Fundamental Accounting Principles, 21st Edition

992

Exercise 17-14 (15 minutes)

RANDA MERCHANDISING, INC.

Income Statement

For Year Ended December 31, 2013

Net sales ………………………………………………………………..

$2,900,000

Expenses

Cost of goods sold ……………………………………………...

$1,480,000

Salaries expense ………………………………………………...

640,000

Depreciation expense ………………………………………....

232,500

Total expenses …………………………………………………...

2,352,500

Income from continuing operations before taxes …....

547,500

Income taxes expense …………………………………………...

217,000

Income from continuing operations ………………………..

330,500

Discontinued segment

Loss from operating wholesale business

segment (net of tax) ………………………………………....

(444,000)

Gain on sale of wholesale business

segment (net of tax) ………………………………………....

775,000

331,000

Income before extraordinary gain …………………………..

661,500

Extraordinary gain on condemnation of

company property (net of tax) ……………………………...

230,000

Net income …………………………………………………………....

$ 891,500

Exercise 17-15 (15 minutes)

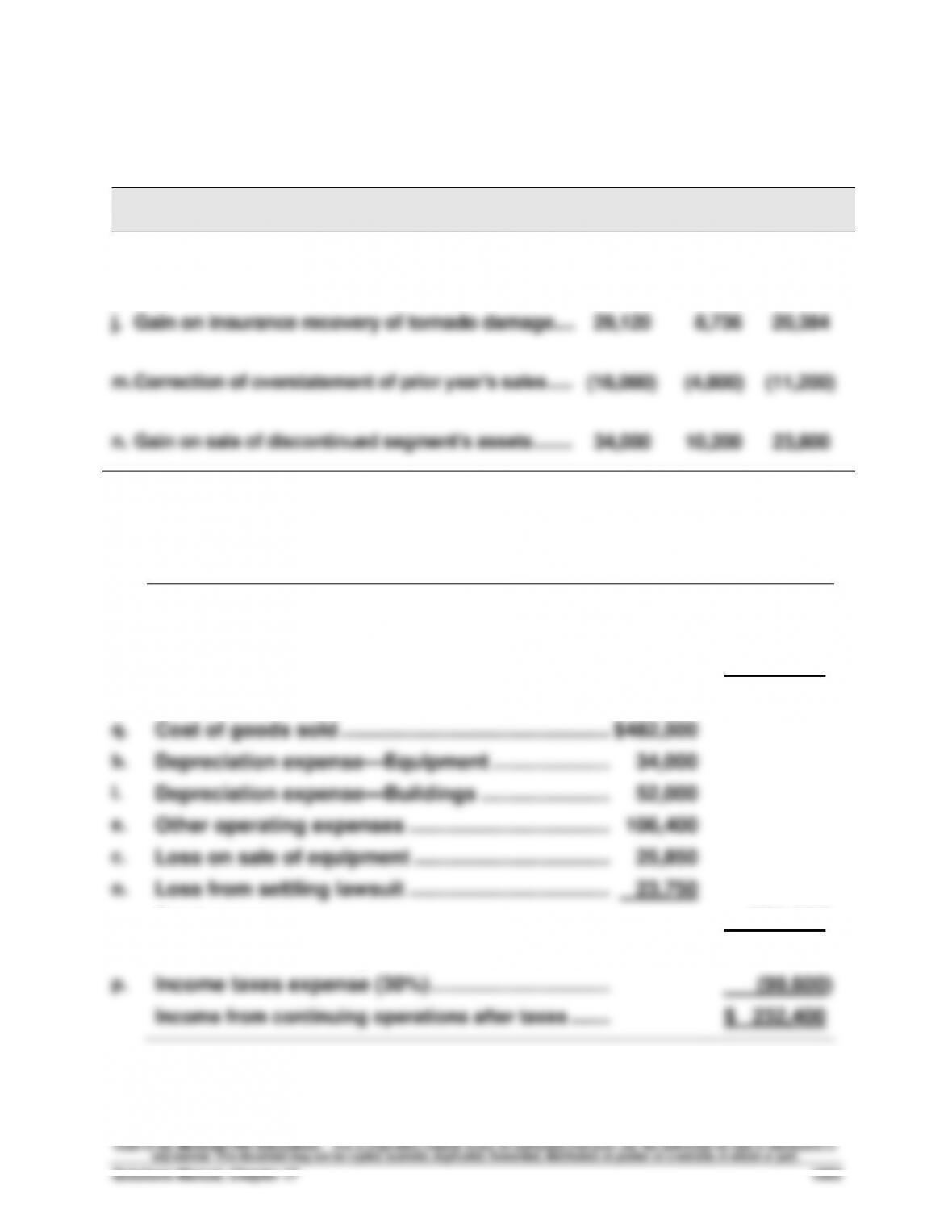

1. Current ratio = (in ¥s) ¥ 1,468,706 / ¥ 333,301 = 4.41

(in $s) $17,695,254 / $4,015,683 = 4.41

2. The results in part 1 reveal that ratios can help us overcome

Fundamental Accounting Principles, 21st Edition

994

PROBLEM SET A

Problem 17-1A (60 minutes)

