Problem 15-6AA (60 minutes)

Part 1

2013

Apr. 8

Cash …………………………………………………………..………………….

5,938

Sales …………………………………………………….…

5,938

July 21

Accounts Receivable⎯Sumito …………………….…….

14,100

Sales …………………………………………………….…

14,100

(1,500,000 yen x $0.0094/yen)

Oct. 14

Accounts Receivable⎯Smithers …………………………..

27,675

Sales …………………………………………………….…

27,675

(19,000£ x $1.4566/£)

Nov. 18

Cash …………………………………………………………..………………….

13,800

Foreign Exchange Loss ………………………………………………….

300

Accounts Receivable⎯Sumito ……………….………….

14,100

(1,500,000 yen x $0.0092/yen)

Dec. 20

Accounts Receivable⎯Hamid Albar …………….…………….

7,652

Sales …………………………………………………….…

7,652

(17,000 ringgits x $0.4501/ringgits)

Dec. 31

Accounts Receivable⎯Smithers. ………………..…………

103

Foreign Exchange Gain * ……………………….….

103

*Original measure = (19,000£ x $1.4566/£) = $27,675

Year-end measure = (19,000£ x $1.4620/£) = 27,778

Gain for the period ……………………… = $ 103

Dec. 31

Foreign Exchange Loss* ……………………………..………………….

77

Accounts Receivable⎯Hamid Albar ……….………………….

77

*Original measure = (17,000 ringgits x $0.4501/ ringgits) = $7,652

Year-end measure = (17,000 ringgits x $0.4456/ ringgits) = 7,575

Loss for the period ……………………………………… = $ 77

2014

Jan. 12

Cash* ………………………………………………………….………………….

27,928

Accounts Receivable⎯Smithers** ………….……………….

27,778

Foreign Exchange Gain …………………………..

150

*(19,000£ x $1.4699/£) **($27,675 + $103)

Jan. 19

Cash* ………………………………………………………….………………….

7,514

Foreign Exchange Loss ………………………………………………….

61

Accounts Receivable⎯Hamid Albar** …….………………….

7,575

*(17,000 ringgits x $0.4420/ ringgits) **($7,652 – $77)

Fundamental Accounting Principles, 21st Edition

896

Problem 15-6AA (Continued)

Part 2

Foreign exchange loss reported on the 2013 income statement

November 18 ………………………………...

$(300)

December 31………………………………….

103

December 31………………………………….

(77)

Total ……………………………………………...

$(274)

Part 3

To reduce the risk of foreign exchange gain or loss, Doering could attempt

to negotiate foreign customer sales that are denominated in U.S. dollars.

PROBLEM SET B

Problem 15-1B (60 minutes)

Part 1

2013

Mar. 10

Short-Term Investments—Trading (AOL) ………….

143,505

Cash …………………………………………………….

143,505

Purchased AOL shares

[(2,400 x $59.15) + $1,545].

May 7

Short-Term Investments—Trading (MTV) ………

184,105

Cash …………………………………………………….

184,105

Purchased MTV shares

[(5,000 x $36.25) + $2,855].

Sept. 1

Short-Term Investments—Trading (UPS) ………

69,950

Cash …………………………………………………….

69,950

Purchased UPS shares

[(1,200 x $57.25) + $1,250].

2014

Apr. 26

Cash ………………………………………………………….

170,450

Loss on Sale of Short-Term Investments …….

13,655

Short-Term Investments—Trading (MTV) …

184,105

Sold MTV shares [(5,000 x $34.50) – $2,050].

27

Cash ………………………………………………………….

70,812

Gain on Sale of Short-Term Investments .

862

Short-Term Investments—Trading (UPS) …

69,950

Sold UPS shares [(1,200 x $60.50) – $1,788].

June 2

Short-Term Investments—Trading (SPW) …………

622,450

Cash …………………………………………………….

622,450

Purchased SPW shares

[(3,600 x $172.00) + $3,250].

14

Short-Term Investments—Trading (W-M) ………

46,307

Cash …………………………………………………….

46,307

Purchased Wal-Mart shares

[(900 x $50.25) + $1,082].

Fundamental Accounting Principles, 21st Edition

898

Problem 15-1B (Concluded)

2015

Jan. 28

Short-Term Investments—Trading (Pepsi) …..…

88,890

Cash …………………………………………………..…

88,890

Purchased PepsiCo shares

[(2,000 x $43.00) + $2,890].

