19-1

CHAPTER 19

JOB ORDER COST ACCOUNTING

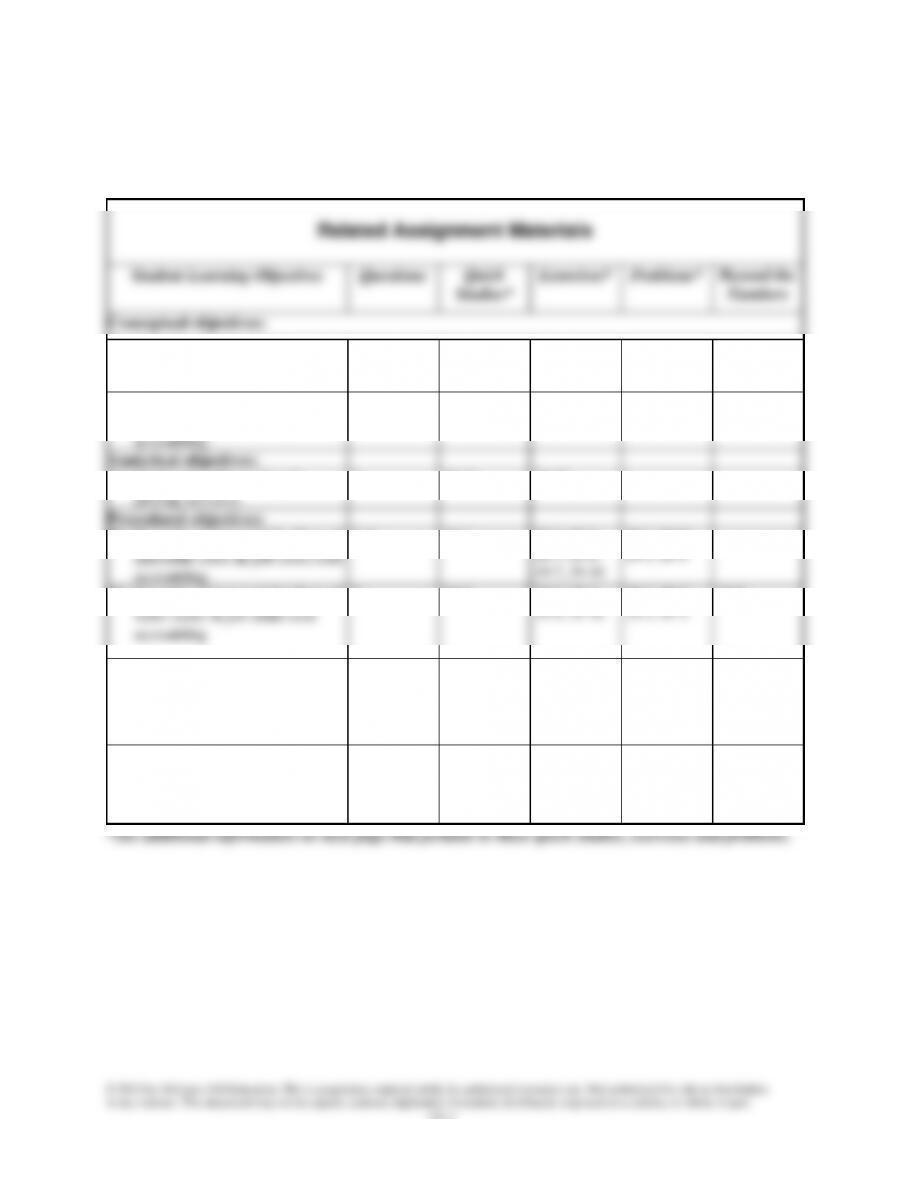

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Describe important features of

job order production.

10, 11, 12, 13

19-1, 19-12

19-1, 19-3,

19-4

19-1, 19–2,

19-4, 19–5,

19-6, 19-7

C2. Explain job cost sheets and how

they are used in job order cost

accounting.

3, 4

19-2, 19-12,

19-13

19-2, 19-4,

19-7

19-1, 19-4

19-4, 19-8

Analytical objectives:

A1 Apply job order costing in

pricing services.