Part 1

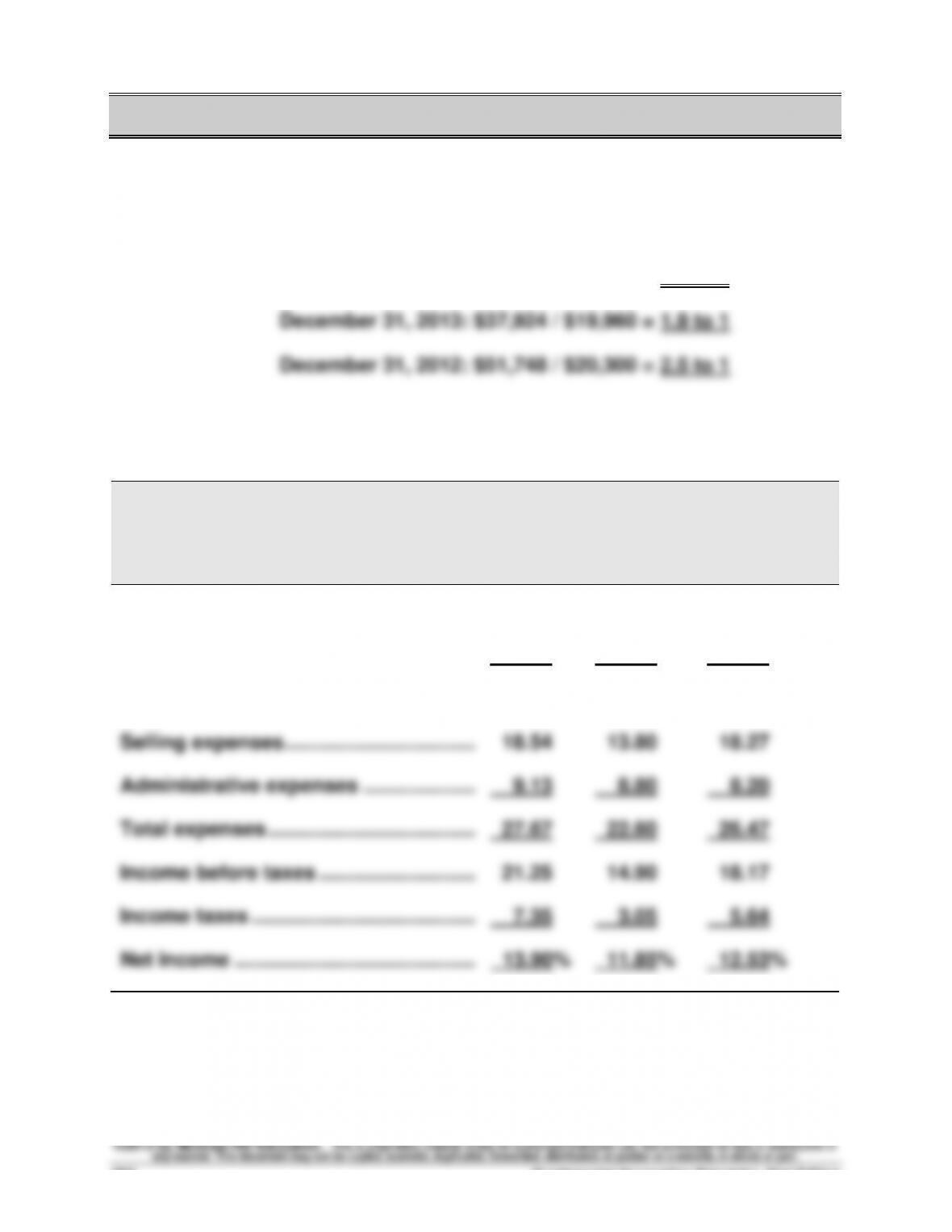

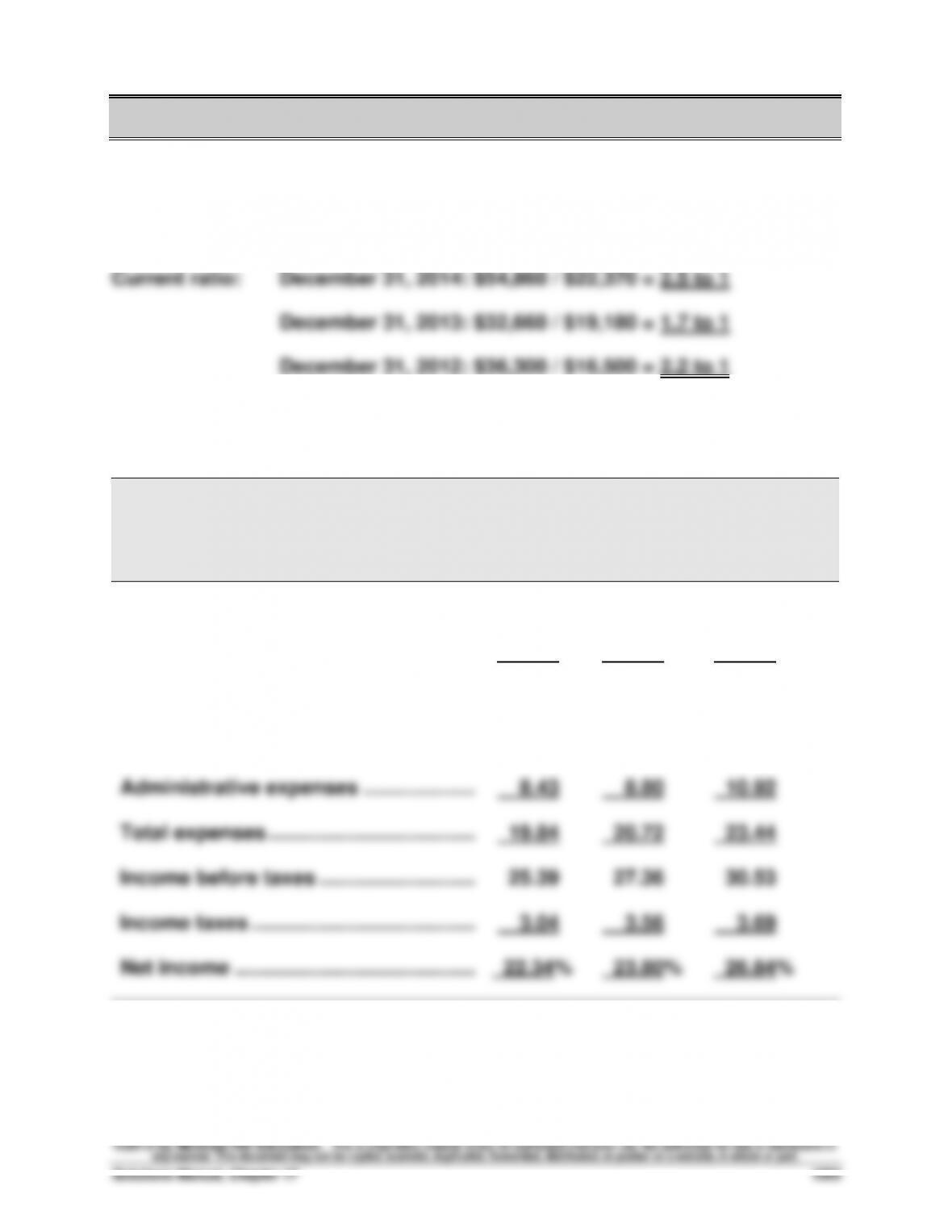

Current ratio: December 31, 2014: $52,390 / $22,800 = 2.3 to 1

Part 2

KORBIN COMPANY

Common-Size Comparative Income Statements

For Years Ended December 31, 2014, 2013, and 2012

2014

2013

2012

Sales ……………………………………………………

100.00%

100.00%

100.00%

Cost of goods sold …………………………..

51.08

62.50

55.36

Gross profit …………………………………………

48.92

37.50

44.64

Selling expenses …………………………….……

18.54

13.80

18.27

Administrative expenses ………………..……

9.13

8.80

8.20

Total expenses ……………………………….……

27.67

22.60

26.47

Income before taxes ……………………….….

21.25

14.90

18.17

Income taxes ………………………………….……

7.35

3.05

5.64

Net income …………………………………….……

13.90%

11.85%

12.53%

Problem 17-1A (Concluded)

Part 3

KORBIN COMPANY

Balance Sheet Data in Trend Percents

December 31, 2014, 2013, and 2012

2014

2013

2012

Assets

Current assets …………………………….

101.24%

73.29%

100.00%

Long-term investments ……………….

0.00

12.66

100.00

Plant assets, net………………………….

166.67

160.00

100.00

Total assets ………………………………..

