Chapter 22

Master Budgets and Planning

QUESTIONS

1. A budget helps managers control and monitor a business by 1) communicating

plans to employees, 2) coordinating the activities of different parts of the

2. Two common benchmarks used by managers to evaluate performance are: past

3. Continuous budgeting provides managers a full set of updated budgets each time a

4. Three common short-term horizons for planning and budgeting purposes are:

monthly, quarterly, and annually. A semiannual planning horizon is also popular.

5. Budgeting can be a strong positive motivating force if employees are involved or

consulted in the process. This participation promotes their commitment to reaching

6. Budgeting helps management coordinate and plan business activities by providing

7. The sales budget reflects the expected sales to be made over a period of time, stated

8. A selling expense budget is a plan of the expenses to be incurred to produce the

Fundamental Accounting Principles, 21st Edition

1264

9. Budgeting promotes good decision making by requiring managers to conduct

research (or analysis) and by focusing their attention on the future.

10. A cash budget shows the planned cash receipts and cash disbursements for each

budget period, including any loans to be received or repaid. Since the operating

11. A production budget shows the number of units to be produced each budget period.

12. A manager of an Apple store would have responsibility for and decision control over

13. With the exception of the decision to operate, the manager of an Arctic Cat

distribution center is not likely to engage in a substantial amount of long-term

14.

Budget Participant

Description

Sales manager ………………..

Information on estimated sales (units and dollars).

Production manager ………..

Number of units to produce based on estimated sales.

Manufacturing manager …..

Amount of direct materials, direct labor, and

manufacturing overhead to produce the estimated level

of production.

Sales manager ………………..

Cost of selling the estimated sales level.

General & admini-

strative managers …………...

Cost to support operations; most often are fixed costs.

Capital expenditures

committee ……………………...

Prepare plans to have available plant assets necessary

to carry on business activities.

Cash managers ……………....

Working with the above budgets, this team will prepare

cash flow analysis.

Accounting and finance

staff ……………………………....

Financial budgets prepared from above information.

QUICK STUDIES

Quick Study 22-1 (5 minutes)

Quick Study 22-2 (10 minutes)

Three useful guidelines to help motivate employees with budgeting are

Quick Study 22-3 (15 minutes)

Montel Company

Computation of Budgeted Cost of Purchases

For Month Ended July 31

Budgeted ending inventory ……………………………………………………….

$ 40,000

Budgeted cost of goods to be sold [$600,000 x (1 – 40%)] …………………

360,000

Required available merchandise …………………………………………….…………

400,000

Less budgeted beginning inventory ……………………………………….…………

50,000

Budgeted cost of purchases ………………………………………………….……

$350,000

Quick Study 22-4 (10 minutes)

1. The bottom-up approach to budgeting is considered more successful

because without active employee involvement in preparing budget

2. Examples of bottom-up budgeting include

• Involving the sales department in preparing sales estimates.

• Involving the production department in preparing its own expense

budget.

Quick Study 22-5 (15 minutes)

Computation of budgeted Accounts Receivable balance as of July 31

Sales month

Total Sales

Credit

Sales*

Percent Still

Uncollected*

Amount

Uncollected

June ……………..….

$420,000

$168,000

10%

$ 16,800

July ………………….

398,000

159,200

80%

127,360

Total …………….….

$144,160

* Credit sales are 40% of total sales—of these credit sales, 20% are collected in the sale month,

70% are collected in the month after sale, and 10% are collected in the second month after sale.

