Problem 25-5A (55 minutes)

Part 1

Product G

Product B

Selling price per unit …………………………………………..…

$120

$160

Variable costs per unit ………………………………………..…

40

90

Contribution margin per unit ……………………………….…

$ 80

$ 70

Machine hours to produce 1 unit …………………………..

0.4

1.0

Contribution per machine hour

(or contribution/[hours per unit]) …………………………

$200

$ 70

Part 2

Sales Mix Recommendation. To the extent allowed by production and

market constraints, the company should produce as much of Product G as

possible. With a single shift yielding 176 hours per month (8 x 22), the

company can produce these units of Product G:

Contribution Margin at Recommended Sales Mix

Problem 25-5A (Continued)

Part 3

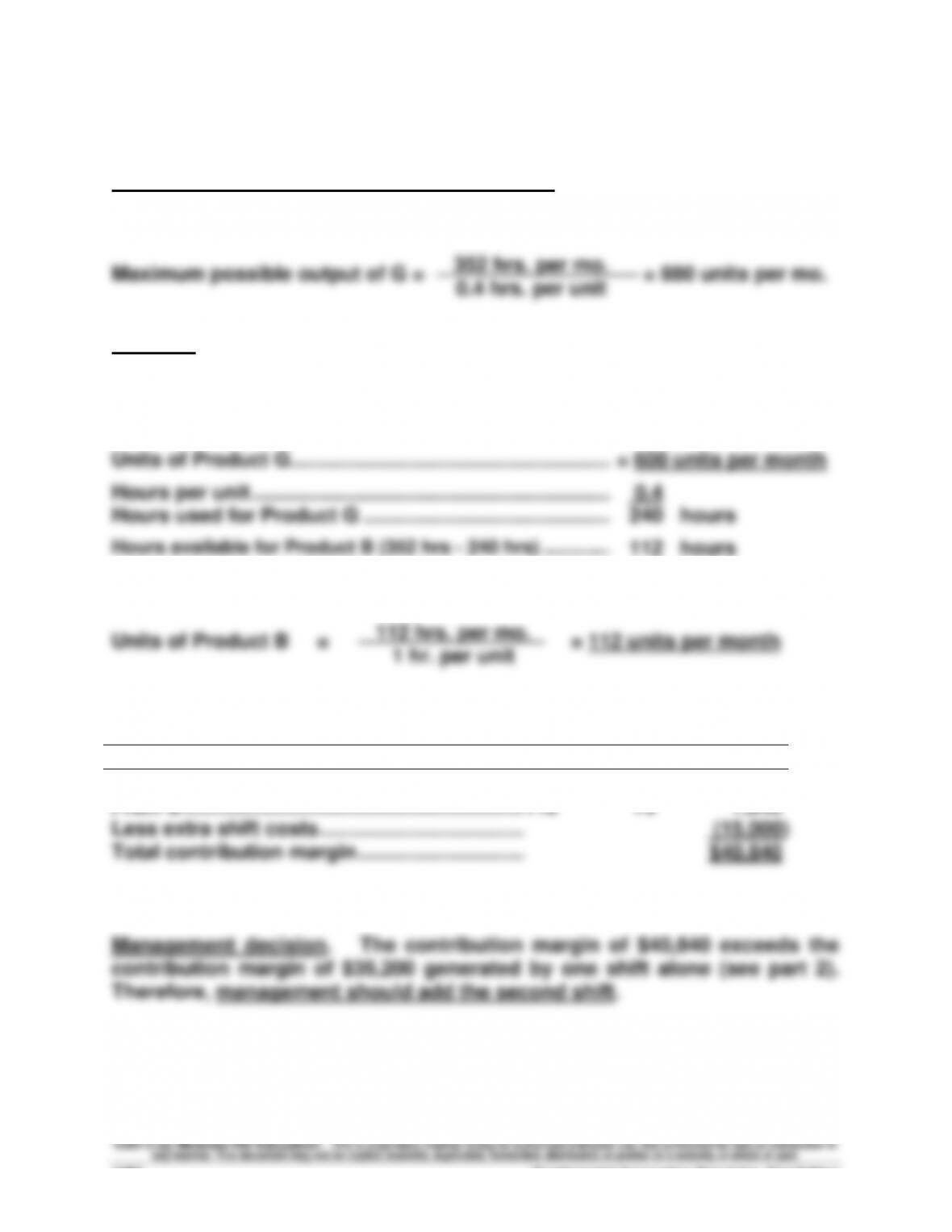

Sales Mix Recommendation with Second Shift. If the second shift is added,

the maximum possible output of G will double

However, this level of output exceeds the company’s market constraint of

600 units of G per month. This means the company should produce 600

units of Product G, and commit the remainder of the productive capacity to

Product B. This is computed as follows

Units of Product G ………………………………………………………

= 600 units per month

Hours per unit ……………………………………………………….

0.4

Hours used for Product G ……………………………………..……

240

hours

Hours available for Product B (352 hrs – 240 hrs) ………….……

112

hours

The output of Product B with 112 production hours is

Contribution Margin at This Sales Mix

Units

Contr./unit

Total

From G …………………………………………………….…

600

$80

$48,000

From B …………………………………………………….…

112

70

7,840

Less extra shift costs ……………………………….…..

(15,000)

Total contribution margin …………………………..

$40,840

Problem 25-5A (Continued)

Part 4

