20,000

Corrected ……………………………….

$ 559,000

$1,033,000

$ 760,000

(b)

Net income

2012

2013

2014

Reported …………………………..…….

$ 230,000

$ 285,000

$ 241,000

Adjustments: 12/31/2012 error ……

+ 56,000

– 56,000

12/31/2013 error ……

.

– 20,000

+ 20,000

Corrected ……………………………….

$ 286,000

$ 209,000

$ 261,000

(c)

Total current assets

2012

2013

2014

Reported …………………………..…….

$1,255,000

$1,365,000

$1,200,000

Adjustments: 12/31/2012 error ……

+ 56,000

12/31/2013 error ……

.

– 20,000

.

Corrected ……………………………….

$1,311,000

$1,345,000

$1,200,000

(d)

Equity

2012

2013

2014

Reported …………………………..…….

$1,387,000

$1,530,000

$1,242,000

Adjustments: 12/31/2012 error ……

+ 56,000

12/31/2013 error ……

_________

– 20,000

.

Corrected ……………………………….

$1,443,000

$1,510,000

$1,242,000

Part 2

Total net income for the combined three-year period ($756,000) is not affected

understatement (or overstatement) in the following year.

Part 3

The understatement of inventory by $56,000 results in an overstatement of cost of

goods sold by that same amount. The $56,000 overstatement of cost of goods

Problem 6-7AA (25 minutes)

Part 1

Number and total cost of units available for sale

23,000 units in beginning inventory @ $15 …………………….. $ 345,000

30,000 units purchased @ $18 ……………………………………….. 540,000

39,000 units purchased @ $20 ……………………………………….. 780,000

Part 2

a. FIFO periodic

Total cost of 150,000 units available for sale …….…………

$3,150,000

Less ending inventory on a FIFO basis

35,000 units @ $26 ………………………………………..…………

$910,000

5,000 units @ $25 ………………………………………..…………

125,000

1,035,000

Cost of goods sold …………………………………………..…………

$2,115,000

b. LIFO periodic

Total cost of 150,000 units available for sale …….…………

$3,150,000

Less ending inventory on a LIFO basis

23,000 beginning inventory units @ $15 ……………………

$345,000

17,000 units @ $18 ………………………………………..…………

306,000

651,000

Cost of goods sold …………………………………………..…………

$2,499,000

c. Weighted average periodic

Total cost of 150,000 units available for sale …….…………

$3,150,000

Less ending inventory at weighted average

($3,150,000/150,000) x 40,000 …………………………..

