Title: Exercise 25-7

QA_Ori:

1.

PROJECT C1

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of Net

Cash Flows

Year 1 $ 12,000 0.8929 $ 10,715

PROJECT C2

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of Net

Cash Flows

Year 1 $ 96,000 0.8929 $ 85,718

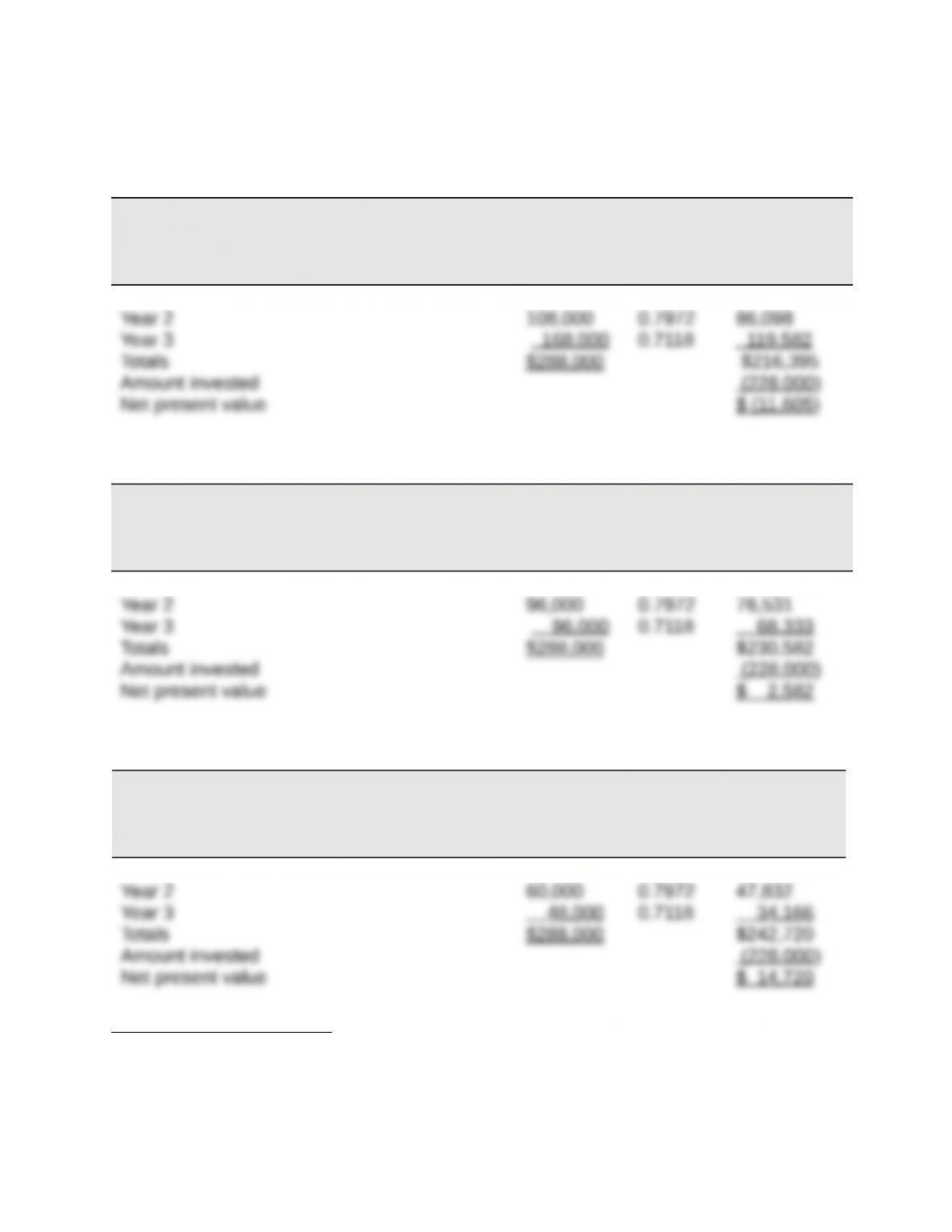

PROJECT C3

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of Net

Cash Flows

Year 1 $180,000 0.8929 $160,722

Analysis and Interpretation: Both Project C2 and C3 yield a positive net present value.