Sales Mix Recommendation. By incurring additional marketing cost, the

Units of Product G ………………………………………………………

= 700 units per month

Hours per unit ……………………………………………………….

0.4

Hours used for Product G ……………………………………..……

280

hours

Hours available for Product B (352 hrs – 280 hrs) ………………

72

hours

The output of Product B with 72 production hours is

Contribution Margin at This Sales Mix

Units

Contr./unit

Total

From G ………………………………………………………….

700

$80

$56,000

From B ………………………………………………………….

72

70

5,040

Less extra shift costs …………………………………….

(15,000)

Less extra marketing costs …………………………..

(12,000)

Total contribution margin ……………………………...

$34,040

Management decision. This contribution margin of $34,040 is less than the

1 hr. per unit

Fundamental Accounting Principles, 21st Edition

1496

Problem 25-6A (60 minutes)

Part 1

ELEGANT DECOR COMPANY

Analysis of Expenses under Elimination of Department 200

Total

Eliminated

Continuing

Expenses

Expenses

Expenses

Cost of goods sold ……………………………………….

$469,000

$207,000

$262,000

Direct expenses

Advertising ……………………………………..………….

29,000

12,000

17,000

Store supplies used …………………………..

7,800

3,800

4,000

Depreciation—Store equipment ……….………….

8,300

8,300

Allocated expenses

Sales salaries* …………………………………………….

104,000

52,000

52,000

Rent expense…………………………………..………….

14,160

14,160

Bad debts expense …………………………..

18,000

8,100

9,900

Office salary* …………………………………..………….

31,200

31,200

Insurance expense* …………………………..

3,100

770

2,330

Miscellaneous office expenses* ……….………….

4,000

400

3,600

Total expenses ………………………………….………….

$688,560

$284,070

$404,490

*Computation notes. Closing Department 200 will eliminate 70% of its insurance

Problem 25-6A (Continued)

