Title: Exercise 14-5

QA_Ori:

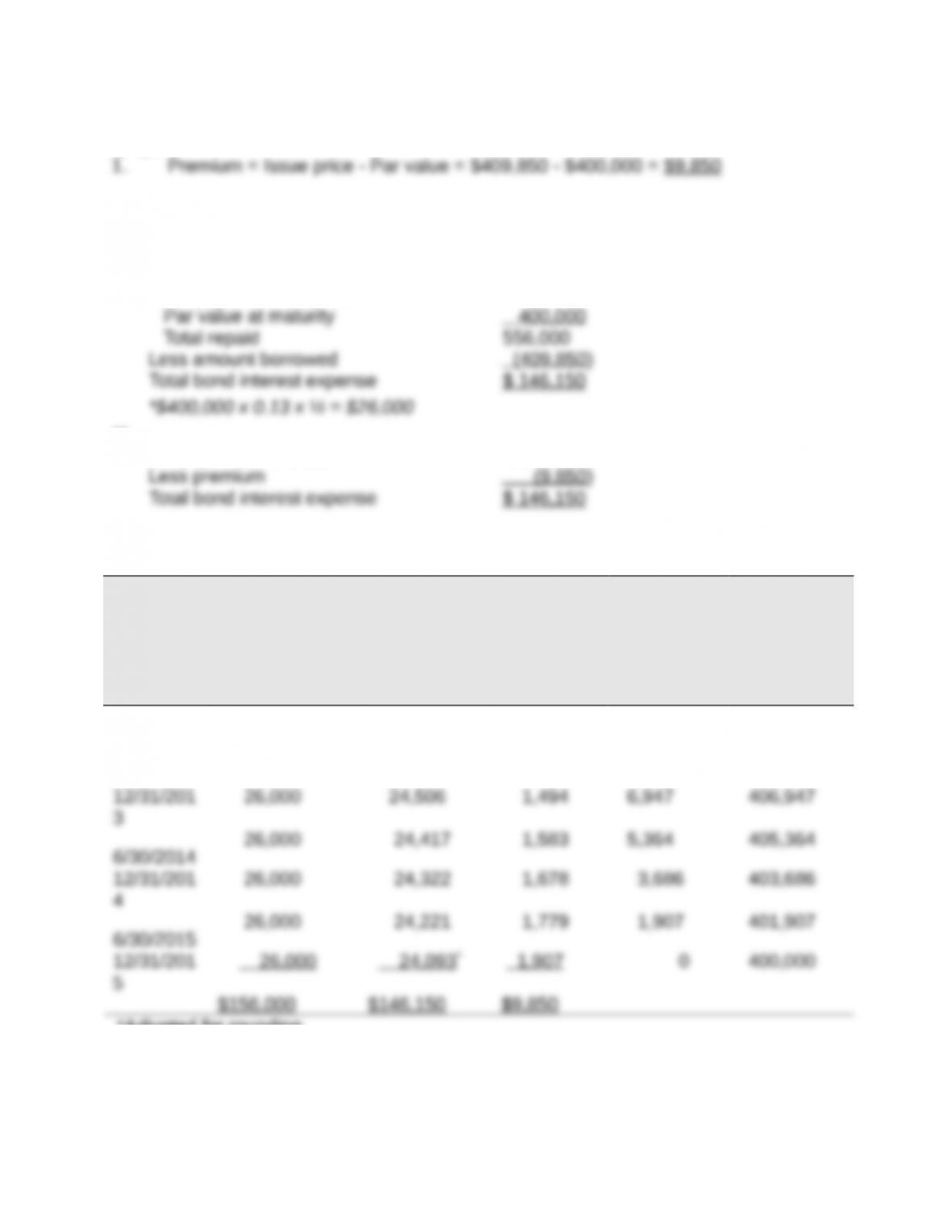

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $26,000* $ 156,000

or

Six payments of $26,000 $ 156,000

3. Effective interest amortization table

Semiannu

al

Interest

Period-En

d

(A)

Cash Interest

Paid

[6.5% x

$400,000]

(B)

Bond Interest

Expense

[6% x Prior

(E)]

(C)

Premium

Amortizatio

n

[(A) – (B)]

(D)

Unamortize

d

Premium

[Prior (D) –

(C)]

(E)

Carrying

Value

[400,000 +

(D)]

1/01/2013

$9,850 $409,850

6/30/2013

$ 26,000 $ 24,591 $1,409 8,441 408,441

*Adjusted for rounding.