Accordingly, both C2 and C3 are acceptable investments.

Title: Exercise 25-7

QA_Ori:

2. INTERNAL RATE OF RETURN VS. NET PRESENT VALUE FOR C2

Project C2 will have an internal rate of return higher than 12%.

We know this because Project C2 has a positive net present value using a 12% rate of

return.

3. INTERNAL RATE OF RETURN FOR PROJECT C2

(i) Present value factor= Amount invested / Net cash flows

= $228,000 / $96,000 = 2.375

*Instructor note: There is not a 13% column in the PV tables; students will need to

interpolate —— 12% + [ (15%-12%) x ({2.4018 – 2.3750}/ 0.1186) ] = 12.68%.

Title: Exercise 25-8

QA_Ori:

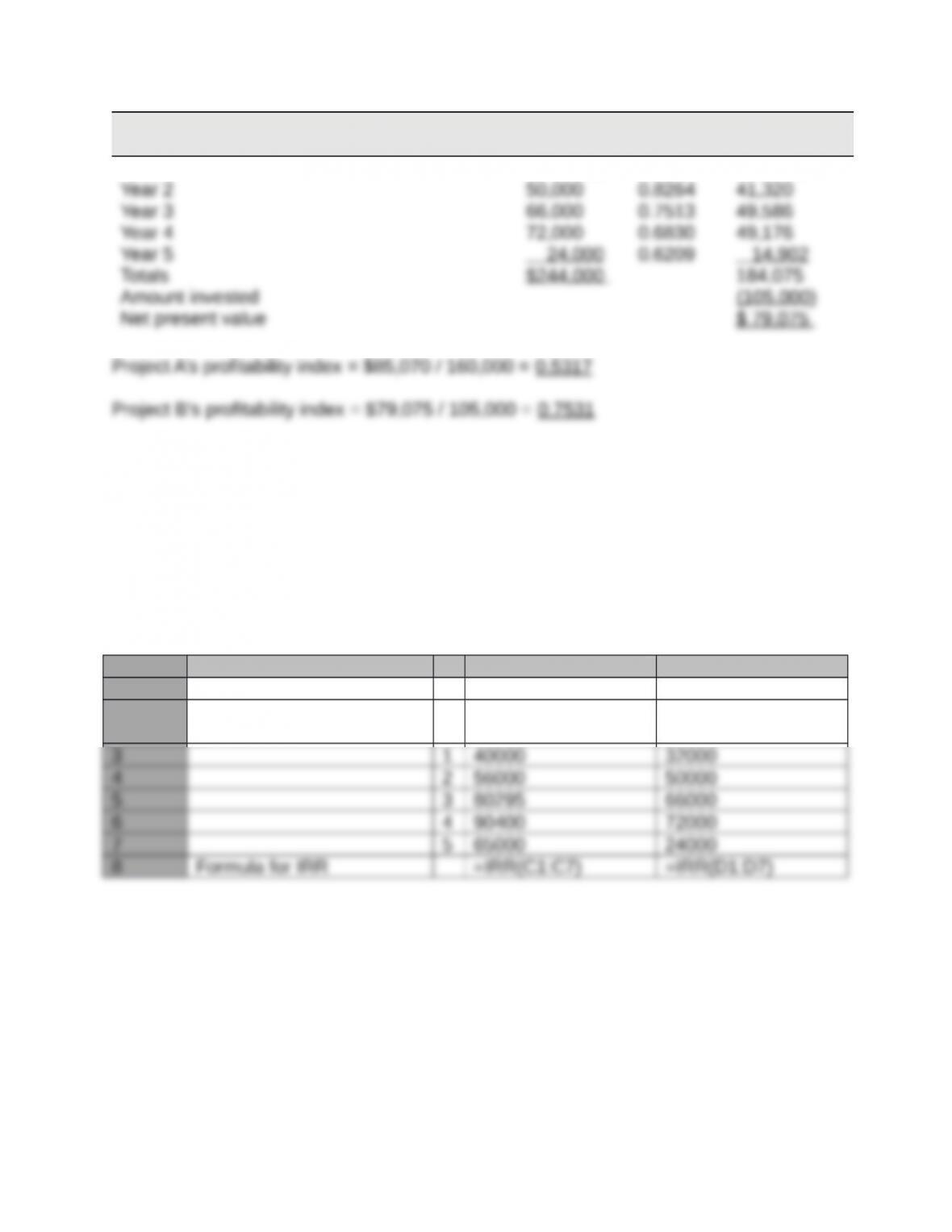

PROJECT A

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of Net

Cash Flows

Year 1 $ 40,000 0.9091 $ 36,364

PROJECT B

Present

Present

Value of Net

Net Cash

Flows

Value of

1 at 10%

Cash Flows

Year 1 $ 32,000 0.9091 $ 29,091

Both projects have positive net present values. However, if the company can choose

only one project, it should select project B, since it has a higher profitability index.

Title: Exercise 25-9A

QA_Ori:

Using Excel, Project A (B) has an internal rate of return of 26.96 (35.00%).

Project A Project B

A B C D

1 Initial investment -160000 -105000