Part 2

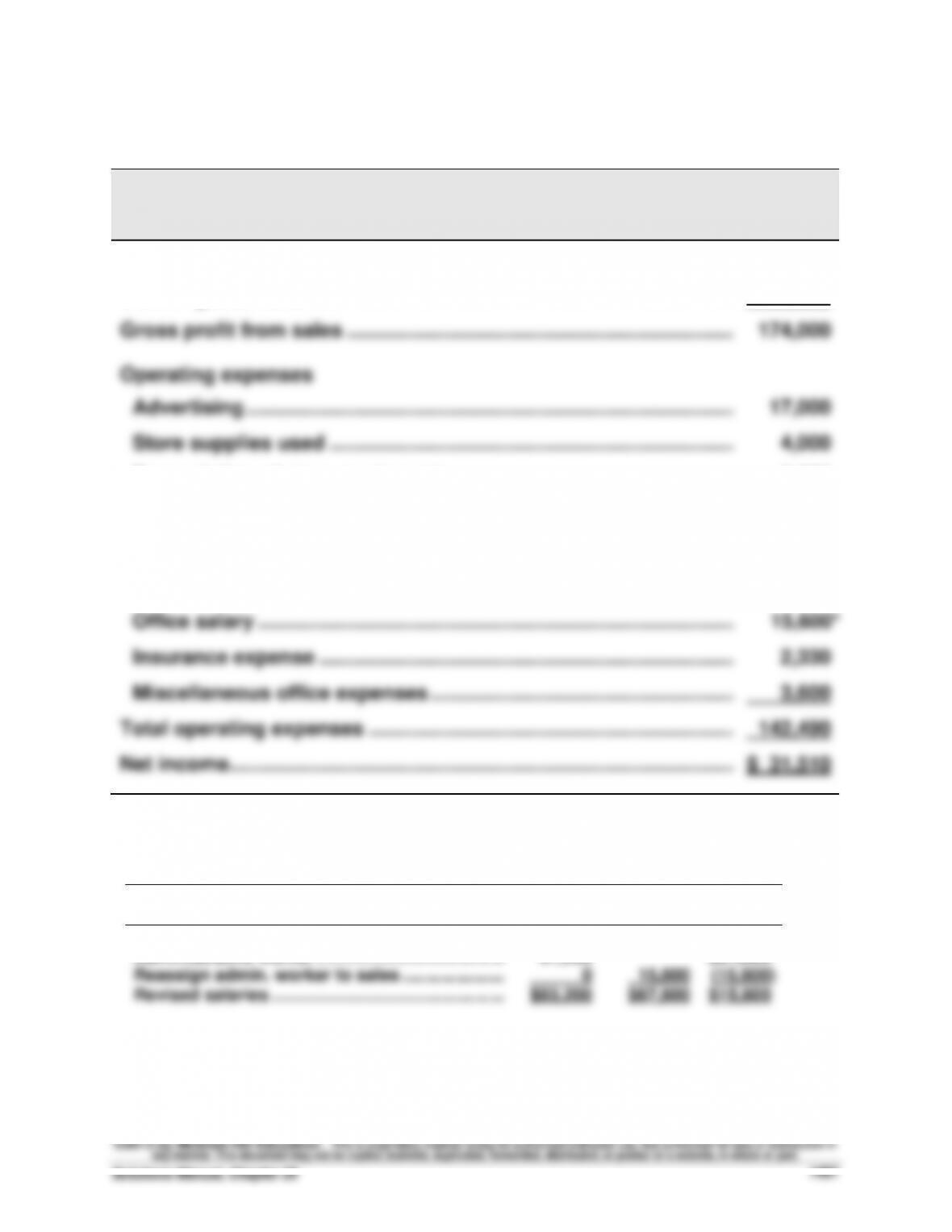

ELEGANT DECOR COMPANY

Forecasted Annual Income Statement

Under Plan to Eliminate Department 200

Sales ………………………………………………………………………………………..….

$436,000

Cost of goods sold …………………………………………………………………..….

262,000

Gross profit from sales …………………………………………………………….….

174,000

Operating expenses

Advertising …………………………………………………………………………….….

17,000

Store supplies used ……………………………………………………………….….

4,000

Depreciation of store equipment …………………………………………….….

8,300

Sales salaries …………………………………………………………………………….

67,600*

Rent expense …………………………………………………………………………….

14,160

Bad debts expense …………………………………………………………………….

9,900

Office salary …………………………………………………………………………..….

15,600*

Insurance expense …………………………………………………………………….

2,330

Miscellaneous office expenses ……………………………………………….….

