Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 2

Analyzing and Recording Transactions

QUESTIONS

1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid

expenses (rent, insurance, etc.), office supplies, store supplies, equipment,

building, and land.

2. A note payable is formal promise, usually denoted by signing a promissory note to

pay a future amount. A note payable can be short-term or long-term, depending on

3. There are several steps in processing transactions: (1) Identify and analyze the

transaction or event, including the source document(s), (2) apply double-entry

4. A general journal can be used to record any business transaction or event.

7. Expense accounts have debit balances because they are decreases to equity (and

equity has a credit balance).

8. The recordkeeper prepares a trial balance to summarize the contents of the ledger

9. The error should be corrected with a separate (subsequent) correcting entry. The

entry’s explanation should describe why the correction is necessary.

10. The four financial statements are: income statement, balance sheet, statement of

owner’s equity, and statement of cash flows.

11. The balance sheet provides information that helps users understand a company’s

12. The income statement lists the types and amounts of revenues and expenses, and

13. An income statement user must know what time period is covered to judge whether

the company’s performance is satisfactory. For example, a statement user would

14. (a) Assets are probable future economic benefits obtained or controlled by a specific

entity as a result of past transactions or events. (b) Liabilities are probable future

15. The balance sheet is sometimes referred to as the statement of financial position.

16. Debit balance accounts on the Polaris balance sheet include: Cash and cash

equivalents; Trade receivables, net; Inventories, net; Prepaid expenses and other;

Income taxes receivable; Deferred tax assets; Land, buildings and improvements;

17. The asset account with receivable in its account title is: Accounts receivable, less

18. KTM’s revenue account is titled “Net sales.”

QUICK STUDIES

Quick Study 2-1 (10 minutes)

The likely source documents include:

a. Sales ticket

Quick Study 2-2 (5 minutes)

a. B Balance sheet

b. E Statement of owner’s equity

Quick Study 2-3 (10 minutes)

a.

Debit

d.

Debit

g.

Credit

b.

Debit

e.

Debit

h.

Debit

c.

Credit

f.

Debit

i.

Credit

Quick Study 2-4 (10 minutes)

a.

Debit

e.

Debit

i.

Credit

b.

Debit

f.

Credit

j.

Debit

c.

Credit

g.

Credit

k.

Debit

d.

Credit

h.

Debit

l.

Credit

Quick Study 2-5 (10 minutes)

a.

Debit

e.

Debit

i.

Credit

b.

Credit

f.

Credit

j.

Debit

c.

Debit

g.

Credit

d.

Credit

h.

Credit

Quick Study 2-6 (15 minutes)

May 15 Cash .......................................................................... 70,000

Equipment ............................................................... 30,000

D. Tyler, Capital ............................................... 100,000

Owner invests cash and equipment.

30 Cash .......................................................................... 1,000

Unearned Landscaping Services Revenue .. 1,000

Received cash in advance for landscaping services.

Quick Study 2-7 (10 minutes)

Quick Study 2-8 (10 minutes)

a.

I

e.

B

i.

E

b.

B

f.

B

j.

B

c.

B

g.

B

k.

I

d.

I

h.

I

l.

I

Quick Study 2-9 (10 minutes)

a. Accounting under IFRS follows the same debit and credit system as

under US GAAP.

b. The same four basic financial statements are prepared under IFRS and

c. Accounting reports under both IFRS and US GAAP are likely different

depending on the extent of accounting controls and enforcement. For

EXERCISES

Exercise 2-1 (10 minutes)

1 a. Analyze each transaction from source documents.

Exercise 2-2 (10 minutes)

a.

3

d.

5

b.

4

e.

2

c.

1

Exercise 2-3 (5 minutes)

a.

2

b.

1

Exercise 2-4 (15 minutes)

Type of

Normal

Increase

Account

Account

Balance

(Dr. or Cr.)

a.

Cash ............................................

asset

debit

debit

b.

Legal Expense ............................

expense

debit

debit

c.

Prepaid Insurance ......................

asset

debit

debit

d.

Land ............................................

asset

debit

debit

e.

Accounts Receivable .................

asset

debit

debit

f.

Owner Withdrawals....................

equity

debit

debit

g.

License Fee Revenue ................

revenue

credit

credit

h.

Unearned Revenue ....................

liability

credit

credit

i.

Fees Earned ................................

revenue

credit

credit

j.

Equipment ..................................

asset

debit

debit

k.

Notes Payable ............................

liability

credit

credit

l.

Owner Capital .............................

equity

credit

credit

Exercise 2-5 (15 minutes)

a.

