Part 2

QA_Ori:

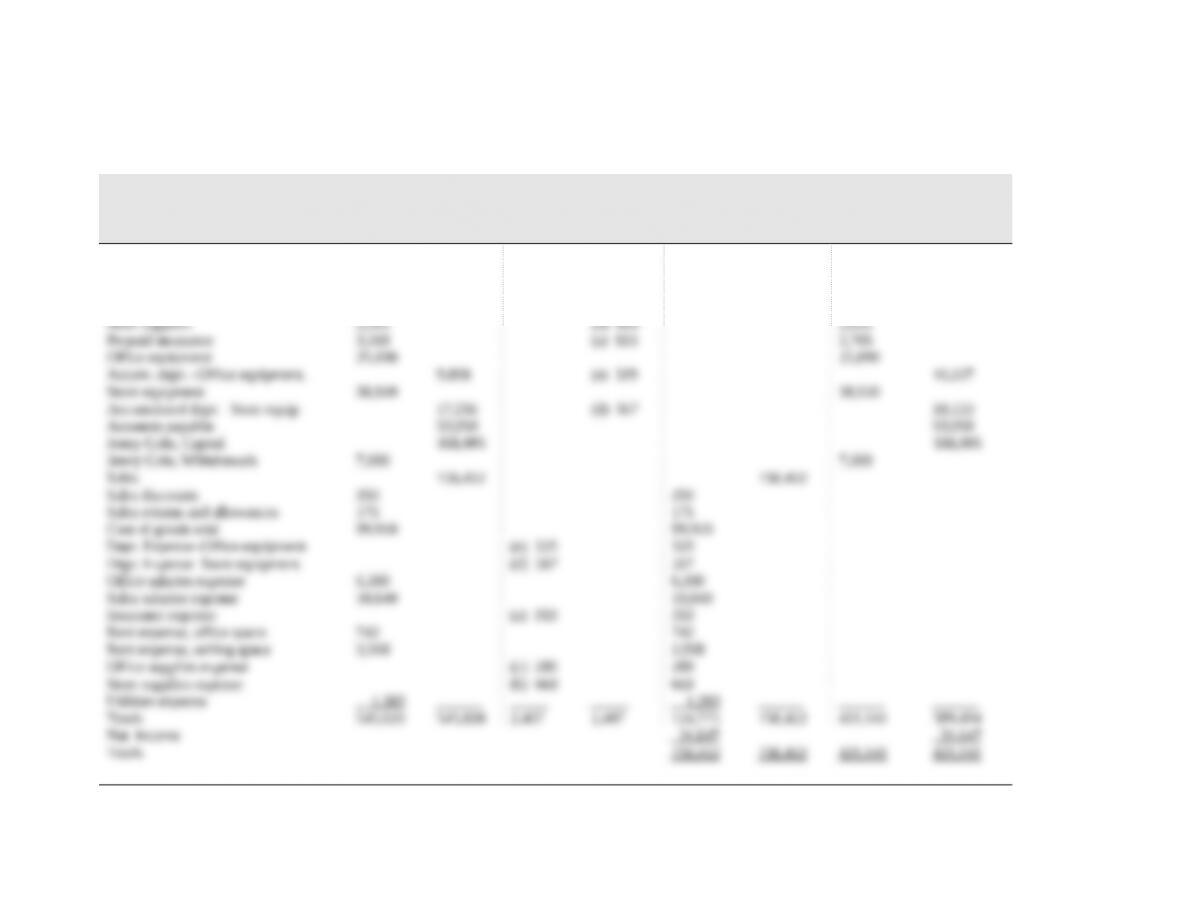

COLO COMPANY

Work Sheet for Month Ended May 31, 2013

Unadjusted Trial

Balance Adjustments

Income

Statement

Balance Sheet or

State-ment of Owner’s

Equity

Account Debit Credit Debit Credit Debit Credit Debit Credit

Cash 135,911 135,911

Accounts receivable 18,200 18,200

Merchandise inventory 189,519 189,519

Office supplies 793 (c) 289 504

Store supplies 3,301 (b) 669 2,632

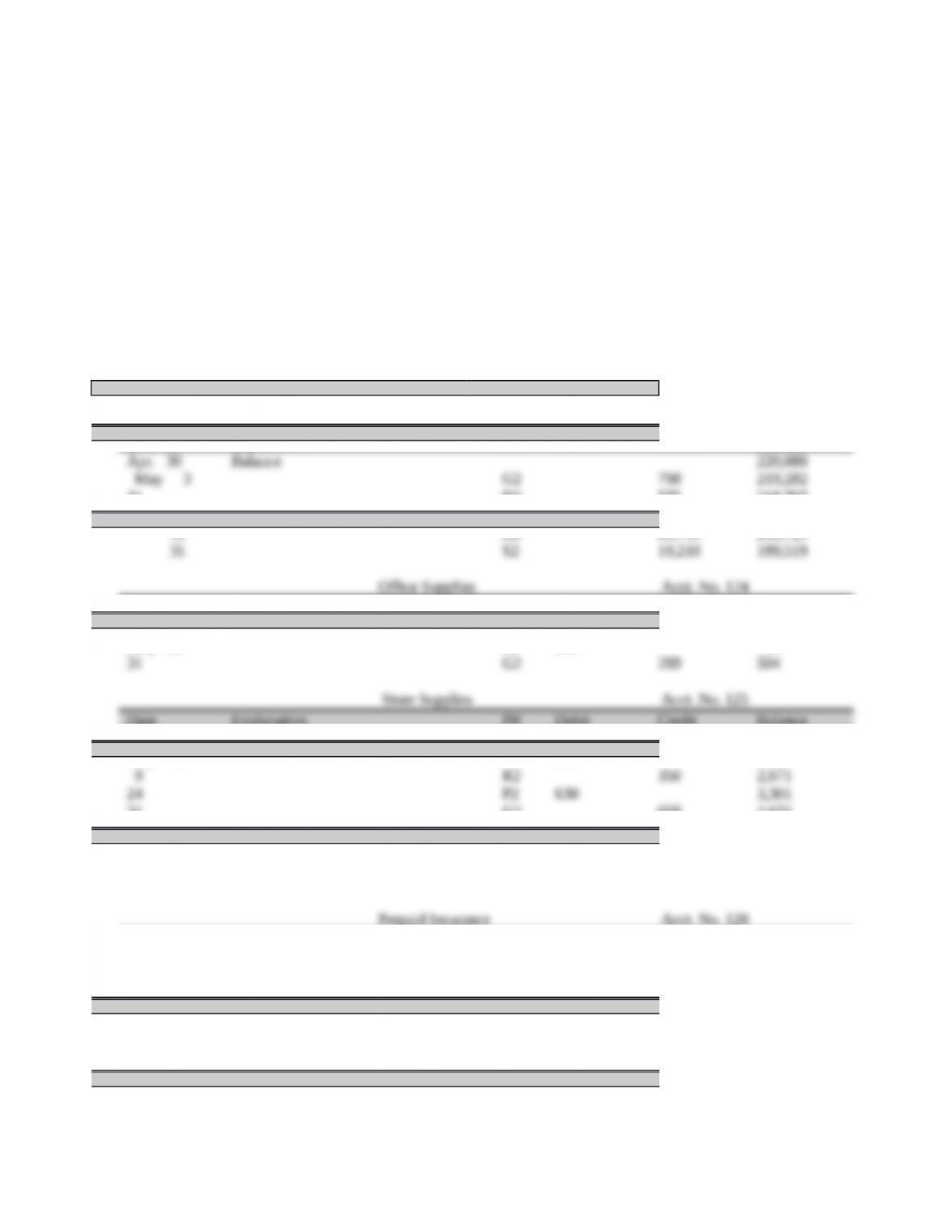

GENERAL LEDGER

Cash Acct. No. 101

Date Explanation PR Debit Credit Balance

Apr. 30 Balance 50,247

Accounts Receivable Acct. No. 106

Date Explanation PR Debit Credit Balance

Apr. 30 Balance 4,725

Merchandise Inventory Acct. No. 119

Date Explanation PR Debit Credit Balance