3,600

Total operating expenses …………………………………………………………….

142,490

Net income ……………………………………………………………………………….….

$ 31,510

* Administrative salary reassignment

Total

Sales

Office

Salaries

Salaries

Salary

Salesclerks ………………………………………………..……..

$52,000

$52,000

Administrative worker ……………………………………………….

31,200

$31,200

Reassign admin. worker to sales …………………………..

0

15,600

(15,600)

Revised salaries ……………………………………………………….

$83,200

$67,600

$15,600

Fundamental Accounting Principles, 21st Edition

1498

Problem 25-6A (Continued)

Part 3

ELEGANT DECOR COMPANY

Reconciliation of Combined Income With Forecasted Income

Combined net income …………………………………………………………….…

$ 37,440

Less Dept. 200’s lost sales ……………………………………………………….

(290,000)

Plus Dept. 200’s eliminated expenses ……………………………………..…

284,070

Forecasted net income ………………………………………………………………

$ 31,510

ANALYSIS

Department 200’s avoidable expenses of $284,070 are $5,930 less than its

PROBLEM SET B

Problem 25-1B (50 minutes)

Part 1

Part 2

Net

Net Cash

Income

Flow

Expected annual sales of new product ………………..…

$1,150,000

$1,150,000

Expected annual costs of new product

Direct materials ………………………………………………..…

300,000

300,000

Direct labor ……………………………………………………….

420,000

420,000

Overhead excluding depr. on new asset ………………

210,000

210,000

Depreciation on new asset ……………………………….…

70,000

Selling and administrative expenses ……………………

100,000

100,000

Income before taxes ………………………………………………

50,000

Income taxes (30%) …………………………………………….…

15,000

15,000

Net income ………………………………………………………….…

$ 35,000

Net cash flow* …………………………………………………….…

$ 105,000

*Alternatively, annual net cash flow can be computed as:

Net income + Depreciation = $35,000 + $70,000 = $105,000

Problem 25-1B (Continued)

Part 3

Part 4

Accounting rate of return = = 21.88%

$35,000

$160,000*

$105,000

Problem 25-2B (55 minutes)