2

19–11

19–17

Procedural objectives:

P1. Describe and record the flow of

materials costs in job order cost

accounting.

5, 6

19-4

19-3, 19–4,

19–7, 19–8,

.19-7, 19–18

19-1, 19–2,

19-3, 19-5

P2. Describe and record the flow of

labor costs in job order cost

accounting

7

19-5

19-3, 19–4,

19-9, 19-16

19-1, 19–2,

19-3, 19-5

19-8

P3. Describe and record the flow of

overhead costs in job order cost

accounting.

1, 2, 8, 11

19-6, 19-7,

19–10

19-3, 19–4,

19-5, 19–6,

19-7, 19–10,

19-13, 19–14,

19-15, 19–16

19-1, 19-2,

19-3, 19–4,

19-5

19-3, 19-8

P4. Determine adjustments for

overapplied and underapplied

factory overhead.

9

19-8, 19-9

19-7, 19–11,

19-12, 19–13,

19–14

19-1, 19–2,

19-4, 19-5

19-8

19-2

Additional Information on Related Assignment Material

Corresponding problems in set B (in text) and set C (on book’s website), also relate to learning

objectives identified in grid on previous page. The Serial Problem for Success Systems continues in this

chapter. Problem 19-4A can be completed using Excel. Problem 19-1A, 19-2A can be completed with

Sage 50 Software.

Connect reproduces assignments online, in static or algorithmic mode, which allows instructors to

monitor, promote, and assess student learning. It can be used for practice, homework, or exams.

Narrated PowerPoint Correlation Guide

Learning Objective

Slides

C1

2-5

C2

6-8

P1

9-14,22,25,37-38

P2

15-17,23,26,38-39

P3

18-20, 26-27, 40-41

P4

28-33

A1

35

Synopsis of Chapter Revision

• Astor and Black: NEW opener with new entrepreneurial assignment

19-3

Chapter Outline

Notes

I. Job Order Cost Accounting

A. Cost accounting system

1. Records manufacturing activities using a perpetual inventory

system.

2. Continuously updates records for costs of materials, goods in

process, and finished goods inventories.

3. Provides timely information about inventories, and

manufacturing costs per unit of product.

4. Two basic types of cost accounting systems are job order cost

accounting and process cost accounting.

B. Job Order Production—producing products or providing services

individually designed to meet the needs of a specific customer

(special orders).

1. The production activities for a customized product is called a

job.

2. A job lot involves producing more than one unit of a unique

product.

C. Events in Job Order Costing

1. Jobs can be initiated by a customer order or management

decision to begin work on job before order (jobs on

speculation).

2. Step 1: Predict the cost to complete the job. Cost depends on

the product design prepared by either the customer or the

producer.

3. Step 2: Negotiate price and decide whether to pursue the job.

Price is determined on a cost-plus basis or producer evaluates

market price and determines a target cost that would allow a

reasonable profit while meeting competitive market price.

4. Step 3: Schedule production of the job. This must meet

materials and labor is applied to the job.

Chapter Outline

Notes

D. Job Cost Sheet—separate record maintained for each job used to

record costs as incurred

1. Classifies costs as direct materials, direct labor, or overhead.

2. Used by managers to monitor costs incurred to date and to

predict and control costs to complete each job.

3. Accumulated job costs are kept in the goods in process

inventory while goods are being produced.

4. Job cost sheets filed for all of the jobs in process make up a

subsidiary ledger controlled by the Goods in Process

Inventory account in the general ledger.

5. Finished job cost sheets—moved from jobs in process file to

finished jobs file (subsidiary ledger controlled by Finished

Goods Inventory) awaiting delivery to customers.

6. As finished jobs are sold, file moves to permanent file

supporting the cost of goods sold.

II. Job Order Cost Flows and Reports

A. Cost Flows and Documents—the three cost components and

documents used to account for them are:

1. Materials Cost Flows and Documents

a. Receiving report—Source document used to record the

quantity and cost of items received. Materials purchased

are used as a debit to Raw Materials Inventory and a credit

to Accounts Payable.

b. Materials ledger cards (or files)—perpetual records that

units are issued for use in production. Serves as the

subsidiary ledger for the Raw Materials Inventory

account.

c. Materials Requisition⎯document identifying the type and

quantity of material needed in production. Job number is

also identified on direct materials requisitions.