840,000

Cost of goods sold …………………………………………..…………

$2,310,000

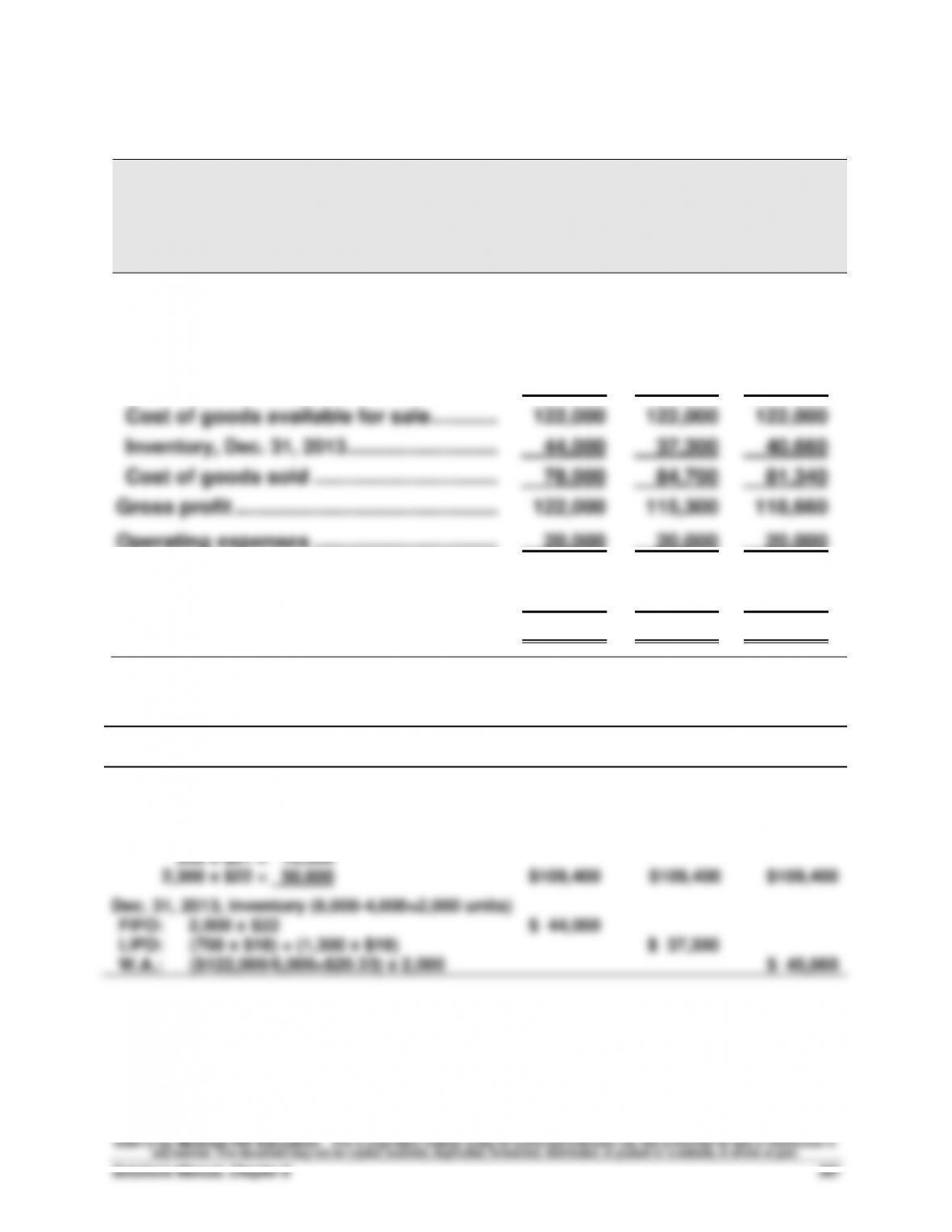

Problem 6-8AA (50 minutes)

Part 1

QP CORP.

Income Statements Comparing FIFO, LIFO, and Weighted Average

For Year Ended December 31, 2013

FIFO

LIFO

Weighted

Average

Sales ………………………………………………….….

$200,000

$200,000

$200,000

Cost of goods sold

Inventory, Dec. 31, 2012 …………………….….

12,600

12,600

12,600

Cost of purchases……………………………..….

109,400

109,400

109,400

Cost of goods available for sale …………….

122,000

122,000

122,000

Inventory, Dec. 31, 2013 ………………………….

44,000

37,300

40,660

Cost of goods sold ……………………………….

78,000

84,700

81,340

Gross profit ………………………………………..….

122,000

115,300

118,660

Operating expenses ……………………………….

20,000

20,000

20,000

Income before taxes ……………………………….

102,000

95,300

98,660

Income taxes expense (40%) ……………….….

40,800

38,120

39,464

Net income …………………………………………….

$ 61,200

$ 57,180

$ 59,196

Supporting calculations

FIFO

LIFO

Weighted

Average

Dec. 31, 2012, inventory (700 x $18). …………….

$ 12,600

$ 12,600

$ 12,600

Purchases

1,700 x $19 = $32,300

800 x $20 = 16,000

500 x $21 = 10,500

2,300 x $22 = 50,600

$109,400

$109,400

$109,400

Dec. 31, 2013, inventory (6,000-4,000=2,000 units)

FIFO:

2,000 x $22

$ 44,000

LIFO:

(700 x $18) + (1,300 x $19)

$ 37,300

W.A.:

($122,000/6,000=$20.33) x 2,000

$ 40,660

Problem 6-8AA (Concluded)

Part 2

If QP Corp. had been experiencing declining costs in the acquisition of

inventory, we would observe the opposite results in our comparisons.

Part 3

Advantages

LIFO: Given the cost trends in the problem, the advantage of using LIFO is

that the lower net income will result in a lower tax obligation (tax deferral).