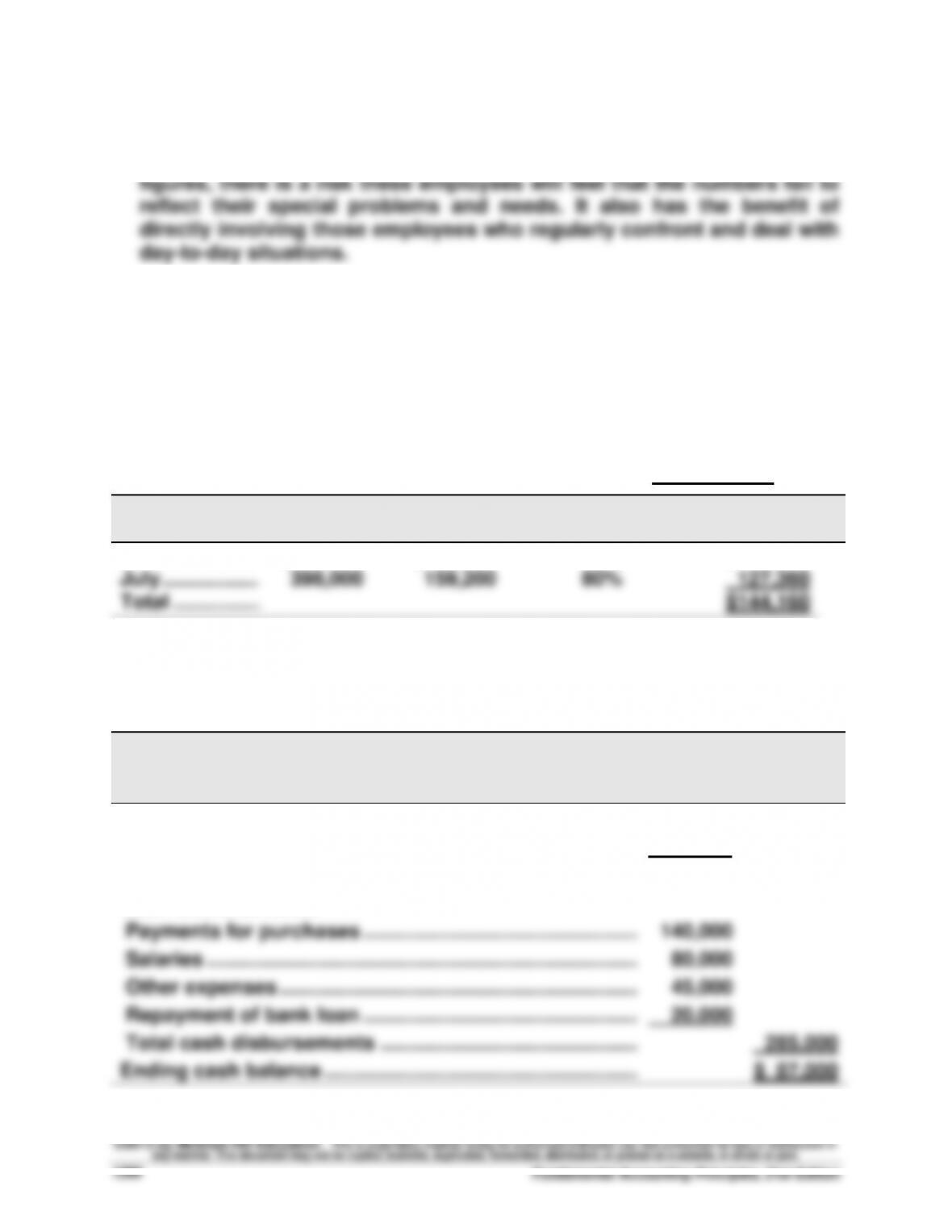

Quick Study 22-6 (15 minutes)

Gado Merchandising Company

Cash Budget

For Month Ended March 31

Beginning cash balance ………………………………………………….

$ 72,000

Cash receipts from sales ………………………………………….…….

300,000

Total cash available ………………………………………………….……

$372,000

Cash disbursements

Payments for purchases ………………………………………….…….

140,000

Salaries …………………………………………………………………..…….

80,000

Other expenses …………………………..…………………………..

45,000

Repayment of bank loan ………………………………………….…….

20,000

Total cash disbursements ……………………………………….…….

285,000

Ending cash balance ………………………………………………..…….

$ 87,000

Quick Study 22-7 (10 minutes)

1. Activity-based budgeting requires managers to focus on the activities of

2. Traditional budgeting consists of listing the amount of resources

Quick Study 22-8 (15 minutes)

Forrest Company

Production Budget

For Month Ended November 30

Next month’s budgeted sales ……………………………………………………...

350,000

Ratio of inventory to future sales ………………………………………………...

x 10%

Budgeted ending inventory ……………………………………………………….

35,000

Add budgeted sales for the month ……………………………………………...

400,000

Required units of available production ………………………………………..

435,000

Less beginning inventory …………………………………………………………...

40,000

Units to be produced …………………………………………………………………..

