Problem 25-5B (55 minutes)

Part 1

Product R

Product T

Selling price per unit ……………………………………………..

$ 60

$ 80

Variable costs per unit …………………………………………..

20

45

Contribution margin per unit ………………………………....

$ 40

$ 35

Machine hours to produce 1 unit …………………………..

0.4

1.0

Contribution per machine hour

(or contribution/[hours per unit]) ………………………...

$100

$ 35

Part 2

Sales Mix Recommendation To the extent allowed by production and

market constraints, the company should produce as much of Product R as

possible. With a single shift yielding 176 hours per month (8 x 22), the

company can produce these units of Product R:

Contribution Margin at Recommended Sales Mix

Problem 25-5B (Continued)

Part 3

Sales Mix Recommendation with Second Shift If the second shift is added,

the maximum possible output of R will double:

However, this level of output exceeds the company’s market constraint of

550 units of Product R per month. This means the company should

produce 550 units of Product R, and commit the remainder of the

productive capacity to Product T. This is computed as follows:

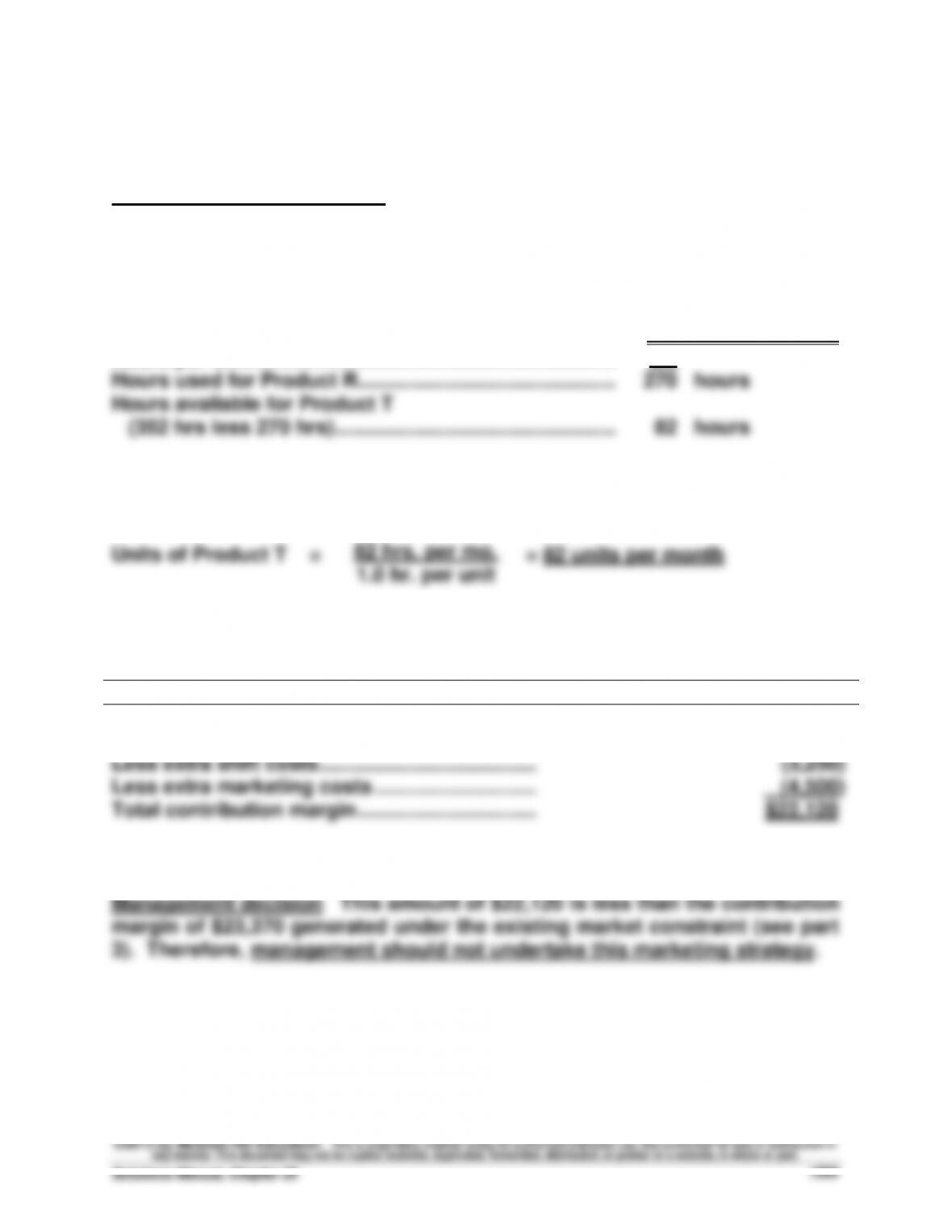

Units of Product R …………………………………………………...

