Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Fundamental Accounting Principles, 21st Edition

1308

Problem 22-5A (Continued)

Part 6

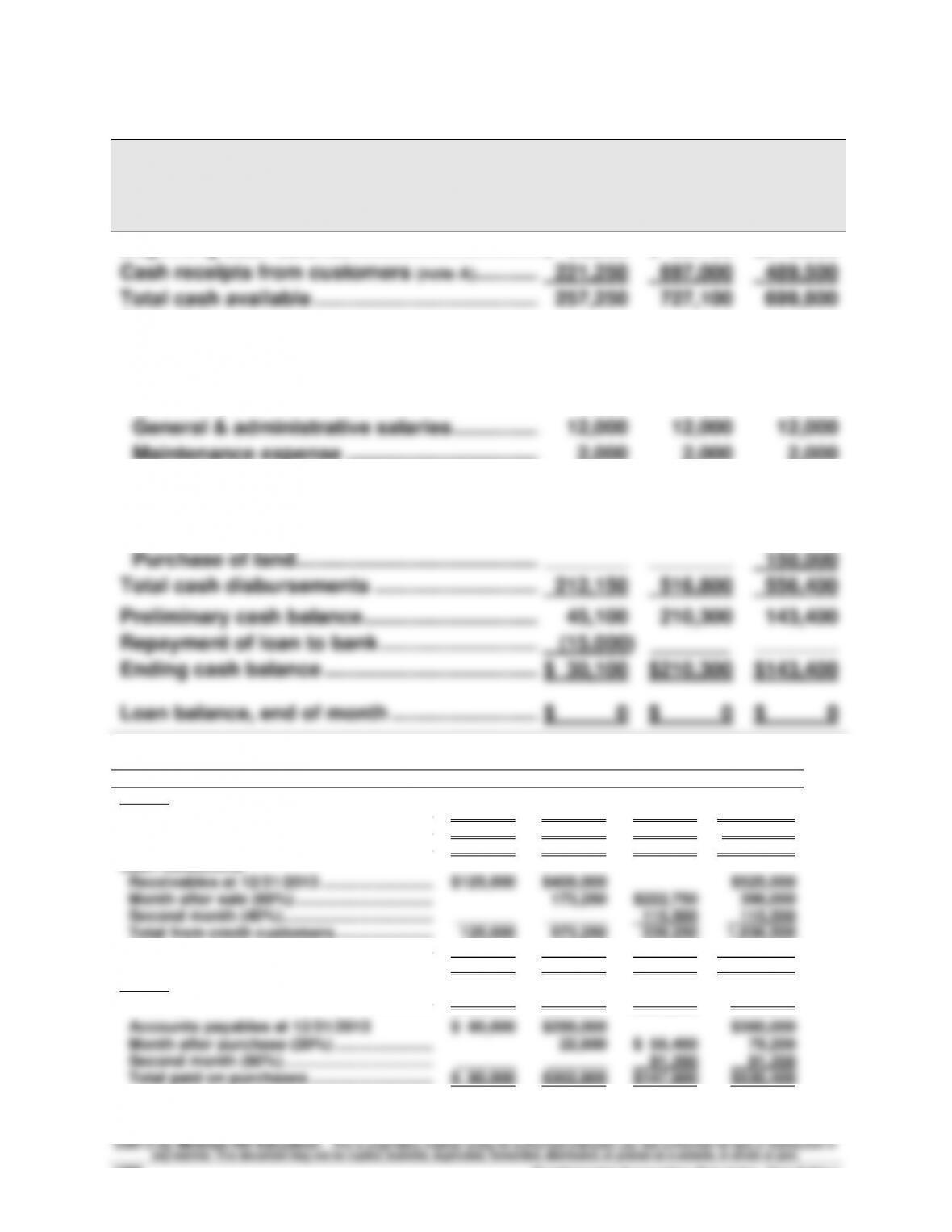

DIMSDALE SPORTS CO.

Cash Budgets

January, February, and March 2014

January

February

March

Beginning cash balance ......................................

$ 36,000

$ 30,100

$210,300

Cash receipts from customers (note A)................

221,250

697,000

489,500

Total cash available .............................................

257,250

727,100

699,800

Cash disbursements

Payments for merchandise (note B) ...................

80,000

302,800

147,600

Sales commissions ...........................................

77,000

99,000

121,000

Sales salaries .....................................................

5,000

5,000

5,000

General & administrative salaries ....................

12,000

12,000

12,000

Maintenance expense .......................................

2,000

2,000

2,000

Interest ($15,000 x 1%) ............................................

150

Taxes payable ....................................................

90,000

Purchases of equipment ................................

36,000

96,000

28,800

Purchase of land ................................................

________

________

150,000

Total cash disbursements ................................

212,150

516,800

556,400

Preliminary cash balance ................................

45,100

210,300

143,400

Repayment of loan to bank ................................

(15,000)

_______

________

Ending cash balance ...........................................

$ 30,100

$210,300

$143,400

Loan balance, end of month ...............................

$ 0

$ 0

$ 0

Supporting calculations

January

February

March

Total

Note A: Cash receipts from customers

Total sales .........................................................

$385,000

$495,000

$605,000

$1,485,000

Cash sales (25%) ..............................................

96,250

123,750

151,250

371,250

Credit sales (75%) ............................................

288,750

371,250

453,750

1,113,750

Cash collections

Receivables at 12/31/2013 ...............................

$125,000

$400,000

$525,000

Month after sale (60%) ................................

173,250

$222,750

396,000

Second month (40%) ........................................

_______

_______

115,500

115,500

Total from credit customers ............................

125,000

573,250

338,250

1,036,500

Cash sales.........................................................

96,250

123,750

151,250

371,250

Total cash received ..........................................

$221,250

$697,000

$489,500

$1,407,750

Note B: Cash payments for merchandise

Credit purchases ..............................................

$114,000

$282,000

$324,000

$720,000

Accounts payables at 12/31/2013

$ 80,000

$280,000

$360,000

Month after purchase (20%) ............................

22,800

$ 56,400

79,200

Second month (80%) ........................................

_______

_______

91,200

91,200

Total paid on purchases ................................