Disadvantages

LIFO: Given the cost trends in the problem, the disadvantage of using LIFO

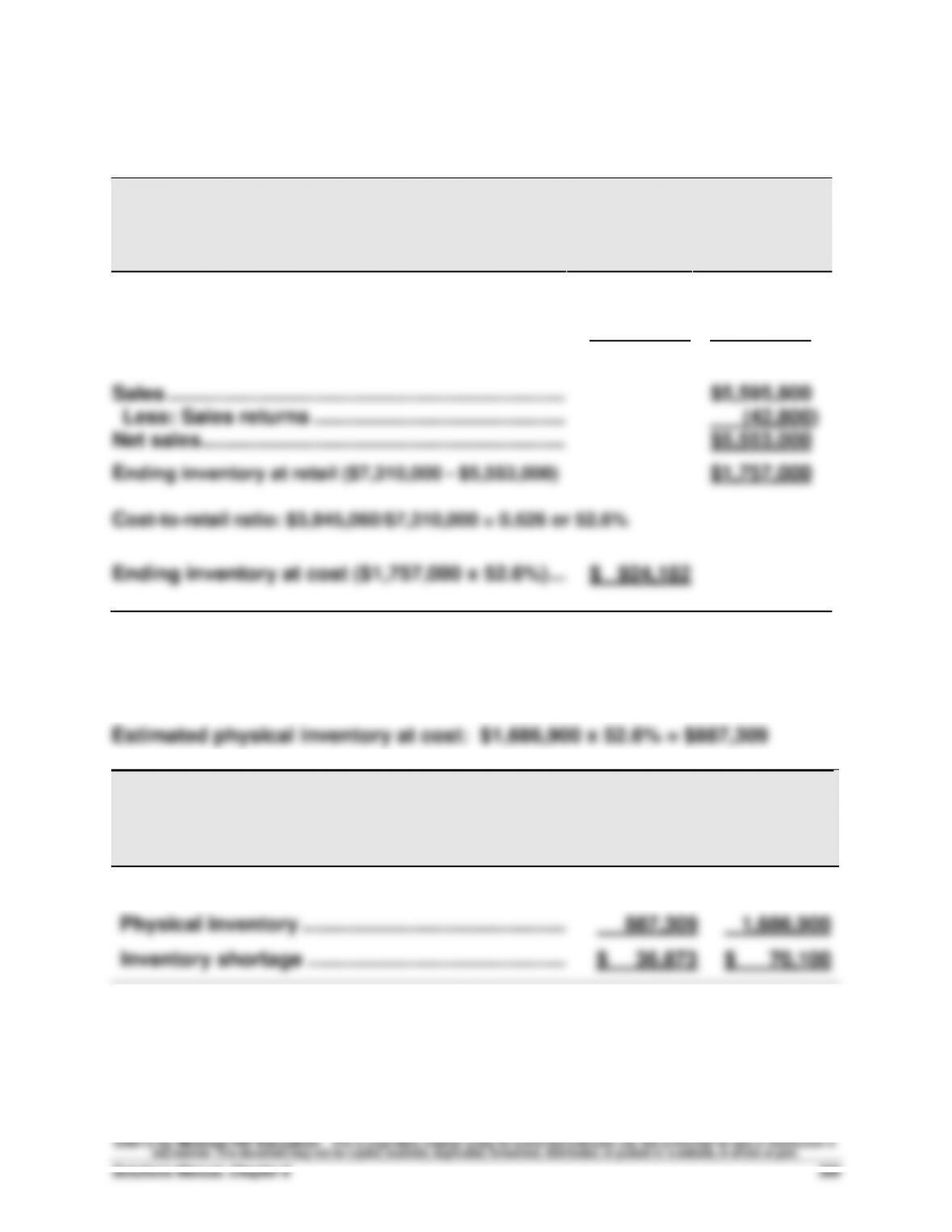

Problem 6-9AA (25 minutes)

Part 1

ALASKA COMPANY

Estimated Inventory

December 31

At Cost

At Retail

Goods available for sale

Beginning inventory……………………………………..

$ 469,010

$ 928,950

Cost of goods purchased ……………………………..

3,376,050

6,381,050

Goods available for sale ……………………………….

$3,845,060

$7,310,000

Sales ……………………………………………………………..

$5,595,800

Less: Sales returns ………………………………………

(42,800)

Net sales ………………………………………………………..

$5,553,000

Ending inventory at retail ($7,310,000 – $5,553,000)

$1,757,000

Cost-to-retail ratio: $3,845,060/$7,310,000 = 0.526 or 52.6%

Ending inventory at cost ($1,757,000 x 52.6%) ….……….

$ 924,182

Part 2

ALASKA COMPANY

Inventory Shortage

December 31

At Cost

At Retail

Estimated inventory (from part 1) …………………..…..

$ 924,182

$ 1,757,000

Physical inventory ……………………………………………..

887,309

1,686,900

Inventory shortage ………………………………………..…..