= 550 units per month

Hours per unit ………………………………………………………....

0.4

Hours used for Product R ………………………………………...

220

hours

Hours available for Product T (352 hrs – 220 hrs) …………………....

132

hours

The output of Product T with 132 production hours is

1.0 hrs. per unit

Contribution Margin at This Sales Mix

Units

Contr./unit

Total

From R ……………………………………………………….

550

$40

$22,000

From T ……………………………………………………….

132

35

4,620

Less extra shift costs ……………………………………

(3,250)

Total contribution margin …………………………..

$23,370

Management decision This amount of $23,370 exceeds the contribution

0.4 hrs. per unit

Problem 25-5B (Continued)

Part 4

Sales Mix Recommendation By incurring additional marketing cost, the

company can relax the market constraint for sales of Product R up to the

point where 675 units can be sold. This means the company can produce

675 units of Product R, and commit the remainder of its productive

capacity to Product T. These computations are:

Units of Product R …………………………………………………...

= 675 units per month

Hours per unit ………………………………………………………....

0.4

Hours used for Product R ………………………………………...

270

hours

Hours available for Product T

(352 hrs less 270 hrs) …………………………………………....

82

hours

The output of Product T with 82 production hours is

Contribution Margin with This Sales Mix

Units

Contr./unit

Total

From R ……………………………………………………….

675

$40

$27,000

From T ……………………………………………………….

82

35

2,870

Less extra shift costs ……………………………………

(3,250)

Less extra marketing costs ………………………..…

(4,500)

Total contribution margin …………………………..

$22,120

Fundamental Accounting Principles, 21st Edition

1510

Problem 25-6B (60 minutes)