Chapter Outline

Notes

2. Labor Cost Flows and Documents

a. Clock cards—used by employees to record hours worked.

Used to determine total labor costs for pay period. This

amount is debited to Factory Payroll account and credited

to Cash.

b. Time tickets—indicate how much time employees spent

on each job. Used to assign (direct) labor costs to specific

jobs and (indirect) to overhead. Direct labor costs are

debited to Goods in Process Inventory and credited to

Factory Payroll.

c. Job Cost Sheets—accumulates the cost of direct labor

(from time tickets and related entry) as these costs are

incurred.

d. Indirect labor card in Factory Overhead Ledger—

accumulates indirect labor costs (from time tickets and

related entry). Entry to record indirect labor costs debits

Factory Overhead and credits Factory Payroll.

(Estimated overhead costs divided by estimated factor

costs).

f. Recording Overhead Costs—debited Factory Overhead;

account credited varies by overhead element and action at

point the cost is incurred.

19-6

Chapter Outline

Notes

4. Summary of Cost Flows—Summary journal entries are used

to record cost flows as follows:

a. Into (debit) Raw Materials Inventory as acquired.

b. From (credit) Raw Materials Inventory to (debit) Goods In

Process Inventory (direct materials) and (debit) Factory

Overhead (indirect materials) as good are requisitioned.

Direct material costs also accumulated on Job Cost Sheets.

c. Into (debit) Factory Payroll as labor is incurred.

d. From (credit) Factory Payroll to (debit) Goods In Process

Inventory (direct labor) and (debit) Factory Overhead

(indirect labor) as labor costs are analyzed. Direct labor

costs also accumulated on Job Cost Sheets.

incurred during the period based on bills received.

2. The credit side shows the amount applied during the period

that was an estimate based on the predetermined overhead

rate.

applied than incurred; an overapplied FOH amount.

B. Underapplied and Overapplied Overhead

1. Factory Overhead debit balance (underapplied amount) is

2. Factory Overhead credit balance (overapplied amount) is

debited (closed) and credited to Cost of Goods Sold.

19-7

Chapter Outline

Notes

IV. Decision Analysis—Pricing for Services

A. Job order costing concepts and procedures are applicable to a

service setting.

B. Procedure to determine:

1. Determine direct labor costs

2. Determine the overhead based on predetermined rate(s).

3. Combine labor and overhead to obtain cost of job. Note:

service firms do not have material costs or inventory.