131.71

116.19

100.00

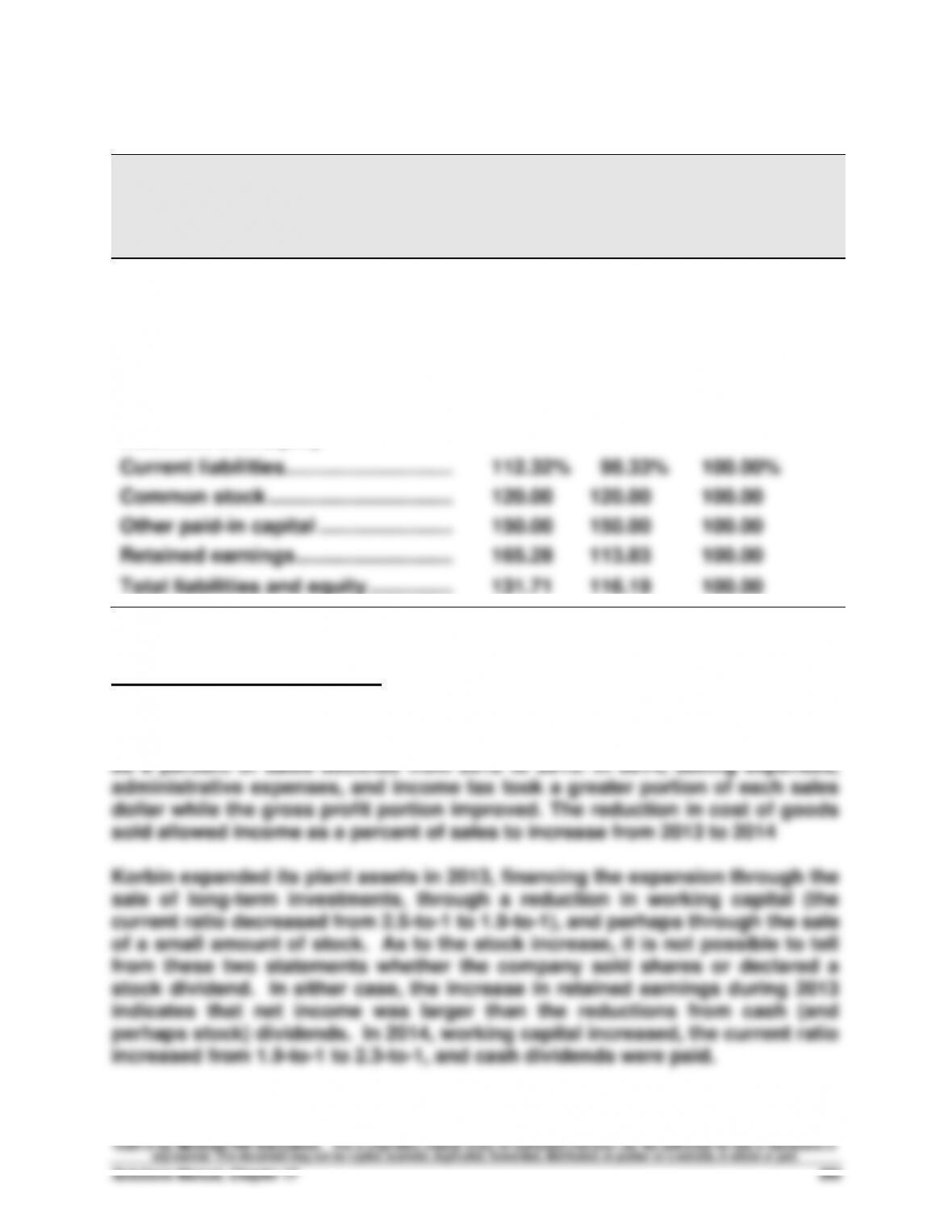

Liabilities and Equity

Current liabilities…………………………

112.32%

98.33%

100.00%

Common stock …………………………...

120.00

120.00

100.00

Other paid-in capital ……………………

150.00

150.00

100.00

Retained earnings ……………………….

165.28

113.83

100.00

Total liabilities and equity ……………

131.71

116.19

100.00

Part 4

Significant relations revealed

Korbin’s selling expenses and income taxes consumed smaller portions of

each sales dollar in 2013 than 2012. However, cost of goods sold and

administrative expenses consumed a larger portion in 2013. Therefore, income

Problem 17-2A (120 minutes)

Part 1

HAROUN COMPANY

Income Statement Trends

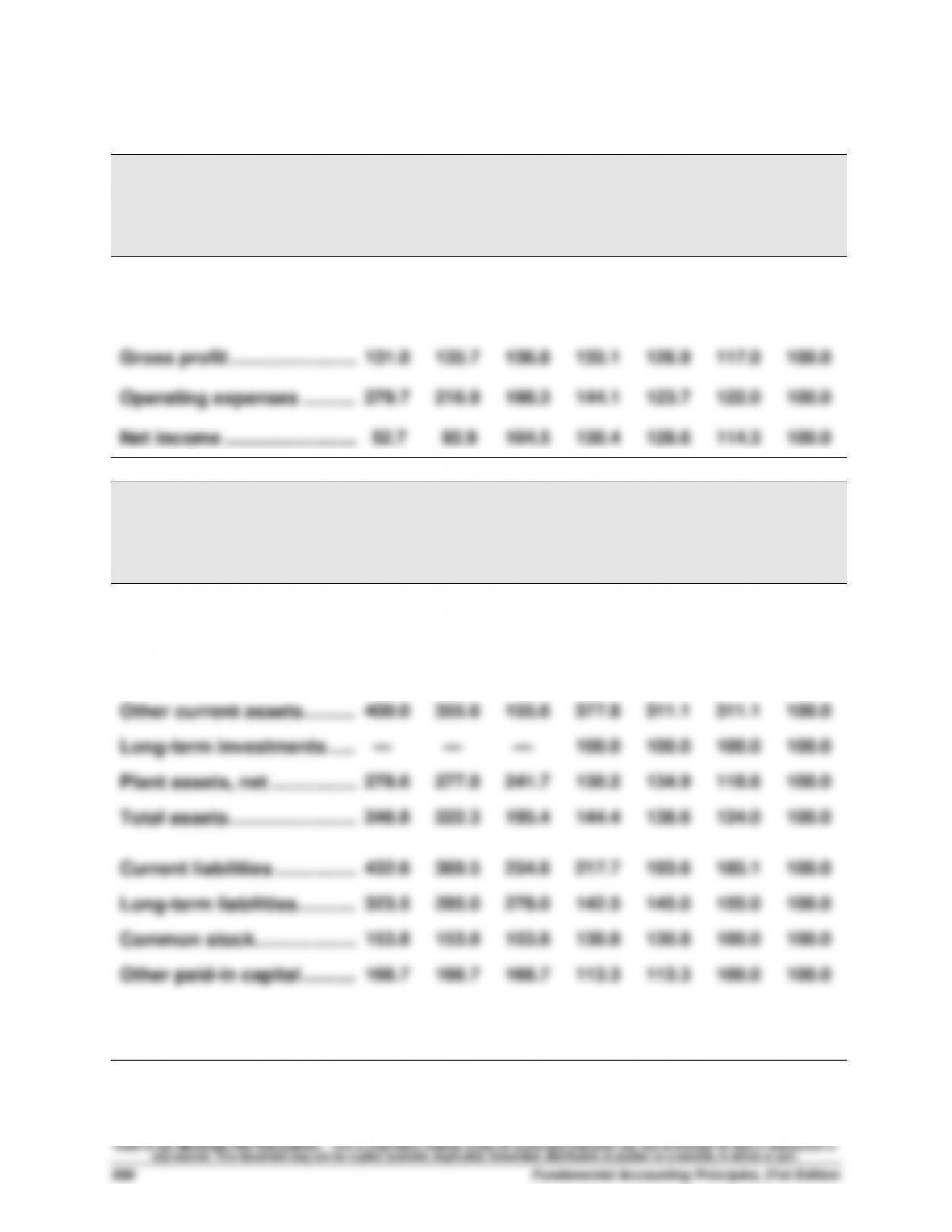

For Years Ended December 31, 2014-2008

2014

2013

2012

2011

2010

2009

2008

Sales ……………………………….