Part 1

ESME COMPANY

Analysis of Expenses under Elimination of Department Z

Total

Eliminated

Continuing

Expenses

Expenses

Expenses

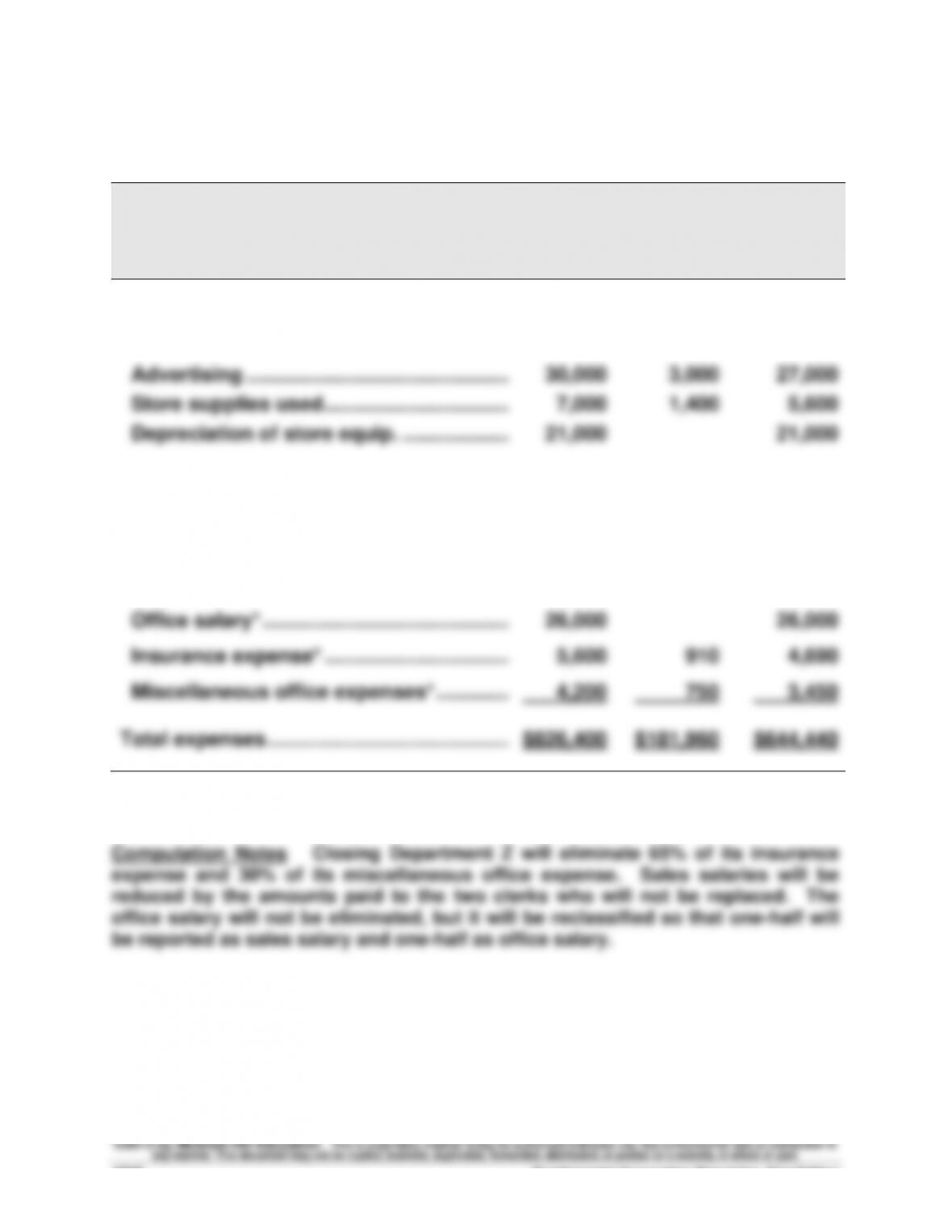

Cost of goods sold ……………………………….………

$586,400

$125,100

$461,300

Direct expenses

Advertising …………………………………………………

30,000

3,000

27,000

Store supplies used …………………………….………

7,000

1,400

5,600

Depreciation of store equip. ………………..………

21,000

21,000

Allocated expenses

Sales salaries* …………………………………….………

93,600

46,800

46,800

Rent expense………………………………………………

27,600

27,600

Bad debts expense ……………………………..………

25,000

4,000

21,000

Office salary* ………………………………………………

26,000

26,000

Insurance expense* …………………………….………

5,600

910

4,690

Miscellaneous office expenses* …………..………

4,200

750

3,450

Total expenses ……………………………………..………

$826,400

$181,960

$644,440

Problem 25-6B (Continued)

Part 2

ESME COMPANY

Forecasted Annual Income Statement

Under Plan to Eliminate Department Z

Sales ………………………………………………………………………………………...

$700,000

Cost of goods sold …………………………………………………………………...

461,300

Gross profit from sales ……………………………………………………………..

238,700

Operating expenses

Advertising ……………………………………………………………………………..

27,000

Store supplies used ………………………………………………………………..

5,600

Depreciation of store equipment ……………………………………………..

21,000

Sales salaries ………………………………………………………………………….

59,800*

Rent expense ………………………………………………………………………….

27,600

Bad debts expense ………………………………………………………………….

21,000

Office salary …………………………………………………………………………...

13,000*

Insurance expense ………………………………………………………………….

4,690

Miscellaneous office expenses ………………………………………………..

3,450

Total operating expenses ………………………………………………………….

183,140

Net income ………………………………………………………………………………..

$ 55,560

* Office salary reassignment

Total

Sales

Office

Salaries

Salaries

Salary

Sales clerks ……………………………………….………………

$46,800

$46,800

Office clerk ………………………………………..……………..

26,000

$26,000

Reassign office clerk to sales ……………..……………

0

13,000

(13,000)

Revised salaries……………………………………………………….

$72,800

$59,800

$13,000

Fundamental Accounting Principles, 21st Edition

1512

Problem 25-6B (Continued)

Part 3

ESME COMPANY

Reconciliation of Combined Income with Forecasted Income

Combined net income …………………………………………………………………

$ 48,600

Less Dept. Z’s lost sales ………………………………………………………………

(175,000)

Plus Dept. Z’s eliminated expenses ………………………………………………

181,960

Forecasted net income …………………………………………………………………

$ 55,560

ANALYSIS

Department Z’s avoidable expenses of $181,960 are $6,960 greater than its

SERIAL PROBLEM — SP 25

Serial Problem, Success Systems (50 minutes)