$ 36,873

$ 70,100

Problem 6-10AB (25 minutes)

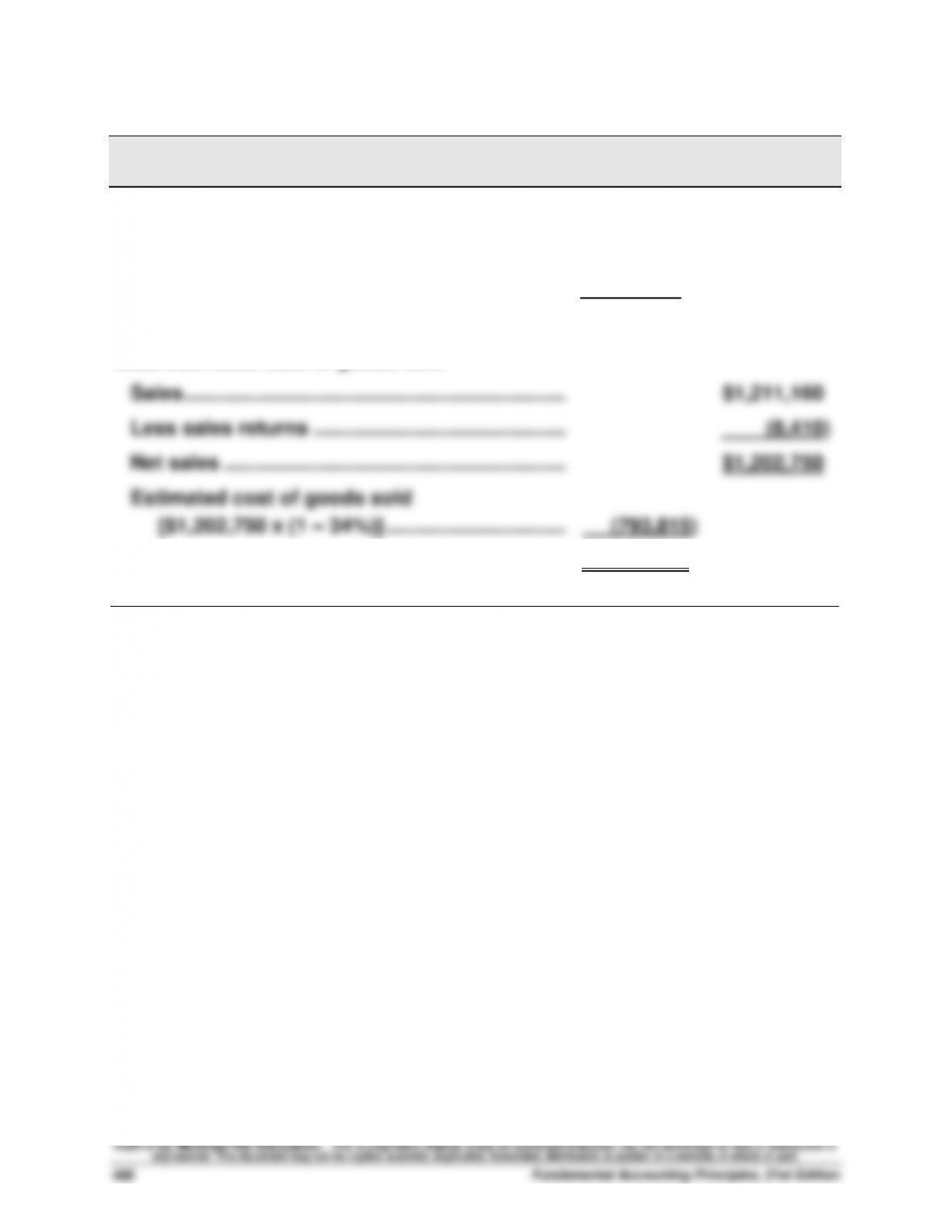

WAYWARD COMPANY

Estimated Inventory at March 31

Goods available for sale

Inventory, January 1 …………………………………….…

$ 302,580

Cost of goods purchased ……………………………..…

941,040

Goods available for sale ……………………………….…

1,243,620

Less estimated cost of goods sold

Sales ………………………………………………………………

$1,211,160

Less sales returns ……………………………………….…

(8,410)

Net sales ……………………………………………………....

$1,202,750

Estimated cost of goods sold

[$1,202,750 x (1 – 34%)] ………………………………

(793,815)

Estimated March 31 inventory …………………………..

$ 449,805

PROBLEM SET B

Problem 6-1B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

20 units @ $3,000

$ 60,000

April 6 …………………………………………..

30 units @ $3,500

105,000

April 17 ………………………………………….

5 units @ $4,500

22,500

April 25 ………………………………………….

10 units @ $4,800

48,000

Units available ……………………………….

65 units

Cost of goods available for sale ……..

$235,500

2. Units in ending inventory

Units available (from part 1) …………..…………..

65 units

Less: Units sold (35 + 25) …………………………..