Apr. 30 Balance 220,080

May 3 G2 798 219,282

Office Supplies Acct. No. 124

Date Explanation PR Debit Credit Balance

Apr. 30 Balance 430

Store Supplies Acct. No. 125

Date Explanation PR Debit Credit Balance

Apr. 30 Balance 2,447

Prepaid Insurance Acct. No. 128

Date Explanation PR Debit Credit Balance

Apr. 30 Balance 3,318

May 31 G2 553 2,765

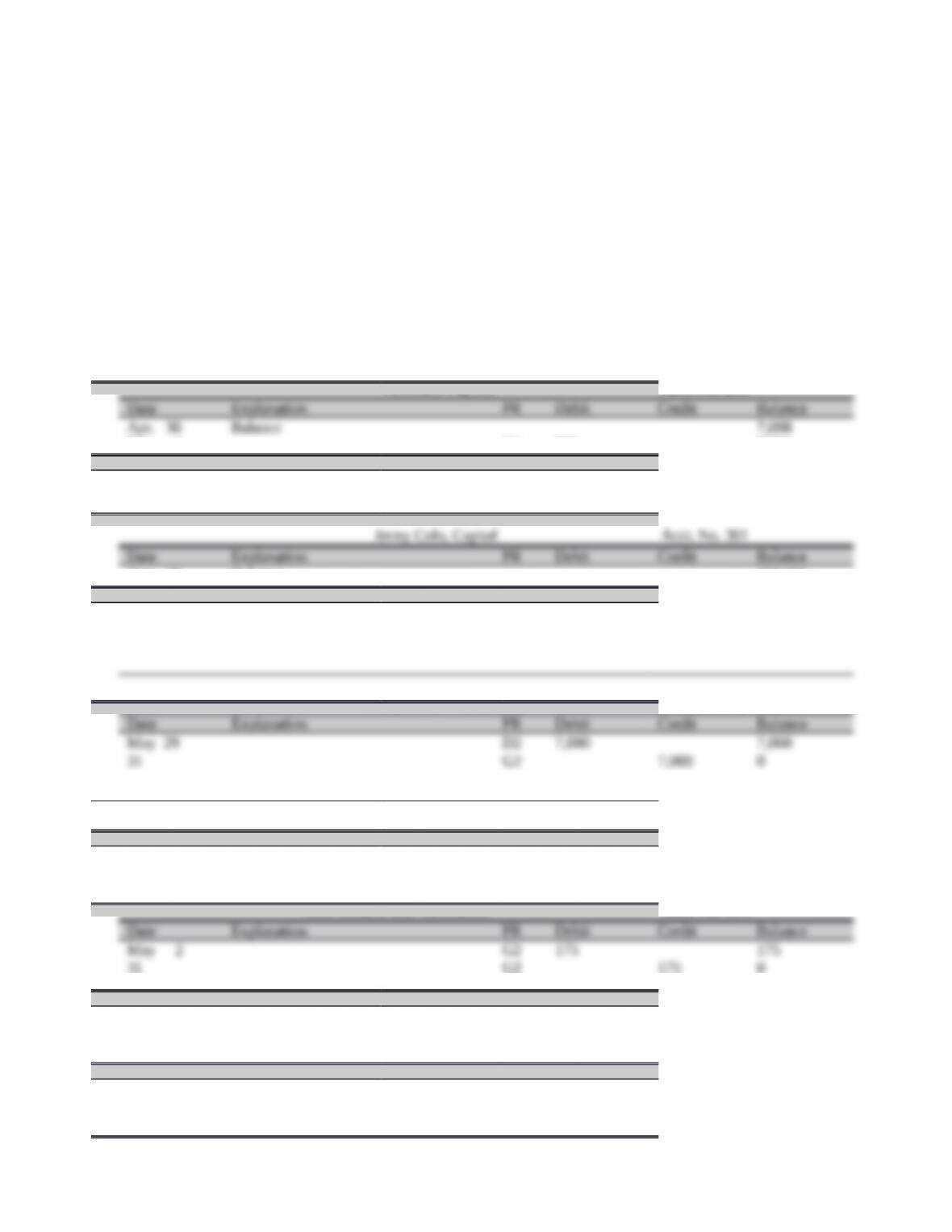

Office Equipment Acct. No. 163

Date Explanation PR Debit Credit Balance

Apr. 30 Balance 22,470

May 10 P2 4,074 26,544

12 G2 854 25,690

Accumulated Depreciation–Office Equipment Acct. No. 164

Date Explanation PR Debit Credit Balance

Store Equipment Acct. No. 165

Date Explanation PR Debit Credit Balance

Apr. 30 Balance 38,920

Accumulated Depreciation–Store Equipment Acct. No. 166