$ 80,000

$302,800

$147,600

$530,400

Problem 22-5A (Continued)

Part 7

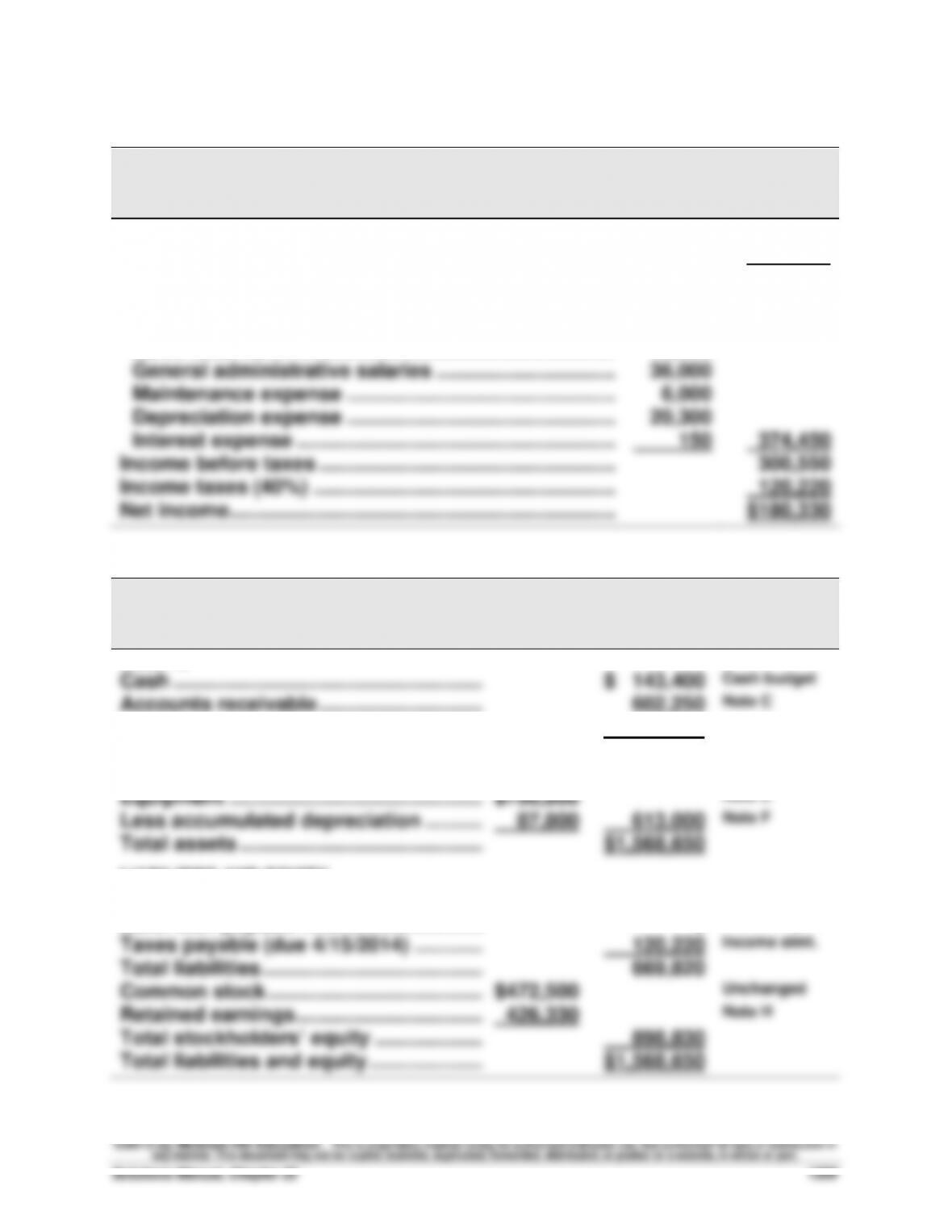

DIMSDALE SPORTS CO.

Budgeted Income Statement

For Three Months Ended March 31, 2014

Sales ................................................................................

$1,485,000

Cost of goods sold (27,000 units @ $30) .....................

810,000

Gross profit ....................................................................

675,000

Operating expenses

Sales commissions .....................................................

$297,000

Sales salaries ...............................................................

15,000

General administrative salaries ................................

36,000

Maintenance expense .................................................

6,000

Depreciation expense .................................................

20,300

Interest expense ..........................................................

150

374,450

Income before taxes ......................................................

300,550

Income taxes (40%) .......................................................

120,220

Net income ......................................................................

$180,330

Part 8

DIMSDALE SPORTS CO.

Budgeted Balance Sheet

March 31, 2014

ASSETS

Cash ............................................................

$ 143,400

Cash budget

Accounts receivable ................................

602,250

Note C

Inventory .....................................................

60,000

Note D

Total current assets ................................

805,650

Land ............................................................

150,000

Capital budget

Equipment ..................................................

$700,800

Note E

Less accumulated depreciation ...............

87,800

613,000

Note F

Total assets ................................................

$1,568,650

LIABILITIES AND EQUITY

Accounts payable ......................................

$ 549,600

Note G

Bank loan payable .....................................

0

Cash budget

Taxes payable (due 4/15/2014) .................

120,220

Income stmt.

Total liabilities ............................................

669,820

Common stock ...........................................

$472,500

Unchanged

Retained earnings ......................................

426,330

Note H

Total stockholders’ equity ........................

898,830

Total liabilities and equity .........................

$1,568,650

Fundamental Accounting Principles, 21st Edition

1310

Problem 22-5A (Concluded)

Supporting Footnotes

Note C

Beginning receivables ......................................................

$ 525,000

Credit sales ........................................................................

1,113,750

Less collections ................................................................

(1,036,500)

Ending receivables ............................................................

$ 602,250

Note D

Beginning inventory ..........................................................

$ 150,000

Purchases ..........................................................................

720,000

Less cost of goods sold ...................................................

(810,000)

Ending inventory* ..............................................................

$ 60,000

*Also equals 2,000 units @ $30 = $60,000

Note E

Beginning equipment ........................................................

$ 540,000

Purchased in January .......................................................

36,000

Purchased in February......................................................

96,000

Purchased in March ..........................................................

28,800

Total ...................................................................................

$ 700,800

Note F

Beginning accumulated depreciation ..............................

$ 67,500

Depreciation expense .......................................................

20,300

Total ...................................................................................

$ 87,800

Note G

Beginning accounts payable ............................................

$ 360,000

Purchases ..........................................................................

720,000

Payments ...........................................................................

(530,400)

Ending accounts payable .................................................

$ 549,600

Note H

Beginning retained earnings ............................................

$ 246,000

Net income .........................................................................

180,330

Total ...................................................................................

$ 426,330

Problem 22-6A (40 minutes)

Part 1

BLACK DIAMOND COMPANY

Production Budget (in units)

Third Quarter

Budgeted ending inventory (skis) .........................................................