395,000

Fundamental Accounting Principles, 21st Edition

1268

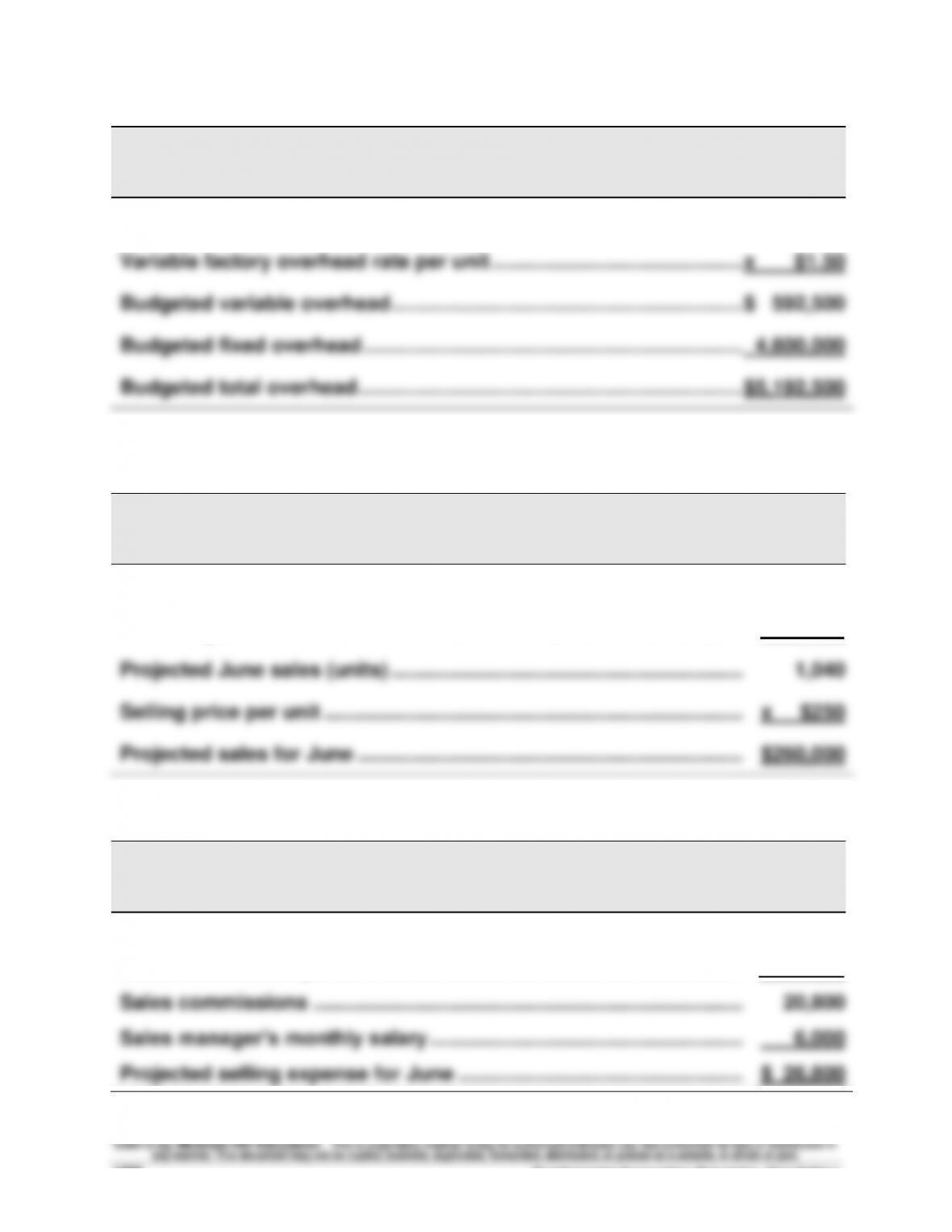

Quick Study 22-9 (15 minutes)

Forrest Company

Factory Overhead Budget

For Month Ended November 30

Units to be produced (from QS 22-8) …………………………………………...

395,000

Variable factory overhead rate per unit ………………………………………..

x $1.50

Budgeted variable overhead ……………………………………………………….

$ 592,500

Budgeted fixed overhead …………………………………………………………....

4,600,000

Budgeted total overhead ……………………………………………………………..

$5,192,500

Quick Study 22-10 (10 minutes)

Grace

Sales Budget

For Month Ended June 30

Prior month’s unit sales ……………………………………………………………...

1,000

Plus 4% growth in unit sales ……………………………………………………....

40

Projected June sales (units) ……………………………………………………….

1,040

Selling price per unit …………………………………………………………………..

x $250

Projected sales for June ……………………………………………………………..

$260,000

Quick Study 22-11 (10 minutes)

Grace

Selling Expense Budget

For Month Ended June 30

Budgeted sales (from QS 22-10) ………………………………………………....

$260,000

Sales commission percent ………………………………………………………....

x 8%

Sales commissions …………………………………………………………………....

20,800

Sales manager’s monthly salary ………………………………………………....

6,000

Projected selling expense for June ……………………………………………..

$ 26,800

Quick Study 22-12 (10 minutes)

Grace

Budgeted Cash Receipts

For Month Ended June 30

Budgeted sales (from QS 22-10) ………………………………………………....

$260,000

Less ending accounts receivable ($260,000 x 0.40) ……………………...

104,000

Cash sales ($260,000 x 0.60)) ……………………………………………………...

156,000

Collections of last month’s receivables* ……………………………………...

100,000

Total cash receipts ……………………………………………………………………..

$256,000

*$250,000 x 40% = $100,000. Last month’s sales of $250,000 from QS 22-10.

Quick Study 22-13 (15 minutes)

Sales …………………………..…………………………………………………………….. BIS

Office salaries paid ……………………………………………………………………. BIS

Quick Study 22-14 (10 minutes)

CANDLE SHOPPE

Cash Receipts Budget

For Month Ended September 30

Cash receipts from September cash sales (40% x $170,000) ………...

$ 68,000

Collection of prior month’s receivables (60% x $150,000) …………....

90,000

Total cash receipts ……………………………………………………………………..