60 units

Ending Inventory (units) ………………..…………

5 units

Problem 6-1B (Continued)

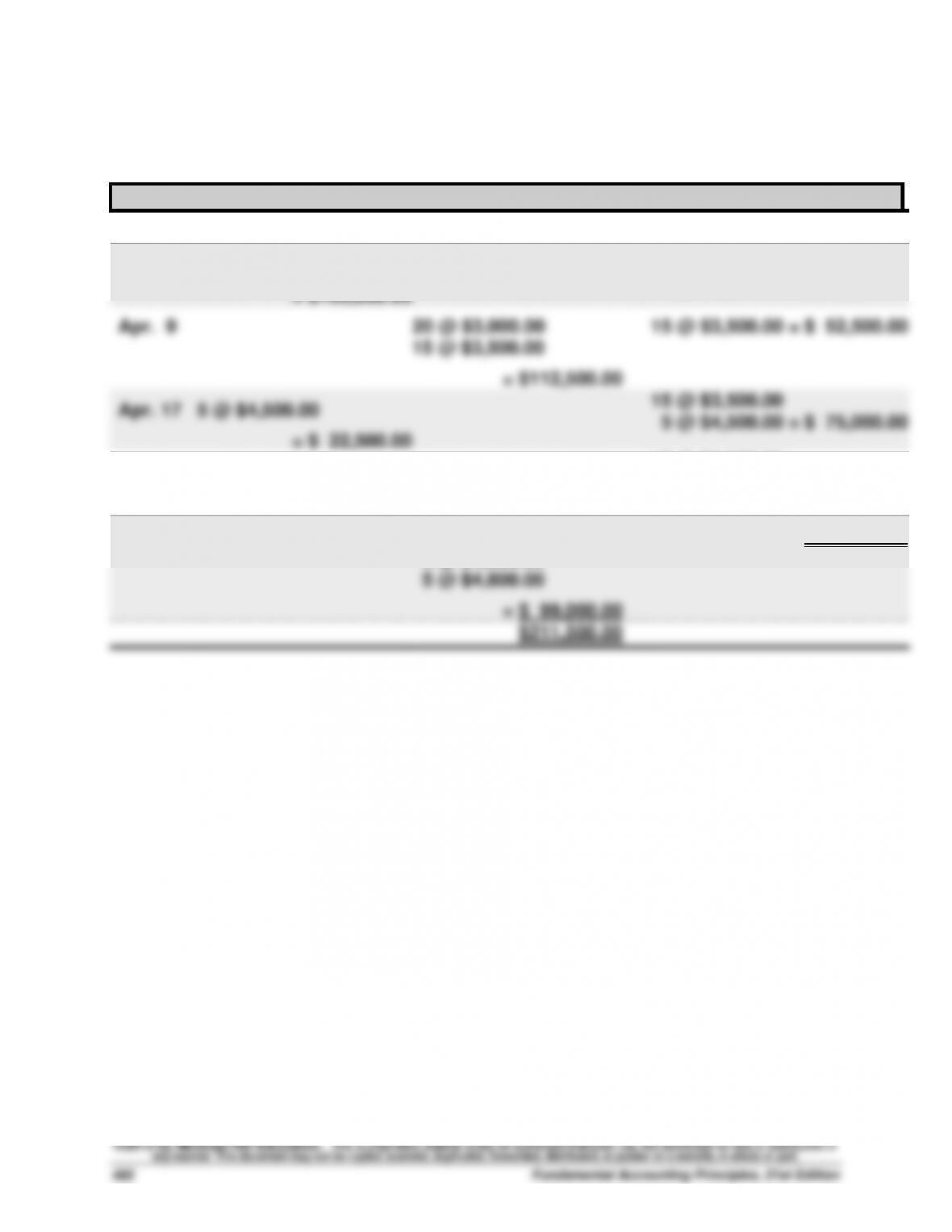

3a. FIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Apr. 1

20 @ $3,000.00 = $ 60,000.00

Apr. 6

30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9

20 @ $3,000.00

15 @ $3,500.00

= $112,500.00

15 @ $3,500.00 = $ 52,500.00