2Annual cash flows, end of

period

Title: Exercise 25-10

QA_Ori:

Sunk cost

Relevant benefits

Avoidable costs

Out-of-pocket cost

Opportunity cost

Title: Exercise 25-11

QA_Ori:

ALTERNATIVE A: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine $(115,000)

*(36,000 – $19,000) X 5 years

ALTERNATIVE B: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine $(125,000)

**(36,000 – $15,000) X 5 years

Title: Exercise 25-12

QA_Ori:

(1) The incremental income from selling as scrap is $55,000 (22,000 x $2.50).

(2)

INCREMENTAL INCOME FROM REWORK

*Sales price per unit – cost per unit = $8.50 – $6 = $2.50.

(3) The product should not be reworked as the $33,000 income from reworking is less

Title: Exercise 25-13

QA_Ori:

Normal Additional Combined

Volume Volume* Total

Sales $2,250,000 $180,000 $2,430,000

Costs and expenses

1(15,000 x $2) 2 (15,000 x $4)

*ADDITIONAL VOLUME COMPUTATIONS

RECOMMENDATION : The company should accept the offer because the additional sales

would yield an incremental net income of $3,000.

Title: Exercise 25-14

QA_Ori:

INCREMENTAL COST OF MAKING THE PART

INCREMENTAL COST OF BUYING THE PART

RECOMMENDATION : Note that the allocated fixed costs of $58,500 are not relevant to this

Title: Exercise 25-15

QA_Ori:

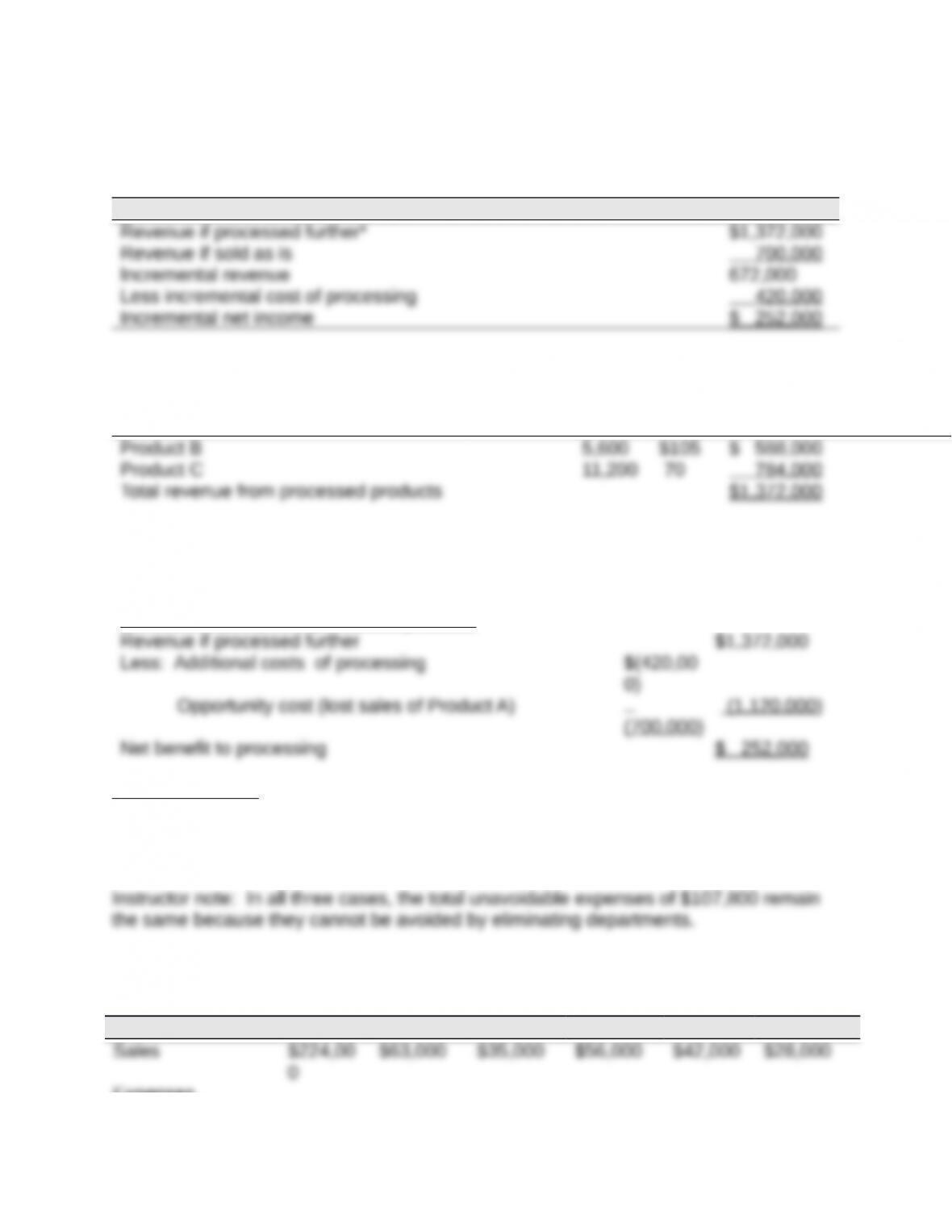

INCREMENTAL REVENUE AND COST OF ADDITIONAL PROCESSING

*Revenue from processed products

Units Price Total

ALTERNATE SOLUTION FORMAT

Net income (loss) from processed products

RECOMMENDATION : This analysis shows that the company will be better off by $252,000

if it chooses to process Product A into the two products of B and C. (Note that the $28

per unit cost of manufacturing Product A is sunk and irrelevant to this decision.)

Title: Exercise 25-16

QA_Ori:

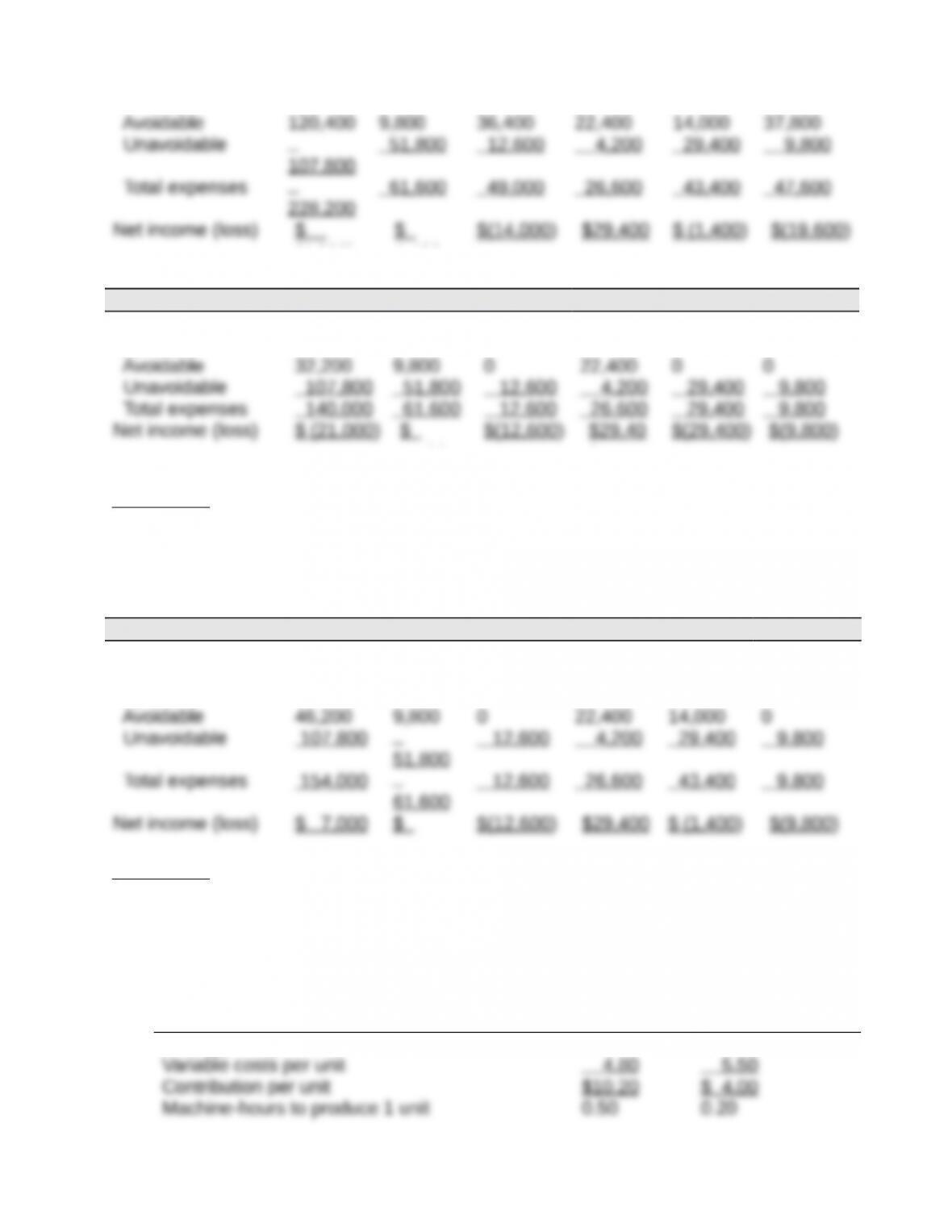

1. NO DEPARTMENTS ELIMINATED

Total M N O P T

0

Expenses

(4,200)

1,400

2. DEPARTMENTS WITH EXPECTED NET LOSSES ELIMINATED

Total M N O P T

Sales $119,000 $63,000 $ 0 $56,000 $ 0 $ 0

Expenses

1,400

0

Explanation: This income statement reflects elimination of Departments N, P, and T. The

sales and avoidable expenses are the combined amounts for Departments M and O.

The net loss has actually increased because the excess of sales dollars over avoidable

expenses has declined and less remains to cover unavoidable expenses.

3. DEPARTMENTS WITH LESS SALES THAN AVOIDABLE EXPENSES ELIMINATED

Total M N O P T

Sales $161,000 $63,00

0

$ 0 $56,000 $42,000 $ 0

Expenses

1,400

Explanation: This income statement reflects the Departments M, O, and P. Departments

N and T are eliminated because their sales dollars do not cover their avoidable costs.