182.5%

161.2%

147.6%

136.2%

127.8%

119.6%

100.0%

Cost of goods sold …………..

212.6

176.1

153.9

136.9

128.3

121.2

100.0

Gross profit ……………………..

131.0

135.7

136.8

135.1

126.9

117.0

100.0

Operating expenses ………...

279.7

216.9

198.3

144.1

123.7

122.0

100.0

Net income ……………………...

52.7

92.9

104.5

130.4

128.6

114.3

100.0

HAROUN COMPANY

Balance Sheet Trends

December 31, 2014-2008

2014

2013

2012

2011

2010

2009

2008

Cash ………………………………..

65.2%

87.6%

92.1%

94.4%

98.9%

96.6%

100.0%

Accounts recble., net ……….

226.9

238.0

215.7

166.7

147.2

139.8

100.0

Merchandise inventory ……..

298.9

221.8

195.8

167.8

152.2

131.7

100.0

Other current assets ………...

400.0

355.6

155.6

377.8

311.1

311.1

100.0

Long-term investments …….

—

—

—

100.0

100.0

100.0

100.0

Plant assets, net ……………...

278.6

277.8

241.7

130.2

134.9

118.6

100.0

Total assets ……………………..

246.8

222.3

195.4

144.4

138.6

124.0

100.0

Current liabilities ……………..

432.6

369.5

254.6

217.7

193.6

185.1

100.0

Long-term liabilities ………….

323.5

285.0

278.0

142.5

145.0

155.0

100.0

Common stock ………………...

153.8

153.8

153.8

130.8

130.8

100.0

100.0

Other paid-in capital ………...

166.7

166.7

166.7

113.3

113.3

100.0

100.0

Retained earnings…………….

213.2

179.2

137.7

124.5

109.4

91.2

100.0

Total liabilities & equity …….

246.8

222.3

195.4

144.4

138.6

124.0

100.0

Problem 17-2A (concluded)

Part 2

Analysis and Interpretation

• The statements and the trend percent data indicate that the company

significantly expanded its plant assets in 2012. Prior to that time, the

company enjoyed increasing gross profit and net income.

assets to generate income.

• The short-term liquidity of the company continued to decline. Accounts

receivable did not change significantly for the period of 2012 to 2014,

but cash steadily declined and inventory sharply increased as did

current liabilities.

Fundamental Accounting Principles, 21st Edition

998

Problem 17-3A (60 minutes)