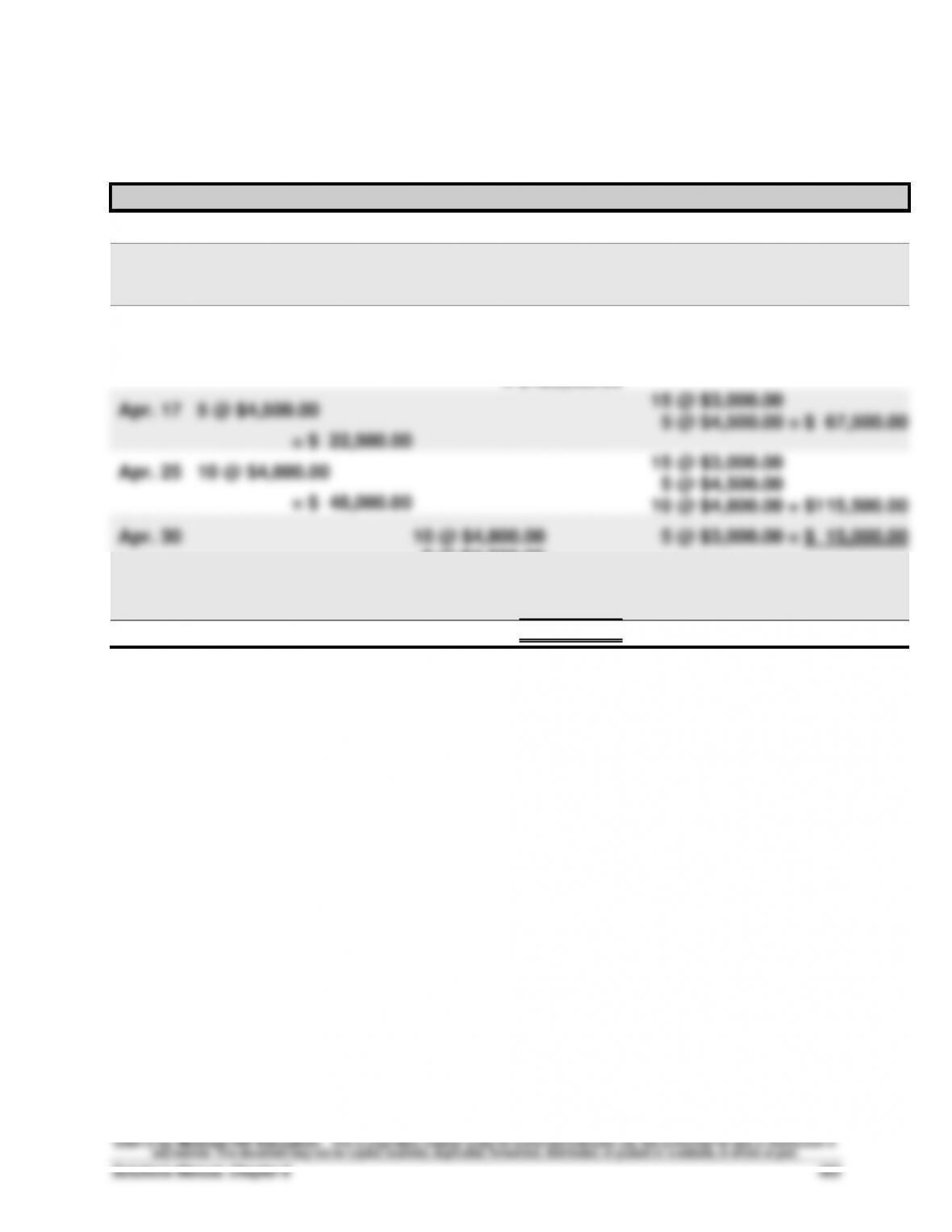

Apr. 17

5 @ $4,500.00

= $ 22,500.00

15 @ $3,500.00

5 @ $4,500.00 = $ 75,000.00

Apr. 25

10 @ $4,800.00

= $ 48,000.00

15 @ $3,500.00

5 @ $4,500.00

10 @ $4,800.00 = $123,000.00

Apr. 30

15 @ $3,500.00

5 @ $4,500.00

5 @ $4,800.00

= $ 99,000.00

5 @ $4,800.00 = $ 24,000.00

$211,500.00

Problem 6-1B (Continued)