3,500

Add budgeted sales ................................................................................

150,000

Required units of available production ................................................

153,500

Deduct beginning inventory (skis) ........................................................

(5,000)

Units to be manufactured ................................................................

148,500

Part 2

BLACK DIAMOND COMPANY

Direct Materials Budget (in lbs, except where noted)

Third Quarter

Materials (carbon fiber) needed for production (148,500 x 2) ........

297,000

Add budgeted ending inventory (carbon fiber) ...............................

4,000

Total materials (carbon fiber) requirements ....................................

301,000

Deduct beginning inventory (carbon fiber) ......................................

(6,000)

Units of materials (carbon fiber) to be purchased ...........................

295,000

Materials cost per pound ...................................................................

$15

Total cost of materials purchases (295,000 x $15) ..........................

$4,425,000

Fundamental Accounting Principles, 21st Edition

1312

Problem 22-6A (concluded)

Part 3

BLACK DIAMOND COMPANY

Direct Labor Budget

Third Quarter

Units to be produced ...............................................................

148,500

Labor requirements per unit (hours) ................................

x 0.50

Total labor hours needed ........................................................

74,250

Labor rate (per hour) ...............................................................

x $20

Labor dollars ............................................................................

$1,485,000

Part 4

BLACK DIAMOND COMPANY

Factory Overhead Budget

Third Quarter

Total labor hours needed ........................................................

74,250

Variable overhead rate per DL hour .......................................

x $8

Budgeted variable overhead ...................................................

$ 594,000

Budgeted fixed overhead ........................................................

1,782,000

Budgeted total overhead .........................................................

$2,376,000

Problem 22-7A (130 minutes)

Part 1

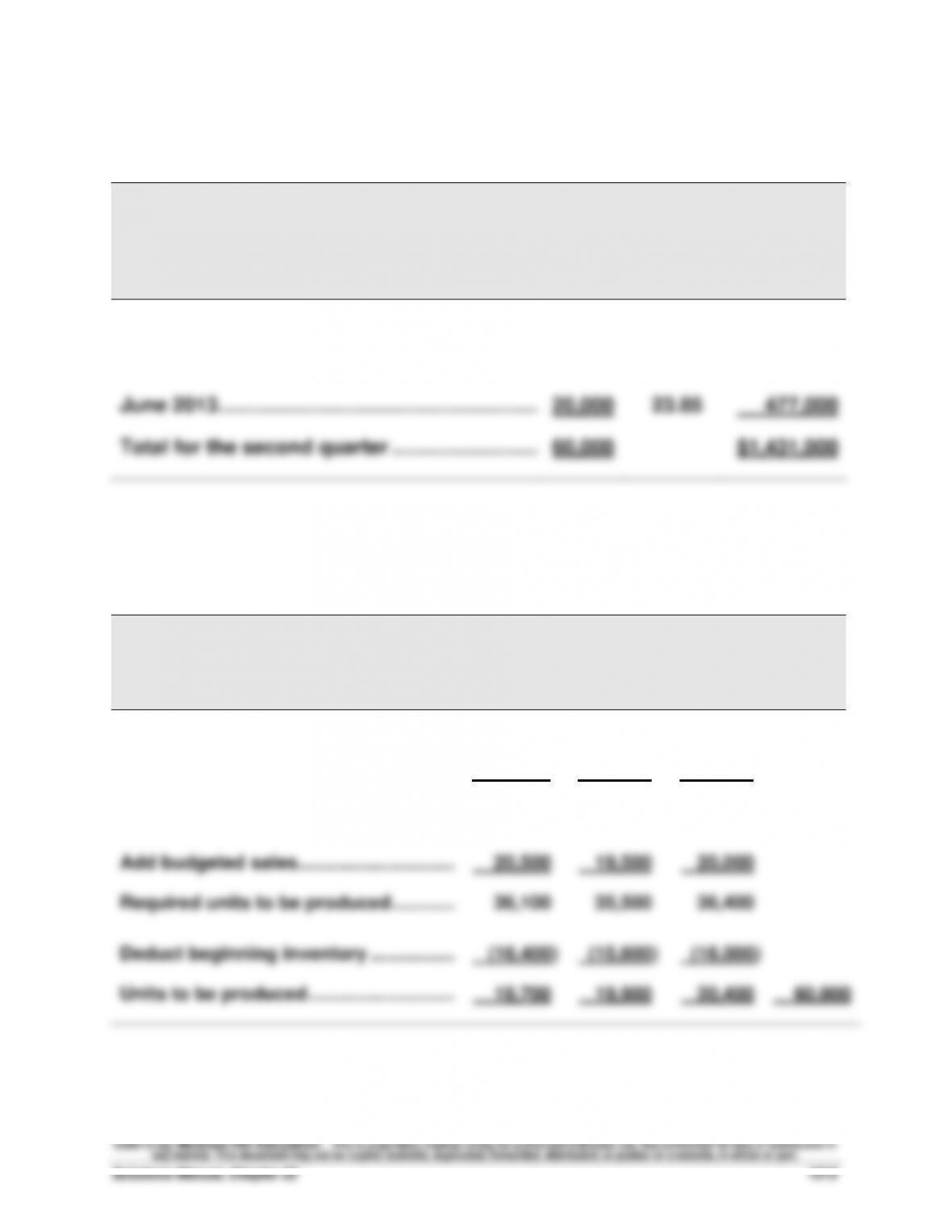

ZIGBY MANUFACTURING

Sales Budgets

April, May, and June 2013

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

April 2013 ..............................................................

20,500

$23.85

$ 488,925

May 2013 ...............................................................

19,500

23.85

465,075

June 2013 ..............................................................

20,000

23.85

477,000

Total for the second quarter ...............................

60,000

$1,431,000

Part 2

ZIGBY MANUFACTURING

Production Budget

April, May, and June 2013

April

May

June

Total

Next month’s budgeted sales ...............

19,500

20,000

20,500

Ratio of inventory to future sales .........

x 80%

x 80%

x 80%

Budgeted ending inventory ..................

15,600

16,000

16,400

Add budgeted sales ...............................

20,500

19,500

20,000

Required units to be produced .............

36,100

35,500

36,400

Deduct beginning inventory .................

(16,400)

(15,600)

(16,000)

Units to be produced .............................