$158,000

Fundamental Accounting Principles, 21st Edition

1270

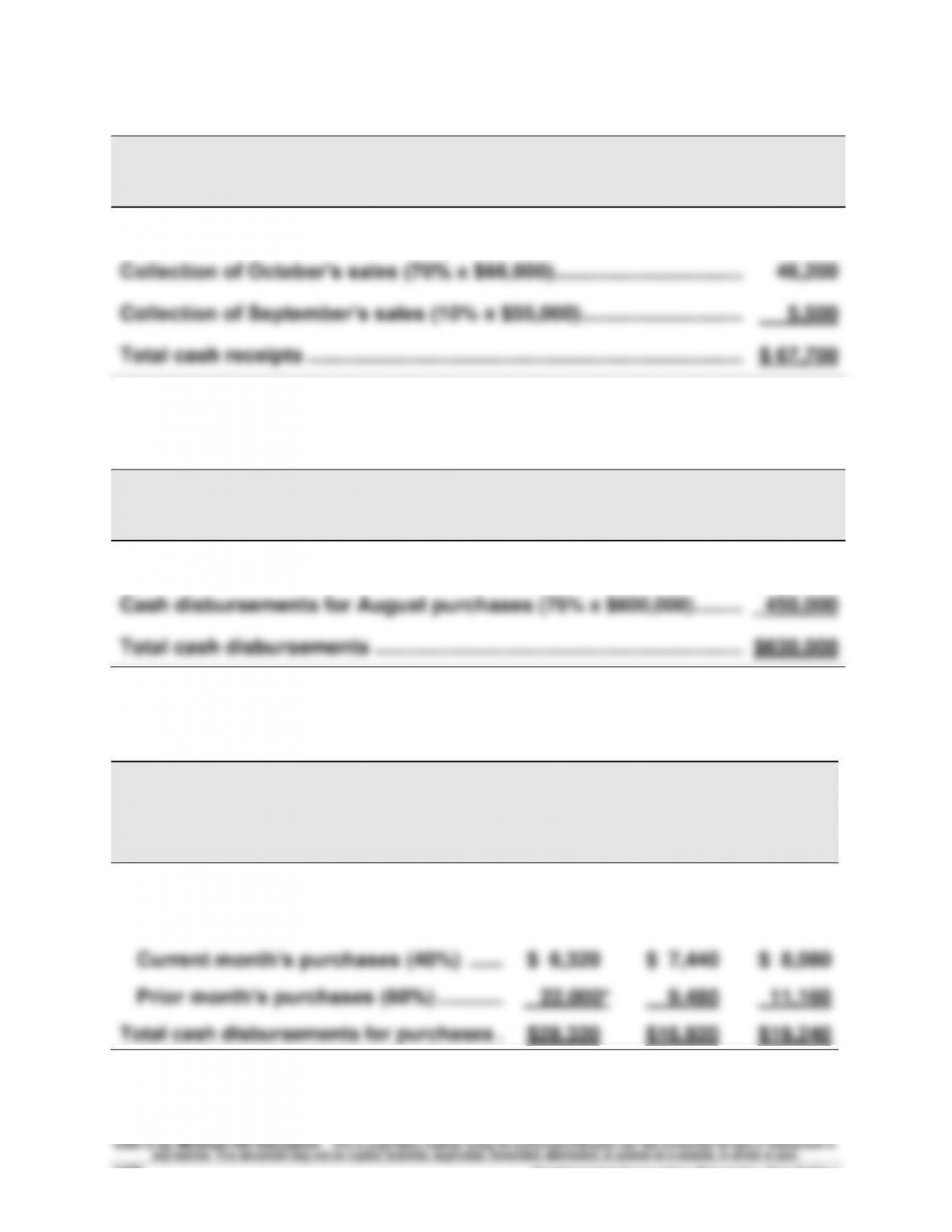

Quick Study 22-15 (10 minutes)

WELLS COMPANY

Budgeted Cash Receipts

For Month Ended November 30

Cash receipts from November cash sales (20% x $80,000) …………...

$ 16,000

Collection of October’s sales (70% x $66,000) ……………………………...

46,200

Collection of September’s sales (10% x $55,000) ………………………....

5,500

Total cash receipts ……………………………………………………………………..

$ 67,700

Quick Study 22-16 (10 minutes)

GORDANDS

Cash Disbursements for Merchandise (Budgeted)

For Month Ended September 30

Cash disbursements for September purchases (25% x $720,000) ....

$180,000

Cash disbursements for August purchases (75% x $600,000) ………..

450,000

Total cash disbursements …………………………………………………………..

$630,000

Quick Study 22-17 (10 minutes)

MEYER CO.

Cash Disbursements for Merchandise (Budgeted)