31

Cash ………………………………………………………..…

602,760

Loss on Sale of Short-Term Investments …..…

19,690

Short-Term Investments—Trading (SPW) ……

622,450

Sold SPW shares [(3,600 x $168) – $2,040].

Aug. 22

Cash ………………………………………………………..…

133,720

Loss on Sale of S-T Investments ……………….…

9,785

Short-Term Investments—Trading (AOL) ……

143,505

Sold AOL shares [(2,400 x $56.75) – $2,480].

Sept. 3

Short-Term Investments—Trading (Voda) ………

62,430

Cash …………………………………………………..…

62,430

Purchased Vodaphone shares

[(1,500 x $40.50) + $1,680].

Oct. 9

Cash ………………………………………………………..…

47,155

Gain on Sale of Short-Term Investments …..…

848

Short-Term Investments—Trading (W-M) …..…

46,307

Sold Wal-Mart shares

[(900 x $53.75) – $1,220].

Part 2 (Adjusting entry at December 31, 2015)

Dec. 31

Unrealized Loss—Income ………………………………..

13,820

Fair Value Adjustment—Trading* …………..

13,820

To reflect an unrealized loss in fair values of

trading securities.

* Fair value adjustment computations

Trading Securities’

Portfolio

Shares

Price at

12/31/15

Fair

Value

Cost

Unrealized

Gain (Loss)

PepsiCo …………….………..

2,000

$41.00

$ 82,000

$ 88,890

$ (6,890)

Vodaphone …………………..

1,500

$37.00

55,500

62,430

(6,930)

Totals ……………….………..

$137,500

$151,320

$(13,820)

Problem 15-2B (40 minutes)

Part 1

Feb. 6

Short-Term Investments—AFS (Nokia)………...

143,250

Cash …………………………………………………...

143,250

Purchased 3,400 shares of Nokia

[(3,400 x $41.25) + $3,000].

15

Short-Term Investments—AFS (T-bills) ………..

20,000

Cash …………………………………………………...

20,000

Purchased U.S. Treasury bills.

Apr. 7

Short-Term Investments—AFS (Dell) …………..

48,655

Cash …………………………………………………...

48,655

Purchased 1,200 shares of Dell

[(1,200 x $39.50) + $1,255].

June 2

Short-Term Investments—AFS (Merck) ………..

184,140

Cash …………………………………………………...

184,140

Purchased 2,500 shares of Merck

[(2,500 x $72.50) + $2,890].

30

Cash ………………………………………………………….

646

Dividend Revenue …………………………………..

646

Received dividends on Nokia stock

(3,400 x $0.19).

Aug. 11

Cash* ……………………………………………………….

38,050

Gain on Sale of Short-Term Investments ….

2,237

Short-Term Investments—AFS (Nokia)** ….

35,813

Sold 850 shares of Nokia. (rounded)

* [(850 x $46.00) – $1,050] **($143,250 x 850/3,400)

16

Cash ………………………………………………………...

20,600

Short-Term Investments—AFS (T-bills) ……..

20,000

Interest Revenue* …………………………………...

600

Proceeds of U.S. Treasury bills.

*($20,000 x .06 x 6/12)

24

Cash ………………………………………………………...

120

Dividend Revenue …………………………………..

120

Received dividends on Dell stock (1,200 x $0.10).

Nov. 9

Cash ………………………………………………………….

510

Dividend Revenue …………………………………..

510

Received dividends on Nokia stock

(2,550 x $0.20).

Dec. 18

Cash ………………………………………………………….

180

Dividend Revenue …………………………………..

180

Received dividends on Dell stock (1,200 x $0.15).

Fundamental Accounting Principles, 21st Edition

900

Problem 15-2B (Concluded)

Part 2

Comparison of Cost and Fair Values of AFS Portfolio

Unrealized

Cost Fair Value Gain (Loss)

Nokia (2,550 x $41.25) + $2,250a ……… $107,437

2,550 x $40.25 (rounded) ……… $102,638

Dell (1,200 x $39.50) + $1,255b ……… 48,655

1,200 x $40.50 ……………………. 48,600

Part 3

Dec. 31

Unrealized Loss—Equity ……………………………………..

41,494

Fair Value Adjustment—AFS (ST) ……………….

41,494

To reflect an unrealized loss in fair values of

available-for-sale securities.

Part 4

The balance sheet would report the cost of these short-term investments in

available-for-sale securities at $340,232 and show a subtraction of $41,494

Part 5

(a) Income statement

(i) Interest Revenue, $600

(ii) Dividend Revenue, $1,456 [$646 + $120 + $510 + $180]

Problem 15-3B (60 minutes)

Part 1

2013

Mar. 10

Long-Term Investments—AFS (Apple) …………………………..