19,700

19,900

20,400

60,000

Fundamental Accounting Principles, 21st Edition

1314

Problem 22-7A (continued)

Part 3

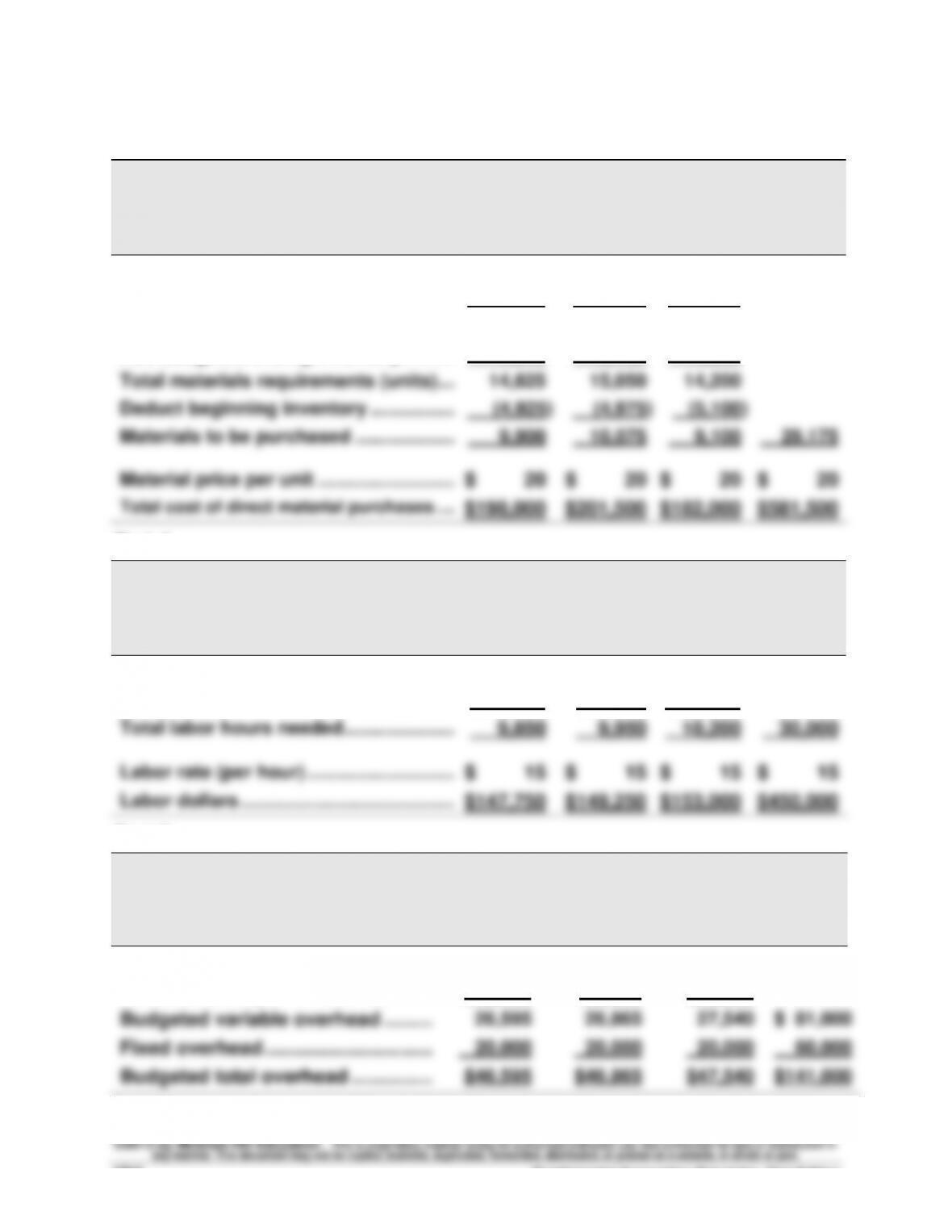

ZIGBY MANUFACTURING

Raw Materials Budget

April, May, and June 2013

April

May

June

Total

Production budget (units) .....................

19,700

19,900

20,400

Materials requirement per unit .............

x 0.50

x 0.50

x 0.50

Materials needed for production ..........

9,850

9,950

10,200

Add budgeted ending inventory ...........

4,975

5,100

4,000

Total materials requirements (units) ....

14,825

15,050

14,200

Deduct beginning inventory .................

(4,925)

(4,975)

(5,100)

Materials to be purchased ....................

9,900

10,075

9,100

29,175

Material price per unit ...........................

$ 20

$ 20

$ 20

$ 20

Total cost of direct material purchases .....

$198,000

$201,500

$182,000

$581,500

Part 4

ZIGBY MANUFACTURING

Direct Labor Budget

April, May, and June 2013

April

May

June

Total

Budgeted production (units) ................

19,700

19,900

20,400

Labor requirements per unit (hours) ....

x 0.50

x 0.50

x 0.50

Total labor hours needed ......................

9,850

9,950

10,200

30,000

Labor rate (per hour) .............................

$ 15

$ 15

$ 15

$ 15

Labor dollars ..........................................

$147,750

$149,250

$153,000

$450,000

Part 5

ZIGBY MANUFACTURING

Factory Overhead Budget

April, May, and June 2013

April

May

June

Total

Labor hours needed .............................

9,850

9,950

10,200

Variable factory overhead rate ............

x $2.70

x $2.70

x $2.70

Budgeted variable overhead ...............

26,595

26,865

27,540

$ 81,000

Fixed overhead ................................

20,000

20,000

20,000

60,000

Budgeted total overhead .....................

$46,595

$46,865

$47,540

$141,000

Problem 22-7A (continued)