Date Explanation PR Debit Credit Balance

Accounts Payable Acct. No. 201

Date Explanation PR Debit Credit Balance

Apr. 30 Balance 7,098

May 3 G2 798 6,300

Jenny Colo, Capital Acct. No. 301

Date Explanation PR Debit Credit Balance

Jenny Colo, Withdrawals Acct. No. 302

Date Explanation PR Debit Credit Balance

May 29 D2 7,000 7,000

31 G2 7,000 0

Sales Acct. No. 413

Date Explanation PR Debit Credit Balance

Sales Returns and Allowances Acct. No. 414

Date Explanation PR Debit Credit Balance

May 2 G2 175 175

31 G2 175 0

Sales Discounts Acct. No. 415

Date Explanation PR Debit Credit Balance

May 31 R2 350 350

31 G2 350 0

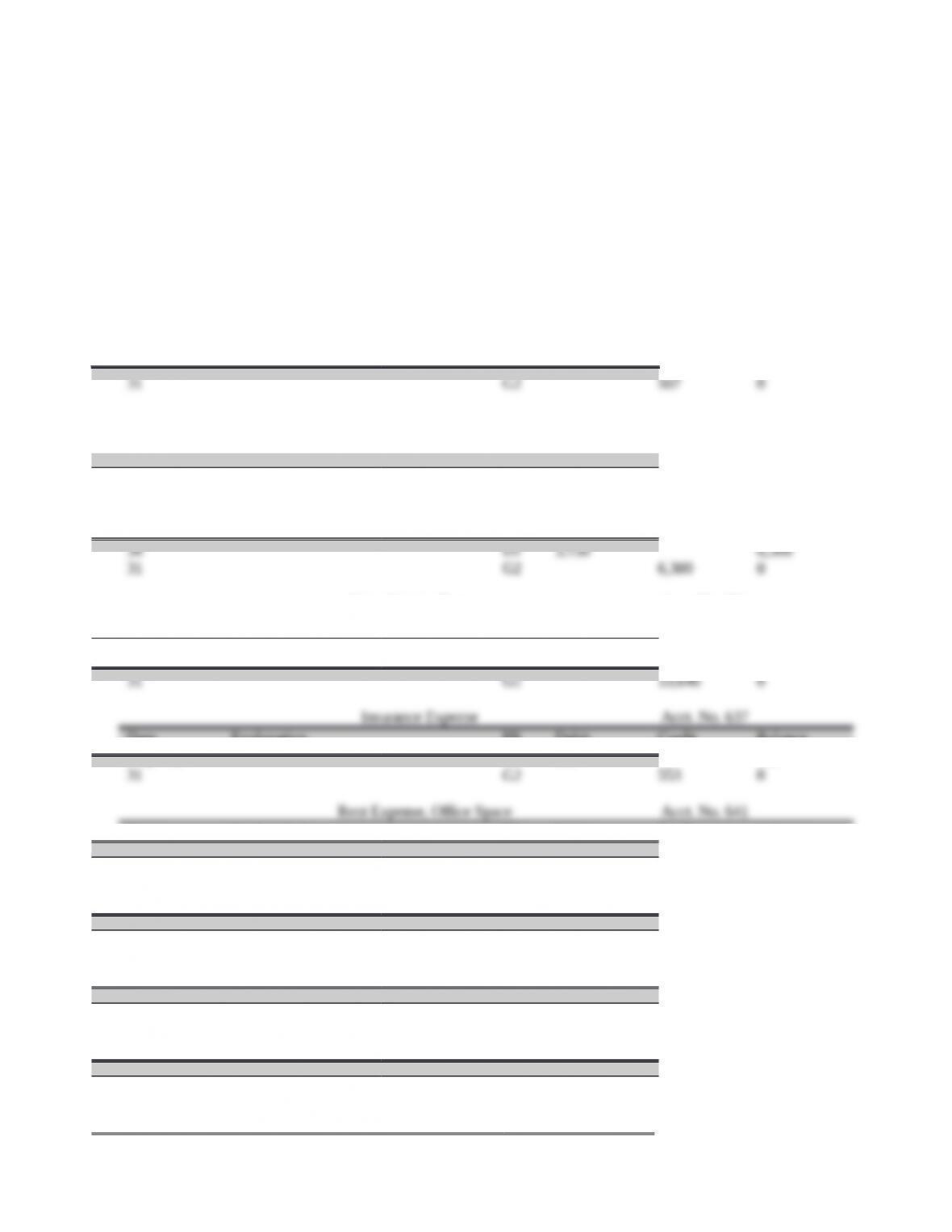

Cost of Goods Sold Acct. No. 502

Date Explanation PR Debit Credit Balance