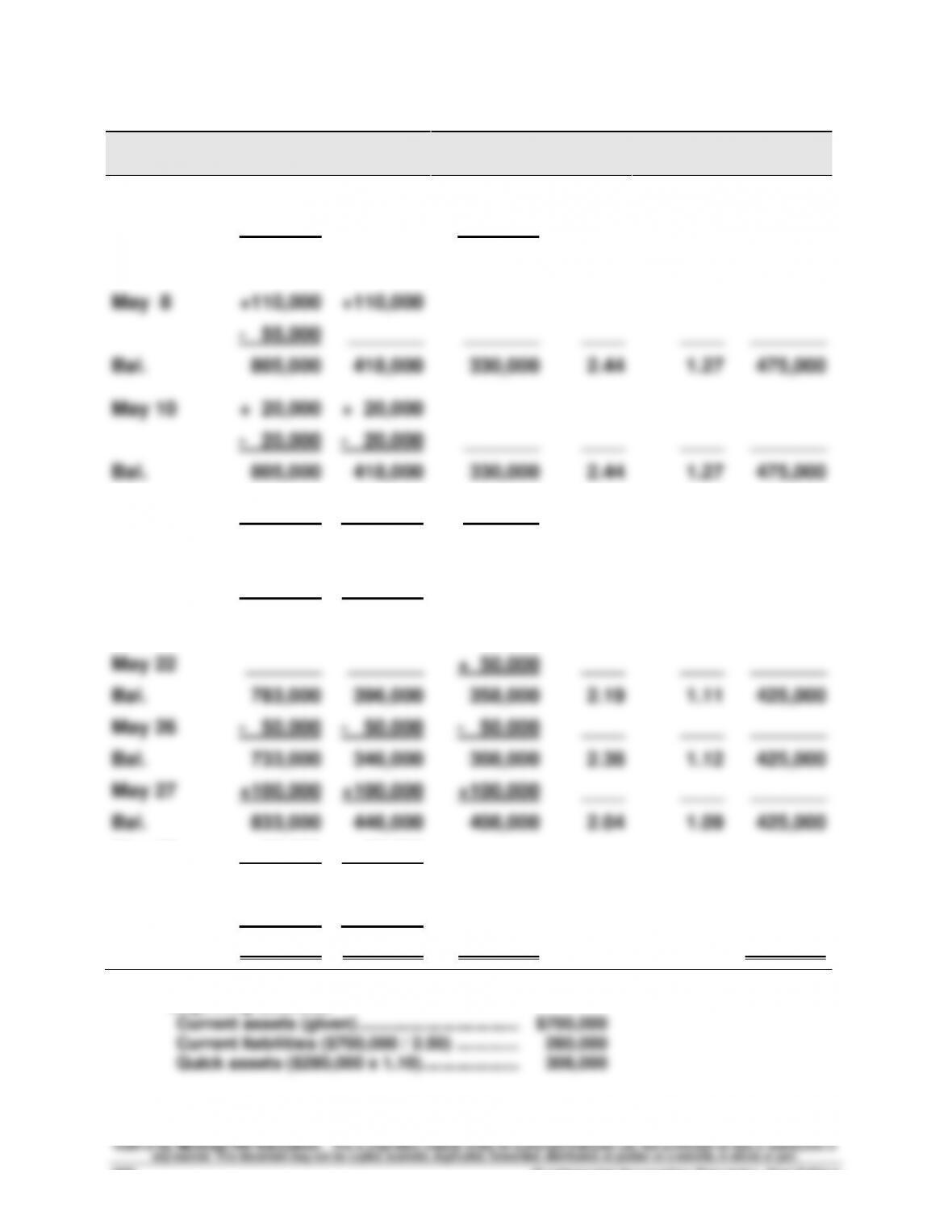

Trans-

action

Current

Assets

Quick

Assets

Current

Liabilities

Current

Ratio

Acid-Test

Ratio

Working

Capital

Beginning*

$700,000

$308,000

$280,000

2.50

1.10

$420,000

May 2

+ 50,000

_______

+ 50,000

____

____

_______

Bal.

750,000

308,000

330,000

2.27

0.93

420,000

May 8

+110,000

+110,000

– 55,000

_______

_______

____

____

_______

Bal.

805,000

418,000

330,000

2.44

1.27

475,000

May 10

+ 20,000

+ 20,000

– 20,000

– 20,000

_______

____

____

_______

Bal.

805,000

418,000

330,000

2.44

1.27

475,000

May 15

– 22,000

– 22,000

– 22,000

____

____

_______

Bal.

783,000

396,000

308,000

2.54

1.29

475,000

May 17

+0

+0

_______

____

____

_______

Bal.

783,000

396,000

308,000

2.54

1.29

475,000

May 22

_______

_______

+ 50,000

____

____

_______

Bal.

783,000

396,000

358,000

2.19

1.11

425,000

May 26

– 50,000

– 50,000

– 50,000

____

____

_______

Bal.

733,000

346,000

308,000

2.38

1.12

425,000

May 27

+100,000

+100,000

+100,000

____

____

_______

Bal.

833,000

446,000

408,000

2.04

1.09

425,000

May 28

+ 80,000

+ 80,000

________

____

____

_______

Bal.

913,000

526,000

408,000

2.24

1.29

505,000

May 29

– 180,000

– 180,000

________

____

____

_______

Bal.

$733,000

$346,000

$408,000

1.80

0.85

$325,000

*Beginning balances

Current assets (given) ……………………………………..

$700,000

Current liabilities ($700,000 / 2.50) ………….………..

280,000

Quick assets ($280,000 x 1.10) ………………..………..