Beginning accounts payable (credit) .............................................

$152,000

Purchases on account in October (credits) ................................

281,000

Payments on accounts in October (debits) ................................

( ?)

Ending accounts payable (credit) ..................................................

$132,500

Payments on accounts in October (debits) ................................

$300,500

b.

Beginning accounts receivable (debit) ..........................................

$102,500

Sales on account in October (debits) ............................................

?

Collections on account in October (credits) ................................

(102,890)

Ending accounts receivable (debit) ...............................................

$ 89,000

Sales on account in October (debits) ............................................

$ 89,390

c.

Beginning cash balance (debit) ......................................................

$ ?

Cash received in October (debits) .................................................

102,500

Cash disbursed in October (credits) ..............................................

(103,150)

Ending cash balance (debit) ...........................................................

$ 18,600

Beginning cash balance (debit) ......................................................

$ 19,250

Exercise 2-6 (15 minutes)

Of the items listed, the following effects should be included:

a. $28,000 increase in a liability account.

increase in cash, an $80,000 increase in computer equipment, and a

$28,000 increase in its liabilities. The net value received by the company is

$62,000.

Exercise 2-7 (25 minutes)

Aug. 1 Cash .................................................................. 6,500

Photography Equipment ................................. 33,500

M. Harris, Capital ....................................... 40,000

Owner investment in business.

31 Utilities Expense .............................................. 675

Cash ............................................................ 675

Paid for August utilities.

Exercise 2-8 (30 minutes)