For January, February, and March

January

February

March

Purchases …………………………………………..…

$15,800

$18,600

$20,200

Cash disbursements for

Current month’s purchases (40%) ………

$ 6,320

$ 7,440

$ 8,080

Prior month’s purchases (60%) ……………

22,000*

9,480

11,160

Total cash disbursements for purchases ..…

$28,320

$16,920

$19,240

* Accounts payable balance at December 31

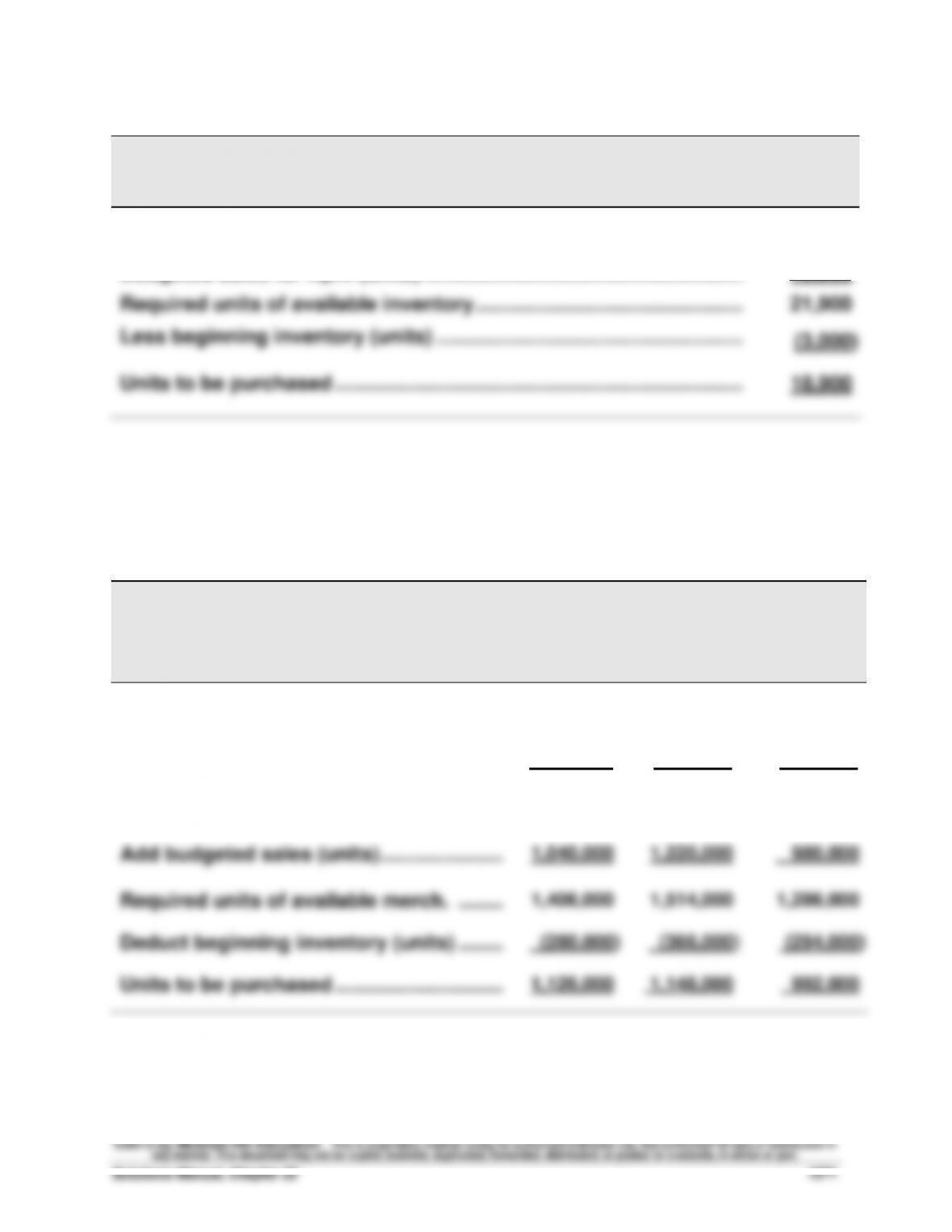

Quick Study 22-18 (5 minutes)

RAIDER-X CORP.

Purchases Budget (in units)

For Month Ended April 30

Budgeted ending inventory (130% x 3,000) …………………………………..

3,900

Budgeted sales for April (units) …………………………………………………..

18,000

Required units of available inventory …………………………………………..

Less beginning inventory (units) ………………………………………………...

21,900

(3,000)

Units to be purchased ………………………………………………………………...

18,900

Quick Study 22-19 (15 minutes)

LEXI COMPANY

Merchandise Purchases Budget

For April, May, and June

April

May

June

Next month’s budgeted sales (units) ………

1,220,000

980,000

1,020,000

Ratio of inventory to future sales ……………

x 30%

x 30%

x 30%

Budgeted ending inventory (units) …………

366,000

294,000

306,000

Add budgeted sales (units) ………………….…

1,040,000

1,220,000

980,000

Required units of available merch. ……..…

1,406,000

1,514,000

1,286,000

Deduct beginning inventory (units) ……..…

(280,000)

(366,000)

(294,000)

Units to be purchased …………………………..

1,126,000

1,148,000

992,000

Fundamental Accounting Principles, 21st Edition

1272

Quick Study 22-20 (10 minutes)