Depreciation Expense—Office Equipment Acct. No. 612

Date Explanation PR Debit Credit Balance

May 31 G2 329 329

31 G2 329 0

Depreciation Expense—Store Equipment Acct. No. 613

Date Explanation PR Debit Credit Balance

Office Salaries Expense Acct. No. 620

Date Explanation PR Debit Credit Balance

Sales Salaries Expense Acct. No. 621

Date Explanation PR Debit Credit Balance

Insurance Expense Acct. No. 637

Date Explanation PR Debit Credit Balance

May 31 G2 553 553

31 G2 553 0

Rent Expense, Office Space Acct. No. 641

Date Explanation PR Debit Credit Balance

May 1 D2 742 742

31 G2 742 0

Rent Expense, Selling Space Acct. No. 642

Date Explanation PR Debit Credit Balance

May 1 D2 2,968 2,968

31 G2 2,968 0

Office Supplies Expense Acct. No. 650

Date Explanation PR Debit Credit Balance

May 31 G2 289 289

31 G2 289 0

Store Supplies Expense Acct. No. 651

Date Explanation PR Debit Credit Balance

Utilities Expense Acct. No. 690

Date Explanation PR Debit Credit Balance

Income Summary Acct. No. 901

Date Explanation PR Debit Credit Balance

ACCOUNTS RECEIVABLE LEDGER

Crane Corp.

Date Explanation PR Debit Credit Balance

May 26 S2 14,210 14,210

Hensel Company

Date Explanation PR Debit Credit Balance

Knox, Inc.

Date Explanation PR Debit Credit Balance

Lee Services

Date Explanation PR Debit Credit Balance

May 22 S2 6,850 6,850

30 R2 6,850 0

ACCOUNTS PAYABLE LEDGER

Fink Corp.

Date Explanation PR Debit Credit Balance

Garcia, Inc.

Date Explanation PR Debit Credit Balance

Gear Supply Co.