Title: Exercise 25-17

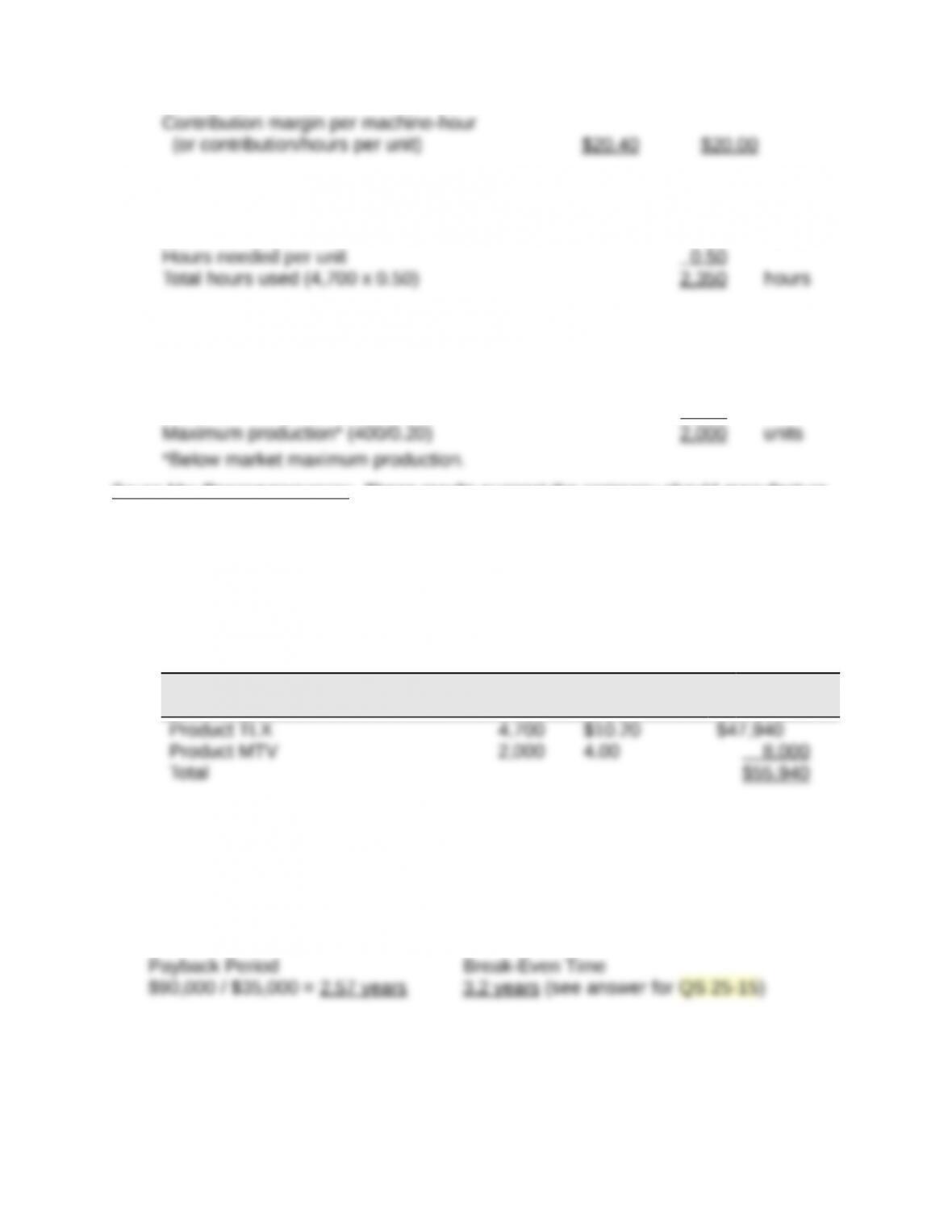

QA_Ori:

Preliminary computations

Contribution margin per hour Product TLX Product MTV

Selling price per unit $15.00 $ 9.50

1. FOR PRODUCT TLX

Maximum sales 4,700 units

FOR PRODUCT MTV

Remaining hours (2,750 – 2,350) 400 hours

Hours needed per unit 0.20

SALES MIX RECOMMENDATION : These results suggest the company should manufacture

as many units of Product TLX as it can produce and sell until reaching a (market or

production) constraint. Thereafter, any remaining capacity should be devoted to

Product MTV, up to the maximum that can be produced and/or sold.

2. CONTRIBUTION MARGIN FROM THE RECOMMENDED SALES MIX

Units

Contribution per

Unit Total

Title: Exercise 25-18

QA_Ori:

1. Recovery time computation

2. The advantage of break-even time is that it considers the time value of money.

This means break-even time should provide a superior estimate of the recovery time

relative to the payback period method.

3. When (1) the interest rate is very low, 1% for example, and (2) the payback

period is very short, then payback period and break-even time will yield similar results.