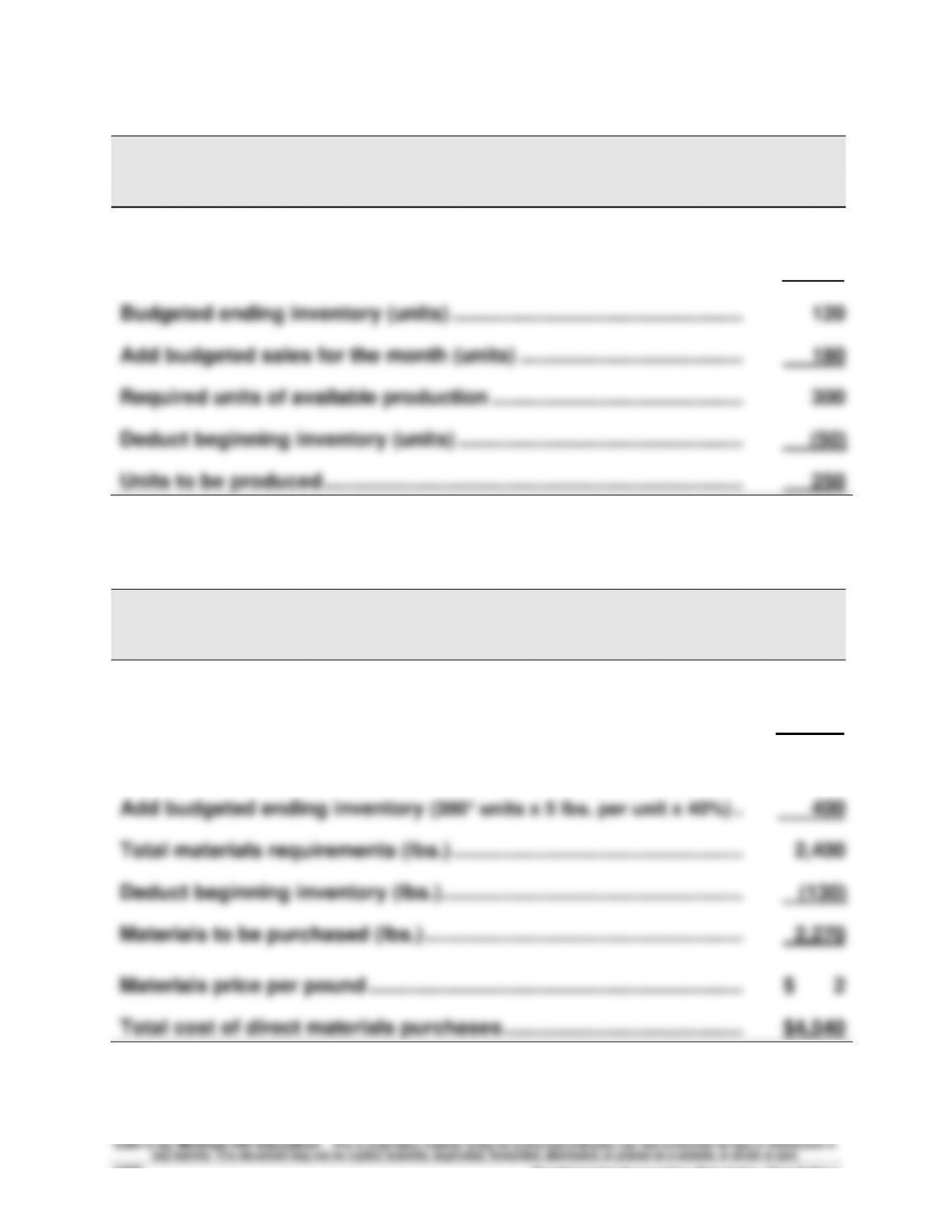

CHAMP, INC.

Production Budget

For Month Ended May 31

Next month’s budgeted sales (units) …………………………………………...

200

Ratio of inventory to future sales ………………………………………………...

x 60%

Budgeted ending inventory (units) ……………………………………………...

120

Add budgeted sales for the month (units) …………………………………...

180

Required units of available production ………………………………………..

300

Deduct beginning inventory (units) ……………………………………………..

(50)

Units to be produced …………………………………………………………………..

250

Quick Study 22-21 (10 minutes)

ZORTEK CORP.

Direct Materials Budget

For Month Ended January 31

Budget production (units) …………………………………………………………...

400

Materials requirements per unit …………………………………………………..

x 5 lbs.

Materials needed for production (lbs.) ………………………………………...

2,000

Add budgeted ending inventory (200* units x 5 lbs. per unit x 40%) ....

400

Total materials requirements (lbs.) ……………………………………………...

2,400

Deduct beginning inventory (lbs.) ………………………………………………..

(130)

Materials to be purchased (lbs.) …………………………..……………………...

2,270

Materials price per pound …………………………………………………………...

$ 2

Total cost of direct materials purchases ……………………………………...

$4,540

*February’s budgeted production.

Quick Study 22-22 (5 minutes)