Part 1

PROJECT A

Net income ………………………………………………………………………………..…

$39,900

Depreciation expense* …………………………………………………………………

60,000

Net cash flow …………………………………………………………………………….…

$99,900

PROJECT B

Net income ………………………………………………………………………………..…

$ 25,900

Depreciation expense* …………………………………………………………………

80,000

Net cash flow …………………………………………………………………………….…

$105,900

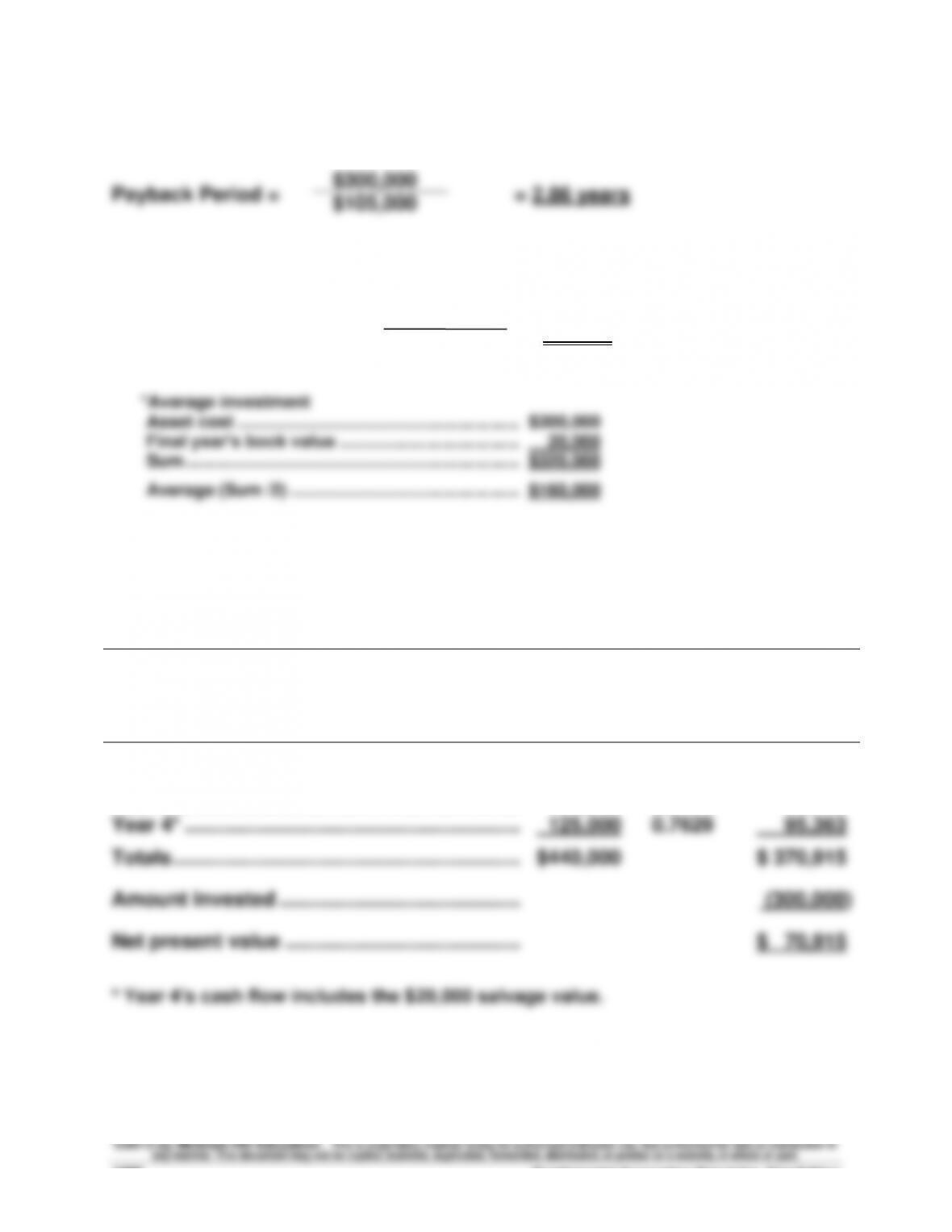

3 years

Part 2

PROJECT A

Payback Period = = 2.4 years

PROJECT B

$240,000

$105,900

4 years

$240,000

$ 99,900

Fundamental Accounting Principles, 21st Edition

1502

Problem 25-2B (Continued)

Part 3

PROJECT A

Accounting rate of return = = 33.3%

*Average investment

Asset cost ………………………………………….

$240,000

Average (Cost/2) ………………………………...

$120,000

PROJECT B

*Average investment

Asset cost ………………………………………….

$240,000

Average (Cost/2) ………………………………...

$120,000

$39,900

$120,000*

$120,000*

Problem 25-2B (Continued)

Part 4

PROJECT A

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-4 ……………………………………………….