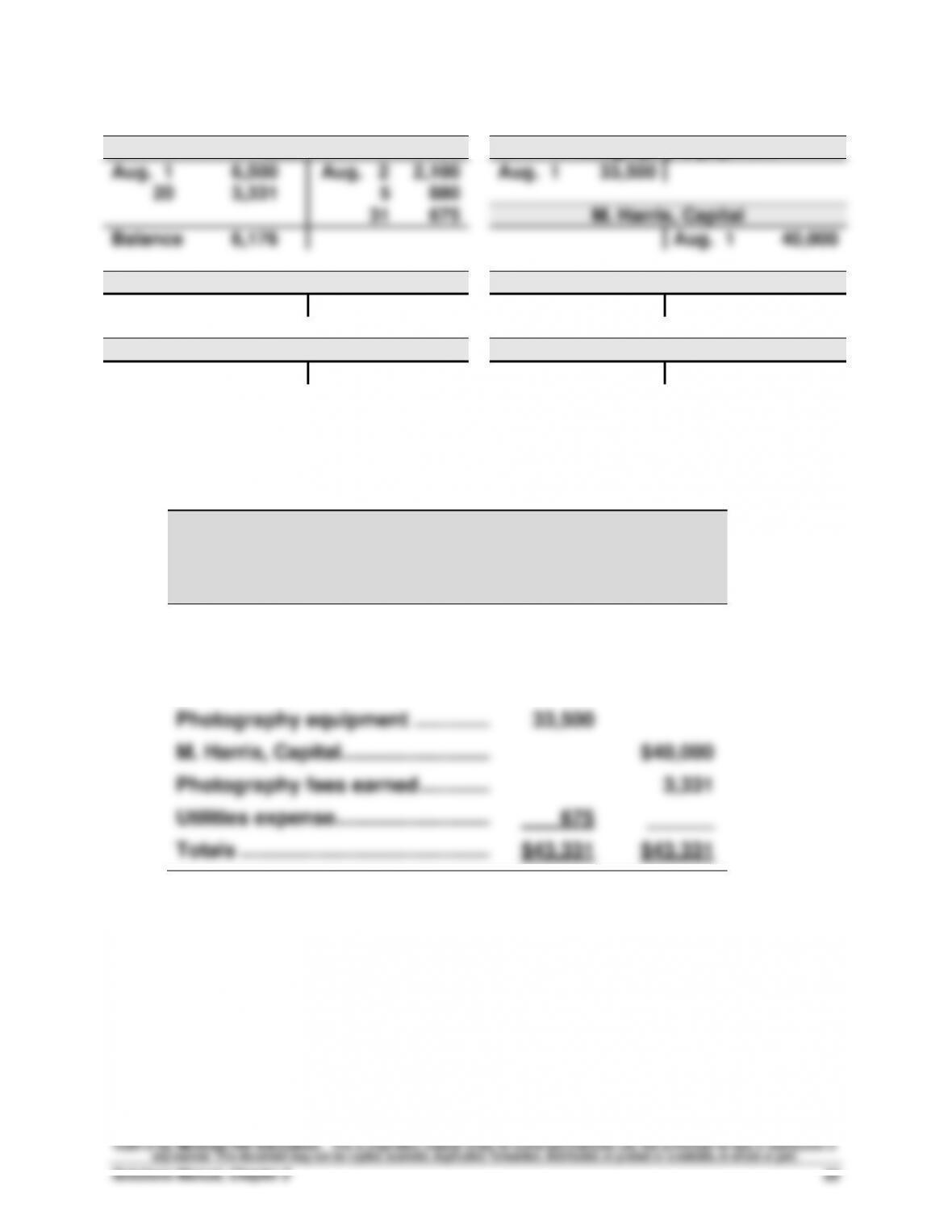

Cash

Photography Equipment

Aug. 1

6,500

Aug. 2

2,100

Aug. 1

33,500

20

3,331

5

880

31

675

M. Harris, Capital

Balance

6,176

Aug. 1

40,000

Office Supplies

Photography Fees Earned

Aug. 5

880

Aug. 20

3,331

Prepaid Insurance

Utilities Expense

Aug. 2

2,100

Aug. 31

675

POSE-FOR-PICS

Trial Balance

August 31

Debit

Credit

Cash ..................................................

$ 6,176

Office supplies ................................

880

Prepaid insurance ............................

2,100

Photography equipment .................

33,500

M. Harris, Capital..............................

$40,000

Photography fees earned ................

3,331

Utilities expense...............................

675

______

Totals ................................................

$43,331

$43,331

Exercise 2-9 (30 minutes)

a. Cash ........................................................................... 100,750

K. Spade, Capital ............................................... 100,750

Owner invested in the business.

f. Accounts Receivable ................................................ 2,700

Fees Earned ....................................................... 2,700

Billed customer for services provided.

g. Rent Expense ............................................................ 1,225

Cash .................................................................... 1,225

Paid for this period’s rental charge.