COMPUTING NET CASH FLOWS FROM NET INCOME

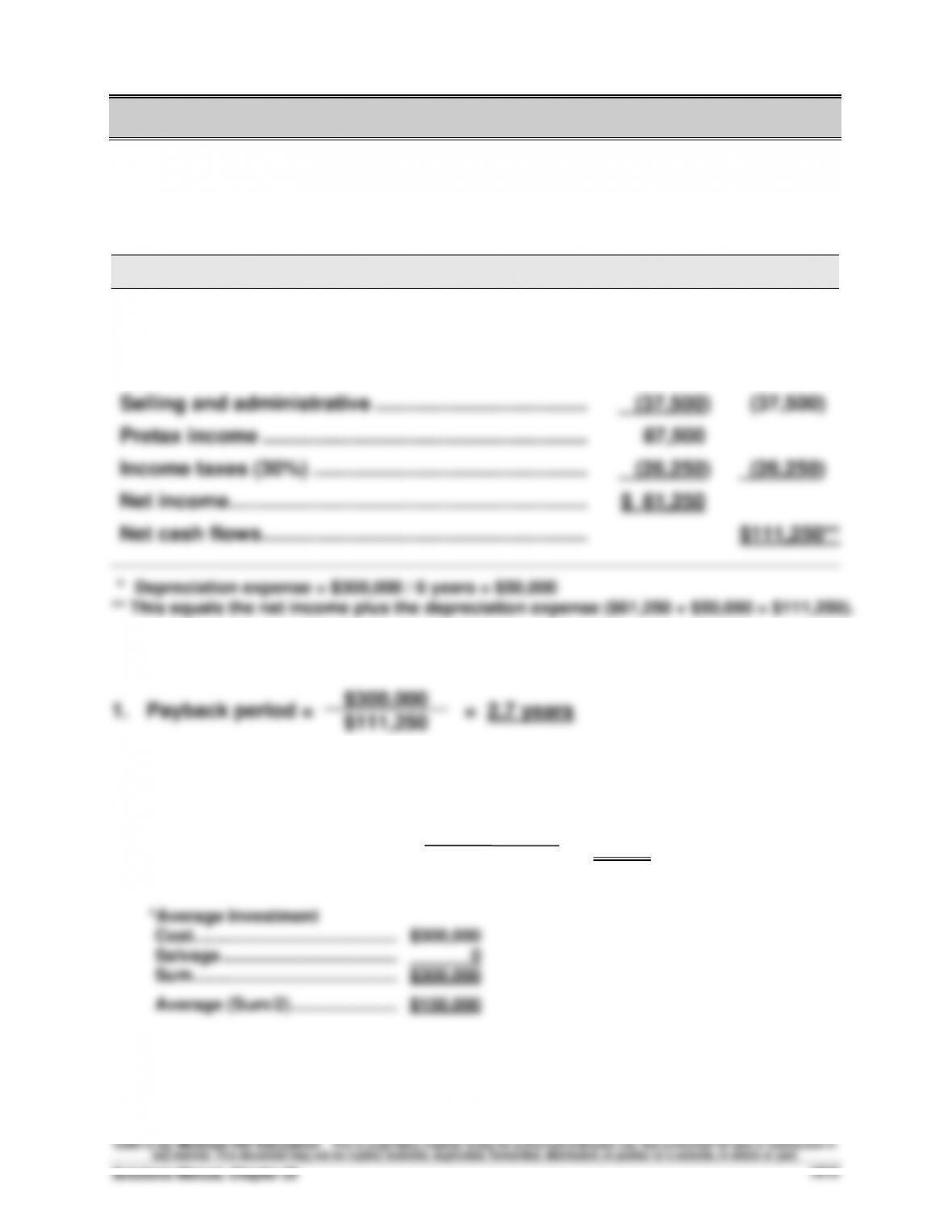

Net income

Cash flows

Sales ………………………………………………………………..……

$375,000

$375,000

Materials, labor & overhead ……………………………………

(200,000)

(200,000)

Depreciation* ……………………………………………………….

(50,000)

Selling and administrative ………………………………..……

(37,500)

(37,500)

Pretax income ………………………………………………….……

87,500

Income taxes (30%) ………………………………………….……

(26,250)

(26,250)

Net income ……………………………………………………….

$ 61,250

Net cash flows ………………………………………………….……

$111,250**

* Depreciation expense = $300,000 / 6 years = $50,000

** This equals the net income plus the depreciation expense ($61,250 + $50,000 = $111,250).

2. Accounting rate of return = = 40.8%

$111,250

$61,250

$150,000*

Reporting in Action — BTN 25-1

1. The internal rate of return (given here as 10%) is the rate which yields a

net present value of zero for an investment. The annuity factor for 10

periods and a discount rate of 10% is 6.1446. This means we can solve

for the amount of annual cash flows as follows:

of $345,018.39 per year for 10 years.