$99,900

3.3121

$330,879

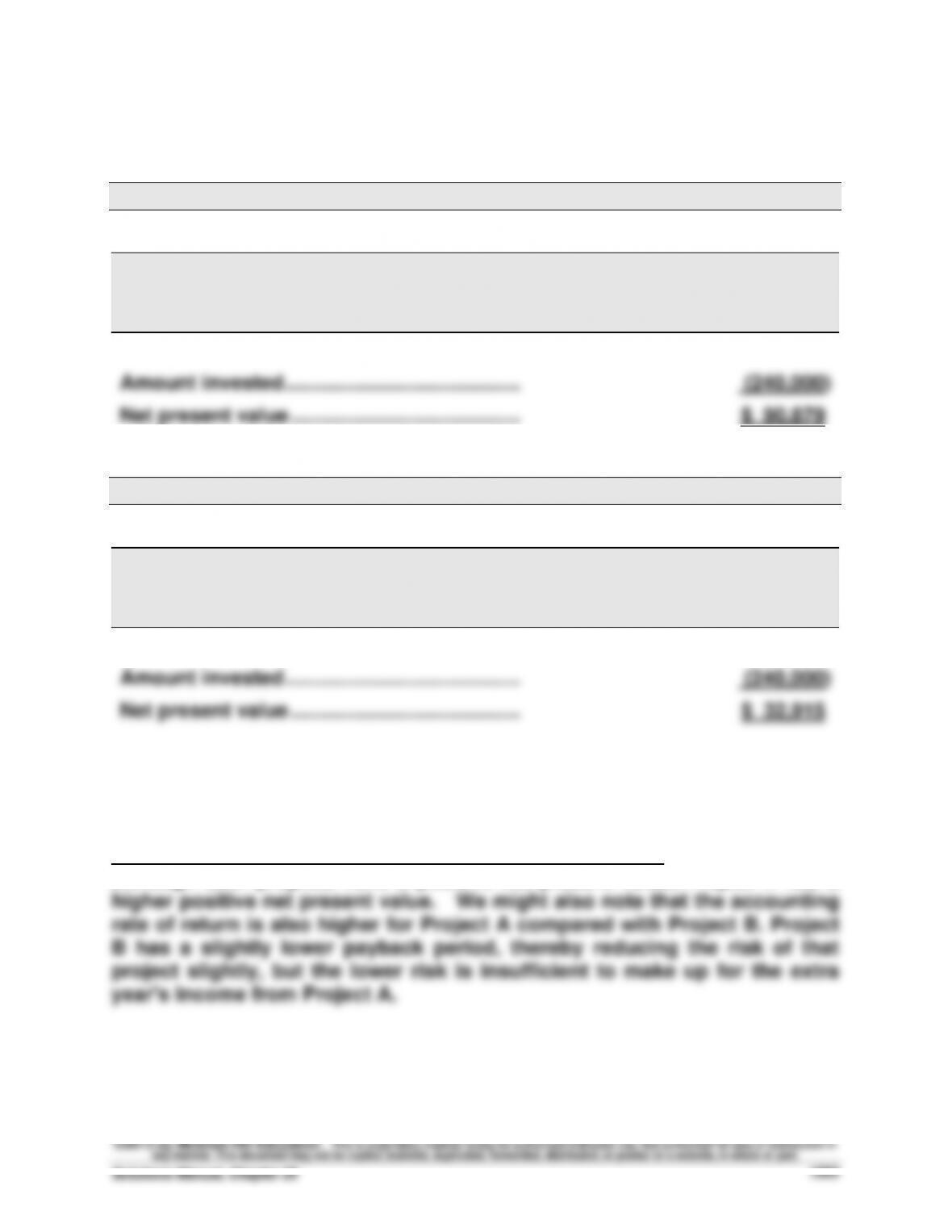

Amount invested ……………………………………

(240,000)

Net present value …………………………………..

$ 90,879

PROJECT B

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-3 ……………………………………………….

$105,900

2.5771

$272,915

Amount invested ……………………………………

(240,000)

Net present value …………………………………..

$ 32,915

Part 5

Recommendation to management is to pursue Project A. This is because

although both projects have a positive net present value, Project A has a

Fundamental Accounting Principles, 21st Edition

1504

Problem 25-3B (60 minutes)