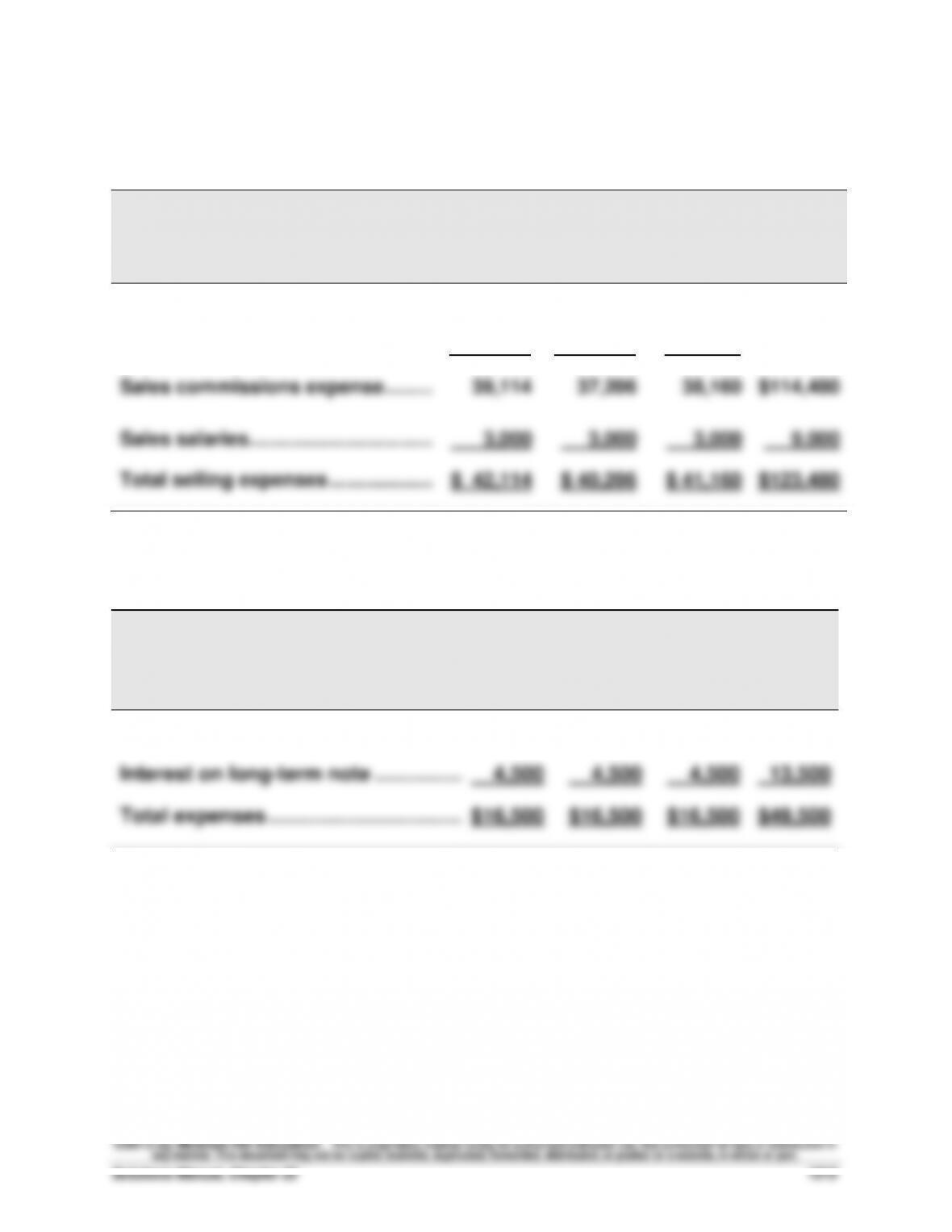

Part 6

ZIGBY MANUFACTURING

Selling Expense Budgets

April, May, and June 2013

April

May

June

Total

Budgeted sales ................................

$488,925

$465,075

$477,000

Sales commission percent ..................

x 8%

x 8%

x 8%

Sales commissions expense ...............

39,114

37,206

38,160

$114,480

Sales salaries........................................

3,000

3,000

3,000

9,000

Total selling expenses .........................

$ 42,114

$ 40,206

$ 41,160

$123,480

Part 7

ZIGBY MANUFACTURING

General and Administrative Expense Budgets

April, May, and June 2013

April

May

June

Total

Salaries .......................................................

$12,000

$12,000

$12,000

$36,000

Interest on long-term note ........................

4,500

4,500

4,500

13,500

Total expenses ...........................................

$16,500

$16,500

$16,500

$49,500

*$500,000 x 0.90%

Fundamental Accounting Principles, 21st Edition

1316

Problem 22-7A (Continued)