Title: Exercise 14-6

QA_Ori:

2013

(a)

Dec. 31 Cash 186,534

2014

(b)

June 30 Bond Interest Expense 7,684

(c)

Dec. 31 Bond Interest Expense 7,684

Title: Exercise 14-7

QA_Ori:

2013

(a)

Dec. 31 Cash 188,000

(b)

2014

June 30 Bond Interest Expense 8,000

Discount on Bonds Payable* 3,000

Dec. 31 Bond Interest Expense 8,000

2015

June 30 Bond Interest Expense 8,000

Dec. 31 Bond Interest Expense 8,000

(c)

Dec. 31 Bonds Payable 200,000

Title: Exercise 14-8

QA_Ori:

2012

(a)

Dec. 31 Cash 216,222

2013

(b)

June 30 Bond Interest Expense 8,378

(c)

Dec. 31 Bond Interest Expense 8,378

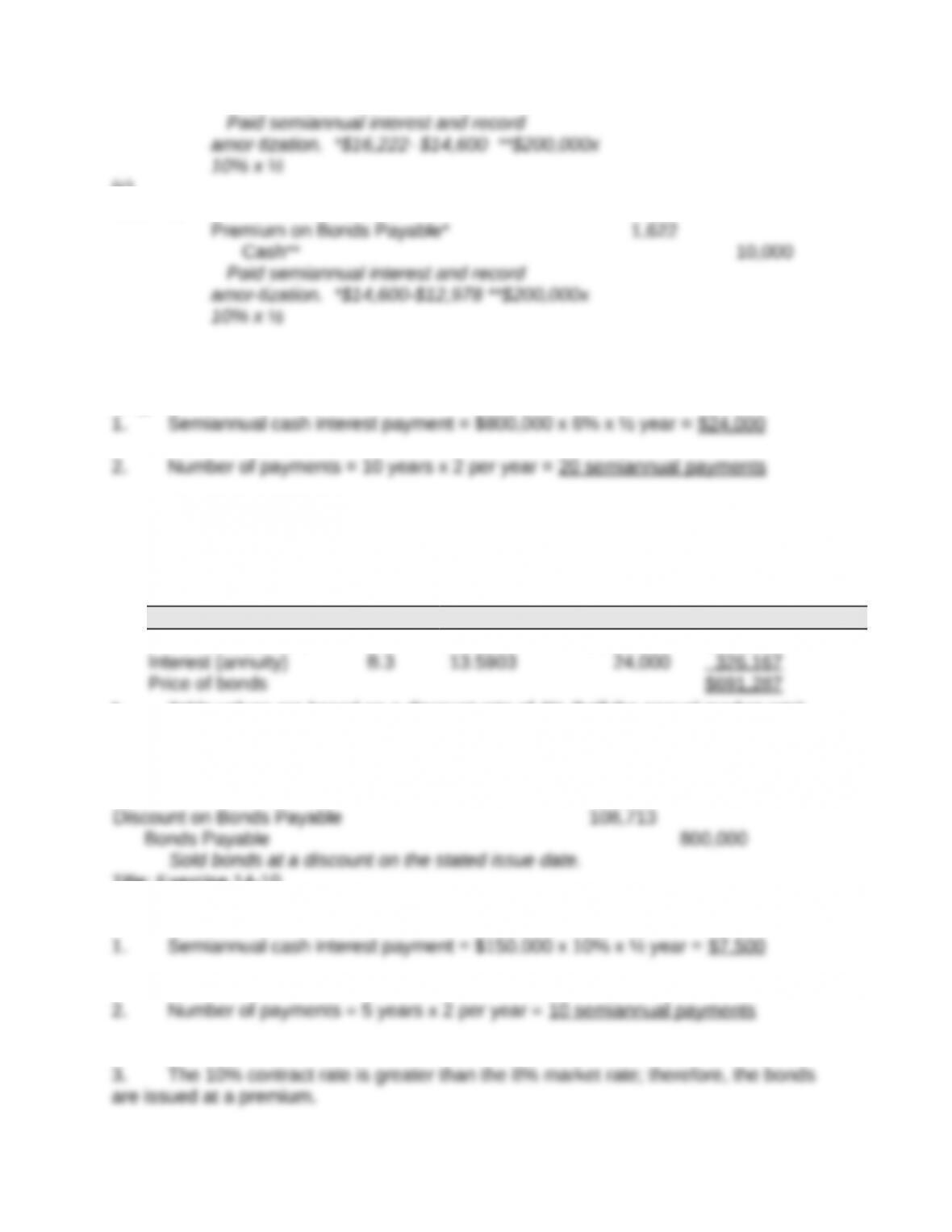

Title: Exercise 14-9

QA_Ori:

3. The 6% contract rate is less than the 8% market rate; therefore, the bonds are

issued at a discount.

4. Estimation of the market price at the issue date

Cash Flow Table Table Value* Amount Present Value

Par (maturity) value B.1 0.4564 $800,000 $365,120

* Table values are based on a discount rate of 4% (half the annual market rate)

and 20 periods (semiannual payments).

5.

Cash 691,287

Title: Exercise 14-10

QA_Ori:

4. Estimation of the market price at the issue date

Cash Flow Table Table Value* Amount Present Value

Par (maturity) value B.1 0.6756 $150,000 $101,340

* Table values are based on a discount rate of 4% (half the annual market rate)

and 10 periods (semiannual payments).

5.