31,400

Cash ……………………………………………………….

31,400

Purchased Apple shares

[(1,200 x $25.50) + $800].

April 7

Long-Term Investments—AFS (Ford) ……………..……………

57,283

Cash ……………………………………………………….

57,283

Purchased Ford shares

[(2,500 x $22.50) + $1,033].

Sept. 1

Long-Term Investments—AFS (Polaroid) ………..………………..

29,090

Cash ……………………………………………………….

29,090

Purchased Polaroid shares

[(600 x $47.00) + $890].

Dec. 31

Unrealized Loss—Equity ……………………………….………………..

2,873

Fair Value Adjustment—AFS (LT)* …………………………..

2,873

Annual adjustment to fair values.

*

Cost _

Fair Value

Apple …………..…….

$ 31,400

$ 33,000

Ford …………….…….

57,283

52,500

Polaroid ……….…….

29,090

29,400

Total…………….…….

$117,773

$114,900

Apple: 1,200 x $27.50 = $33,000

Ford: 2,500 x $21.00 = 52,500

Polaroid: 600 x $49.00 = 29,400

$117,773 – $114,900 = $2,873

Fundamental Accounting Principles, 21st Edition

902

Problem 15-3B (Continued)

2014

Apr. 26

Cash ………………………………………………………………………………

50,043

Loss on Sale of Investments ……………………..……

7,240

Long-Term Investments—AFS (Ford) …….……………………

57,283

Sold Ford shares

[(2,500 x $20.50) – $1,207].

June 2

Long-Term Investments—AFS (Duracell) ……..……………………

35,700

Cash ……………………………………………………….

35,700

Purchased Duracell shares

[(1,800 x $19.25) + $1,050].

June 14

Long-Term Investments—AFS (Sears) …………………………..

25,480

Cash …………………………………………………..…..

25,480

Purchased Sears shares

[(1,200 x $21.00) + $280].

Nov. 27

Cash ………………………………………………………..……………………

29,755

Gain on Sale of Investments ………………..…………

665

Long-Term Investments—AFS (Polaroid) ………………………

29,090

Sold Polaroid shares

[600 x $51.00) – $845].

Dec. 31

Fair Value Adjustment—AFS (LT)* …………………………..

5,093

Unrealized Loss—Equity …………………………..

2,873

Unrealized Gain—Equity ……………………….….

2,220

Annual adjustment to fair values.

*

Cost _

Fair Value

Apple ………..

$31,400

$34,800

Duracell …….

35,700

32,400

Sears ………..

25,480

27,600

Total …………

$92,580

$94,800

Apple: 1,200 x $29.00 = $34,800

Duracell: 1,800 x $18.00 = $32,400

Sears: 1,200 x $23.00 = $27,600

$92,580 – $94,800 = $2,220

Fair Value Adjustment account:

Required balance ….. $2,220 Dr.

Unadjusted balance.. 2,873 Cr.

Required change …… $5,093 Dr.

Problem 15-3B (Continued)

2015

Jan. 28

Long-Term Investments—AFS (Coca-Cola) ……..………………..

41,480

Cash ……………………………………………………….

41,480

Purchased Coca-Cola shares

[(1,000 x $40.00) + $1,480].

Aug. 22

Cash ……………………………………………………………………………..

23,950

Loss on Sale of Investments …………………………..

7,450

Long-Term Investments—AFS (Apple) ………………………..

31,400

Sold Apple shares [(1,200 x $21.50) – $1,850].

Sept. 3

Long-Term Investments—AFS (Motorola) ………..………………..

84,780

Cash ……………………………………………………….

84,780

Purchased Motorola shares

[(3,000 x $28) + $780].

Oct. 9

Cash ……………………………………………………………………………..

28,201

Gain on Sale of Investments …………………..………

2,721

Long-Term Investments—AFS (Sears) ……….………………..

25,480

Sold Sears shares [(1,200 x $24.00) – $599].

Oct. 31

Cash ……………………………………………………………………………..

26,102

Loss on Sale of Investments ………………………..…

9,598

Long-Term Investments—AFS (Duracell) ……………………..

35,700

Sold Duracell shares [(1,800 x $15.00) – $898].

Dec. 31

Unrealized Gain⎯Equity ……………………………….………………..

2,220

Unrealized Loss⎯Equity ………………………………………………..