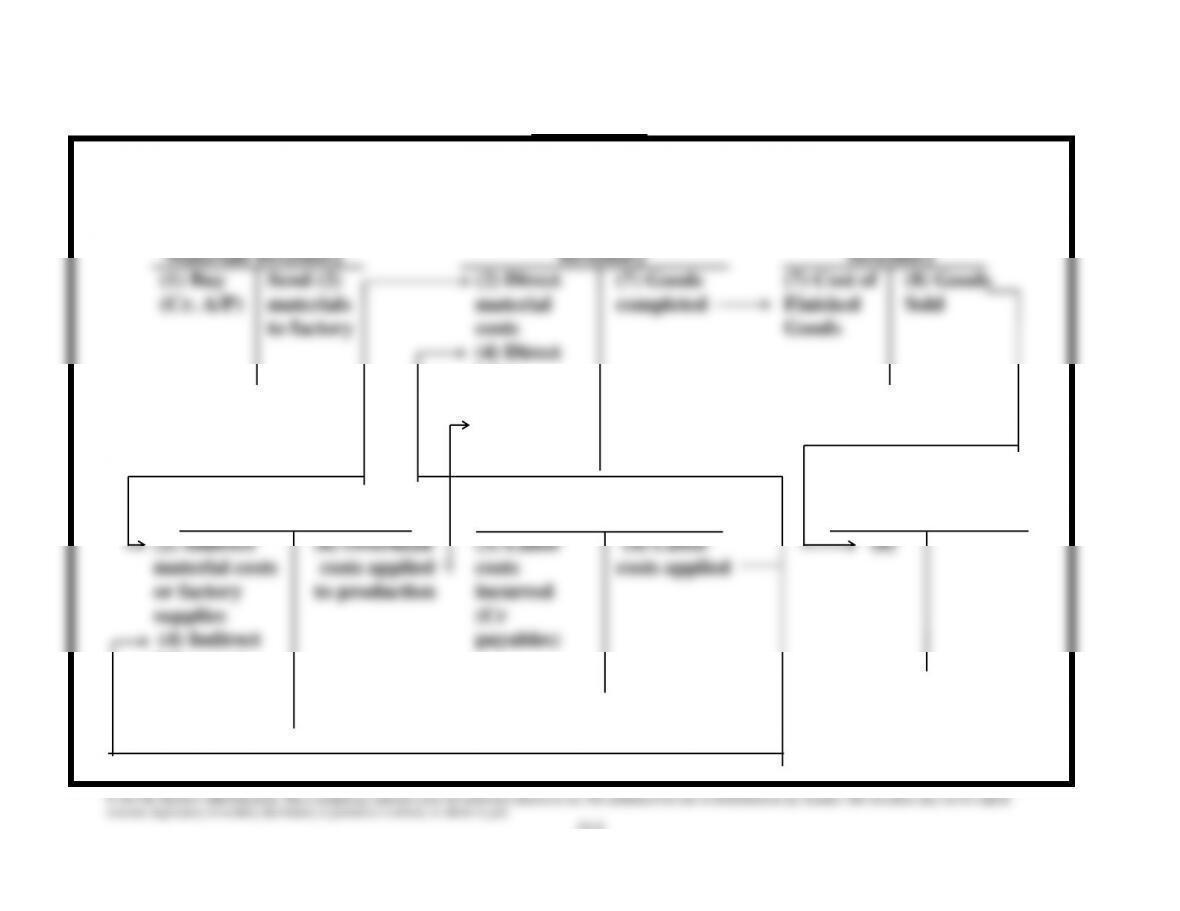

VISUAL #19-1

Tracing Product Costs

Through a Cost Accounting System

Work in Progress Finished Goods

labor

costs

(6) Overhead

costs

Factory Overhead Factory Payroll Cost of Goods Sold

labor costs

(5) Other

factory OH

costs incurred (Cr varies)