Part 1

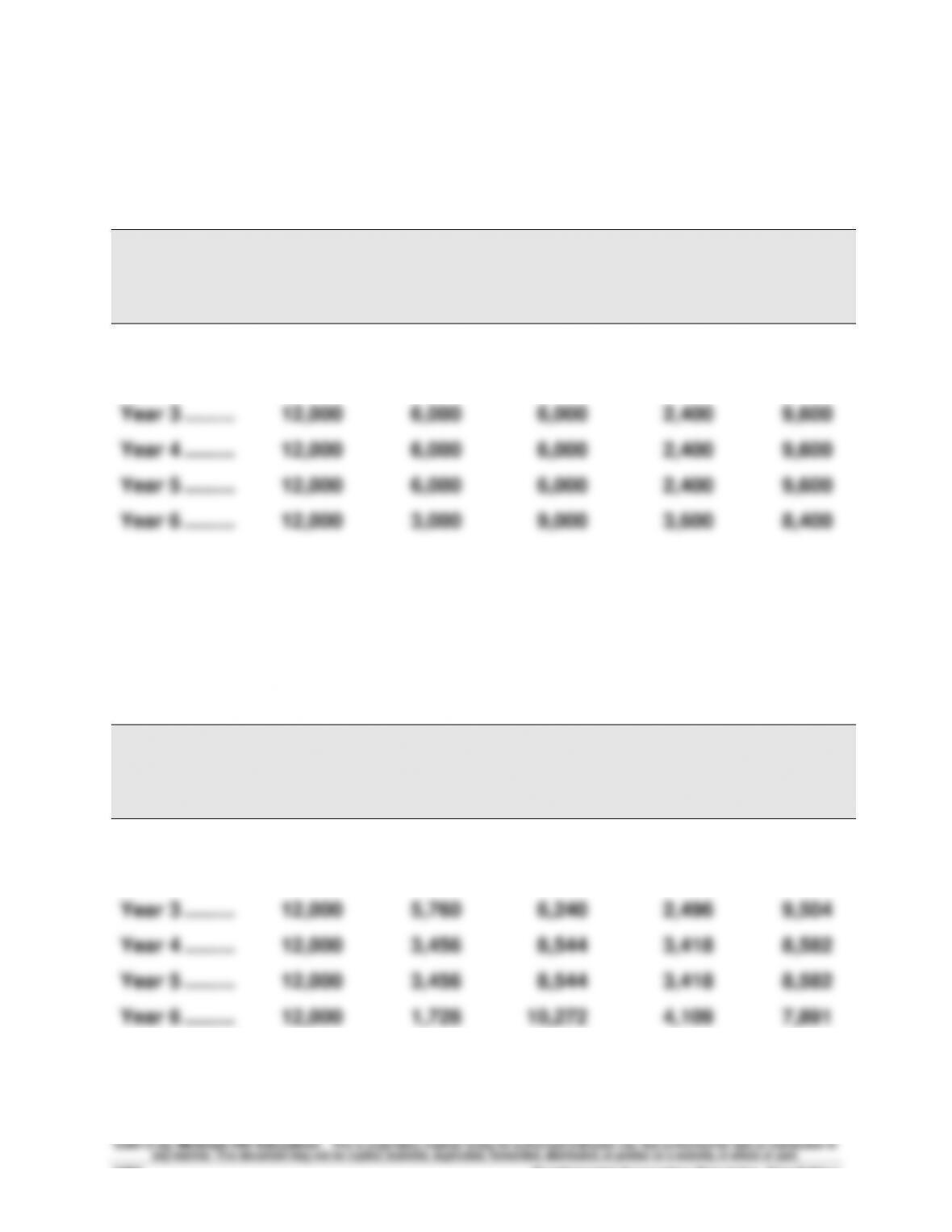

RESULTS USING STRAIGHT-LINE DEPRECIATION

(a)

Income

Before

Deprec.

(b)

Straight–

Line

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 ……….………………

$12,000

$3,000

$ 9,000

$3,600

$8,400

Year 2 ……….………………

12,000

6,000

6,000

2,400

9,600

Year 3 ……….………………

12,000

6,000

6,000

2,400

9,600

Year 4 ……….………………

12,000

6,000

6,000

2,400

9,600

Year 5 ……….………………

12,000

6,000

6,000

2,400

9,600

Year 6 ……….………………

12,000

3,000

9,000

3,600

8,400

Part 2

RESULTS USING MACRS DEPRECIATION

(a)

Income

Before

Deprec.