6,260

Fair Value Adjustment—AFS (LT)* ……………..……………

8,480

Annual adjustment to fair values.

*

Cost _

Fair Value

Coca-Cola …………………...

$ 41,480

$ 48,000

Motorola ……………………...

84,780

72,000

Total…………………………….

$126,260

$120,000

Coca-Cola: 1,000 x $48.00 = $48,000

Motorola: 3,000 x $24.00 = $72,000

$126,260 – $120,000 = $6,260

Fair Value Adjustment account:

Required balance …… $6,260 Cr.

Unadjusted balance .. 2,220 Dr.

Required change ……. $8,480 Cr.

Fundamental Accounting Principles, 21st Edition

904

Problem 15-3B (Concluded)

Part 2

12/31/2013

12/31/2014

12/31/2015

Long-Term AFS Securities (cost)…………...

$117,773

$92,580

$126,260

Fair Value Adjustment ……………………...

(2,873)

2,220

(6,260)

Long-Term AFS Securities (fair value) …...

$114,900

$94,800

$120,000

Part 3

2013

2014

2015

Realized gains (losses)

Sale of Ford shares ………………………….

$(7,240)

Sale of Polaroid shares …………………….

665

Sale of Duracell shares …………………….

$ (9,598)

Sale of Apple shares ………………………..

(7,450)

Sale of Sears shares ………………………..

______

______

2,721

Total realized gain (loss) ……………………

$ 0

$(6,575)

$(14,327)

Unrealized gains (losses) at year–end …

$(2,873)

$ 2,220

$ (6,260)

Problem 15-4B (40 minutes)