19-9

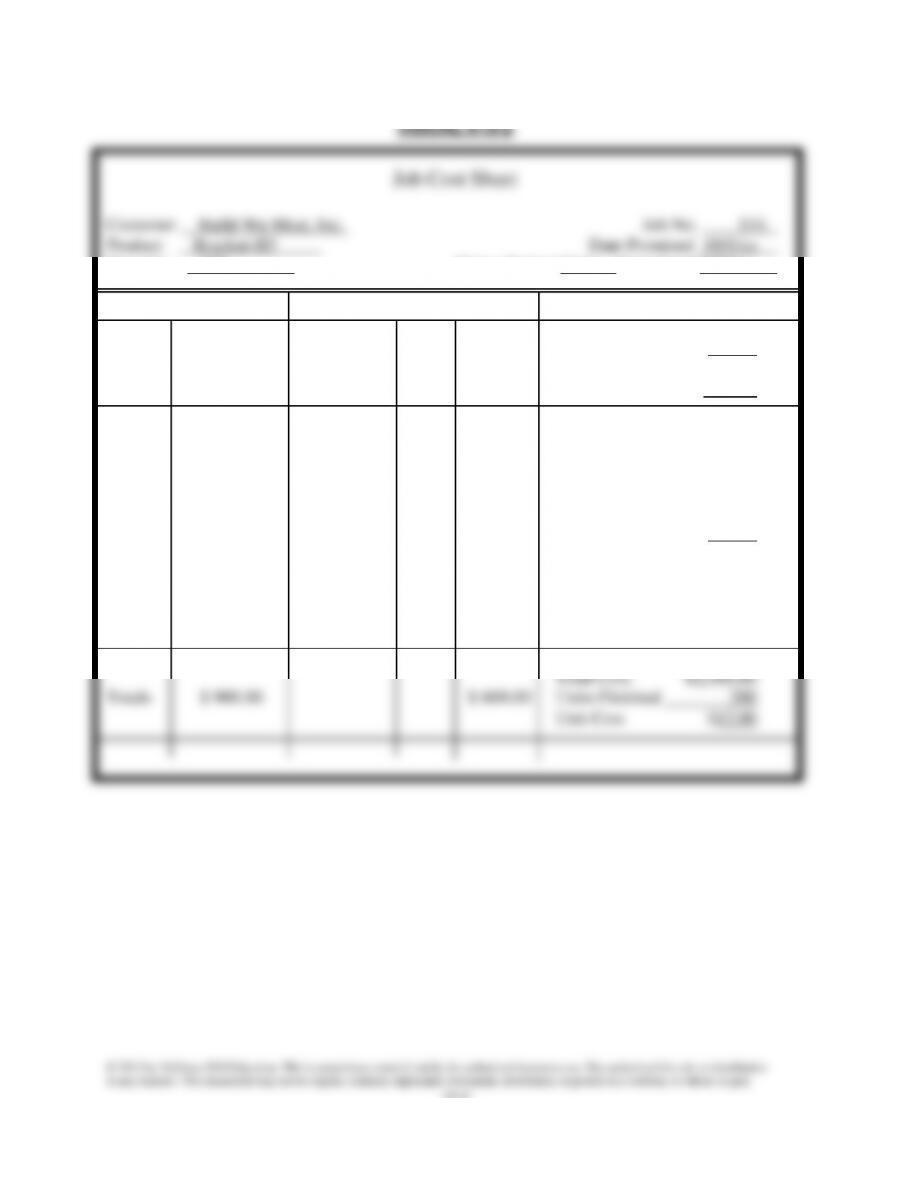

Quantity 200 Dates: Started 9/1/xx Completed 9/20/xx

Direct Material Direct Labor Cost Summary

Mat’l. Payroll Direct Material $ 900.00

Req’n. Summary

No. Amount Dated Dept. Amount Direct Labor 600.00

667 $ 340.00 9/2 A $ 70.00

673 180.00 9/9 A 240.00 Factory Overhead

691 200.00 9/16 B 190.00 (applied at):

623 180.00 9/23 B 100.00

150% of direct

labor cost 900.00

19-10

Alternate Demo Problem Nineteen

The following information was taken from the accounting records of the

Superior Company:

Depreciation of equipment ………………………………………………

$ 70,000

Direct labor …………………………………………………………………….

120,000

Factory taxes ………………………………………………………………….

2,000

Goods in process inventory, Dec. 31, 2013 ………………………

250,000

Indirect labor …………………………………………………………………..

10,000

Power ……………………………………………………………………………..

16,000

Raw materials inventory, Dec. 31, 20113 ………………………….

60,000

Raw materials purchases, for year …………………………………..

230,000

Goods in process inventory, January 1, 2013 …………………..

302,000

Raw materials inventory, January 1, 2013 ………………………..

110,000

Required:

Prepare a manufacturing statement for the Superior Company for 2013.

19-11

Solution: Alternate Demo Problem Nineteen

SUPERIOR MANUFACTURING COMPANY

Manufacturing Statement

For Year Ended December 31, 2013

Direct materials:

Raw materials inventory, 1/1/13 ……………………..

$110,000

Raw materials purchases ………………………………

230,000

Raw materials available for use ……………………..

340,000

Raw materials inventory, 12/31/13 ………………….

60,000

Direct materials used …………………………………….

$280,000

Direct labor …………………………………………………..

120,000

Factory overhead costs: ………………………………..

Indirect labor …………………………………………………

10,000

Power ……………………………………………………………

16,000

Factory taxes ………………………………………………..

2,000

Depreciation of equipment …………………………….

70,000

Total factory overhead costs …………………………

98,000

Total manufacturing costs …………………………….

498,000

Goods in process inventory, 1/1/13 ………………..

302,000

Total goods in process during the year ………….

800,000

Goods in process inventory, 12/31/13 …………….

250,000

Cost of goods manufactured …………………………

$550,000