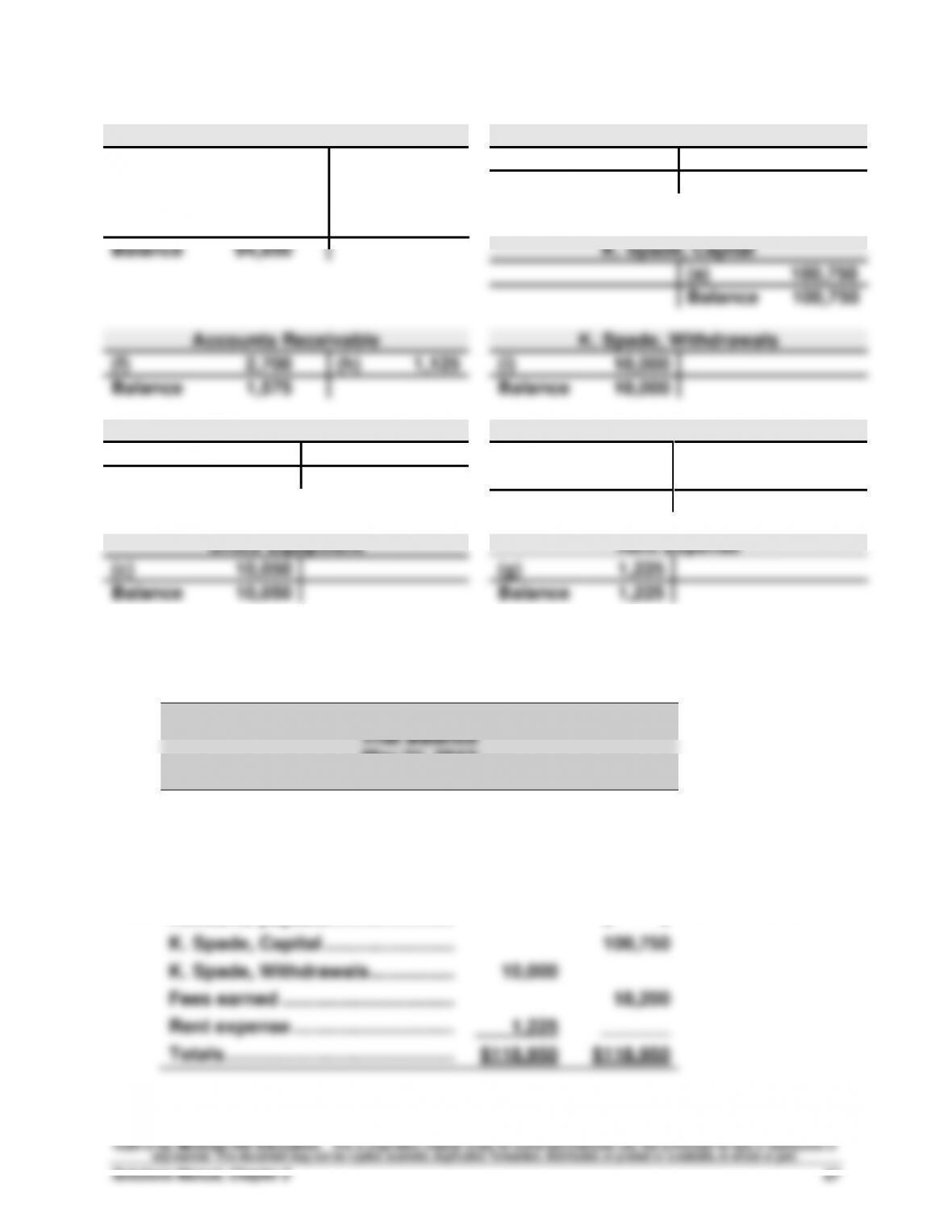

Exercise 2-9 (concluded)

Cash

Accounts Payable

(a)

100,750

(b)

1,250

(e)

10,050

(c)

10,050

(d)

15,500

(e)

10,050

Balance

0

(h)

1,125

(g)

1,225

(i)

10,000

Balance

94,850

K. Spade, Capital

(a)

100,750

Balance

100,750

Accounts Receivable

K. Spade, Withdrawals

(f)

2,700

(h)

1,125

(i)

10,000

Balance

1,575

Balance

10,000

Office Supplies

Fees Earned

(b)

1,250

(d)

15,500

Balance

1,250

(f)

2,700

Balance

18,200

Office Equipment

Rent Expense

(c)

10,050

(g)

1,225

Balance

10,050

Balance

1,225

Exercise 2-10 (15 minutes)

SPADE COMPANY

Trial Balance

May 31, 2013

Debit

Credit

Cash .............................................

$ 94,850

Accounts receivable ...................

1,575

Office supplies.............................

1,250

Office equipment .........................

10,050

Accounts payable ........................

$ 0

K. Spade, Capital .........................

100,750

K. Spade, Withdrawals ................................

10,000

Fees earned .................................

18,200

Rent expense ................................

1,225

_______

Totals .............................................

$118,950

$118,950

Exercise 2-11 (20 minutes)

Transactions that created revenues:

b. Accounts Receivable .......................................... 2,300

Services Revenue ......................................... 2,300

Provided services on credit.

Transactions that did not create revenues along with the reasons are:

a. This transaction brought in cash, but this is an owner investment.

d. This transaction brought in cash, but it created a liability because the

services have not yet been provided to the client.

Exercise 2-12 (20 minutes)

Transactions that created expenses:

b. Salaries Expense ......................................... 1,233

Cash ....................................................... 1,233

Paid salary of receptionist.

Transactions a, c, and e are not expenses for the following reasons:

a. This transaction decreased assets in settlement of a previously

existing liability, and equity did not change. Cash payment does not

mean the same as using up of assets (expense is recorded when the

supplies are used).

Exercise 2-13 (15 minutes)

HELP TODAY

Income Statement

For Month Ended August 31

Revenues

Consulting fees earned ......................... $ 27,000

Expenses

Rent expense ......................................... $ 9,550

Exercise 2-14 (15 minutes)