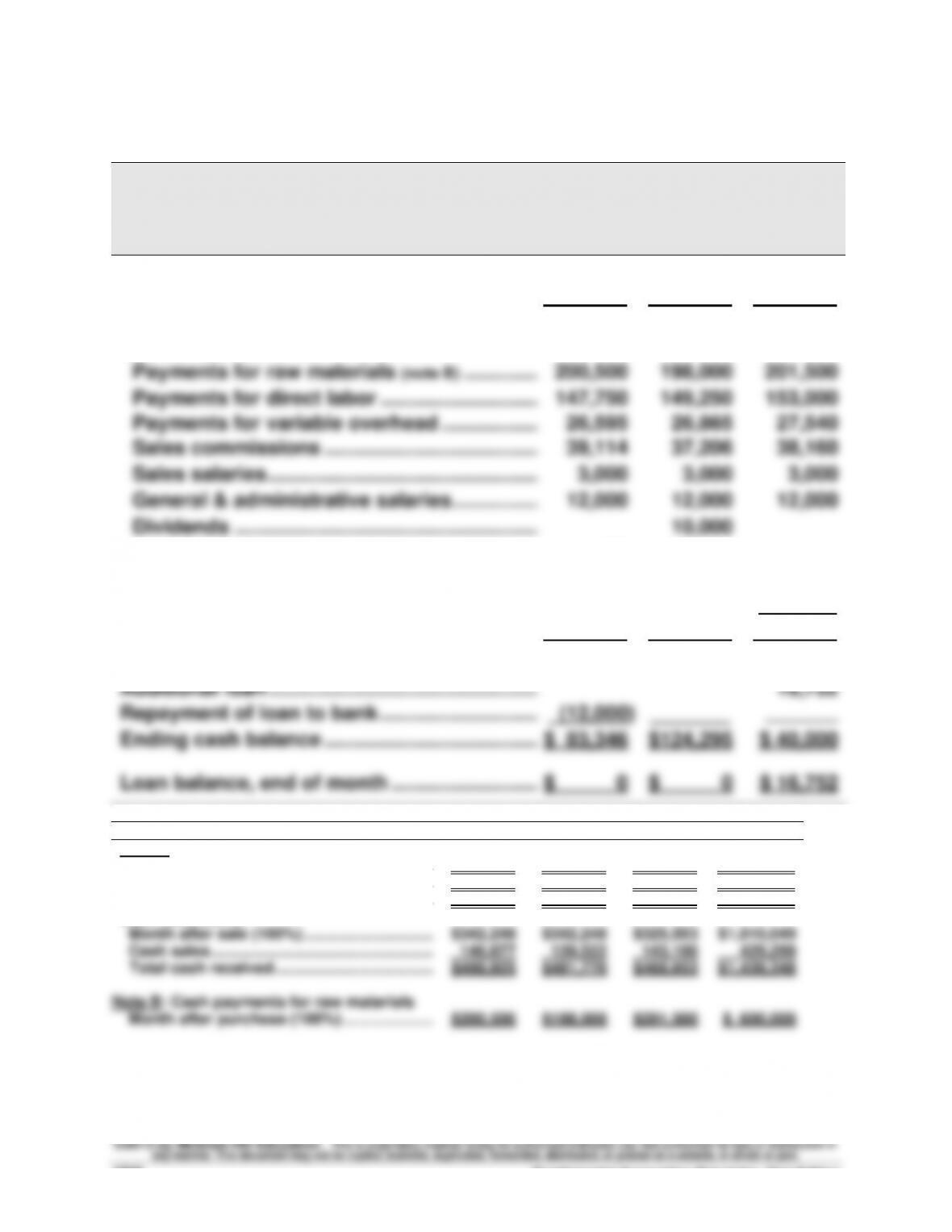

Part 8

ZIGBY MANUFACTURING

Cash Budgets

April, May, and June 2013

April

May

June

Beginning cash balance ......................................

$ 40,000

$ 83,346

$124,295

Cash receipts from customers (note A)................

488,925

481,770

468,653

Total cash available .............................................

528,925

565,116

592,948

Cash disbursements

Payments for raw materials (note B) ..................

200,500

198,000

201,500

Payments for direct labor ................................

Payments for variable overhead ......................

Sales commissions ...........................................

147,750

26,595

39,114

149,250

26,865

37,206

153,000

27,540

38,160

Sales salaries .....................................................

3,000

3,000

3,000

General & administrative salaries ....................

12,000

12,000

12,000

Dividends ...........................................................

10,000

Loan interest ($12,000 x 1%) ................................

120

Long-term note interest ($500,000 x .0.9%) ............

Purchase of equipment .....................................

4,500

_______

4,500

_______

4,500

130,000

Total cash disbursements ................................

433,579

440,821

569,700

Preliminary cash balance ................................

95,346

124,295

23,248

Additional loan .....................................................

Repayment of loan to bank ................................

(12,000)

_______

16,752

_______

Ending cash balance ...........................................

$ 83,346

$124,295

$ 40,000

Loan balance, end of month ...............................

$ 0

$ 0

$ 16,752

Supporting calculations

April

May

June

Total

Note A: Cash receipts from customers

Total sales .........................................................

$488,925

$465,075

$477,000

$1,431,000

Cash sales (30%) ..............................................

146,677

139,522

143,100

429,299

Credit sales (70%) ............................................

342,248

325,553

333,900

1,001,701

Cash collections

Month after sale (100%) ................................

$342,248

$342,248

$325,553

$1,010,049

Cash sales.........................................................

146,677

139,522

143,100

429,299

Total cash received ..........................................

$488,925

$481,770

$468,653

$1,439,348

Month after purchase (100%) ..........................

$200,500

$198,000

$201,500

$ 600,000

NOTE: Cash sales are rounded down to the nearest whole dollar. All other amounts are rounded

up to the nearest whole dollar. Student answers will vary slightly if they round differently.

Problem 22-7A (Continued)

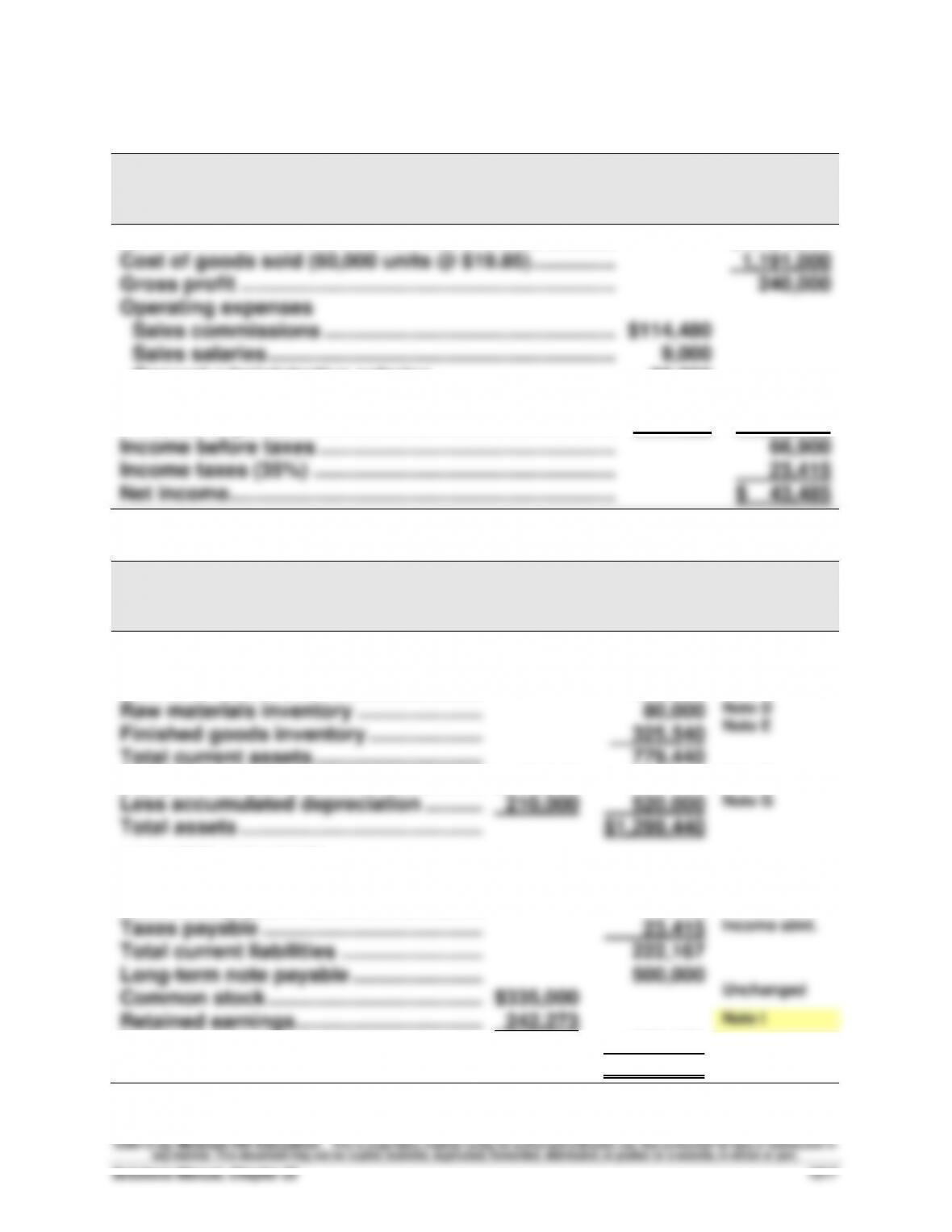

Part 9

ZIGBY MANUFACTURING

Budgeted Income Statement

For Three Months Ended June 30, 2013

Sales ................................................................................