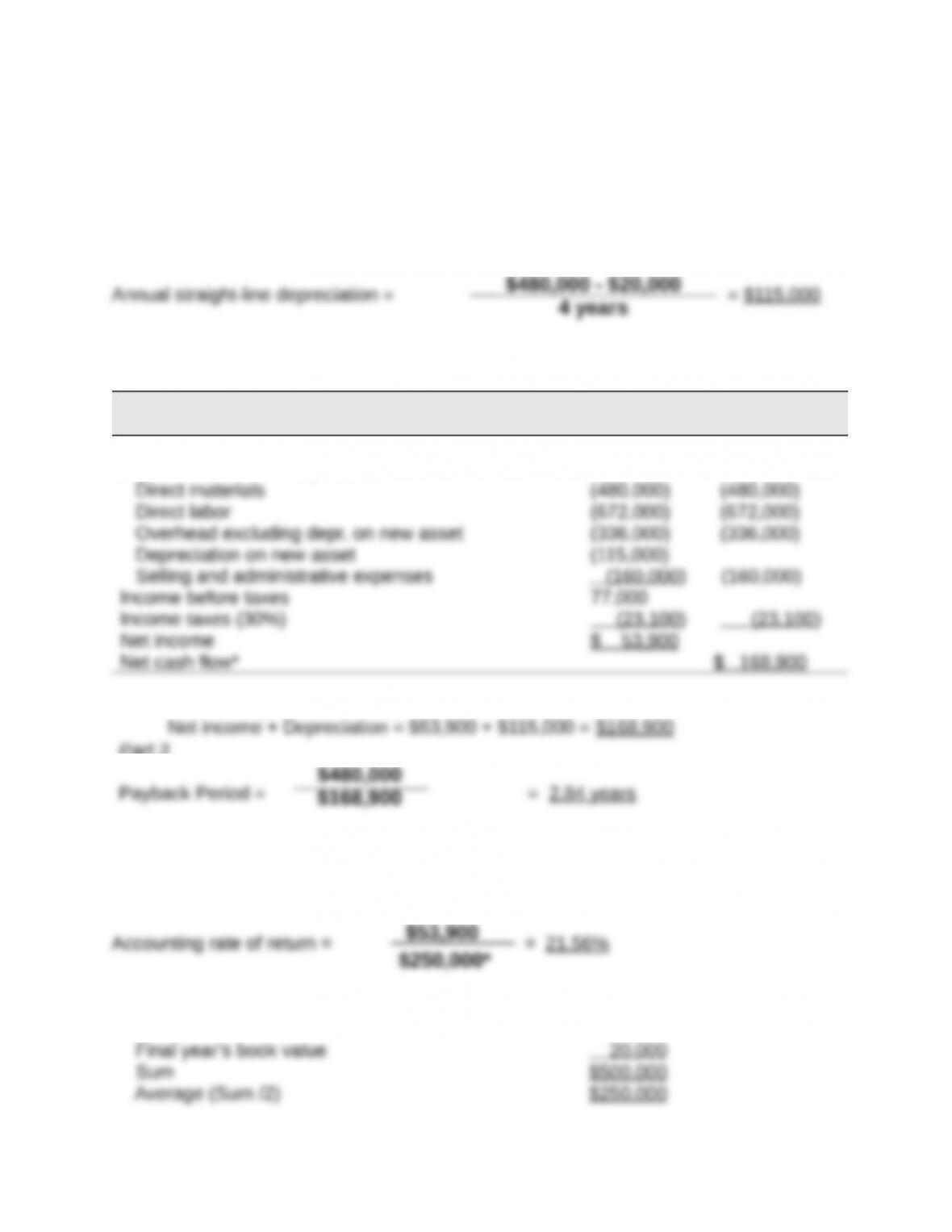

Title: Problem 25-1A

QA_Ori:

Part 1

Part 2

Net Net Cash

Income Flow

Expected annual sales of new product $1,840,000 $1,840,000

Expected costs of new product

* Alternatively, annual net cash flow can be computed as

Part 3

QA_Ori:

Part 4

* Average investment

Asset cost $480,000

Final year’s book value 20,000

Sum $500,000

Average (Sum /2) $250,000

$480,000 – $20,000

4 years

$53,900

$250,000*

$480,000

$168,900

Part 5

Present Value of Net Cash Flows

Present Present

Net Cash Value of Value of Net

Flows 1 at 7% Cash Flows

Year 1 $168,900 0.9346 $ 157,854

* Year 4’s cash flow includes the $20,000 salvage value.