Date Explanation PR Debit Credit Balance

Peyton Products

Date Explanation PR Debit Credit Balance

Apr. 29 P2 7,098 7,098

May 3 G2 798 6,300

8 D2 6,300 0

25 P2 3,080 3,080

Part 3

COLO COMPANY

Income Statement

For Month Ended May 31, 2013

Revenue

General and administrative expenses

Depreciation expense—Office equipment 329

Office salaries expense 6,300

Insurance expense 553

Rent expense—Office space 742

Office supplies expense 289

Utilities expense 1,283

Total general and administrative expenses 9,496

Total operating expenses 24,340

Net income $ 31,647

COLO COMPANY

Statement of Owner’s Equity

For Month Ended May 31, 2013

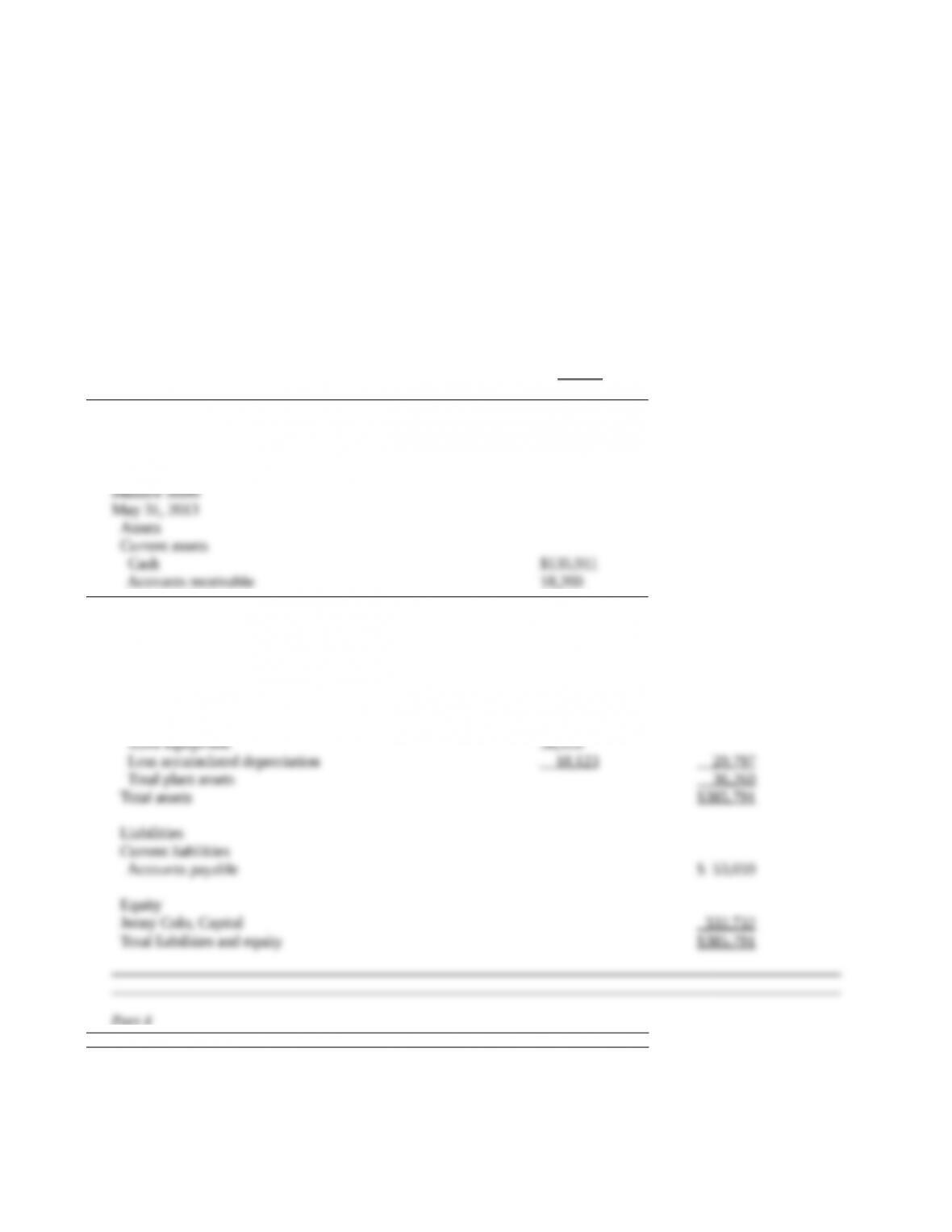

COLO COMPANY

Balance Sheet

May 31, 2013

Assets

Current assets

Cash $135,911

Accounts receivable 18,200

Merchandise inventory 189,519

Part 4

COLO COMPANY

Post-Closing Trial Balance

May 31, 2013

Cash $135,911

Accounts receivable 18,200

Merchandise inventory 189,519

Office supplies 504

Store supplies 2,632

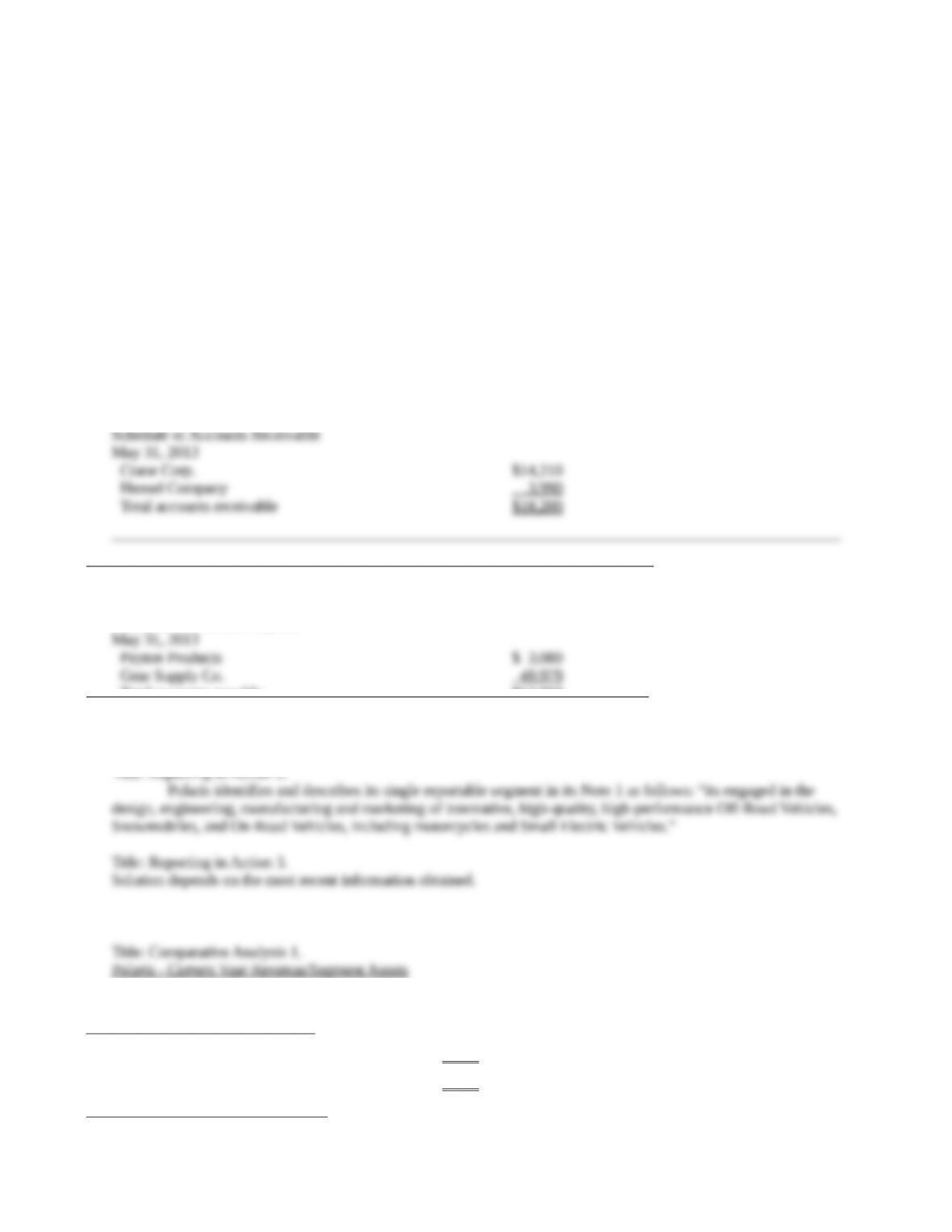

COLO COMPANY

Schedule of Accounts Receivable

May 31, 2013

COLO COMPANY

Schedule of Accounts Payable

May 31, 2013

Title: Comparative Analysis 1.