$1,431,000

Cost of goods sold (60,000 units @ $19.85) ................

1,191,000

Gross profit ....................................................................

240,000

Operating expenses

Sales commissions .....................................................

$114,480

Sales salaries ...............................................................

9,000

General administrative salaries ................................

36,000

Long-term note interest ..............................................

13,500

Interest expense ..........................................................

120

173,100

Income before taxes ......................................................

66,900

Income taxes (35%) .......................................................

23,415

Net income ......................................................................

$ 43,485

Part — Budgeted Retained Earnings & Budgeted Balance Sheet

ZIGBY MANUFACTURING

Budgeted Balance Sheet

June 30, 2013

ASSETS

Cash ............................................................

$ 40,000

Cash budget

Accounts receivable ................................

333,900

Note C

Raw materials inventory ...........................

Finished goods inventory .........................

80,000

325,540

Note D

Note E

Total current assets ................................

779,440

Equipment ..................................................

$730,000

Note F

Less accumulated depreciation ...............

210,000

520,000

Note G

Total assets ................................................

$1,299,440

LIABILITIES AND EQUITY

Accounts payable ......................................

$ 182,000

Note H

Bank loan payable .....................................

16,752

Cash budget

Taxes payable ............................................

23,415

Income stmt.

Total current liabilities ..............................

222,167

Long-term note payable ............................

Common stock ...........................................

$335,000

500,000

Unchanged

Retained earnings ......................................

242,273

Note I

Total stockholders’ equity ........................

577,273

Total liabilities and equity .........................

$1,299,440

Fundamental Accounting Principles, 21st Edition

1318

Problem 22-7A (Concluded)

Supporting Footnotes

Note C

Beginning receivables ......................................................

$ 342,248

Credit sales ........................................................................

1,001,701

Less collections ................................................................

(1,010,049)

Ending receivables ............................................................

$ 333,900

Note D

Beginning raw materials inventory ................................

$ 98,500

Purchases of raw materials ..............................................

581,500

Less materials used in production** ................................

(600,000)

Ending raw materials inventory* ......................................

$ 80,000

*Also equals 4,000 units @ $20 = $80,000

**30,000 units x $20 per unit

Note E

Beginning finished goods inventory ................................

$ 325,540

Cost of goods completed during the period ...................

1,191,000

Less cost of goods sold during the period .....................

(1,191,000)

Ending finished goods inventory*................................

$ 325,540

*Also equals 16,400 units @ $19.85 = $325,540

Note F

Beginning equipment ........................................................

$ 600,000

Purchased in June ............................................................

130,000

Total ...................................................................................

$ 730,000

Note G

Beginning accumulated depreciation ..............................

$ 150,000

Depreciation expense .......................................................

60,000

Total ...................................................................................

$ 210,000

Note H

Beginning accounts payable ............................................

$ 200,500

Purchases of raw materials ..............................................

581,500

Payments for raw materials ..............................................

(600,000)

Ending accounts payable .................................................

$ 182,000

Note I

ZIGBY MANUFACTURING

Budgeted Statement of Retained Earnings

For Three Months Ended June 30, 2013

Retained earnings, Beginning ......................... $208,788

Add: Net income ......................................... 43,485

PROBLEM SET B

Problem 22-1B (60 minutes)

Part 1

H2O SPORTS CORPORATION

Merchandise Purchases Budgets

For April, May, and June

April

May

June

WATER SKIS

Budgeted sales for next month ...........................

90,000

130,000

100,000

Ratio of ending inventory to future sales ...........

10%

10%

10%

Budgeted ending inventory ................................

9,000

13,000

10,000

Add budgeted sales ..............................................

70,000

90,000

130,000

Required units of available merchandise ...........

79,000

103,000

140,000

Less actual (or budgeted) beginning inventory .......

(40,000)

(9,000)

(13,000)

Budgeted purchases ............................................

39,000

94,000

127,000

TOW ROPES

Budgeted sales for next month ...........................

90,000

110,000

100,000

Ratio of ending inventory to future sales ...........

10%

10%

10%

Budgeted ending inventory ................................

9,000

11,000

10,000

Add budgeted sales ..............................................

100,000

90,000

110,000

Required units of available merchandise ...........

109,000

101,000

120,000

Less actual (or budgeted) beginning inventory .......

(90,000)

(9,000)

(11,000)

Budgeted purchases ............................................

19,000

92,000

109,000

LIFE JACKETS

Budgeted sales for next month ...........................

190,000

200,000

120,000

Ratio of ending inventory to future sales ...........

10%

10%

10%

Budgeted ending inventory ................................

19,000

20,000

12,000

Add budgeted sales ..............................................

160,000

190,000

200,000

Required units of available merchandise ...........

179,000

210,000

212,000

Less actual (or budgeted) beginning inventory .......

(150,000)

(19,000)

(20,000)

Budgeted purchases ............................................

29,000

191,000

192,000

Fundamental Accounting Principles, 21st Edition

1320

Problem 22-1B (Concluded)

Part 2. Analysis Component

The factor that causes the first month’s purchases to be so much smaller is

the excess inventory that accumulated just prior to the budgeting period.

This overstocking factor could exist for a number of reasons, including:

• Management may have simply lost sight of inventory levels, thereby

allowing them to reach inappropriately high levels.

• Competition among suppliers may have caused them to become more

customer oriented, with the result that they will deliver products in

smaller lots more quickly.

Problem 22-2B (50 minutes)

SONY STEREO

Cash Budgets

For April, May, and June

April

May

June

Beginning balance ..........................................

$ 3,000

$ 53,000

$ 44,000

Cash receipts

Collection on accounts receivable* ............

136,000

210,000

290,200

Receipts from bank loan ..............................

80,000

_______

_______

Total cash available ........................................

219,000

263,000

334,200

Cash disbursements

Payments on accounts payable** ...............

80,000

188,000

186,000

Payroll ............................................................

16,000

17,000

18,000

Rent ................................................................

6,000

6,000

6,000

Other expenses .............................................

64,000

8,000

7,000

Repayment on bank loan .............................

80,000

Interest on bank loan* ................................