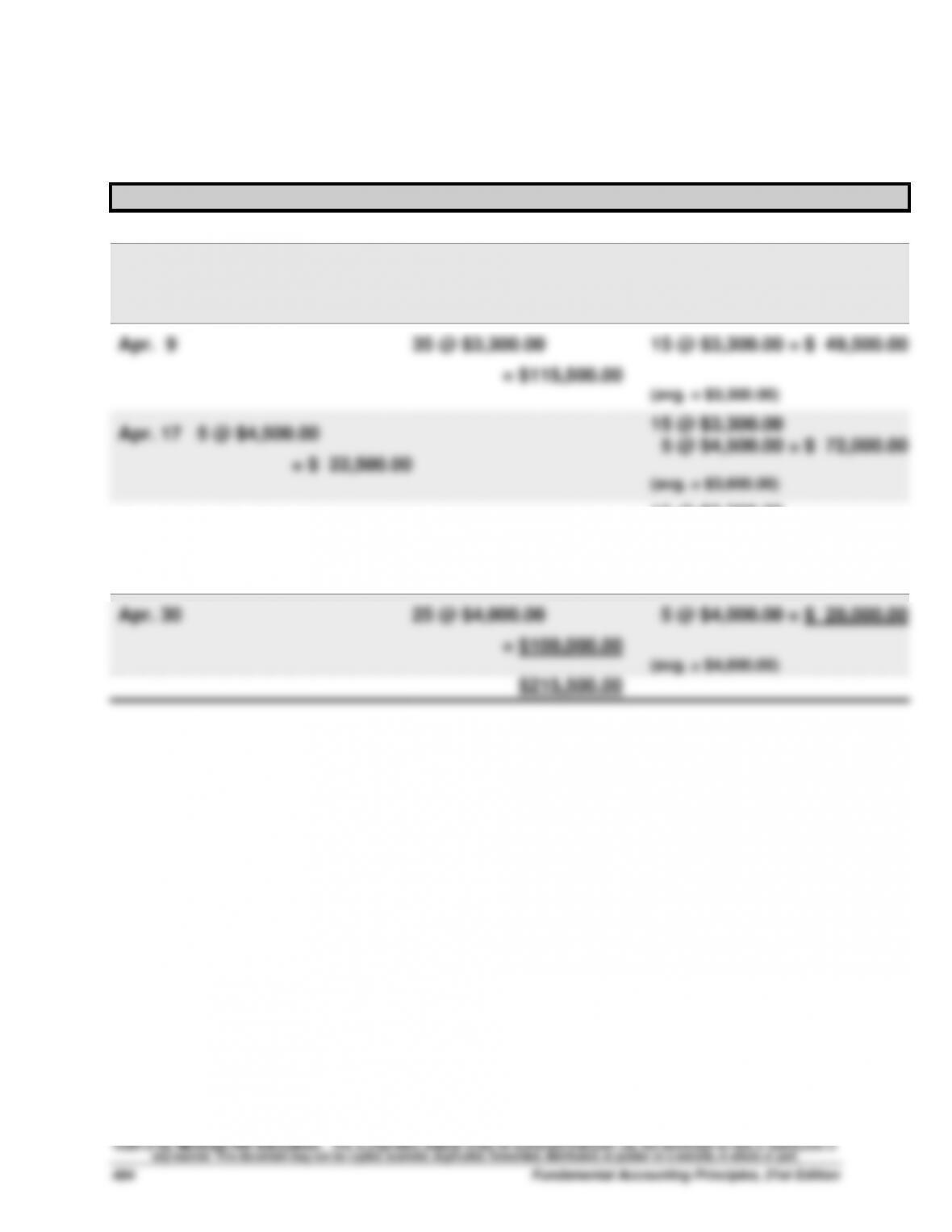

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Apr. 1

20 @ $3,000.00 = $ 60,000.00

Apr. 6

30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9

30 @ $3,500.00

5 @ $3,000.00

= $120,000.00

15 @ $3,000.00 = $ 45,000.00

Apr. 17

5 @ $4,500.00

= $ 22,500.00

15 @ $3,000.00

5 @ $4,500.00 = $ 67,500.00

Apr. 25

10 @ $4,800.00

= $ 48,000.00

15 @ $3,000.00

5 @ $4,500.00

10 @ $4,800.00 = $115,500.00

Apr. 30

10 @ $4,800.00

5 @ $4,500.00

10 @ $3,000.00

= $100,500.00

5 @ $3,000.00 = $ 15,000.00

$220,500.00

Problem 6-1B (Continued)

3c. Weighted Average perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Apr. 1

20 @ $3,000.00 = $ 60,000.00

Apr. 6

30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

(avg. = $3,300.00)

Apr. 9

35 @ $3,300.00

= $115,500.00

15 @ $3,300.00 = $ 49,500.00

(avg. = $3,300.00)

Apr. 17

5 @ $4,500.00

= $ 22,500.00

15 @ $3,300.00

5 @ $4,500.00 = $ 72,000.00

(avg. = $3,600.00)

Apr. 25

10 @ $4,800.00

= $ 48,000.00

15 @ $3,300.00

5 @ $4,500.00

10 @ $4,800.00 = $120,000.00

(avg. = $4,000.00)

Apr. 30

25 @ $4,000.00

= $100,000.00

5 @ $4,000.00 = $ 20,000.00

(avg. = $4,000.00)

$215,500.00

Problem 6-1B (Concluded)