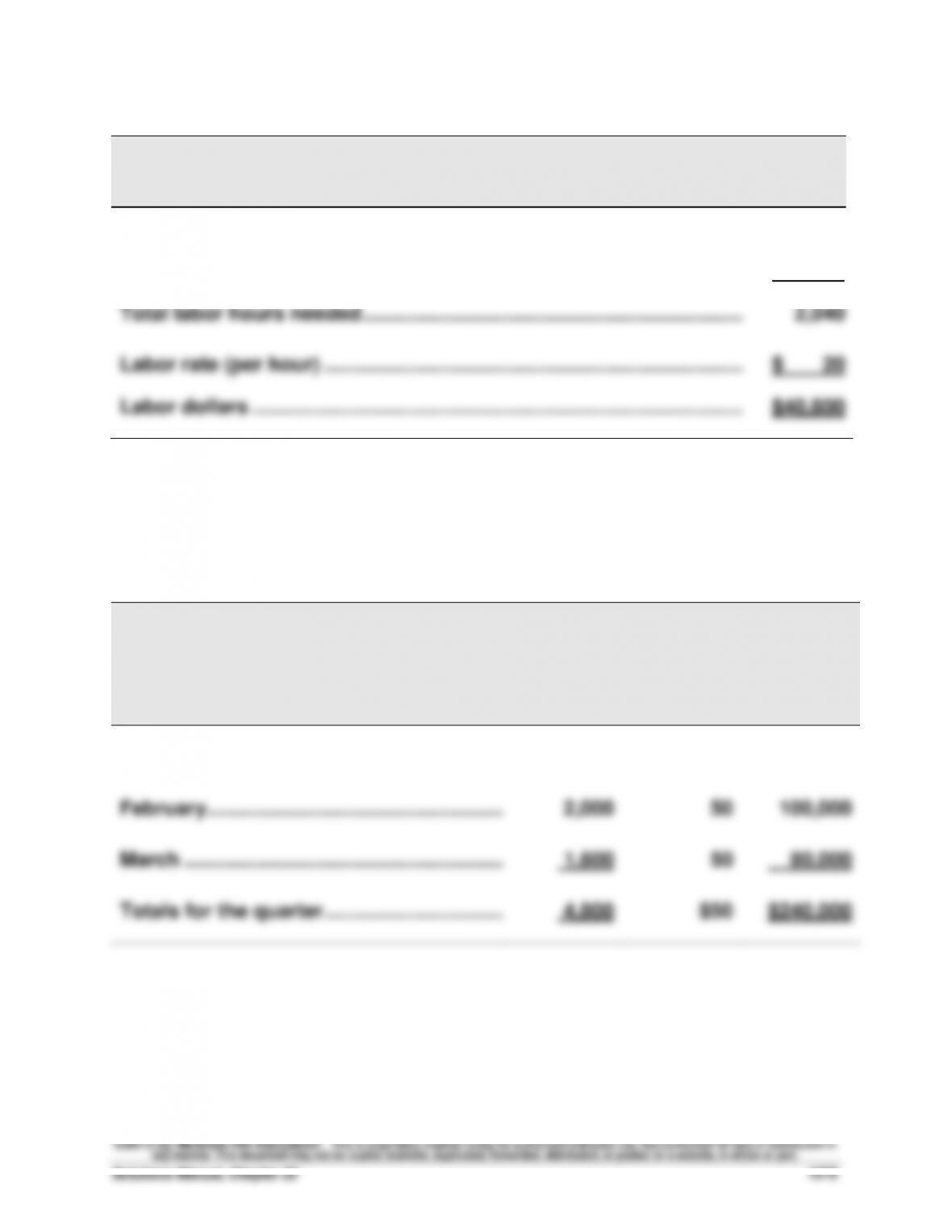

TORA CO.

Direct Labor Budget

For Month Ended July 31

Budget production (units) …………………………………………………………...

1,020

Labor requirements per unit (hours) …………………………………………...

x 2

Total labor hours needed …………………………………………………………....

2,040

Labor rate (per hour) …………………………………………………………………..

$ 20

Labor dollars ……………………………………………………………………………...

$40,800

Quick Study 22-23 (10 minutes)

SCORA INC.

Sales Budget

For January, February, and March

Budgeted

Unit Sales

Budgeted

Unit Price

Budgeted

Total Sales

January …………………………………………………

1,200

$50

$ 60,000

February ……………………………………………..…

2,000

50

100,000

March ……………………………………………………

1,600

50

80,000

Totals for the quarter …………………………..