Part 1

Available–for-sale securities on December 31, 2013

Security

Cost

Fair Value

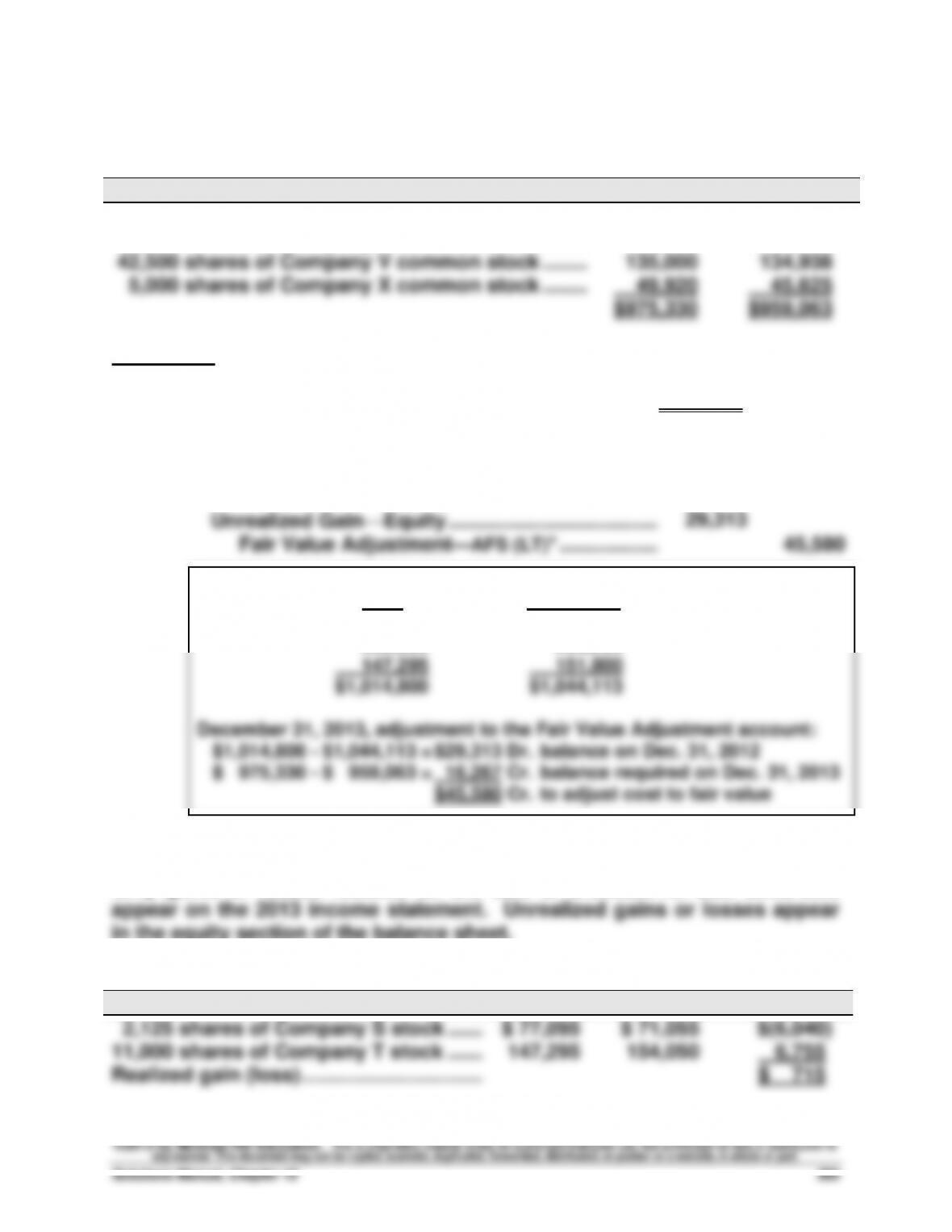

27,500 shares of Company R common stock ……..…..

$559,125

$568,125

6,375 shares of Company S common stock ……..…..

231,285

210,375

42,500 shares of Company V common stock ……..…..

135,000

134,938

5,000 shares of Company X common stock ……..…..

49,920

45,625

$975,330

$959,063

Disclosure

The portfolio of available–for-sale securities would be reported on the

December 31, 2013, balance sheet at its fair fair value of $959,063.

Part 2

Dec. 31

Unrealized Loss⎯Equity ……………………………….……………….

16,267

Unrealized Gain⎯Equity ………………………………..……………….

29,313

Fair Value Adjustment—AFS (LT)* …………………………..

45,580

*December 31, 2012, available-for-sale securities:

Cost

Fair Value

$ 559,125

$ 599,063

308,380

293,250

147,295

151,800

$1,014,800

$1,044,113

December 31, 2013, adjustment to the Fair Value Adjustment account:

$1,014,800 – $1,044,113 = $29,313 Dr. balance on Dec. 31, 2012

$ 975,330 – $ 959,063 = 16,267 Cr. balance required on Dec. 31, 2013

$45,580 Cr. to adjust cost to fair value

Part 3

Only gains or losses realized on the sale of available-for-sale securities

in the equity section of the balance sheet.

Year 2013 realized gain (loss)

Stock Sold

Cost

Sale

Gain (Loss)

2,125 shares of Company S stock ……..

$ 77,095

$ 71,055

$(6,040)

11,000 shares of Company T stock ……..

147,295

154,050

6,755

Realized gain (loss) …………………………….

$ 715

Fundamental Accounting Principles, 21st Edition

906

Problem 15-5B (50 minutes)

Part 1

1. Journal entries (assuming significant influence)

2013

Jan. 5

Long-Term Investments—Bloch ………………..…………

200,500

Cash ……………………………………………………….

200,500

Purchased Bloch shares.