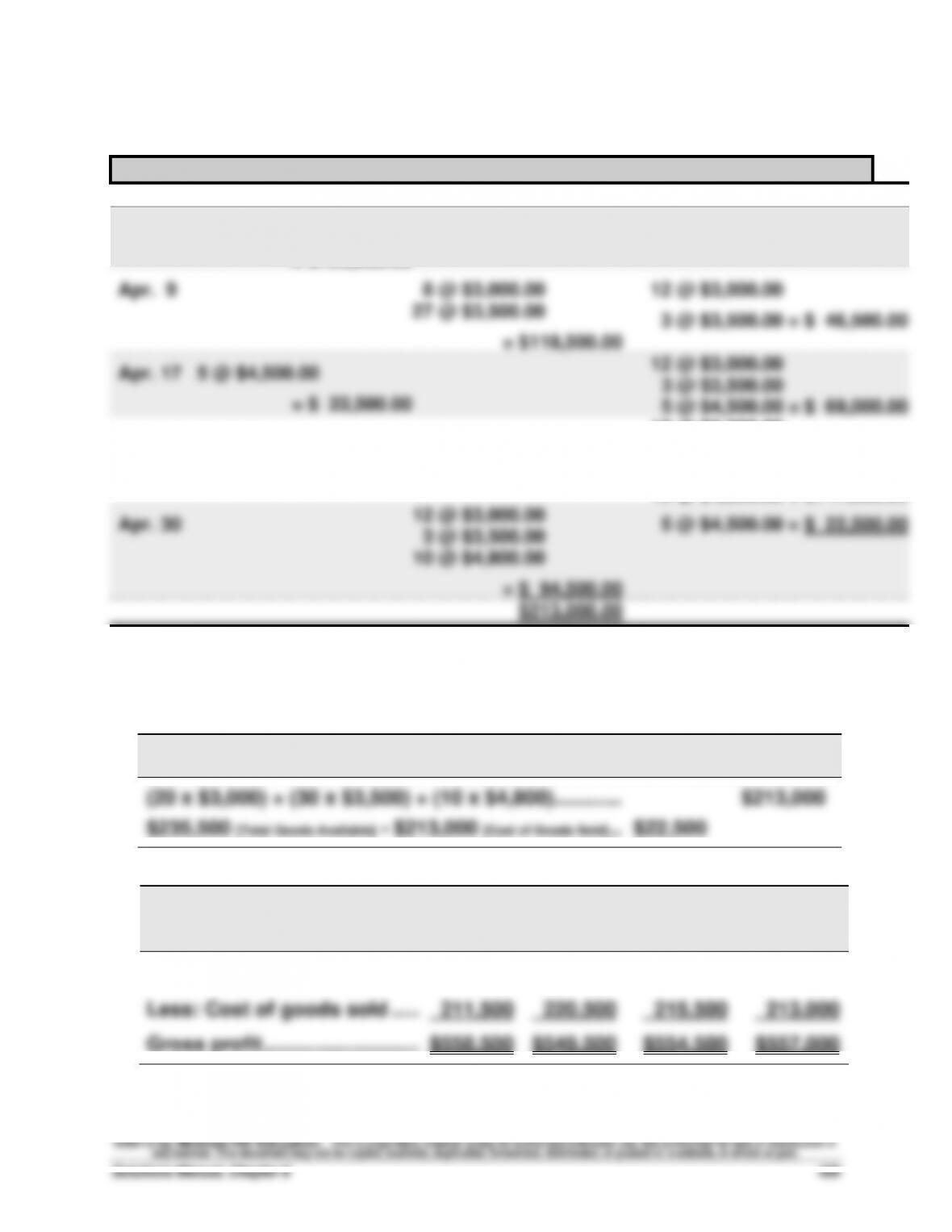

3d. Specific Identification

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Apr. 1

20 @ $3,000.00 = $ 60,000.00

Apr. 6

30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9

8 @ $3,000.00

27 @ $3,500.00

= $118,500.00

12 @ $3,000.00

3 @ $3,500.00 = $ 46,500.00

Apr. 17

5 @ $4,500.00

= $ 22,500.00

12 @ $3,000.00

3 @ $3,500.00

5 @ $4,500.00 = $ 69,000.00

Apr. 25

10 @ $4,800.00

= $ 48,000.00

12 @ $3,000.00

3 @ $3,500.00

5 @ $4,500.00

10 @ $4,800.00 = $117,000.00

Apr. 30

12 @ $3,000.00

3 @ $3,500.00

10 @ $4,800.00

= $ 94,500.00

5 @ $4,500.00 = $ 22,500.00

$213,000.00

Specific identification—Alternative Computation

Cost of goods sold—20 [8+12] units from beginning inventory, 30 [27+3] units from

April 6 purchase, and 10 units from April 25 purchase

Ending Cost of

Specific Identification Inventory Goods Sold

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$770,000

$770,000

$770,000

$770,000

Less: Cost of goods sold …...

211,500

220,500

215,500

213,000

Gross profit ………………………..

$558,500

$549,500

$554,500

$557,000

*Sales = (35 units x $12,000) + (25 units x $14,000) = $770,000