4,800

$50

$240,000

Fundamental Accounting Principles, 21st Edition

1274

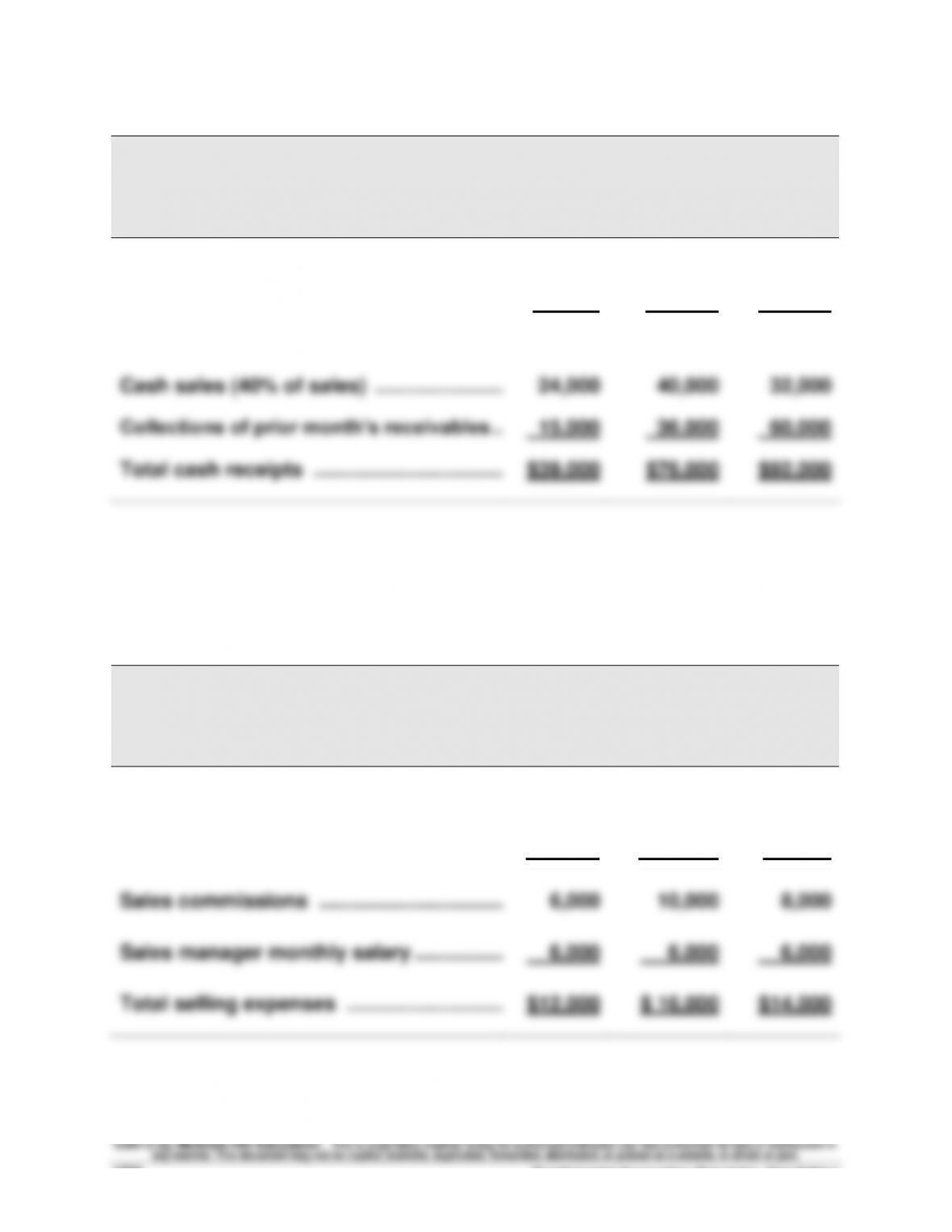

Quick Study 22-24 (10 minutes)

SCORA INC.

Cash Receipts Budget

For January, February, and March

January

February

March

Sales (from QS 22-23) …………………………..

$60,000

$100,000

$80,000

Less ending accts. receivable (60%) ………

36,000

60,000

48,000

Cash receipts from

Cash sales (40% of sales) …………………..…

24,000

40,000

32,000

Collections of prior month’s receivables ……

15,000

36,000

60,000

Total cash receipts …………………………….…

$39,000

$76,000

$92,000

Quick Study 22-25 (10 minutes)

SCORA INC.

Selling Expense Budget

For January, February, and March

January

February

March

Budgeted sales (from QS 22-23) ………….…

$60,000

$100,000

$80,000

Sales commission percent ………………….…

x 10%

x 10%

x 10%

Sales commissions ………………………………

6,000

10,000

8,000

Sales manager monthly salary …………….…

6,000

6,000

6,000

Total selling expenses ……………………….…

$12,000

$ 16,000

$14,000

Quick Study 22-26 (5 minutes)

MESSERS COMPANY

Cash Budget

For Month Ended February 28

Beginning cash balance ……………………………………………………………...

$ 20,000

Cash receipts ……………………………………………………………………………..

75,000

Total cash available ……………………………………………………….…………...

95,000

Cash disbursements…………………………………………………………………...

(100,250)

Preliminary cash balance ……………………………………………………….…...

$ (5,250)

Additional loan from bank …………………………………………………………..

10,250

Ending cash balance …………………………………………………………………..

$ 5,000

Based on the cash budget above, the company must borrow $10,250 during

February to maintain a $5,000 cash balance.

Quick Study 22-27 (10 minutes)

1.

Sales (current year) ………………………………………………………..

(in € millions)

€25,400

Sales growth (€25,400 x 3%) ……………………………………………

762

Budgeted sales (next year) ……………………………………………..

€26,162

2.

Note: Assume sales of €26,000 for this question.

Budgeted selling expenses (€26,000 x 20%) …………………….

€5,200

Budgeted general and admin. expenses (€26,000 x 4%) …..

1,040

EXERCISES

Exercise 22-1 (25 minutes)

KAYAK COMPANY

Cash Budget

For January, February, and March

January

February

March

Beginning cash balance …………………………

$ 30,000

$ 30 ,000

$ 69,294

Cash receipts ……………………………………..…

525,000

400,000

450,000

Total cash available …………………………….…

555,000

430,000

519,294

Cash disbursements………………………………

475,000

350,000

525,000

Interest expense

January ($60,000 x 1%) …………………….…

600

February ($10,600 x 1%) …………………….…

________

106

________

Preliminary cash balance …………………….…

79,400

79,894

(5,706)

Additional loan from bank …………………..…

35,706

Repayment of loan to bank ………………….…

(49,400)

(10,600)

________

Ending cash balance …………………………..

$ 30,000

$ 69,294

$ 30,000

Ending loan balance*…………………………..

$ 10,600

$ 0

$ 35,706

*Loan balance is $60,000 at the beginning of January. January’s ending loan balance is

computed as $60,000 – 49,400.

Exercise 22-2 (30 minutes)

1. Merchandise Purchases Budget

Note: Shaded numbers represent known information provided in the exercise.

Walker Company

Merchandise Purchases Budget

For July, August, and September

July

August

September

Next month’s budgeted sales …………..

315,000

270,000

200,000

(10)

Ratio of inventory to next month sales .

x 15%

(9)

x 15%

(9)

x 15%

(9)

Budgeted ending inventory ……………..

47,250

(6)

40,500

(3)

30,000

Add budgeted sales for month …………

180,000

315,000

270,000

Required units available inventory …..

227,250

(7)

355,500

(4)

300,000

(1)

Less beginning inventory ………………..

27,000

(8)

47,250

(5)

40,500

(2)

Budgeted merchandise purchases …..

200,250

308,250

259,500

The following notes (1) through (10) provide supporting calculations and explanations.

Notes: (1) September required units

Ending inventory

30,000

Add budgeted sales

270,000

Total required in September

300,000

(2) September beginning Inventory

Total required (1 above)

300,000

Less budgeted purchases

(259,500)

September beginning inventory

40,500

(3) September Beginning Inventory = August Ending Inventory

(4) August required units

Ending inventory

40,500

Add budgeted sales

315,000

Total required in August

355,500