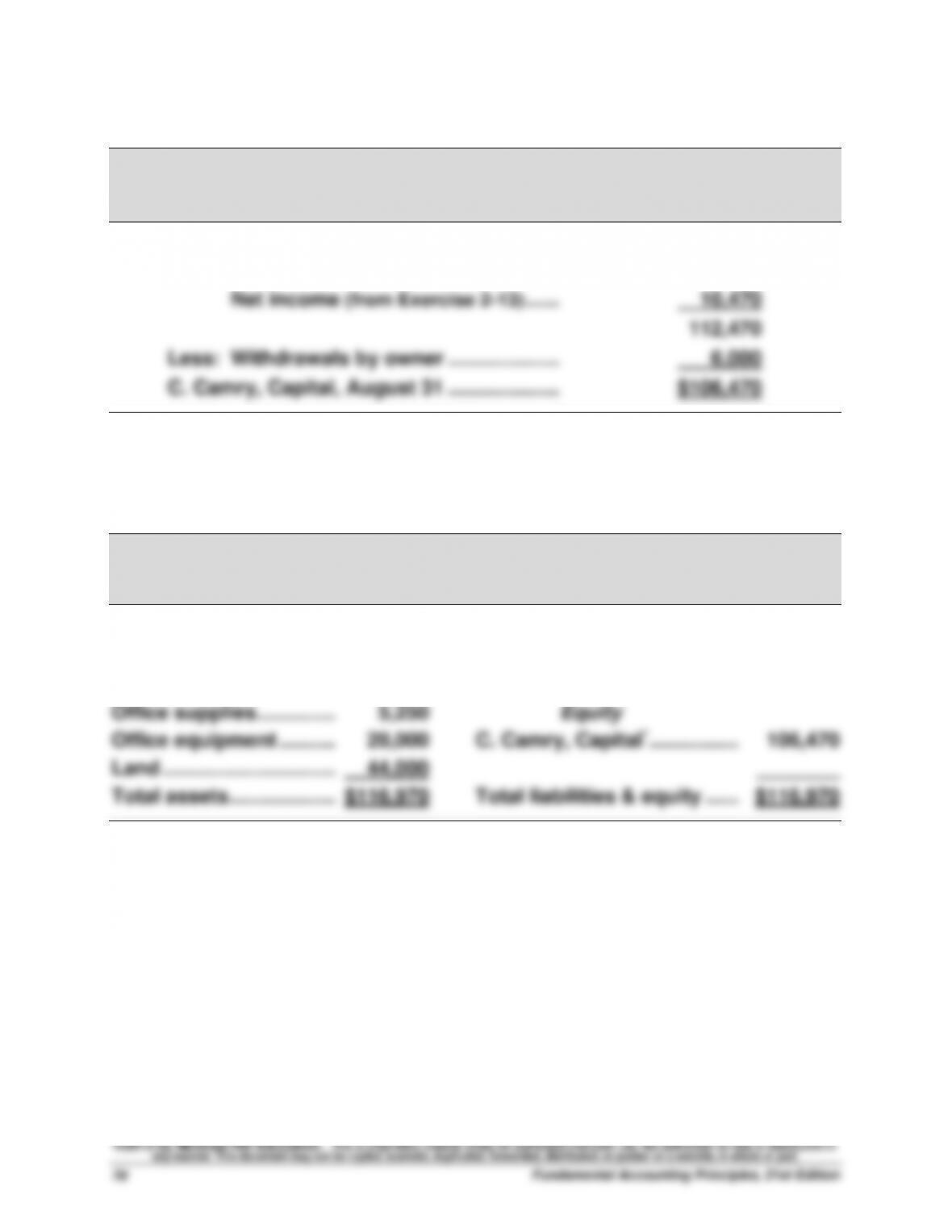

HELP TODAY

Statement of Owner’s Equity

For Month Ended August 31

C. Camry, Capital, July 31 ......................... $ 2,000

Add: Investment by owner ...................... 100,000

Exercise 2-15 (15 minutes)

HELP TODAY

Balance Sheet

August 31

Assets Liabilities

Cash ............................... $ 25,360 Accounts payable ................ $ 10,500

Accounts receivable .... 22,360

* Amount from Exercise 2-14.

Exercise 2-16 (20 minutes)

Calculation of change in equity for part a through part d

Assets

-

Liabilities

=

Equity

Beginning of the year ..........

$ 60,000

-

$20,000

=

$40,000

End of the year .....................

105,000

-

36,000

=

69,000

Net increase in equity ..........

$29,000

a. Net income ..........................................................

$ ?

Plus owner investments ....................................

0

Less owner withdrawals ...................................

(0)

Change in equity ................................................

$29,000

Net Income = $29,000

Since there were no additional investments or withdrawals, the net

income for the year equals the net increase in owner's equity.

b. Net income ..........................................................

$ ?

Plus owner investments ....................................

0

Less owner withdrawals ($1,250/mo. x 12 mo.)

(15,000)

Change in equity ................................................

$29,000

Net Income = $44,000

The withdrawals were added back because they reduced equity

without reducing net income.

c. Net income ..........................................................

$ ?

Plus owner investment ......................................

55,000

Less withdrawals by owner ...............................

(0)

Change in equity ................................................

$29,000

Net Loss = $26,000

The investment was deducted because it increased equity without

creating net income.

d. Net income ..........................................................

$ ?

Plus owner investment ......................................

35,000

Less owner withdrawals ($1,250/mo. X 12 mo.)

(15,000)

Change in equity ................................................

$29,000

Net Income = $9,000

The withdrawals were added back because they reduced equity

without reducing net income and the investments were deducted

because they increased equity without creating net income.