308,000

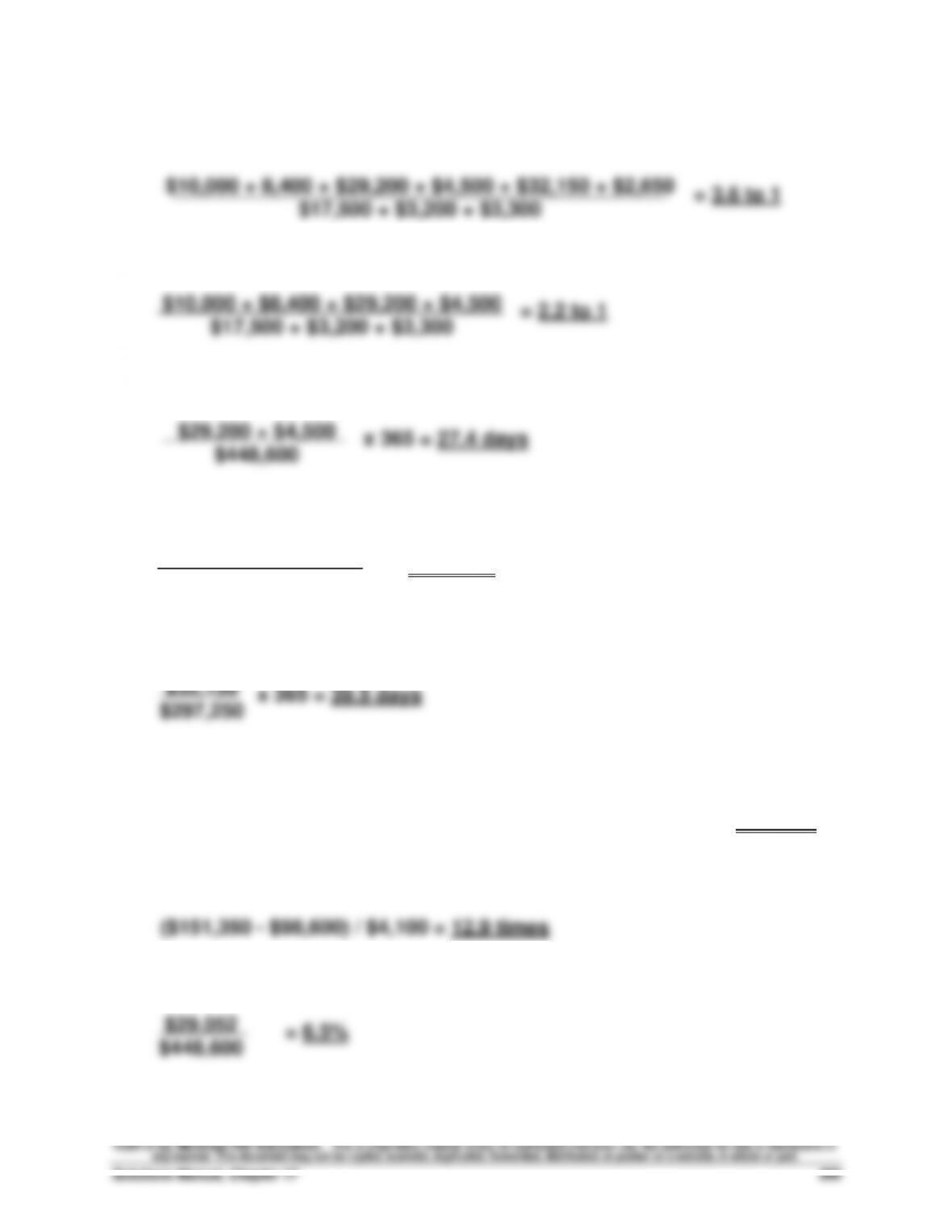

Problem 17-4A (50 minutes)

1. Current ratio

2. Acid-test ratio

3. Days’ sales uncollected

4. Inventory turnover

= 7.3 times

5. Days’ sales in inventory

6. Debt–to-equity ratio

($17,500 + $3,200 + $3,300 + $63,400) / ($90,000 + $62,800) = 0.57 to 1

7. Times interest earned

8. Profit margin ratio

$17,500 + $3,200 + $3,300

$297,250

($48,900 + $32,150)/2

$32,150

Problem 17-4A (Concluded)

9. Total asset turnover

10. Return on total assets

11. Return on common stockholders’ equity

Problem 17-5A (60 minutes)

Part 1

Barco Company

Kyan Company

a. Current ratio

= 2.5 to 1

= 2.6 to 1

* $19,500 + $37,400 + $9,100 + $84,440 + $5,000 = $155,440

**$34,000 + $57,400 + $7,200 + $132,500 + $6,950 = $238,050

b. Acid-test ratio

= 1.1 to 1

= 1.1 to 1

**$34,000 + $57,400 + $ 7,200 = $98,600

c. Accounts receivable turnover

= 20.2 times = 14.8 times

d. Inventory turnover

e. Days’ sales in inventory

f. Days’ sales uncollected

Short-term credit risk analysis: Barco and Kyan have essentially equal

$770,000

($37,400 + $9,100 + $29,800)/2

$585,100

$880,200

($57,400 + $7,200 + $54,200)/2

$155,440*

$61,340

$66,000*

$61,340

$238,050**

$93,300

$98,600**

$93,300

$632,500

Problem 17-5A (Concluded)

Part 2

Barco Company

Kyan Company

a. Profit margin ratio

b. Total asset turnover

c. Return on total assets

= 38.5% = 45.5%

d. Return on common stockholders’ equity

e. Price-earnings ratio

f. Dividend yield

= 5.1% = 5.1%

Investment analysis: Kyan’s profit margin ratio, total asset turnover, return on

$162,200

$770,000

($445,440 + $398,000)/2

$162,200

($445,440 + $398,000)/2

$3.80

$75

$210,400

$880,200

($542,450 + $382,500)/2

$210,400

($542,450 + $382,500)/2

$3.80

$75

Problem 17-6AA (60 minutes)

Part 1

Effect of income taxes (debits or losses in parentheses)

Pretax

30% Tax

Effect

After-Tax

i. Loss from operating a discontinued segment …………..

(18,250)

(5,475)

(12,775)

j. Gain on insurance recovery of tornado damage …...

29,120

8,736

20,384

m. Correction of overstatement of prior year’s sales ……..

(16,000)

(4,800)

(11,200)

n. Gain on sale of discontinued segment’s assets ………..