Polaris – Current Year Revenue/Segment Assets

Domestic segment: $1,864,099 / [($957,497 + $873,183)/2] = 203.7%

International segment: $792,850 / [($270,527 + $188,464)/2] = 345.5%

Polaris – One Year Prior Revenue/Segment Assets

Arctic Cat – Current Year Revenue/Segment Assets

Arctic Cat – One Year Prior Revenue/Segment Assets

Title: Comparative Analysis 2.

QA_Ori:Polaris’s domestic revenue as a percent of its domestic assets is markedly higher than of Arctic Cat’s for

both years for the domestic segment. However, for the international segment, Arctic Cat’s revenue as a percent of

Ethics Challenge — BTN 7-3

Title: Ethics Challenge 1.

QA_Ori:Independence in fact means that the auditor maintains an objective point of view of the client.

Title: Ethics Challenge 2.

QA_Ori:While auditors are hired by their clients to perform audits, auditors have a responsibility to the

Title: Ethics Challenge 3.

QA_Ori:Since Erica Gray is a sole practitioner it is questionable whether she can consult on the client’s

accounting system and then remain objective in subsequent years when she performs the audit of the company.

(Note to instructors: The Sarbanes-Oxley Act specifically prohibits auditors from providing financial information

and system designs for their SEC audit clients. This was codified by the SEC [Final Ruling 68].)

Title: Communicating in Practice

QA_Ori:The memo should recommend the use of special journals and subsidiary ledgers. It should explain the

time-saving aspect of journalizing in labeled columns and also the posting of column totals representing the impact

of groups of like transactions. The memo should discuss the timely information provided by subsidiary ledgers

regarding customer and creditor balances. A discussion of the uses of a schedule for verifying the accuracy of

subsidiary ledgers should also be included.

Title: Taking It to the Net

(See Dell’s Note 14 – Segment Information)

1. Large Enterprise; Public; Small and Medium Business; and Consumer.

2. The Large Enterprise segment reports $1,854 million of operating income and the Large Enterprise segment

3. Dell’s Operating Income and Total Assets by Segment

($ millions)

Operating

Income 2012

Total Assets 2012 : Total

Assets 2011

Segment Return on

Assets

Large Enterprise $ 1,854 $3,108 : $2,934 61.4%

4. The six product groups reported by Dell include: Desktop PCs, Mobility, Software and peripherals, Servers

and networking, Enhanced services, and Storage.

($ millions) 2012 Fiscal Year

Mobility $19,104 30.8%

Desktop PCs 14,144 22.8

Dell earned more—in both dollars and returns—from its Mobility group; its Desktop PCs was second in both

categories.

Title: Teamwork in Action

For check figures in the implementation of this activity see the solution to Problem 7-3A or 7-3B.

Title: Entrepreneurial Decision

1. The following special journals are likely to be used:

Sales journal to record credit sales

Cash receipts journal to record all cash receipts

Purchases journal to record credit purchases

Cash disbursements journal to record all cash payments

General journal to record all transactions not in special journals

The company also is likely to use the following subsidiary ledgers:

Accounts receivable subsidiary ledger to track amounts owed by individual customers

Accounts payable ledger to track amounts owed to individual vendors

Inventory ledger to keep track of all different inventory items (including inventory ready to sell, inventory in the

process of being completed, and materials to be used in the production of inventory)

2.

Year

One Year

Hence

Two Years

Hence

Three Years

Hence

Four Years

Hence

Five Years

Hence

Sales $100.0 mil 120.0 mil $138.0 mil $172.5 mil $207.0 mil

If sales follow the growth projected, the company will have more than doubled the current $100 mil in

annual sales to $207 mil annually.

Title: Global Decision

KTM has the following reported segments:

Europe

North America

Others

KTM discloses dollar amounts for the following line items:

Profit and Loss Information

Net sales

External net sales

EBIT

Balance sheet information

Assets

Liabilities

Investments

Depreciation

Yes. On most financial measures reported, the Europe segment appears to dominate KTM’s other segments.