Title: Exercise 14-11

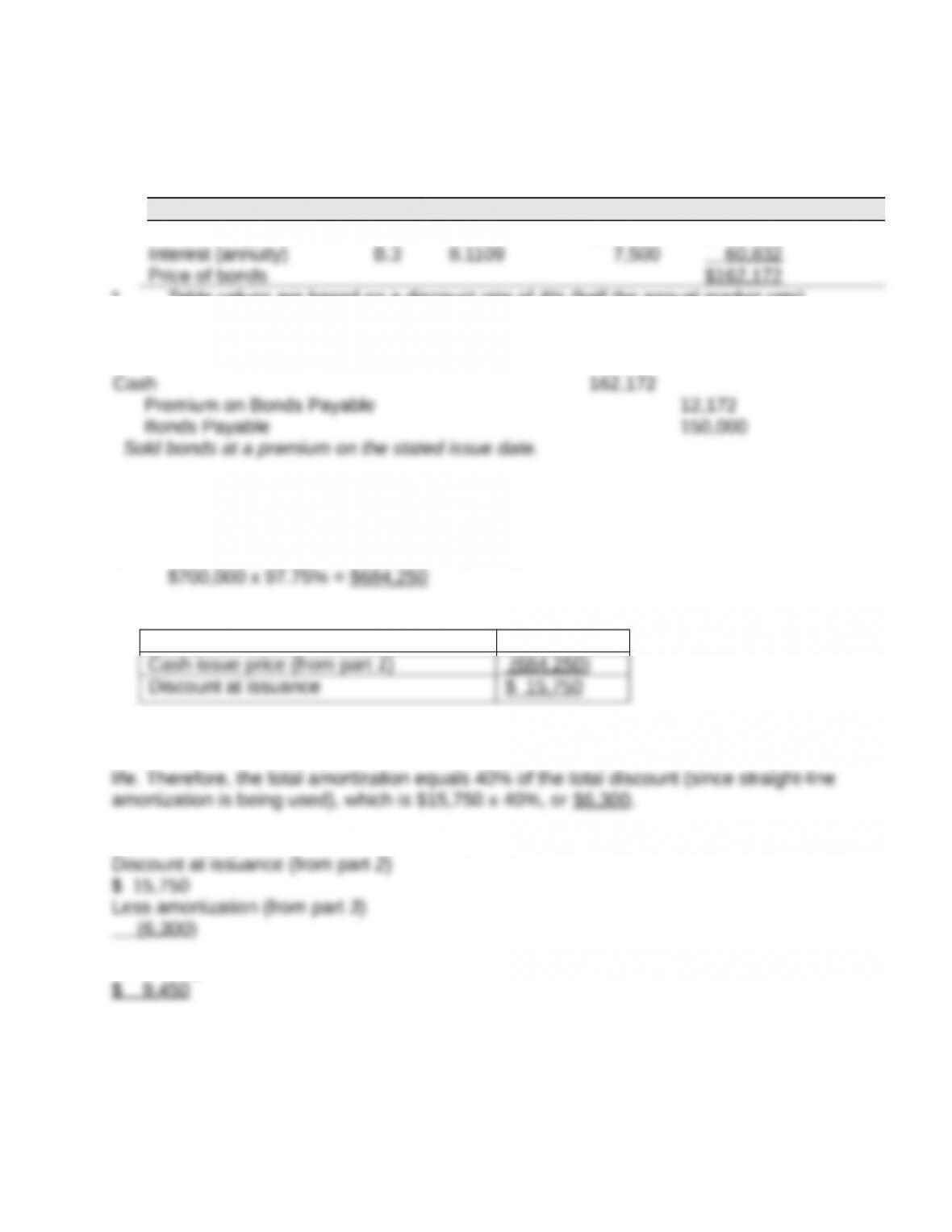

QA_Ori:

1. Cash proceeds from sale of bonds at issuance

2. Discount at issuance

Par value $700,000

3. Total amortization for first 6 years

The first six years (from 1/1/13 to 12/31/18) equals 40% of the bonds’ 15-year

4. Carrying value of the bonds at 12/31/2018

Remaining discount

Entire Group

Retired 20%

Remaining discount

Carrying value

5. Cash purchase price

6. Loss on retirement

7. Journal entry at retirement for 20% of bonds

2019

Jan. 1 Bonds Payable 140,000

Title: Exercise 14-12

QA_Ori:

2. Journal entries

2013

May 1 Cash 3,502,000

June 30 Interest Payable 102,000

Dec. 31 Bond Interest Expense 153,000

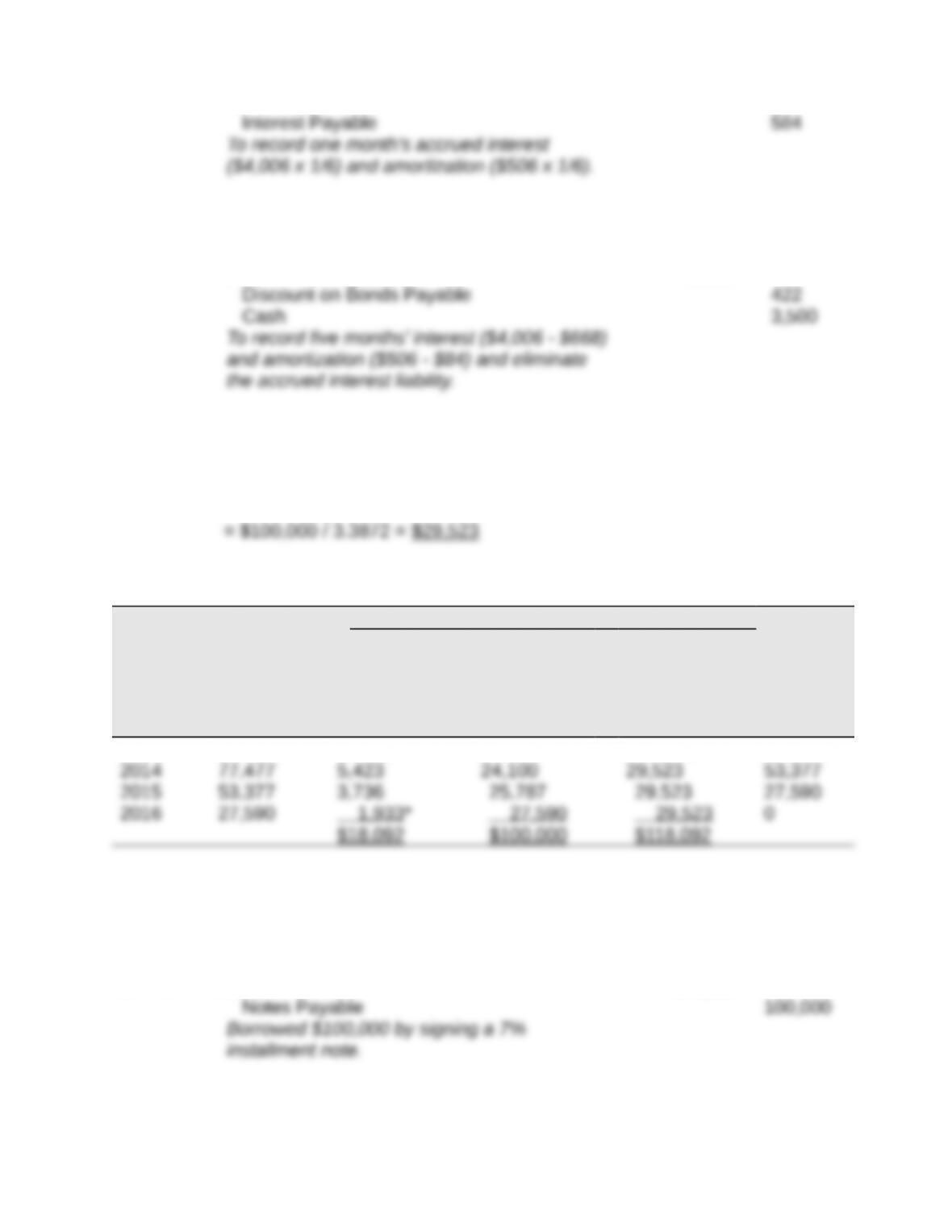

Title: Exercise 14-13

QA_Ori:

1. Straight-line amortization table (($100,000-$95,948)/8 = $506.5)

Semiannual

Period-End

Unamortized

Discount †

Carrying

Value

6/01/2013 $4,052 $95,948

11/30/2013 3,546 96,454

* Adjusted for rounding difference.

† Supporting computations

Eight payments of $3,500** $ 28,000

or

Eight payments of $3,500 $ 28,000

2.

2013

Nov. 30 Bond Interest Expense 4,006

Dec. 31 Bond Interest Expense 668

Discount on Bonds Payable 84

2014

May 31 Interest Payable 584

Bond Interest Expense 3,338

Title: Exercise 14-14

QA_Ori:

1. Amount of each payment = Initial note balance / Table B.3 value

2. Amortization table for the loan

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[7% x (A)]

+

(C)

Debit Notes

Payable [(D)

– (B)] =

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

2013 $100,000 $ 7,000 $ 22,523 $ 29,523 $77,477

*Adjusted for rounding.

Title: Exercise 14-15

QA_Ori:

2013

Jan. 1 Cash 100,000

2013

2014

Dec. 31 Interest Expense 5,423

2015

Dec. 31 Interest Expense 3,736

2016

Dec. 31 Interest Expense 1,933

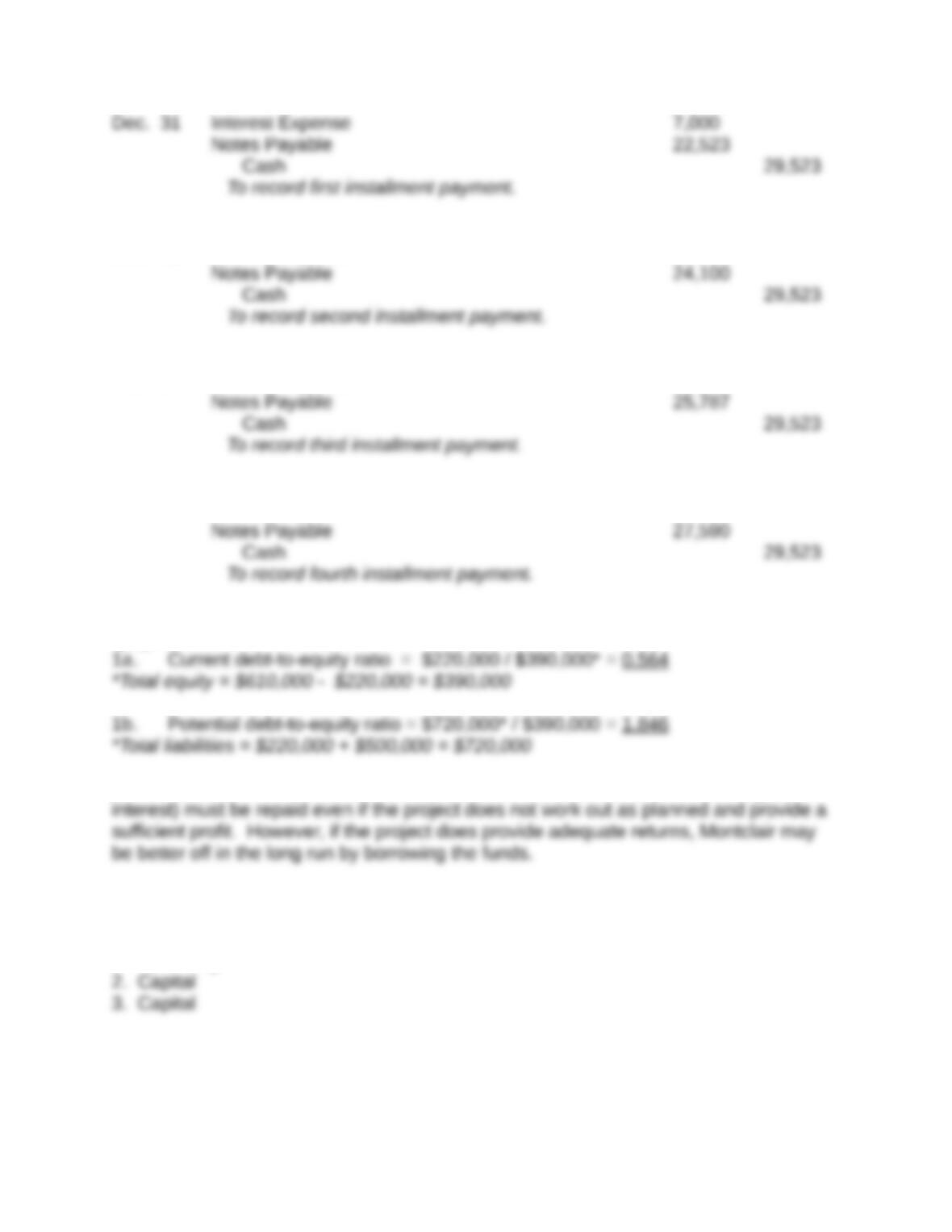

Title: Exercise 14-16

QA_Ori:

2. Montclair’s risk will increase because it will have more debt. That debt (plus

Title: Exercise 14-17

QA_Ori:

1. Operating

Title: Exercise 14-18

QA_Ori:

1. Leased Asset—Office Equipment 41,000

2. Depreciation Expense—Office Equipment 8,200

Title: Exercise 14-19

QA_Ori:

[Note: 12% / 12 months = 1% per month as the relevant interest rate.]

Analysis: Option 2 has the lowest present value at $38,035 and, thus, is the best lease

deal.

Title: Exercise 14-20

QA_Ori:

1. Cash 1,920

2. Loans and Borrowings 3,000

3. Heineken’s Loans and Borrowings carried a premium of € 78 as of December 31,

2010. This is computed as its carrying value of € 8,078 less its par value of € 8,000.

4. The contract rate was higher than the market rate at issuance. This is implied

(Recall: Contract rate > Market rate Premium)