2. Answer depends on the information obtained.

Comparative Analysis — BTN 25-2

1. Answer depends on the newspaper selected and its price for advertising

2. If we assume that the average product of Polaris and Arctic Cat sells for

around $12,000, then the contribution margin per product is about

$2,400 (using the 20% stated assumption in the problem). This would

3.

MEMORANDUM

TO:

FROM:

DATE:

SUBJECT:

Primary points for discussion of the importance of effective

advertising:

(a) Students need to recognize that advertising is very expensive

and crucial to most merchandisers.

(b) The students should also recognize that an advertisement

must be effective to justify its cost and the related product mix

decision of managers.

(c) In most cases the advertisement must generate several

thousand dollars in sales to pay for the advertisement.

Ethics Challenge — BTN 25-3

1. Present value of $100 to be received in 10 years assuming a 12%

discount rate is approximately $32. This is computed as $100 x 0.322.

2. We need to be concerned about any project with expected long-term

cash inflows. This is especially the case if the larger cash inflows are

Communicating in Practice — BTN 25-4

Instructor note: Answers will vary, but responses should address the questions

asked and include some discussion of the following points for each method.

Payback Period

Accounting Rate

of Return

Net Present

Value

Internal Rate

of Return

Measurement

basis

• Cash flows

• Accrual income

• Cash flows

• Profitability

• Cash flows

• Profitability

Measurement

unit

• Periods

• Percent

• Dollars

• Percent

Strengths

• Easy to

understand

• Allows

comparison of

projects

• Easy to

understand

• Allows

comparison of

projects

• Reflects

time value

of money

• Reflects

different

risk levels

over

project’s life

• Reflects

time value

of money

• Allows

compari-

sons of

dissimilar

projects

Limitations

• Ignores time

value of money

• Ignores cash

flows after

payback period

• Ignores time

value of

money

• Ignores annual

rates over life

of project

• Difficult to

compare

dissimilar

projects

• Ignores

varying

risk levels

over life of

project

Taking It to the Net — BTN 25-5

1. According to Bizbrim, the business processes typically outsourced are

2. Companies who are outsourcing their business processes are able to

Teamwork in Action — BTN 25-6

Instructor note: Answers will vary across students. Yet the examples, while

different, should capture similar qualitative factors.

SAMPLE SOLUTION

Qualitative Factors

• Competition has a new, more efficient and effective system.

• Need to replace old system.

Entrepreneurial Decision — BTN 25-7

1. Charlie could use payback period, accounting rate of return, net present

2. For these tools, Charlie needs estimates of how much the bakery and

warehousing center will cost, both upfront and for recurring (e.g.

3.

Payback Period

Accounting Rate

of Return

Net Present

Value

Internal Rate

of Return

Advantages

• Easy to

understand

• Allows

comparison of

projects

• Easy to

understand

• Allows

comparison of

projects

• Reflects

time value

of money

• Reflects

different

risk levels

over

project’s life

• Reflects

time value

of money

• Allows

compari-

sons of

dissimilar

projects

Disadvantages

• Ignores time

value of money

• Ignores cash

flows after

payback period

• Ignores time

value of

money

• Ignores annual

rates over life

of project

• Difficult to

compare

dissimilar

projects

• Ignores

varying

risk levels

over life of

project

Hitting the Road — BTN 25-8

1. Answers will vary among students.

Sample Example

For illustrative purposes, one sample solution would appear as follows:

Lease terms—$400 per month for 35 months; plus $10,000 final

payment at the end of 35 months; 12% annual interest rate.

To compute the present value of the lease payments

PV of 35 payments of $400 per month discounted

at 1% (12%/12 months) …………………………………………………..…..

$11,763*

PV of $10,000 final payment at end of 35 months

discounted at 1% …………………………………………………………..……..

7,059**

Total PV of lease ……………………………………………………………………..

$18,822

* $400 x 29.4086 (from Table B.3)

** $10,000 x 0.7059 (from Table B.1)

Purchase terms—$16,500

2. In most cases the students will find it more costly to lease an

automobile than to purchase it outright. Also, getting the salesperson

Global Decision — BTN 25-9

There are probably several reasons why KTM would take on this project.

One reason is that the lower ongoing packaging costs can generate some