________

________

2,400

Total cash disbursements ...........................

166,000

219,000

299,400

Ending cash balance ......................................

$ 53,000

$ 44,000

$ 34,800

* Interest at 12% on $80,000 for 90 days is $2,400.

Supporting calculations

Collections of credit sales*

March

April

May

June

March sales ($180,000)—[25%: 45%: 20%: 9%] ..............

$ 45,000

$ 81,000

$ 36,000

$ 16,200

April sales ($220,000)—[25%: 45%: 20%] .......................

-

55,000

99,000

44,000

May sales ($300,000)—[25%: 45%] ................................

-

-

75,000

135,000

June sales ($380,000)—[25%] ................................

-

-

-

95,000

Total ..................................................................................

$ 45,000

$136,000

$210,000

$290,200

Payments on credit purchases**

March

April

May

June

March purchases ($100,000)—(0%: 80%: 20%) ................................

$ 0

$ 80,000

$ 20,000

$ -

April purchases ($210,000)—(0%: 80%: 20%) ................................

-

0

168,000

42,000

May purchases ($180,000)—(0%: 80%) ................................

-

-

0

144,000

June purchases ($220,000)—(0%) ................................

-

-

-

0

Total ................................................................................................

$ 0

$ 80,000

$188,000

$186,000

Fundamental Accounting Principles, 21st Edition

1322

Problem 22-3B (70 minutes)

Part 1

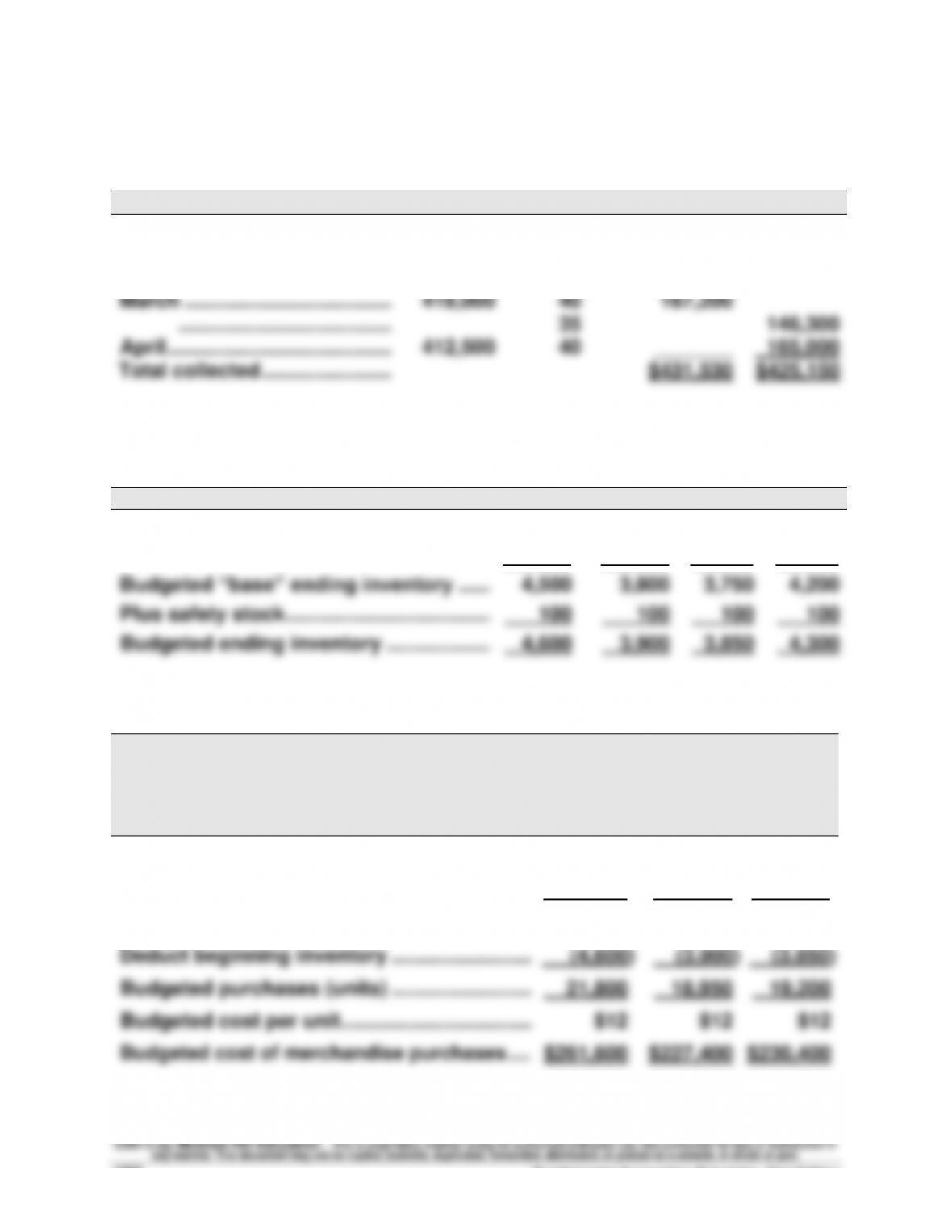

Cash collections of credit sales (accounts receivable)

From sales in

Total

% Collected

March

April

January .....................................

$396,000

23%

$ 91,080

February ....................................

495,000

35

173,250

................................

23

$113,850

March ........................................

418,000

40

167,200

.........................................

35

146,300

April ...........................................

412,500

40

_______

165,000

Total collected ..........................

$431,530

$425,150

Part 2

Budgeted ending inventories (in units)

January

February

March

April

Next month’s budgeted sales .....................

22,500

19,000

18,750

21,000

Ratio of inventory to future sales ...............

20%

20%

20%

20%

Budgeted “base” ending inventory ...........

4,500

3,800

3,750

4,200

Plus safety stock..........................................

100

100

100

100

Budgeted ending inventory ........................

4,600

3,900

3,850

4,300

Part 3

CONNICK COMPANY

Merchandise Purchases Budgets

For February, March, and April

February

March

April

Budgeted ending inventory (from part 2) ............

3,900

3,850

4,300

Add budgeted sales ..........................................

22,500

19,000

18,750

Required units of available merchandise .......

26,400

22,850

23,050

Deduct beginning inventory ............................

(4,600)

(3,900)

(3,850)

Budgeted purchases (units) ............................

21,800

18,950

19,200

Budgeted cost per unit .....................................

$12

$12

$12

Budgeted cost of merchandise purchases ........

$261,600

$227,400

$230,400