34,000

10,200

23,800

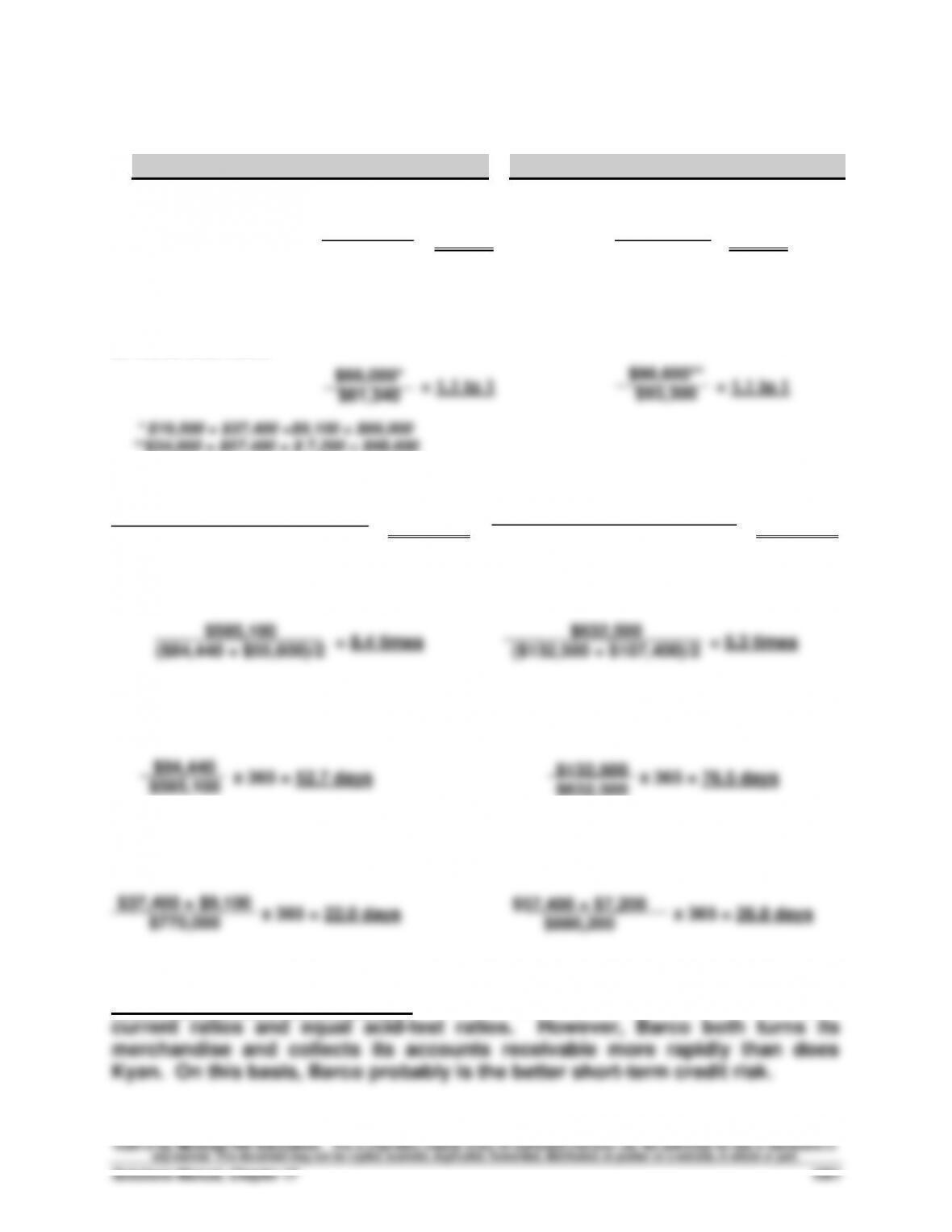

Part 2 Income from continuing operations (and its components)

k.

Net sales ………………………………………………………...

$ 998,500

a.

Interest revenue ……………………………………………...

14,000

g.

Gain from settling lawsuit ………………………………..

44,000

Total revenues and gains ………………………………..

1,056,500

q.

Cost of goods sold ………………………………………….

$482,500

b.

Depreciation expense—Equipment ………………….

34,000

l.

Depreciation expense—Buildings …………………...

52,000

e.

Other operating expenses ……………………………….

106,400

c.

Loss on sale of equipment ……………………………...

25,850

o.

Loss from settling lawsuit …………………………..…..

23,750

Total expenses ………………………………………………..

(724,500)

Income from continuing operations before taxes …..

332,000

p.

Income taxes expense (30%) …………………………..

(99,600)

Income from continuing operations after taxes ……..

$ 232,400

Fundamental Accounting Principles, 21st Edition

1004

Problem 17-6AA (Concluded)

Part 3 Income from discontinued segment

i.

Loss from operating a discontinued

segment (after-tax) …………………………………………………….…

$ (12,775)

n.

Gain on sale of discontinued segment’s

assets (after-tax) ……………………………………………………….

23,800

Income from discontinued segment ……………………………..…………………..

$ 11,025

Part 4 Income before extraordinary items

Income from continuing oper. after taxes (from Part 2) …………………………..

$232,400

Income from discontinued segment (from Part 3) …………………………..

11,025

Income before extraordinary items ……………………………….…………………..

$243,425

Part 5 Net income

Income before extraordinary items ……………………………….…………………..

$243,425

j.

Extraordinary item

Gain on insurance recovery of tornado damage

(after-tax) ……………………………………………………………..…………………..

20,384

Net income …………………………………………………………………..……………….

$263,809

PROBLEM SET B

Problem 17-1B (60 minutes)

Part 1

Part 2

BLUEGRASS CORPORATION

Common-Size Comparative Income Statements

For Years Ended December 31, 2014, 2013, and 2012

2014

2013

2012

Sales ……………………………………………………

100.00%

100.00%

100.00%

Cost of goods sold …………………………..

54.77

51.91

46.04

Gross profit …………………………………………

45.23

48.09

53.96

Selling expenses …………………………….……

11.41

11.92

12.52

Administrative expenses ………………..……

8.43

8.80

10.92

Total expenses ……………………………….……

19.84

20.72

23.44

Income before taxes ……………………….….

25.39

27.36

30.53

Income taxes ………………………………….……

3.04

3.56

3.69

Net income …………………………………….……

22.34%

23.80%

26.84%

* Some totals do not reconcile due to rounding.

Problem 17-1B (Concluded)

Part 3

BLUEGRASS CORPORATION

Balance Sheet Data in Trend Percents

December 31, 2014, 2013, and 2012

2014

2013

2012

Assets

Current assets ………………………………..……

151.13%

89.97%

100.00%

Long-term investments …………………..……

0.00

16.04

100.00

Plant assets …………………………………………

142.80

143.87

100.00

Total assets …………………………………………

133.18

117.57

100.00

Liabilities and Equity

Current liabilities…………………………….……

135.58%

116.24%

100.00%

Common stock ……………………………….……

125.68

125.68

100.00

Other paid in capital ……………………….….

122.57

122.57

100.00

Retained earnings …………………………..

139.03

112.09

100.00

Total liabilities and equity ……………….……

133.18

117.57

100.00

Part 4

Significant relations revealed

Bluegrass’s cost of goods sold took a larger percent of sales each year.

Selling and administrative expenses and income taxes took a somewhat

smaller portion each year, but not enough to offset the effect of cost of