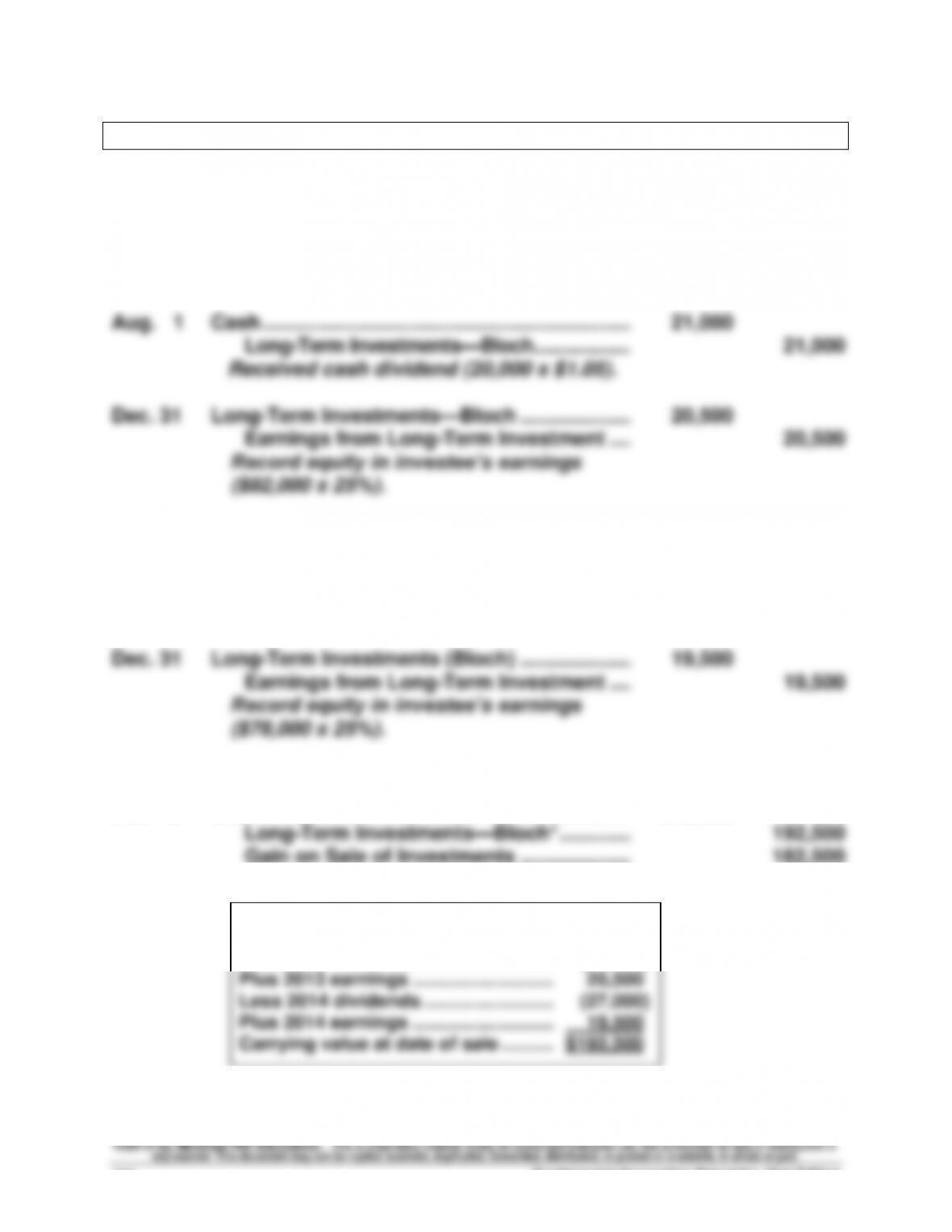

Aug. 1

Cash ………………………………………………………………………………

21,000

Long–Term Investments—Bloch ……………….………….

21,000

Received cash dividend (20,000 x $1.05).

Dec. 31

Long-Term Investments—Bloch ………………..…………

20,500

Earnings from Long-Term Investment ….……………………

20,500

Record equity in investee’s earnings

($82,000 x 25%).

2014

Aug. 1

Cash ………………………………………………………………………………

27,000

Long-Term Investments—Bloch …………..………………

27,000

Record cash dividend (20,000 x $1.35).

Dec. 31

Long-Term Investments (Bloch) ………………..…………

19,500

Earnings from Long-Term Investment ….……………………

19,500

Record equity in investee’s earnings

($78,000 x 25%).

2015

Jan. 8

Cash ………………………………………………………………………………

375,000

Long-Term Investments—Bloch* ………….……………….

192,500

Gain on Sale of Investments ………………..…………

182,500

Sold Bloch shares.

*Investment carrying value at Jan. 7, 2015

Original cost ………………………………..….

$200,500

Less 2013 dividends …………………….….

(21,000)

Plus 2013 earnings ………………………….

20,500

Less 2014 dividends …………………….….

(27,000)

Plus 2014 earnings ………………………….

19,500

Carrying value at date of sale ……….….

$192,500

Problem 15-5B (Continued)

2. Carrying value per share (see computations in part 1)

3. Change in Brinkley’s equity

Earnings from Bloch-2013 …………………………..

$ 20,500

Earnings from Bloch-2014 …………………………..

19,500

Gain on sale of investments ………………………….

182,500

Net increase ……………………………………………..….

$222,500

Part 2

1. Journal entries (assuming NO significant influence)

2013

Jan. 5

Long-Term Investments—AFS (Bloch) ……….………………….

200,500

Cash ……………………………………………………….

200,500

Purchased Bloch shares.

Aug. 1

Cash ………………………………………………………………………………

21,000

Dividend Revenue ……………………………….……………………

21,000

Received cash dividend (20,000 x $1.05).

Dec. 31

Fair Value Adjustment—AFS (LT)* ……………..……………

37,500

Unrealized Gain—Equity …………………………..

37,500

Record fair value adjustment.

*20,000 x $11.90 = $238,000

$238,000 – $200,500 = $37,500