(b)

MACRS

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 ……….………………

$12,000

$6,000

$ 6,000

$2,400

$ 9,600

Year 2 ……….………………

12,000

9,600

2,400

960

11,040

Year 3 ……….………………

12,000

5,760

6,240

2,496

9,504

Year 4 ……….………………

12,000

3,456

8,544

3,418

8,582

Year 5 ……….………………

12,000

3,456

8,544

3,418

8,582

Year 6 ……….………………

12,000

1,728

10,272

4,109

7,891

Problem 25-3B (Continued)

Part 3

NET PRESENT VALUE OF ASSET USING STRAIGHT-LINE DEPRECIATION

Present

Present

Net Cash

Value of

Value of Net

Flows

1 at 10%

Cash Flows

Year 1 …………………………………………………..

$ 8,400

0.9091

$ 7,636

Year 2 …………………………………………………..

9,600

0.8264

7,933

Year 3 …………………………………………………..

9,600

0.7513

7,212

Year 4 …………………………………………………..

9,600

0.6830

6,557

Year 5 …………………………………………………..

9,600

0.6209

5,961

Year 6 …………………………………………………..

8,400

0.5645

4,742

Totals …………………………..………………………

$55,200

$40,041

Amount invested …………………………………..

(30,000)

Net present value ………………………………….

$10,041

Part 4

NET PRESENT VALUE OF ASSET USING MACRS DEPRECIATION

Present

Present

Net Cash

Value of

Value of Net

Flows

1 at 10%

Cash Flows

Year 1 …………………………………………………..

$ 9,600

0.9091

$ 8,727

Year 2 …………………………………………………..

11,040

0.8264

9,123

Year 3 …………………………………………………..

9,504

0.7513

7,140

Year 4 …………………………………………………..

8,582

0.6830

5,862

Year 5 …………………………………………………..

8,582

0.6209

5,329

Year 6 …………………………………………………..

7,891

0.5645

4,454

Totals …………………………..………………………

$55,199

$40,635

Amount invested …………………………………..

(30,000)

Net present value ………………………………….

$10,635

Part 5

Analysis: The net present value using MACRS depreciation is greater than the

Fundamental Accounting Principles, 21st Edition

1506

Problem 25-4B (45 minutes)

WINDMIRE COMPANY

COMPARATIVE INCOME STATEMENTS

(1)

(2)

(3)

Normal

New

Volume

Business

Combined

Sales …………………………………………………...

$1,200,000

$172,000

$1,372,000

Costs and expenses

Direct materials ………………………………....

384,000

64,000

448,000

Direct labor ………………………………………..

96,000

24,000

120,000

Overhead …………………………..……………...

288,000

36,000

324,000

Selling expenses ………………………………..

120,000

120,000

Administrative expenses …………………...

80,000

4,000

84,000

Total costs and expenses …………………....

968,000

128,000

1,096,000

Operating income ………………………………..

$ 232,000

$ 44,000

$ 276,000

Supporting computations

Normal direct material cost ……………………………………..………

$384,000

Units of output ………………………………………………………..………

300,000

Cost per unit …………………………………………………………..………

$ 1.28

New business volume …………………………..…………………………

50,000

New business direct material cost ……………………………………

$ 64,000

Normal direct labor cost …………………………..……………..………

$ 96,000

Units of output ………………………………………………………..………

300,000

Cost per unit …………………………………………………………..………

$ 0.32

Overtime per unit (50%) …………………………………………..………

0.16

New business direct labor cost per unit …………………………..

$ 0.48

New business volume …………………………..…………………………

50,000

New business direct labor cost ………………………………..………

$ 24,000

Total overhead ………………………………………………………..………

$288,000

Fixed overhead (25%) ……………………………………………..………

72,000

Variable overhead …………………………………………………..…..

$216,000

Units of output ………………………………………………………..………

300,000

Cost per unit …………………………………………………………..………

$ 0.72

New business volume …………………………..…………………………

50,000

New business variable overhead cost …………………………..

$ 36,000